Good morning / afternoon / evening (please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Before I jump in to the Global Wall Street inbox and link-A-palooza with all the expected recaps / victory laps-a-thon and the sellside sayin’ I TROLLED ya so, something I missed Friday morning which may become more evident (and important over the weekend and days ahead…

Thanks for reading The BondBeat! Subscribe for free to receive new posts and support my work.

ZH: China Property Bailout Rumors Send Global Markets Higher

This is something which will need to be watched as many had hoped (still HOPE) for some sort of CHINA led V-covery to impact global supply / DEMAND.

IF they make some moves it is likely they can / WILL reverberate all the way through global capital markets and, well, we should consider the possibility …

NOW as far as the data Friday morning,

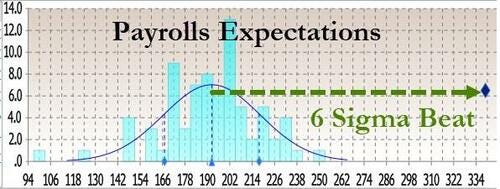

ZH: Payrolls Soar By 339K, Blowing Away Highest Estimate, Even As People Employed Tumble By 310K Sending Unemployment Rate Higher

… Going back to the May print, not only was this a 4 sigma beat to expectations...

... but it was the 12th beat of expectations in the past 13 months.

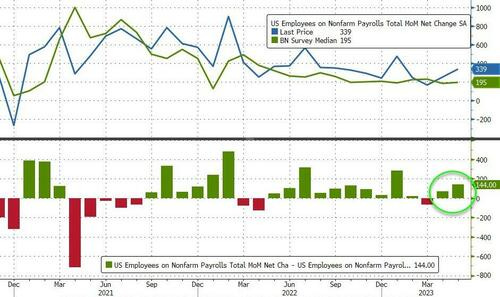

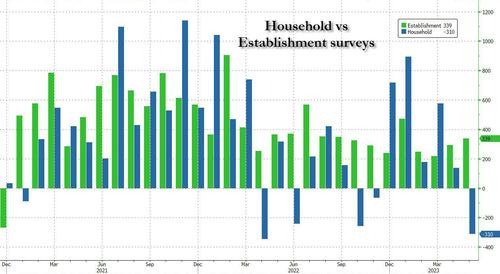

And yet, while the Establishment survey was a blowout beat and the strongest print since January, the Household survey unexpectedly tumbled by the most since April 22 as it plunged by 310K jobs...

... pushing the divergence between the two series back to near record wides...

ZH: A More Complex Report Than The Headlines Suggest

… But the Household report says we lost 310k jobs in the month. And for 2 months we have lost 170k jobs on a cumulative basis. The unemployment rate ticked higher to 3.7% from 3.4%. That is based on jobs lost in the Household report, since the participation rate remains unchanged (except for rounding).

So the jobs number we all look at screams HIKE, but the unemployment rate at least says hike or even pause.

Hourly earnings were revised down a touch last month, but remain above 4%. For those in the Fed who believe wage inflation is the key driver of inflation, that will tilt them slightly hawkish.

Hours worked continued to slide, from 34.6 hours in January to 34.3 hours in May, often a prelude to declining hiring needs.

I think we have to price in:

Possibility of June hike increased (higher 2 year yields)

The likelihood that the Fed will have to react to the strength in the report and ignore the weak parts (more inversion of 2s vs 10s).

Given ADP, I can see how we are going to run with the job market is great scenario (though the new ADP was changed to better track NFP, so I’m not sure what to make of that)…

What’s it all add up to? MONSTER bid for stocks because, you know

ZH: 'Goldilocks' Jobs Data Drives Stock Short-Squeeze, Hammers Bonds & Gold

I’ll leave it for you to browse through ZH link while still readily avail and NOT paywalled (?) and as you do, ask yourself how to justify monster move HIGHER in stocks (and so, EASIER in financial conditions) works with a pause or rate cuts? Goldilocks only had 3 bowls of porridge, best I reckon …

