Morning … today’s note feels different and should be brief given the gravity of the moments just ahead (specifically, 846a, 903a, 937a and 1003a).

We’ll have some distractions like an interview with BOJs Ueda — his first interview since becoming BOJ Governor,

Nikkei: Japan's 10-year bond yield hits highest since 2014 on Ueda remark

… The long-term rate had hovered at 0.650% over the weekend. In an interview with the Yomiuri Shimbun dated Saturday, BOJ Gov. Kazuo Ueda expressed his belief that the lifting of the negative interest rate policy would be "an option if we could be confident about rising prices."

Attempt here to highlight on both daily AND WEEKLY basis, 3yy (not best FedFunds proxy but with auction today, a look at willingness to buy ahead of a September PAUSE and potential hike towards end of year…) that momentum remains overSOLD. This, in and of itself is NOT reason to buy (for 10 of those, see below) and note ‘end user demand’ (keep reading for more on that, too) has been robust.

Personally, I do NOT see the Fed as being DONE BUT … I am more than willing and able to consider idea that bonds are a ‘screaming buy’ and sympathetic to the idea an economic slowdown is coming (counter TO the notion put out there last week by FRB Chicago, all is well, and impacts in rear view mirror).

I also will admit a bit of an uncomfortable feeling as it would appear to be the CONsensus thinking — rates are to DROP — but that, in and of itself — should not dissuade anyone from their view.

I digress … the moments and hours ahead today are tougher for some than others and to one and all, we’ll remember and give thanks

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mostly lower with the curve pivoting steeper off a little changed 2-year benchmark after Japan's Ueda warned this weekend that the BOJ's negative rates policy could end if further progress to their 2% inflation target is made (link above). JGB 5yr yields closed +6.3bp, DXY is lower (-0.4%) while front WTI futures are too (-0.5%). Asian stocks were mixed, EU and UK share markets are all higher (SX5E and DAX up around +0.5%) while ES futures are showing +0.40% here at 6:50am. Our overnight US rates flows saw Treasuries dragged lower by the JGB market during Asian hours with the desk reporting mixed flows and uninspiring volumes despite the heave-ho in JGB's. The London desk also reported lethargic activity with steepeners still popular and systematic accounts fading the front-end ahead of today's up-sized 3-year sale. Overnight Treasury volume was about 80% of average overall with 3yrs (104%) seeing the only above-average turnover ahead of today's sale.

I can't remember a time when we've checked in daily on receipts posted by the US Department of Education to the Treasury. But it may be an important exercise this year and next to help determine the trajectory of household consumption patterns and, thus, the direction of travel for US growth. Our first attachment this morning shows DOE receipts through September 7th. The sharp upturn in receipts caught our eyes earlier, just as the very recent plunge in receipts has... Happily, the fine folks at Wrightson ICAP addressed the wild swings in their MMO this morning: "The spike at the end of last month may have been tied to the fact that regular interest accruals were due to kick in again on September 1. Anecdotally, a common piece of advice from financial planners was to delay loan payments as long as the COVID-era 0% interest rate was in effect, but to repay as much as possible when that rate-relief expired at the beginning of this month. The pattern of daily DOE cash receipts has been consistent with that advice: the series peaked at $1.042 billion on Friday, September 1 and remained above $800 million on the first two days of last week, but slid all the way to $279 million on Thursday, September 7. For now, our assumption for the rest of this month is that DOE receipts will average just slightly more than our original “steady-state” projection of $300 million a day from October onward." So what does all this mean for consumption and Thursday's August retail sales numbers? Well, Wrightson again has some thoughts on that: "Our original baseline assumed that the additional household cash absorbed by loan payment requirements would be equal to roughly 0.4% of PCE. Not all of that hit would flow through to spending, but much of it probably would. It is unclear, however, whether the surge in voluntary repayments in recent weeks would have had the same effect. To the extent that these were pre-planned financial adjustments rather than newly obligatory payments, they would be less likely to have a negative effect on discretionary spending." Regardless, the Bloomberg consensus does expect a step-back in retail sales this week (ex-autos and gas seen at -0.1% MoM after +1.0% in July). Interesting...

