Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Duration supply coming early and often given Friday settlement and so a look at 10yy WEEKLY (complimenting yesterday’s look at 30yy)

Momentum does appear to be remaining overSOLD (buyable, dare I say of the SCREAMING variety?) and holding on for dear life TO support up nearer October cheaps of ~4.33% … Get those bids in for 3yrs Monday, 10yy Tues and long bonds Wednesday — early and often as they say in some circles (likely NOT anywhere ever near GA …)

I’ll quit while I’m behind and get TO the reason many / most are here — not MY views bur rather, some UPDATED WEEKLY NARRATIVES where I’d note a couple / few things which stood out to ME this weekend …

Our bond/stock asset allocation model is indicating that bonds are the asset class offering the most value at this market juncture, as interest rates have risen over the past few weeks. But stocks are not yet seriously overvalued…

… we're comfortable with our admittedly poorly timed long -- especially given the level of real rates …

Goldilocksrates weekly - Approaching the (long) end (asking and NOT answering the right question, IMO)

Are 2% long run real yields a buy? … on a tactical basis, with risks skewed towards a softening of data in Q4, we have argued that these yields are more likely to set for a modest decline rather than a sharp selloff. That said, more structurally, the case for going long at current levels rests not on anticipation of a structural decline in real yields (we think current levels are “fair” from a medium-term perspective), but rather on our view that earning 2% real yields over a longer horizon with little to no credit risk is a reasonable return, and that bonds should have reasonable “insurance” value in the event of either a sharp growth slowdown or an outright recession.

Goldilocks- China: Both CPI and PPI rose sequentially in August (you know, if it was so good, why NOT release during a workday rather than in the dark of night?)

MSs global MACRO Weekly - The Last Bull Standing (combined with increasing SHORT POSITIONS — see below — perhaps rates are just NOW becoming a screamin’ buy?)

… We provide additional rationale for our bullish stance toward government bond duration and highlight the heavy buying from overseas investors in 2Q23 … We maintain long 5y USTs …

… Why are yields resisting moving lower? One key reason is that growth has stayed strong and Treasury yields have focused on upside surprises in growth while ignoring downside surprise in inflation. A second key reason is that August seasonality helped yields to go higher. But the selloff looks vulnerable.

UBS- Watching deflation (don’t worry, be happy, must always challenge notion anything bad and inflation may be sticky … so says this guy — not me),

… US television demand is now below the pre-pandemic trend. If you bought a new television in 2022, you probably won’t buy a new television in 2023. Televisions are now cheaper than January 2020 levels in the US, the UK and the Euro area.

This is a small part of a general durable goods disinflation. It is a reminder to challenge assumptions that inflation must be “sticky”. The laws of supply and demand do still operate, at least when it comes to television prices.

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Interest coverage ratios are declining for investment grade and high yield companies, see charts below.

This is how monetary policy works. Higher interest rates lower earnings and increase debt servicing costs.

With the Fed on hold until the middle of next year, the weakening of corporate balance sheets will continue.

The downside risks to the economic outlook are intensifying with falling interest coverage ratios combined with rising consumer delinquency rates, households running out of excess savings, and student loan payments coming back.

Source: Bloomberg, Apollo Chief Economist

Bloomberg (via ZH): Rising Oil Prices Might Be What Tips US Into Recession (nothing happens without consequence … unless, of course, I missed the memo and the current admin repealed the ‘laws of markets / economic gravity’ )

Authored by Simon White, Bloomberg macro strategist,

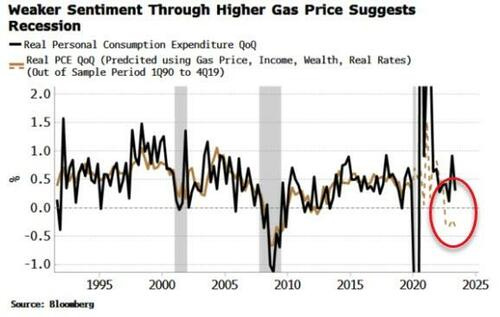

Household spending has kept the US economy afloat, butas growth slows a continued rise in oil and gas prices is poised to push personal consumption expenditure (PCE) lowerand thus trigger a near-term recession - with stocks and bonds unpriced for such an outcome.

Once again it has been the redoubtable consumer that has thus far kept a recession at bay. However, Bloomberg Economics (BBE) pointed out in a recent article that negative household sentiment – in confluence with other drivers of household spending – suggests that we should already be in a recession.

A regression model (using income, wealth and real rates) pins PCE growth roughly where it is. But if we add in the University of Michigan’s Consumer Sentiment index, it indicates much weaker PCE growth and thus an economy that would likely be already be in the midst of a slump.