BMO: shift fwd entry buying of 10yy DIPS to fwd entry 5s30s steepner and NOTES jump in URATE, “…Using history as a guide, the increase in the UNR has reached an inflection point whereby (roughly speaking) a 0.3 percentage point increase in U3 off the trailing 12-month low portends a larger surge in joblessness"…” Cition URATE, “… As we share graphically, prior historical incidences of 3/10ths jumps in the U-3 UR have some often coincided cyclical turning points and sustained rises in the U3…” MScutting ALL it’s trades (incl LONG 5s), NEUTRAL, more UST VOL coming

It goes without saying, there is plenty of ink spilled on the coming onslaught of TBILL ISSUANCE (see MS for example, as it largely motivates them to stand aside, get OUT of trades including 5yy LONGS) because known UNKNOWNS will serve to INCREASE VOL in markets.

This VOL may serve up reason for a pause (of hikes) which may very well refresh.

Turning FROM Global Wall Street inbox and TO the www, a couple / few MORE links to help tide you over until … markets open Sunday evening.

On NFP,

LPL - Will A Blowout Jobs Report Change the Fed’s Mind?

Highlights:

Company payrolls grew by 339,000 in May as April estimates were revised higher to 294,000.

Job gains were broad-based and occurred in professional and business services, health care, construction, and social assistance services.

The unemployment rate increased by 0.3 percentage points to 3.7%, the highest rate since October.

Both measures of participation were roughly unchanged, but there were 440,000 more people out of a job, the biggest monthly rise since the beginning of the pandemic.

Wages grew 4.3% from a year ago, a healthy clip but not high enough to incite additional inflationary pressures.

Bottom Line: The Federal Reserve (Fed) will still likely pause later this month, despite today’s payroll report, because policy makers are focused on the lagged effects of the previous rate hikes….

… The Fed is in a tough spot. The job market was hot in May, but some suggest the labor market is not the primary source of current inflationary pressures. As the San Francisco Fed indicated, labor costs do not have a meaningful impact on sticky inflation. The Fed will still likely pause later this month, despite today’s payroll report, because policy makers are focused on the lagged effects of the previous rate hikes. Most voting members of the Federal Open Market Committee (FOMC) do not believe the economy has felt the full impact of tighter financial conditions. If they pause this month, there is a growing expectation the Committee will hike in July if the economy continues to run hotter than expected. Despite the growing uncertainties, the LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) is growing increasingly positive on core bonds, which offer a more competitive alternative to equities than they have in quite some time.

AND from Mr. POSITIVE

First Trust: Data Watch - Nonfarm Payrolls Increased 339,000 in May

… Implications: If you have followed our recent reports on the US labor market the main theme has been ambiguity, and the data in May was no different. Once again, we have a report on the labor market with solid headlines but worrisome details…

… Overall, today’s labor market report echoes a lot of the concerns we raised in this week’s Monday Morning Outlook. It’s easy to find surface level good news on the US economy, but the data behind the scenes leaves us feeling cautious. In other recent news, automakers sold cars and light trucks at a 15.0 million annual rate in May, down 6.5% from April but still up 19.6% from a year ago. In addition, sales of medium and heavy trucks hit a 558,000 annual rate in May, the fastest pace since 2019.

Oh … Ok, then … moving right along … a weekly FI related newsletter from BBG,

The Weekly Fix: The Fed Should Just Go Ahead and Hike in June

Might As Well

With less than two weeks until the Federal Reserve’s June rate decision, bond traders have almost completely bought into the “skip” sequencing: swaps show that a pause is more likely than not in June, followed by a four-in-five chance that rates rise by July.

Fed Governor Philip Jefferson — recently nominated to be the central bank’s next vice chair — said as much on Wednesday. Should policy makers hold rates at this month’s meeting, that decision “should not be interpreted to mean that we have reached the peak rate for this cycle.”

But if June’s hold turns into a hike at July’s meeting, why not get it over with?

“I think the Fed is getting a bit too cutesy with its ‘skip vs. pause’ debate with regards to the June FOMC,” said Win Thin, global head of currency strategy at Brown Brothers Harriman. “Does the extra month between the June 13-14 and July 25-26 meetings really make a difference?”

Yes, we’ll get some valuable information in that additional month: another round of jobs and inflation prints, more clarity on the ripple effects of March’s banking crisis, more time in general for the lagged effects of tightening to surface in the economy.