… and for some MORE of the news you can use » The Morning Hark - 11 Sept 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

I’d like to interrupt todays regularly scheduled programming to bring you this mornings TOP PRESS PICKS by IGM as I think it is a story which continues to develop and I feel as though it will be one with deep impact across all of global macro.

From some of the news to some of THE VIEWS you might be able to use … In addition TO what was noted over the weekend, here’s SOME of what Global Wall St is sayin’ …

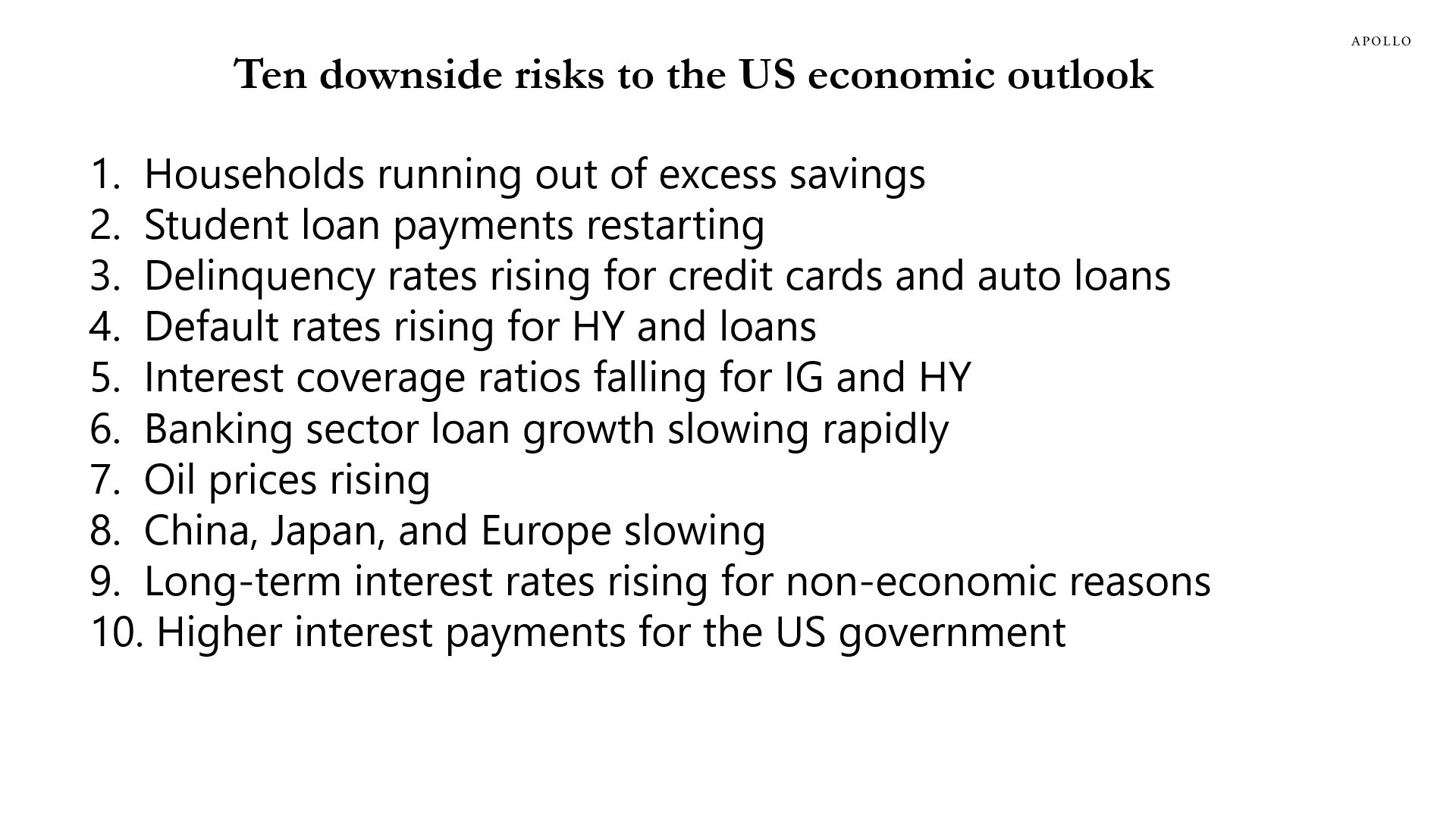

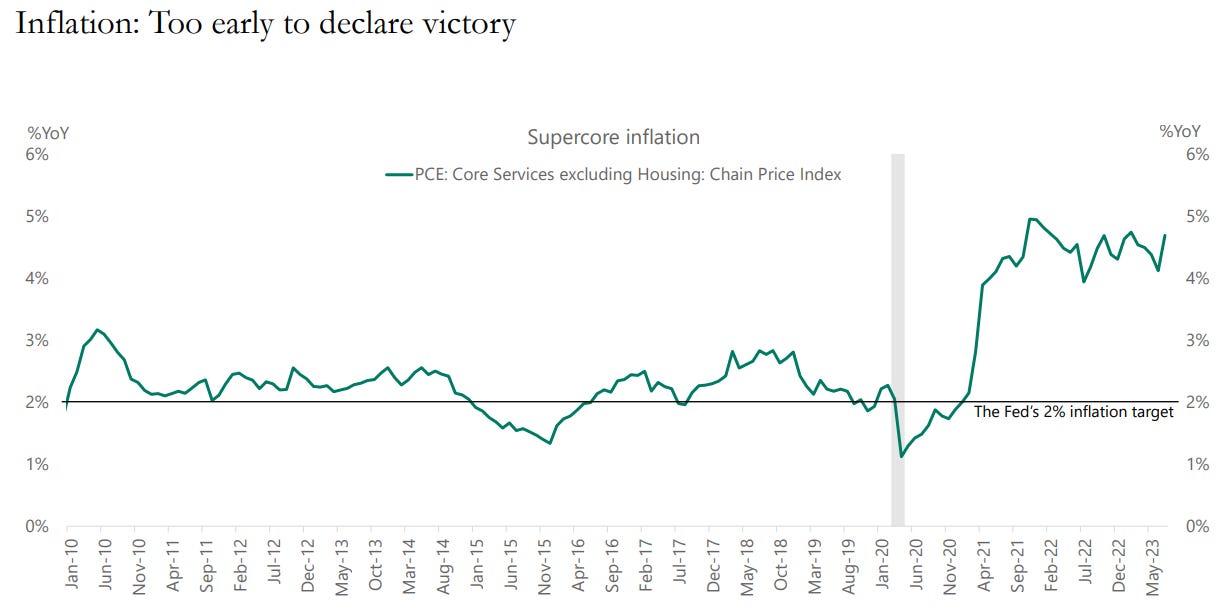

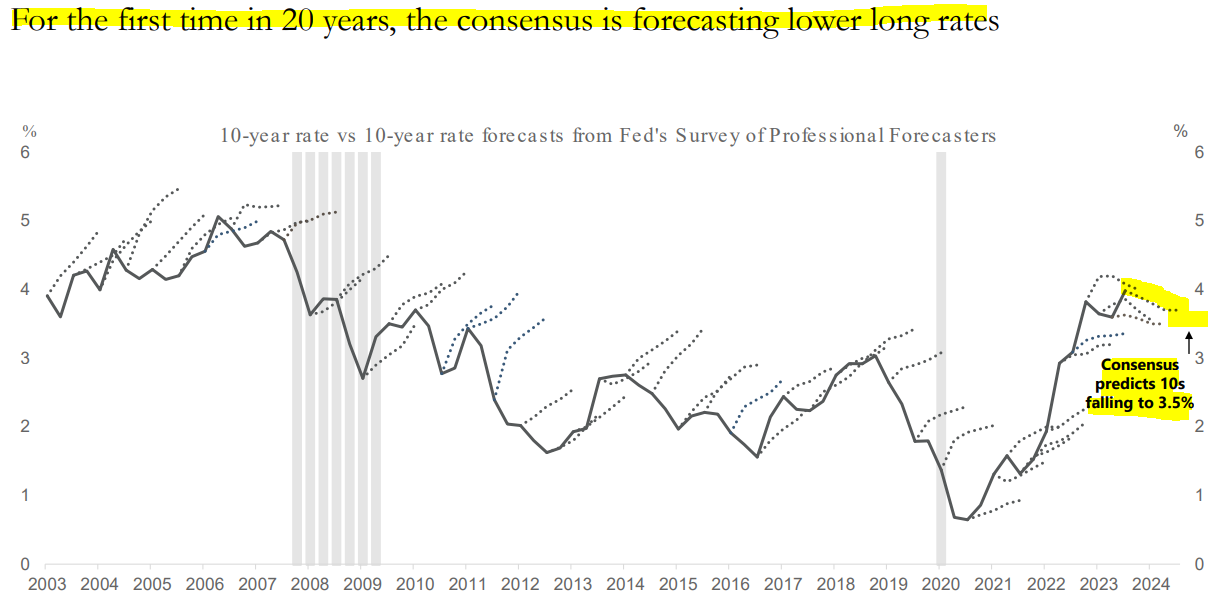

