Fed Governor Waller mentions rate cuts in 2024 and states the path of policy will be "carefully calibrated and not rushed" as he sees "no reason to move as quickly or cut as rapidly as in the past."

USTs sell-off abruptly alongside release of Waller's prepared remarks, although the curve bear-steepens, possibly in anticipation of a weak $13bn 20y UST re-opening auction…

So, wait, what? Yer telling me maybe NOT 6 rate CUTS cuz Wally Says …

ZH: Stocks & Bonds Tumble After Fed's Waller Sends Rate-Cut Odds Reeling (with a link TO the speech … if any trouble sleeping at night)

… But it was the level of detail he added that colored the market's perceptions hawkish (full speech here).

Data-Dependent...

“I am becoming more confident that we are within striking distance of achieving a sustainable level of 2% PCE inflation,” Waller said in prepared remarks at a virtual event hosted by the Brookings Institution on Tuesday.

“As long as inflation doesn’t rebound and stay elevated, I believe the FOMC will be able to lower the target range for the federal funds rate this year.”

But, Waller reiterated his support for three cuts... not six like the market wants...

"This view is consistent with the FOMC's economic projections in December, in which the median projection was three 25-basis-point cuts in 2024".

And certainly does not see the need for aggressive cuts priced into the market:

“When the time is right to begin lowering rates, I believe it can and should be lowered methodically and carefully,” he said.

“With economic activity and labor markets in good shape and inflation coming down gradually to 2%, I see no reason to move as quickly or cut as rapidly as in the past.”

He reiterated that the timing of cuts and the actual number “will depend on the incoming data", specifically calling out the surprising strength in the December jobs report as “largely noise” against a trend of ongoing moderation. He noted a number of 2023 job reports have been revised lower, and “there is a good chance December will be revised down.”

… backing up a sec and being so far removed FROM a professional seat and front-row view, I can’t help but see this …

… in my minds eye, whenever told ‘bout WalleR

I’m sure I get the very same lack of respect (hey, it’s earned)!

In any case, NOT all bad as it would appear to be a welcomed development to those (like large German institutions who have Primary Dealership privelege’s) who will help facilitate this afternoons 20yr auction.

Ahead of this afternoons 20yr auction where it’s good to know / recall that SOME out there view 20s as desirable (this past weekends note referring TO Bloomberg story, “Deutsche Bank Says US 20-Year Bond ‘Comeback’ Merits More Supply” … rates POP are a concession … Here are 20s since their reintroduction TO Global Wall St in the middle of 2020 …

…Just what the C19 pandemic ordered? #Got20s? RECENT trend is somewhat HIGHER and that now exists as momentum (stochastics, bottom panel) double topping so, overSOLD … TIME will tell if there’s ‘nuff concession over 1st couple weeks here of the year. For now, though … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve pivoting flatter (2s30s -7bp) as ECB's Lagarde and Knot joined the crowd of central bankers pushing back on dovish market pricing. DXY is UNCHD while front WTI futures are lower (-1.8%, see attachment). Asian stocks were all dragged into the red by the Chinese exchanges (Hang Seng China Ent -3.95%), EU and UK share markets are all lower too (SX5E -1%) while ES futures are showing -0.4% here at 7am. Our overnight US rates flows saw better real$ selling in 10's through 30yrs after Treasuries opened trading with a bid. In London hours, stop-outs in 2s10s (see attachments) and 5s10s curves were seen/sensed though at the flatter extremes (2s30s -8bp), colleagues said steepener interest re-emerged. Overnight Treasury volume was quite solid at ~145% of average amid choppy conditions.

… and for some MORE of the news you can use » The Morning Hark - 17 Jan 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BAML Global Fund Manager Survey: My Herd is my Bond

Bottom Line: Fund Manager Survey (FMS) respondents are very optimistic on rate cuts and macro “soft” landing but Jan cash levels are up from 4.5% to 4.8% as bond market optimism tempered, and bonds driving the “herd”; BofA Bull & Bear Indicator up to 5.5, highest since Nov'21, positioning not contrarian +ve; new catalysts (e.g. global growth) required for upside…

… On Rates, Crowds & Tails: both bond & equity investors say Fed #1 driver of price in ’24; record optimism on rate cuts (just 3% expect higher rates), but dip in optimism on bond yields; most crowded trade “long Magnificent Seven” & “long-duration tech” best way to play rate cuts, no longer “long 30-year Treasury.”

… FMS investors have never been as bullish on short-term rates as in Jan'24 (data going back to Apr'01) …a record of 91% expect shortterm rates to be lower in the next 12 months, up from 87% in Dec'23:

… Investors turned slightly less bullish on bond yields post the 100bps rally in long-term rates over the past 2 months. 55% expect lower bond yields in the next 12 months, down slightly from a record 62% in Dec'23.