But let’s recap what we’ve seen just in the past couple weeks: inflation is still hot, the labor market is still strong and after much, much ado, it looks as if the US debt ceiling will be raised in the coming days, removing a huge wildcard for policymakers.

“In public appearances, Fed hawks are running circles around the doves and the latter’s insistence that they remain data dependent isn’t helping them build a case for not hiking in June,” SGH Macro Advisors Chief US Economist Tim Duy wrote in a client note. “If anything, the opposite is happening as the data reinforce the case for a rate hike.”

But as BBH’s Thin noted, June’s decision will likely all come down to the data released over the next 12 days — so all eyes on Friday’s May jobs report.

… You Can’t Hide Forever

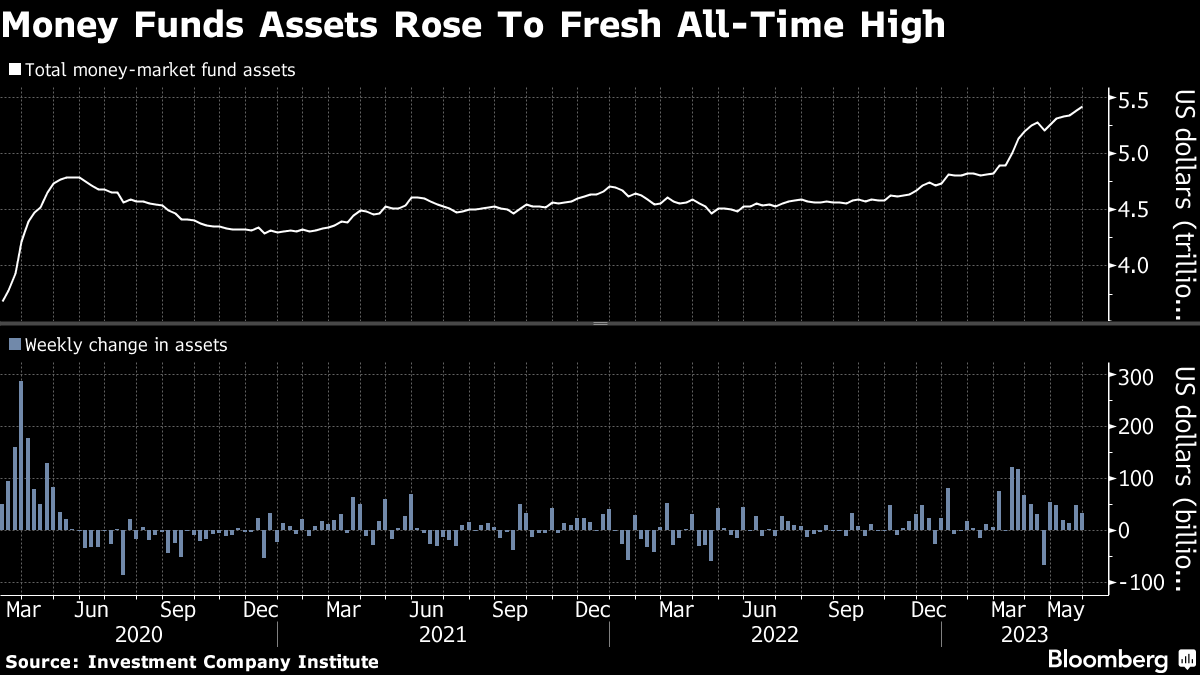

Cash has made a lot of sense this year — short-term rates above 5% in exchange for virtually zero credit or duration risk look great in a bear market. That logic has been the driving force in sending money-market fund assets to a record high of $5.4 trillion.

But now that equity investors have fallen in love with the artificial intelligence narrative and the Nasdaq 100 suddenly up more than 30% on the year, that calculus could stand to change.

“From a sentiment standpoint, it is a vote of extreme pessimism toward risk-on assets by investors,” Ed Clissold, chief US strategist at Ned Davis Research, wrote in a note to clients. “From a flows perspective, the assets represent potential buying power when investors become less risk averse.”