I recreated BBE’s model and got something similar. I then substituted in the Conference Board’s Consumer Index instead of the Michigan survey. This also improves the fit of the original model, but does not paint as negative a picture for PCE. The reason is that the Conference Board’s measure has not deteriorated as much as the Michigan survey.

Why? The divergence between the two likely comes from the Michigan’s greater emphasis on frequent expenditures and business conditions, while the Conference Board’s index is more focused on the jobs market. As an employee, the jobs market has looked pretty good, boosting the Conference Board’s index, while the Michigan survey is more influenced by rising prices and conditions for small-business holders, which have been less rosy.

The Michigan survey is in fact very sensitive to gas prices. In the model, I added the average gas price to the model’s original inputs (i.e. ex Michigan). Doing so also improves the model’s fit, and as the chart below shows, implies notably weaker, and negative, PCE growth – and therefore an economy that would likely already be in a recession.

This highlights that the US economy is potentially on thin ice, with that ice represented by hitherto positive consumer sentiment, driven in no small part by gas prices (and sentiment on how high they are perceived to be) that remain comparatively cheap to the levels they reached last year.

But oil has been rising, driven by excess liquidity, falling inventories and supply cuts.

Tailwinds remain for oil, and therefore the nascent recent rise in gas prices is poised to continue as well. That could be the final straw which unseats the US consumer and tips the US into a recession.

Hedgopia - CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (positions matter and the look at long bond SHORTS GROWING should be incorporated into ones views, tactical and / or strategic, IMO)

… 30-year bond: Currently net short 198.3k, up 7.7k.

ING - US household wealth leapt $5.5tn in the second quarter (we got THAT going for us … which is nice…)

Strong equity markets and a recovery in house prices boosted net wealth in 2Q23, leaving it $37.6tn above pre-pandemic levels. This should be a solid base to withstand economic headwinds, but the data tells us nothing about who holds the wealth. The concern is that lower income households are experiencing financial stress and a consumer slowdown is coming

JPM - Catalysts through year-end: 5 things to watch for (i’m particularly interested in item #2 for what I’d assume are obvious reasons…)

…2) The Fed: Will it signal rate cuts?

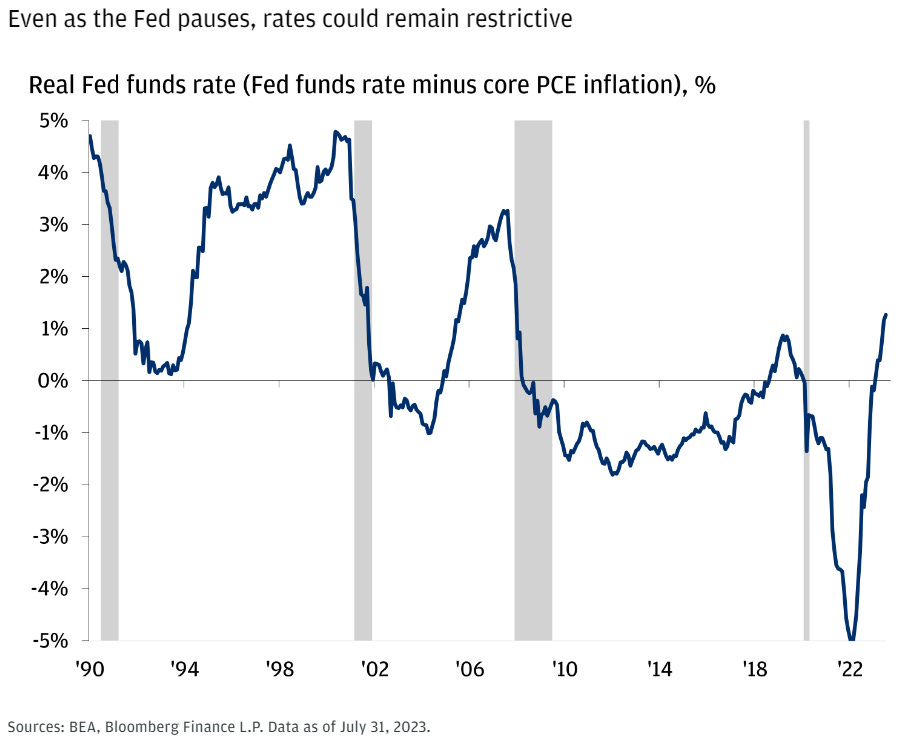

The debate around “is the Fed done?” seems exhausted. Whether the U.S. central bank pauses or has another hike left, the market’s expectation for the Fed’s “terminal” rate has hardly moved all summer.