Apollo - Outlook for Public and Private Markets (really a laundry list of top 10 things which are RISKS TO Team soft / NO landing … ultimately then leaning IN to the idea 10s a ‘screaming buy’ and note the link TO monthly outlook does appear clickable … very first visual of supercore ‘flation sorta stops ya in yer tracks … as does the CONsensus view on 10yy and his very last slide — with what HE thinks and what to do ‘bout it…)

Our monthly outlook for public and private markets is available here.

Fed hikes continue to push delinquency rates higher on credit cards and auto loans.

Also, Fed hikes continue to push higher default rates for HY and loans. And interest coverage ratios are moving down for both IG and HY.

The bottom line is that higher interest rates are biting harder and harder on consumers and firms, and the Fed’s ongoing efforts to cool down the economy will continue. There are more downside risks than upside risks to markets, see overview below.

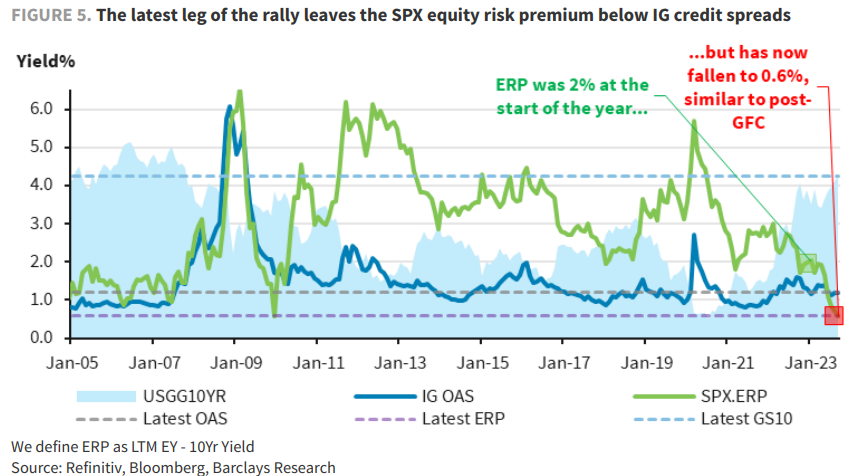

The equity risk premium falling below IG credit spreads leads us to revisit what exactly is being priced in. Even without the influence of lofty Tech valuations, low risk premia for the rest of the S&P 500 suggest excessive optimism around a strong earnings rebound. We see little room for further multiple expansion.