For much of the past year, cash has been considered an asset class in its own right thanks to soaring yields on Treasury bills. However, with the big rebound in equity markets, money managers are starting to view cash through more-typical lenses: as a way station of sorts between allocation decisions.

Similar to Ned Davis, Winnie Cisar of CreditSights views a potential exodus from the sidelines as a tailwind for credit markets — there’s plenty of investors waiting to buy the dip.

“Most of our client conversations are very much struggling with, okay, we have an outsized cash allocation, should we just be rolling three-month T-bills because they’re offering some juice and let’s wait until spreads widen out a bit, until we start to see defaults really pick up?” Cisar said on Bloomberg Television’s ETF IQ. “That’s actually one of the reasons that we’ve been more constructive on the markets, because if everyone is all cashed up in wait-and-see mode, it makes it very hard for spreads to gap significantly wider.”

… An alternative measure is the so-called “Supercore” inflation measure also known as Core CPI Services Less Housing. Fed Chair Powell focuses on this measure because it largely captures wage prices, which historically have been linked to inflation expectations. Supercore inflation is also still above 5%, but the most recent 1-month annualized level is 1.32%, which is a good sign. While one month is arguably not sufficient to predict the annual trend, using a slightly larger window of the past three months, we get 4.04% annualized rate for this measure, showing the trend is moving down, but slowly.

There are some green shoots in the Fed’s disinflation fight. Today’s payroll report showed weekly hours down to 34.4 vs. the 2021 high of 35 hours. However, other costs remain elevated, such as Owners Equivalent Rents, which is currently at a whopping 8.1% year over year. The timelier Zillow Residential Observed Rent Index is not presenting a much rosier picture with a year-over-year change of 5.26%, and a month-over-month annualized rate of 7%.

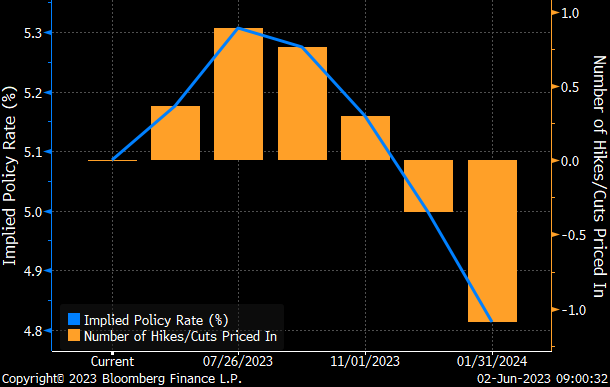

The next important measure of inflation will be the June 13 release of CPI, which takes place on the first day of the Fed’s June FOMC meeting. Currently the market predicts the Fed will wait and see how the effects of the fastest policy rate increase in a generation trickle through to the economy, and depending on how June data comes out, may raise in July.

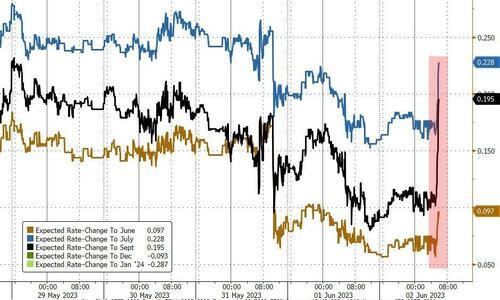

Bloomberg US Interest Rate Probabilities:

Finally, a look at POSITIONS ahead of a quiet week ahead … POSITIONS which may be ultimately MOST important as I used to think one was NOT supposed to be short a quiet market …

Hedgopioa… CoT: Large specs’ net shorts in 10-year note futures UP 10.2% w/w to HIGHEST EVER …

Lot of things to THINK about / consider in to the QUIET days and week just ahead but frankly, not much in the way of DATA and so, we may have to search far and wide (China?) for impulses or it may be as simple as increased supply of TBILL ISSUANCE (and finding willing buyers — from repo or otherwise) which may serve to INCREASE VOL …

