Good morning … While much is being made about the China FIX overnight (see this mornings HARK just below for more), I thought of ALL the news stories (really a stretch here trying to make something outta nothing), this one deserves top billing,

Reuters: Fed's Logan: can skip Sept rate hike, but 'there is work left to do'

… "Forecasts are inherently uncertain. My base case, though, is that there is work left to do," she said in remarks prepared for delivery to the Dallas Business Club at Southern Methodist University. "After the unacceptably rapid price increases of the past several years, I’m not yet convinced that we’ve extinguished excess inflation."

… "Another skip could be appropriate when we meet later this month," Logan said, referring to the Fed's upcoming Sept. 19-20 meeting. "But skipping does not imply stopping."

A dove in hawks clothes? Listen and READ and make of it what ever you will. Worth noting as they try to send signals ahead of the blackout period…which begins TOMORROW. Ahead of THAT, a WEEKLY look at long bond yields which are +5bps or so on the week so far …

Momentum REMAINS overSOLD and rates clinging to ‘support’ in / around 4.41% and seem to be doing so somewhat better than Kadarius Toney able to do in last nights GAME CHANGING MOMENT

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are a touch higher with the curve a hair steeper with little data overnight (see above). DXY is UNCHD while front WTI futures are modestly higher (+0.45%). Asian stocks were mostly lower again, EU and UK share markets are modestly lower while ES futures are showing -0.1% here at 7am. Our overnight US rates flows saw light turnover this morning with little to report thematically. Overnight Treasury volume was about 80% of average overall with 3yrs (160% of ave) seeing some relatively elevated turnover ahead of Monday's $2bn-upsized auction of the same.

… Yesterday we discussed how some/most US duration benchmarks appeared stuck in a vise-like price pattern. We said that because many benchmarks remain pinned near prevailing range support levels even as multi-month bear trends remained trend-dominant. The best way to observe the narrowing confines of such a set-up is via the daily chart of Treasury 10yr yields. Our first attachment this morning show this with the October '22 move highs near 4.335% acting as a predictable cap on rates over the past few weeks of bearish/hawkish pressure. Meanwhile, we've highlighted the bear trend in place since the May 4th move low (3.293%); a bear trend that is also the bottom of a nicely-defined bear channel that has guided 10yr yields over 100bp higher since early May. The two black lines don't converge until late next month but we're of a mind that 10yr yields are at an unstable juncture here being so close to key breakout levels- both above and below. It's important to note that we see nothing that threatens a bull momentum turn yet but such conditions could emerge at any time given the set-ups we see. So, for now, it's the bear trendline that dominates and we'll be patient to see how 10's and other rates benchmarks wriggle out of such handcuffs. It's our view, owing to the still 'oversold' readings in the longer term momentum studies, that a bullish breakout in 10's probably has more bandwidth to extend than a breakout to higher yields may have. We'll see how it goes.

I’m watchin’ 30yy WEEKLY and these guys — some of best in biz — are focused on here and now … WATCHING… and for some MORE of the news you can use » The Morning Hark - 08 Sept 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Apollo - More Consumers Are Using BNPL (what’s BNPL you ask … well, at least I did when I read this and then, well … Ruh Roh RelRoy)

Almost half of US households have used Buy Now Pay Later (BNPL), see chart below.

We forecast headline CPI growth of 0.6% m/m sa, pushing the annual rate higher to 3.7% y/y, and the NSA print at 307.006, led by higher energy prices. We estimate that core inflation pressures firmed modestly, to 0.22% m/m, as a run-up in core services inflation is likely to be partly offset by stronger goods deflation.

A resilient US economy and rising oil prices are challenging the disinflation narrative, hurting both bonds and equities. Although higher oil fuels more stagflation in Europe, the silver lining is that it could lift earnings expectations, as Energy sector has been a drag. US CPI and ECB meeting are key catalysts next week.

Market pricing for the fed funds rate path implies a roughly 70% probability of soft-landing vs. recession. Given our view that recession odds are better than even, this translates into an attractive payoff to front-end receivers. Returns to forward curve steepeners during Fed pauses hinge on the extent to which the Fed cuts more than ex-ante priced. Given this, the payoff to forward steepeners today also looks favorable, even more so due to factors boosting term premia.

… The main risk to the view is a “no landing,” which we define as inflation failing to fall below 3% and the unemployment rate remaining near current lows. Given the Fed’s commitment to its dual mandate, this should ultimately morph into a deeper recession as the Fed tightens more to bring inflation down, but from a mark-tomarket perspective steepeners would not be the right trade for this scenario.