The real question is how long a pause might last, and when and how quickly policymakers can start cutting rates. Just two months ago, investors were betting on Fed funds finishing 2024 around 3.75%; now, that stands around 4.40% (suggesting 65bps fewer cuts than before, with the first cut not coming until summer).

There’s some reason to believe it could potentially be on the earlier side. If inflation continues to cool at the same time the Fed holds rates, this means the real policy rate (the nominal policy rate minus inflation) is getting more restrictive without the Fed doing anything at all. That means just to keep rates as restrictive as they are today, the Fed would need to cut.

What to watch: The Fed’s 2024 dot at its meeting on September 20th. Right now, it’s at 4.625%, signaling even less cuts than the market…

Knowledge Leaders (aka Gavekal) - A Consumer Credit Cycle Has Begun (…and … econ V-COVERYs gone and we’re right back NO / SOFT / HARD landing on horizon and bonds a ‘SCREAMIN BUY’?)

With government stimulus over, accumulated savings starting to become depleted, rents soaring, and student loans about to switch back on, it appears a credit cycle has begun where borrowers struggle to fulfill their financial commitments…

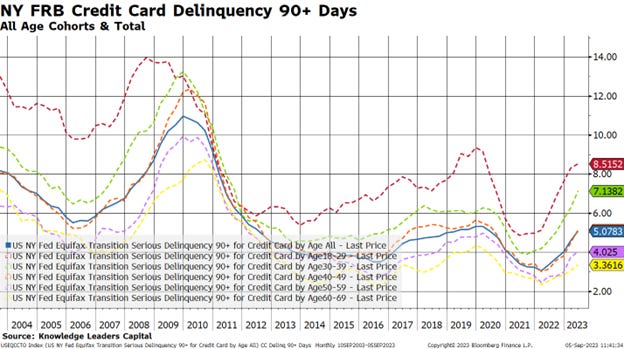

… Lastly, I’ll take a look at credit card delinquencies. Here is where we can really see the stresses building. First, the overall delinquency rate has about doubled from 2.5% to 5% over the last couple years. Second, older borrowers have seen a tick up in delinquency rates, a feature we don’t really see in other credit products. Third, one in 12 younger 18-29 year-old borrowers are 90+ days late making their credit card payments.

In conclusion, we are in the early days of a consumer credit cycle. Younger borrowers are the weakest link in this analysis, and this makes me wonder where rates go when student debt payments turn back on at the end of the month.

LPL- Breaking Down the Breakout in Oil (need. to. read…someone send to www.FEDREAD THIS dot COM)

Key Takeaways:

Oil has staged an impressive rally over the last few months. Voluntary production cut extensions from Saudi Arabia and Russia have helped improve the supply side of the equation. U.S. stockpiles of oil have also dropped to year-to-date lows.

Oil demand is picking up. China has ramped up imports to near-record levels, while the International Energy Agency forecasts fuel consumption likely reached another record-high last month.

The math is simple—declining supply and rising demand equal higher prices. West Texas Intermediate (WTI) recently wrapped up a nine-day winning streak that lifted oil out from a major bottom. Momentum is confirming the breakout.

In terms of upside, the next major area of overhead resistance for WTI sets up near the $94 to $97 range, which traces back to the August-November 2022 highs and a key Fibonacci retracement level of last year’s bear market in oil.

… In terms of upside, the next major area of overhead resistance for WTI sets up near the $94 to $97 range, which traces back to the August-November 2022 highs and a key Fibonacci retracement level of last year’s bear market in oil.

LPL - Weekly Market Performance – Markets Pullback on Strong Economic Data and Energy Prices (decent if only topical RECAP of week just passed)

… Fixed Income Lower The Bloomberg Aggregate Bond Index ended the week lower, struggling to maintain its footing as investors believe the Fed could maintain its hawkish sentiment longer than anticipated. High yield bonds also lost ground this week.

A few months ago, we asked the question: Has the high yield market lost its mind (see blog posthere)? Since then, the high yield corporate credit market has continued to show its resilience with the Bloomberg U.S. Corporate High Yield Index up over 6.8%, year to date.