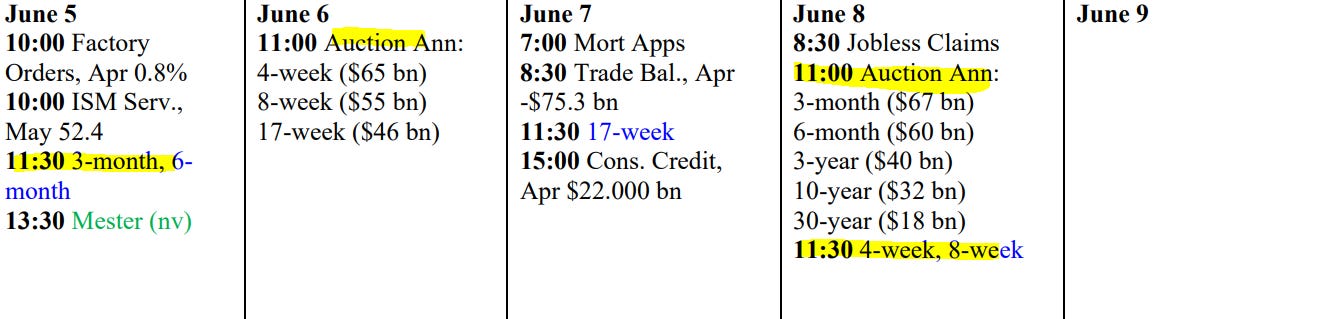

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

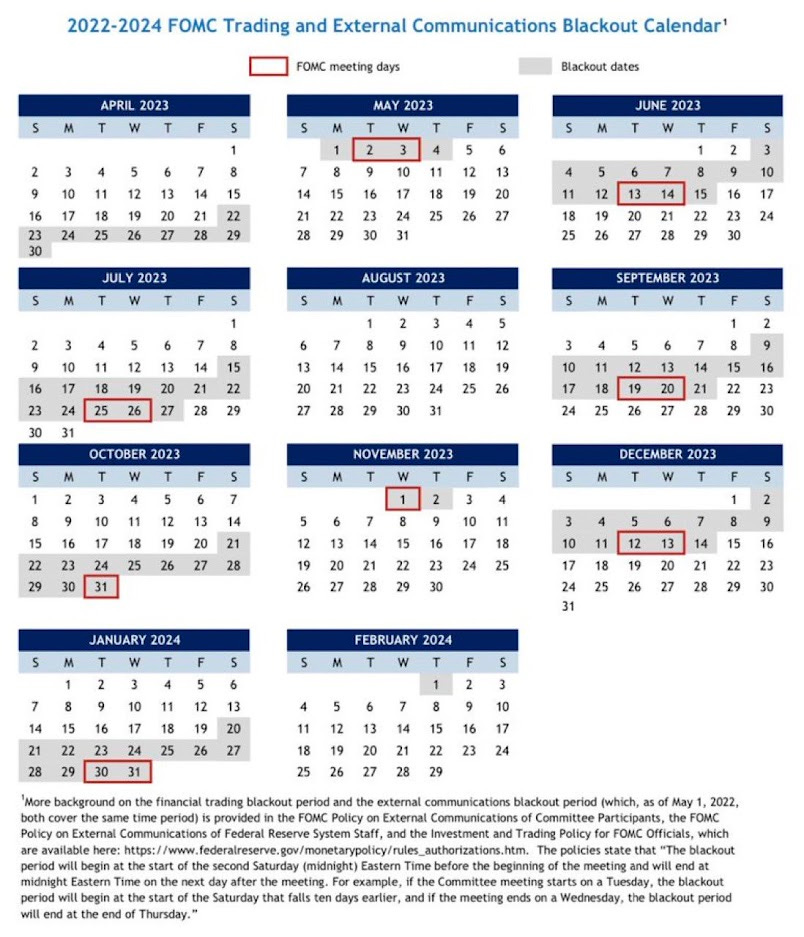

I’ll ADD a visual calendar I found on fintwit which helps detail the FOMC ‘BLACKOUT’ period (The period before FOMC rate-setting meetings, when Fed officials aren’t allowed to make public statements covering monetary policy, banking, or economic issues)

SO we’re IN THE ZONE and CONE OF SILENCE, if you will … THAT is all for now. Enjoy whatever is left of YOUR weekend …

Thanks for reading The BondBeat! Subscribe for free to receive new posts and support my work.