BNP: US rates: Hedging risks of earlier or larger cuts

The December Fed pivot and increased focus on softer core PCE have supported a material upgrade to near-term rate cut risk.

Weaker activity data is likely needed to solidify the case for larger or faster rate cuts in the near-term, leaving us cautious on outright received positions.

We think front-end call spreads offer an attractive way to have leveraged exposure, however. SFRH4 95.0625/95.125 offers the potential for 6.25-to-1 return.

DB: Early Morning Reid (so many different strategists, economists so that at some point we’ll all get a giant TOLD YA SO … someone’s gotta be right and here in this case, there’s some doubt ‘bout soft landing … so, something more nefarious to play out …?)

… After all the comparisons with the 1970s over the last few years, Henry pointed out yesterday that actually the late-1960s are becoming an increasingly good parallel. That was another period of low unemployment, rising deficits, and growing geopolitical risks. But it also saw inflation rebound, as the Fed cut rates just as fiscal spending rose because of the Vietnam War. Although markets are encouraging and hoping for significant rate cuts this year, today’s policymakers are cautious about a repeat. Interestingly since the ECB's Lane spoke over the weekend, the central bank speak has certainly turned a little more cautious about endorsing the amount of cuts currently priced in by markets. Our view is that the pricing is very aggressive versus history absent a recession so for it to be correct you have to believe in the immaculate soft landing scenario or a recession. We will see. Back to Henry's note and overall the late 1960s shows that with tight labour markets, fiscal stimulus and geopolitical shocks, that’s the sort of environment where inflation can return if policy errors are made. See the report here.

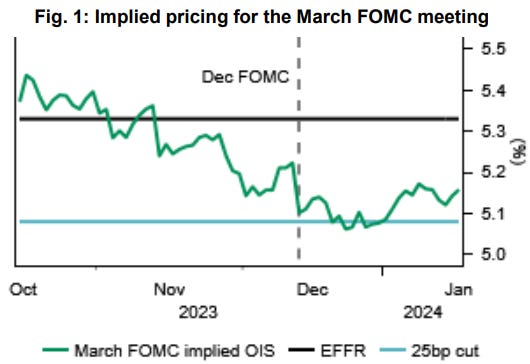

Goldilocks: Waller Speech Raises Risk of a Slightly Later First Cut or Slightly Slower Pace of Cuts

BOTTOM LINE: Comments by Governor Waller in a speech and discussion today raise the risk that the first cut could come slightly later than our forecast of March and that the pace of cuts could be quarterly from the outset, rather than our forecast of three initial consecutive cuts followed by a switch to a quarterly pace. We do not see his comments as necessarily at odds with our forecast, however, and have not made any changes to our baseline of a first cut in March and five cuts total in 2024.

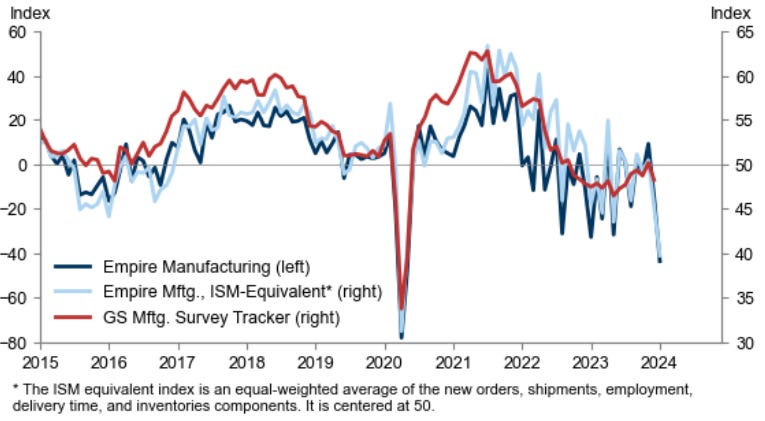

Goldilocks: Empire Manufacturing Index Falls to Lowest Level Outside Covid (misprint? nope)

BOTTOM LINE: The Empire manufacturing index declined by much more than expected in January to the lowest level in the series’ history outside of April 2020. The composition of the report was weak on net, with declines in the new orders and shipment components and a small increase in the employment component. The Empire survey has been particularly volatile since 2022, swinging by at least 20 points in over half of instances (14 of 25).

… Our chart shows that market expectations are set for rate cuts of more than 100bp for both central banks. What’s unusual is that the US normally has a larger and earlier implied move than the ECB. Futures contracts suggest the first cut could come as soon as March for both, and this is where most market participants would push back. It just feels too early to be anticipating rate cuts for the first quarter of 2024.