Despite the solid returns, downgrades and defaults continue to eat away at future returns. However, spreads, or the additional compensation for owning risky debt, continue to shrug off the bad news. Moreover, credit metrics, particularly for the lowest-rated cohort within the index, continue to deteriorate with more than half of the CCC-rated borrowers with earnings lower than their interest payments making future payments and refinancing potentially problematic.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

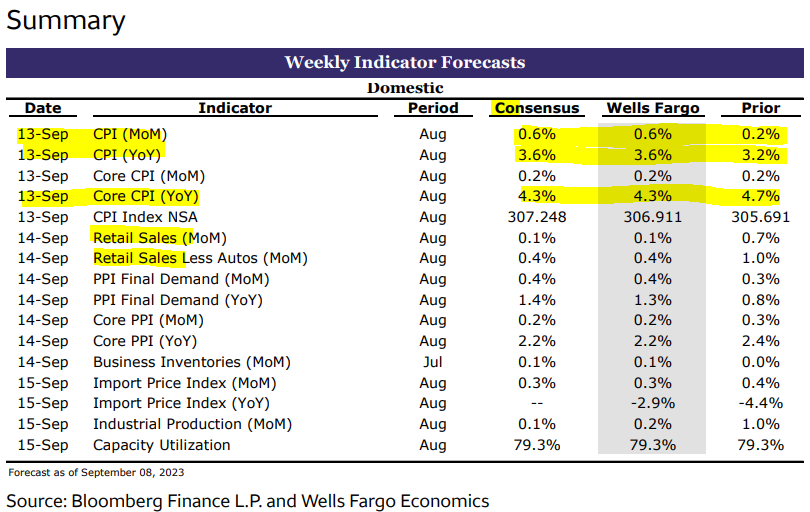

This could be a big week for the stock and bond markets. There will be lots of market-moving inflation indicators: Inflation expectations (Mon), small business pricing intentions (Tue), CPI (Wed), PPI (Thu), and import & export prices (Fri). There will also be a couple of business cycle indicators that could move the markets: retail sales (Thu) and industrial production (Fri). On balance, we expect that the inflation stats will confirm that it remains on a moderating trend, while the sales and output data should suggest that the strength in the Atlanta Fed's GDPNow model (with real GDP up 5.6% during Q3) is a temporary aberration from the soft-landing scenario that has prevailed since the start of last year.

The problem is that the markets may already be priced for this happy scenario. The unhappily surprising alternative would be higher-than-expected inflation and stronger-than-expected economic activity that would send both stock and bond prices lower. This week will be an important one for which scenario the markets will discount. Now consider the following:

Finally, before hitting SEND, I’d like to take a moment and recommend another ‘stack I’ve been reading … I’m NOT a closed - end fund expert BUT a fan of good output and insights (sorta why I keep running tabs on ‘Global Wall Street' and evil ‘sellside’) and this site is, in my view, worth a click … And frankly, wishing I knew ‘bout something like this BEFORE years of ZIRP ultimately led to the removal of ME from my institutional FI seat!

… About Yield Hunting is a full-service retirement and pre-retirement income offering that is devoted to helping members construct a solid portfolio of high-yielding, income producing securities, primarily consisting of Fixed-Income Closed-End Funds, but also includes: REITs, Muni’s, Baby Bonds, and Preferred Stocks.

Our goal is to find yield worth the risk.

Yield Hunting's proprietary Core Income Portfolio seeks to return a mid-to-high single digit yield with stable to rising principal and significantly less downside risk than stocks.

Invest alongside a real portfolio manager and financial advisor with over 25 years experience managing assets- along with his dynamic team. Yield Hunting’s easy-to-follow low-maintenance models are aimed to generate a high single-digit yield for retirement income planning or fixed income allocations.

After hitting SEND here I’m going to RECOMMEND this ‘stack’ directly and wanted you to know as I have NOT yet done so and take the making of recommendations seriously (as one can … one who, like myself, is no longer acting in any capacity of importance) as I have found, after my review past few days / weeks, there to be value derived…

Any / all questions should be directed TO folks who are, like us all, out there, YIELD HUNTING … something one can do now again in the UST market!!

Now … it is time to hit SEND and ask if … yer ready for some football!!

Thing 3 made it home after his frosh practice last night — ridin’ his bike in torrential downpours meanwhile, at home, this is what it was like,

And the older I get the more interest in teams far and wide … Last nights local edition ‘Friday Night Lights’ yielded a DUB,

Finally, am watching BC @ Holy Cross (Punter for BC specifically — a friends son and our oldest’s roommate — who has YET to be called on as BC UP 24-7 at the half …) and then on to HOPING for a GIANT victory tomorrow evening!

On that note, in case you’d like an NFC East preview, check THIS ONE OUT HEREfor fun facts like this,

KEY STAT: Running back Saquon Barkley leads all active NFL players with 5.8 injuries per carry.

Go GINTS! THAT is all for now. Enjoy whatever is left of YOUR weekend …