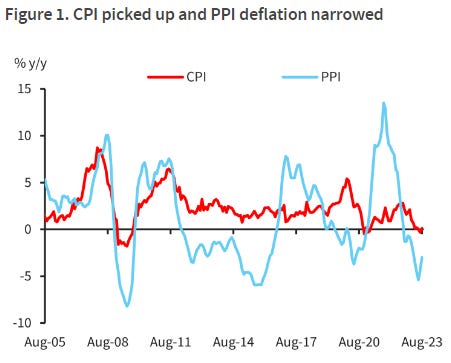

August CPI rose after a 0.3% drop in July, and PPI deflation narrowed for a second month. We think the inflation prints have probably passed their recent troughs, while sluggish CPI and contracting PPI, along with weak trade and property-sales data, suggested demand remained weak. We see more cuts to RRR and policy rates.

BNP - Sunday Tea with BNPP: Priced for exceptionalism (what could POSSIBLY go wrong … see 10 things just above, perhaps, to start?)

KEY MESSAGES

The dual market themes of US exceptionalism and increased debt supply have carried through the unofficial end of summer.

We think we’re in the zone of peak US yields, though cyclical catalysts are needed to drive a more material turn towards lower yields; our near-term preference is to buy on dips and to position for US/EUR yield convergence.

Despite its success, we think carry has more room to run in FX, though a range of factors argue for a defensive approach.

… With consensus growth expectations having reset higher alongside waning recession fears, the bar for the fundamental side to continue to outperform is now decidedly higher. On the technical side, the overall (higher) yield backdrop appears to be supporting appetite for all of the supply.

The upcoming UST auctions (3s, 10s, 30s in the week ahead) will be another useful checkpoint, but measures of end user demand for Treasury issuance have been solid so far (Figure 2). Additionally, the wave of IG supply has been met with healthy support, resulting in a relatively modest impact to spreads. Our near-term bias is that US yields should start to settle into somewhat of a range, arguing for more of a “buy on dips” mentality rather than a desire to lean fully into received positions just yet.

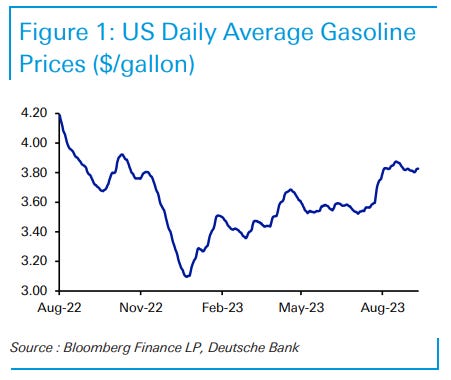

DB - Mapping Markets: The Q4 narrative shift - is stagflation set to return? (gasoline. lives. matter)

Over the past year, an important factor behind lower inflation has been a noticeable decline in commodity prices, with energy commodities like oil and gas prices seeing steep declines. These have heavily pushed down the year-on-year CPI numbers. For instance, US energy CPI in July was down -12.5% on a year-on-year basis, whilst Euro Area energy CPI was down -3.3% in the August flash print.

But over the last couple of months that decline in energy prices has stabilised, and several commodities have posted sharp increases. One example is Brent crude oil prices, which are now above $90/bbl for the first time since November. In turn, that’s begun to pass through to consumers, with a sharp uptick in gasoline/petrol prices across the developed world, as Figures 1 and 2 below show.

This pickup in energy costs is going to feed through to the upcoming inflation figures. That’s already been reflected in near-term market pricing, with inflation swaps for tomorrow’s US August CPI print pricing in a +0.63% reading. If realised, that would be the strongest monthly print since June 2022. Meanwhile, in the Euro Area, headline CPI remained at +5.3% in August, above consensus expectations for a move lower to +5.1%. Likewise in the UK, our economist is also expecting the August CPI print to show an uptick in inflation…

… One prominent theme of Q2 earnings season was a newfound concern about the health of the lower-income consumer, due to rising delinquency rates. To track these developments, we aggregate same-store sales data from 26 retailers representing $1tn of annual spending. Perhaps surprisingly, we find the lower-income consumer is outperforming, with our measure of same-store sales rising 5.6% year-on-year for the 10 retailers whose stores are generally located in lower-income zip codes. Credit card data from Affinity Solutions tell a similar story, with spending among lower-income zip codes up 25% since January 2020 and rising sequentially in August—despite the likely payback from Amazon Prime Day in July. These data argue against an outright decline in consumption, much less one driven by the lower-income consumer.