When considering the outlook for the sporting event, expectations would likely be based on past and present form of individual players, together with what the bookmakers are offering. Then there is the possible impact of wild card player choices, which don’t run with form, providing an element of surprise.

For bonds we can substitute forward rates for expectations, representing a weighted average of everyone’s current view. A measure of form requires us to look at history too, and the bond market wild cards will likely come from economic data, policy statements, or geopolitical shocks.

First, expectations. Our chart captures the difference between the three-month rate today, and a measure of where it will be in a year from now. It shows that the ECB and Fed are neck-to-neck, with market expectations for reductions of 134bp…

… Likewise in bonds we can expect some surprises in the economic data and outsized market moves. It’s highly unlikely we’ll see the ECB and Fed moving tick for tick. Draws in the Ryder Cup are extremely unusual, the last one coming in 1989. We probably won’t have to wait that long to get the winner of our rates Ryder Cup.

UBS (Donovan): Spending power (this guy, dunno … maybe it’s just me? i detect a note of jealousy towards USA whenever he writes…)

Retail sales dominate, and there seems no reason abandon the hedonism of the US consumer. Lower income US households are more constrained, but middle income homeowners are living in a world of around 2% inflation (except in Florida) and have more spending firepower. The narrative has shifted. In 2022, consumers were spending the President Trump’s profligate unemployment payments and were relatively price insensitive. Today consumers are responding to evidence of price discounting.

The Empire State manufacturing survey’s headline plunges further into contraction The FRB of New York’s Empire survey’s manufacturing general business conditions index swung 29.2 points deeper into negative territory in January. Today's headline reading of -43.7 was the index's weakest level since May 2020, well below our estimate of -5.0, and well below all estimates in the Bloomberg survey. The ISM-weighted composite of the components, which was subject to large swings around the expansionarycontractionary benchmark of 50 in the past two years, plummeted to 39.7 (see Figure 1). Since data collection began in 2001, the index has never been so low outside of a recession…

… Looking ahead, the index for business conditions six months in the future increased 6.7 points to 18.8, but firms' optimism was still "subdued," the survey said. New orders, shipments, and employment are expected to increase in the next six months. Capex intentions increased 9.5 points to 13.7, and the technology spending index increased 1.2 points to 9.5. However, all of the above are at relatively low levels for an economic expansion.

… Fed Chair Jerome Powell is undoubtedly monitoring the situation closely since a second oil shock, following the one in 2022, could boost inflation just the way it did in 1979, following the 1973 oil crisis (chart). All the more reason not to rush rate cutting.

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: 3 Reasons to Be Bearish Stocks (read thru like I TOLD YA SO)

Atlanta FED: Is the Last Mile More Arduous? (answer THEY offer: NO and instructive as Atlanta / BOSTIC IS voter — per #FOMC101)

Summary US inflation surged starting in spring 2021, with Consumer Price Index (CPI) inflation reaching a 40-year high of 9 percent in mid-2022. Together with improving supply-chain conditions, policy tightening by the Fed decreased inflation to within 1 to 2 percentage points of its 2 percent target by late 2023 without a significant increase in unemployment. However, concerns have been raised that the last mile of disinflation to reduce inflation consistently to its 2 percent target will be more arduous than the previous miles. Close examination of such concerns indicates that they do not receive compelling support. Because the last mile is likely not significantly more arduous than the rest, it is unlikely that the Fed needs to exert extraordinary effort in terms of additional policy tightening as inflation nears its target. Such tightening unnecessarily increases the risk of a "hard landing."

Bloomberg(via ZH): It Will Take A Lot To Talk Market Down From Rate-Cuts

… We will also get an update on retail sales this week. They have been much better than anticipated given the Fed’s aggressive rate-hiking cycle. Leading data suggests that momentum should continue well into this year.

In normal circumstances, that might mean a reappraisal by the market and a shift to less dovish pricing. But that has not been the case lately, with the economy - and even Fed-speak explicitly talking down a March cut - seemingly ignored.

It will likely take a more coordinated response from the Fed if they want to take an early cut off the table.

There are at least six Fed board members and bank presidents due to speak this week, so we will find out how fervent is the desire to push back against the market’s current dovish outlook.

Bloomberg: Why The Market Is Gunning For An Early Fed Rate-Cut (perhaps getting more to the point…)

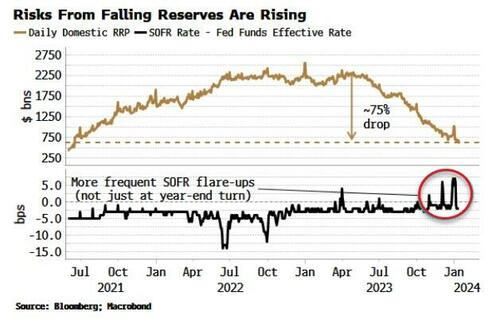

… The savior of market liquidity in the face of vast government supply has been the Treasury’s decision to issue mainly bills, allowing the liquidity parked at the Fed’s reverse repo facility (RRP) to harmlessly absorb much of this supply.