MS - CPI Preview: Core Confirms Recent Progress (sounds not too bad a read, apparently they missed the ‘Ruh Roh RelRoy’ memo)

We expect 0.18%M in August core CPI growth (vs. 0.16%M in July, 0.2%M cons, 4.3%Y). Core services moves sideways (0.36%M vs 0.35% in July) and core goods deflation continues. Higher gasoline price accelerates headline to 0.61%M (3.6%Y NSA, Headline CPI Index NSA: 306.718).

… The main category driving disinflation in August is core goods, where we expect another negative print …

… We see meaningful acceleration in energy bringing headline above core (0.61%M in August). The increase in retail gasoline prices started the last week of July and continued in August, so we expect a relevant impact on energy CPI this month. We see energy CPI at 6.2%M (vs. 0.1%M in July).

Turning away from Global Wall Street TO the interweb, a couple / few things which caught my eyes,

… A Bird in the Hand Cash is still king, even if some investors, including BlackRock Inc.’s Jeff Rosenberg, reckon two-year Treasury notes are a “screaming buy”.

Money-market fund assets climbed to a fresh all-time high for the second straight week as interest rates north of 5% continue to attract investors.

Such funds have generally been speedier in passing on better returns to investors relative to banks, and the odds are rising for another quarter-percentage point this year, with US overnight indexed swaps looking at around a 40% chance by November. So cash will likely retain its allure — at least in the near term.

In comparison, the longer-end of the Treasury curve is eliciting mixed reactions at best. Barclays’ strategists in particular are circumspect.

While ten-year yields over 4% are attractive, the prospects are dim for a meaningful drop in yields that would generate big gains for investors who buy now, strategists led by Anshul Pradhan wrote.

The Barclays’ team additionally noted that the sort of catalysts that could spur a big bond market rally — such as an economic slowdown or an end to Fed rate hikes — are already expected by most people.

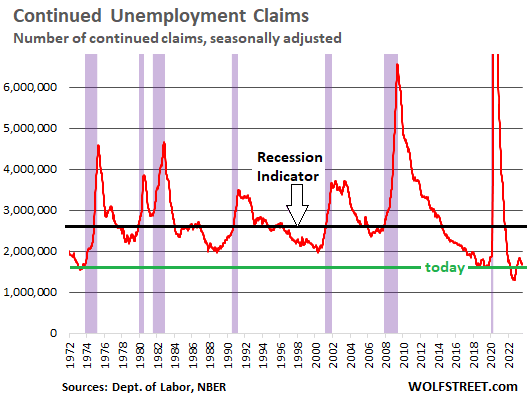

WolfST: My Favorite Recession Indicator: The Next Recession Moves Further out of Sight (continued claims > 2.6mil)

…The recession indicator. Recessions from the Great Recession back through the early 1980s began when continued claims for unemployment insurance spiked through about the 2.6-million mark.

So this 2.6 million line (black) for continued-claims is one of our recession indicators – and my favorite. But continued claims have been backtracking since April, and today’s level of 1.69 million is far below recessionary levels, and has been pulling further away from the recession line:

The long-term view shows that the labor market, as depicted by people continuing to claim unemployment benefits, has strengthened since April, after having weakened a little in late 2022 and early 2023. But throughout this period, it has remained historically tight, and even at the worst point earlier this year, it was in the range of the Good Times just before the pandemic, and much tighter than in the prior 50 years.

What the labor market is telling the recession watchers here is that there is no recession in sight. There will be a recession someday – there always eventually is a recession – but it is not in sight, and we’ll just have to keep watching for it.

ZH: Banks' Usage Of Fed's Emergency Funds Jumps To New Record High, Money-Market Inflows Soar (this one strikes me as important for what I believe to be obvious reasons…)

Finally, from an ‘official’ source, we’re now to believe rate hikes and their lagged impact HAVE BEEN FELT …

We estimate how much of the impact from the Fed’s current tightening cycle is yet to be felt in the U.S. economy in both absolute and relative terms. To do this, we use the model from D’Amico and King (2023), which explicitly incorporates economic expectations and allows for forward guidance.1 That model implies larger effects of monetary policy and faster policy transmission than other empirical models. We estimate that although the majority of the effects on output and inflation have already occurred, the policy tightening that has already been implemented will exert further restraint in the quarters ahead, amounting to downward pressure of about 3 percentage points on the level of real gross domestic product (GDP) and 2.5 percentage points on the Consumer Price Index (CPI) level. Tightening effects on the labor market manifest more slowly, so more than half the policy impact on total hours worked is yet to come. According to the model’s forecast, the policy tightening that’s already been done is sufficient to bring inflation back near the Fed’s target by the middle of 2024 while avoiding a recession…2

In as far as that Laurie Logan speech (and those trading it one way or another),

Hedgeye - Powell’s “Soft Landing” Is Impossible (an oldy — June 2022 — but a goody)

What goes ‘round comes ‘round? AND … THAT is all for now. Off to the day job…

Very good piece that has value. I pledge to subscribe as long as I can justify the cost.