Looking ahead, we expect a temporary lull in consumption growth at +1.4% annualized in Q4, as resuming student-loan payments weigh on upcoming retail sales reports. However, management teams are well aware of this headwind—discussions of the topic rose fourfold in the quarter—and retailer guidance nonetheless points to continued modest growth in spending, both in the aggregate and at the lower-end.

We believe that we are in a late cycle backdrop. More importantly, equity markets are starting to agree based on relative performance under the surface. We recommend sticking with a barbell of defensive growth and Industrials/Energy.

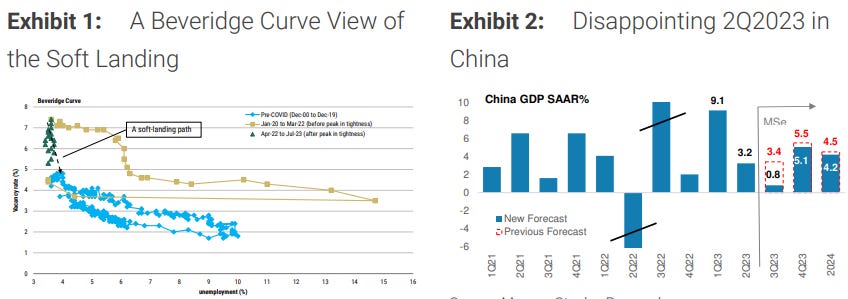

… The recent move higher in both real and nominal yields to cycle highs also poses a headwind to equity valuation as the correlation between real rates and equities has once again pushed deeper into negative territory ( Exhibit 2 ).

… Bottom line, more companies are starting to feel the negative effects of falling inflation. With the positive impact of falling inflation largely already reflected in valuation in our view (the classic late cycle trade that typically happens when the Fed pauses its tightening campaign), stock picking should now come down to owning the companies that can grow the top line even as pricing power fades. As we have noted for the past year, the real change amid this new boom-bust regime is that inflation is more volatile and difficult to manage, particularly for small caps that lack scale and access to capital.

MS - Sunday Start: Adding El Niño to the List of Risks (we KNOW weather and Mother Nature is rough — it delayed NCAAF yest by something like 22hrs yesterday but now, it’s becoming ‘goat for all things markets/economy related? seriously? yep, seriously … )

My father has teased me that the cosmos created meteorologists in order to make economists feel better about their forecasts. This year, that joke will be particularly salient. Weather forecast models suggest there is a 90% chance of a moderate El Niño weather event and a 66% chance for a particularly strong event. El Niño is a phenomenon where typical Pacific weather patterns reverse, with some regions getting more rain (the US, Argentina, and the Andes) while others face the risk of drought (Southeast Asia, Australia, Brazil, Colombia, Africa, Central America, and the Caribbean). The last strong El Niño cycle occurred in 2015/16 and brought food price volatility and energy disruptions. Recent shocks from Covid and the Russian invasion of Ukraine have already caused volatility in these markets, so a severe El Niño event could heighten global risks, perhaps more than in the past given climate change…

… We will not know the severity of this year’s El Niño for a few more weeks. If confirmed, El Niño should peak around year-end and early next year, which allows some planning time to mitigate the effects. Morgan Stanley has recently published on the micro and macro effects of El Niño, highlighting which economies and sectors are most likely to be affected.

History suggests that the implications for economic growth are actually fairly limited, apart from countries with the largest net trade surpluses or deficits in agriculture. Precise quantification is impossible, but the relatively small proportion of GDP that comes from agriculture means that, all else equal, we look to inflation as the primary economic risk from the disturbance.

El Niño most directly affects consumer inflation as food and energy commodities prices pass through. Of late, inflation has been coming down across both developed and emerging markets, with global headline inflation falling to 3.4%Y in June from 3.8%Y in May. July prints also showed further progress. But inflation is still above central bank targets in most countries, hence a severe El Niño could be a headwind for policy normalization. Indeed, the central banks of Brazil and India reference El Niño risks on their forecast horizon. The market implication is the risk of a slower cutting cycle and thus higher rates. Most exposed are countries with a high share of food and energy in their inflation baskets, which tend to be in emerging markets (Exhibit 1), especially those with lower incomes.

MSs - The Weekly Worldview: Looking Backwards and Forwards (this allows an intra quarter / 1/2yr update whereby one can mark calls to market thereby and ultimately regaining optionality to say … they told us so…?)

The week after Labor Day is back to school season, and the economics team released a publication that marks to market our views into year end. The strategy team has done the same in a similar note. The biggest calls this year have been the US and China. Our soft landing call has become consensus for the US, that expectation has been a key driver of asset prices, and if anything our call was not bullish enough—US growth has outperformed our call. Conversely, Chinese growth has consistently surprised us to the downside, and the policy stimulus has been insufficient to drive the cyclical rebound we had expected.

Since early 2022, we have said despite the aggressive hiking cycle from the Fed, we do not expect a recession. That call was out of consensus, in large part because history provides few if any examples of a soft landing. In the event, data for Q2 and Q3 actually surprised us to the upside, in particular with more spending from state and local governments and extra nonresidential structures investment. That fact might be evidence that fiscal policy is more supportive than we had thought. Consumer spending has also had a few one-off upside surprises, but discretionary categories have shown the slowing we have been expecting. Most importantly, the rapid fall in inflation we have been expecting materialized. The market is debating whether one more hike is in the cards, but we think the pause has begun.

We look for the FOMC to keep its target range for the federal funds rate unchanged at 5.25-5.50% at its meeting on September 20. Most market participants expect rates to remain on hold as well.

Recent data suggest that the U.S. economy generally remains resilient despite the 525 bps of rate hikes that the FOMC has delivered since March 2022. That said, it appears that the monetary tightening of the past 18 months is beginning to have its intended effect. The labor market is becoming less tight, and price pressures are easing.

There remains some distance to go before reaching the Fed's inflation target of 2% on a sustained basis. Therefore, we expect the post-meeting statement will continue to signal that the Committee maintains a hawkish bias.

The FOMC will release its quarterly Summary of Economic Projections (SEP) at the conclusion of the meeting. We expect that the September SEP will portray a more optimistic outlook for the U.S. economy than the last SEP did in June. Specifically, we look for the FOMC to raise its forecast for real GDP growth this year while also nudging down its outlook for inflation.

We do not expect major changes in the "dot plot." The median dot for 2023 stood at 5.625% in the June SEP, which would imply another 25 bps rate hike between now and the end of the year. We think it will be a close call on whether the median stays at 5.625% in the new dot plot or drops to the current midpoint of 5.375%. We lean toward the latter, though the August CPI report, to be released on September 13, may be the ultimate deciding factor.

We do not think the median dots for 2024 and 2025 will change much, if at all, though some of the highest dots may be reined in a bit.

https://youtu.be/JfjoF6AoRFU?si=eYHkEAXpOOtOVgnj

Commentary on United and American Airlines Options Activity on 9/11

by Jon Najarian

Outstanding work !!!

I'm looking for a Hot CPI and to a lesser extent PPI.

El Nino probably Moderate to Strong, judging by the Record Breaking heat in Arizona.

Inflation has come down, but I think we may stalling out.

The Last Percent or so, will be difficult and take time....maybe the whole 2024, to get to 2-2,25%

Saw the Second Plane hit, as I was watching CNBC Pre-Market Open.

I was in my apartment in Rochester, NY.

Called my Dad.

Never will forget it !!!