But now the RRP is dropping rapidly, and continues to fall as money market funds’ assets keep rising and bill yields remain attractive.

But the closer the RRP gets to zero, the nearer we are to the point where reserves are approaching their so-called lowest comfortable level, and funding problems could ignite as they did in September 2019.

In a sign risks are already rising, SOFR has jumped higher on more frequent occasions in recent months.

As a result, several banks have brought forward when they believe the Fed will begin to taper and then end QT.

JP Morgan, Bank of America and Barclays believe the process will start as early as April, and end as soon as mid-summer.

This highlights that financial-instability risks are possibly much closer than is commonly thought.

Why?

In practice the Fed does not want to run reserves down to their lowest comfortable level.

Powell has talked about ending QT when reserves are still abundant, but with an added buffer.

Banks will also want to keep a buffer in their reserves so they don’t run into funding issues.

But if perceived risks are rising – which we know is the case as end-of-QT forecasts are brought forward – the incentive is to increase the buffer.

If everyone does this - and everyone knows everyone else is doing it - then it’s prudent to raise your buffer a little more: if you’re going to panic, it’s best to panic first. Reserves could go from superabundant to scarce very rapidly.

Thus a linear correlation between reserves and financial conditions is not the appropriate way to judge whether the relationship is spurious or not, as Cameron argues it may well be.

In non-linear relationships it’s not about what happens through all time, but at turning points.

With reserves, there is likely to be a regime shift when they go below a certain level, where suddenly they do have a strong causal correlation with financial conditions.

That’s why QT’s end could happen rapidly once any taper starts. Cameron disagrees, giving the analogy of running while juggling tennis balls, with the juggling representing banks trading reserves with one another, and the speed of the running the pace of QT. More juggling is needed the more that reserves fall, thus it’s prudent to run slower.

In the analogy, however, there is no penalty for dropping one of the balls. If this cost is perceived to be rising, and yet you’re still being forced to run at a certain pace, i.e. QT is ongoing, then you might decide to stop juggling altogether! In other words, the funding markets would seize up, with negative repercussions for asset prices.

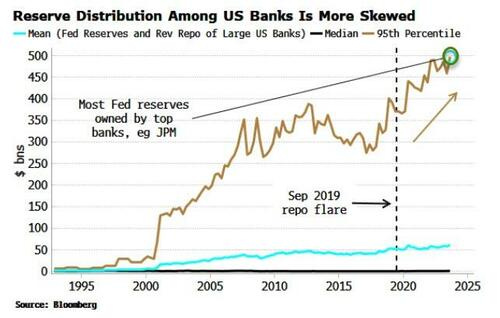

Banks with plenty of reserves will be OK, but it is the unevenness in how they are distributed that is the problem.

5% of the largest US banks own 40% of reserves, and the problem has become even more acute since the repo flare-up in 2019.

Pricing is set at the margin, and smaller banks without reserves will push up the cost of funding - a major risk to financial stability if it happens in an uncontrolled fashion.

The sooner rates are cut, the sooner pressure is taken off reserves from government interest payments, which are set to balloon to as high as an astronomical $1.5 trillion this year.

A simple regression shows that that the drop in yields since November as more rate cuts were priced in could already have taken $250 billion off the government’s interest-rate bill. That eases pressure on the government to tax and borrow more, which is ultimately a boon for reserves and their velocity.

Rate cuts should also bolster banks’ balance sheets as duration positions become less underwater – reducing the risk that banks stop dealing with one another in funding markets.

The Fed may purport to believe in the separation principle, but its unexpected pivot in December without obvious economic justification hints it may not. Either way, neither does the market, hardwired to seek what works in practice, not in theory. If perceived risks are rising, then pushing for an early rate cut makes sense (especially as there is no direct way to express a view on when QT ends).

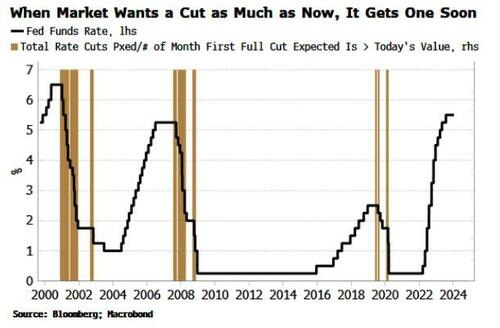

And we are now at the stage where the market has always got its way.

The chart below shows a market-based Fed easing trigger.

The brown bars are the times when at least the same amount of rate cuts have been priced as there is today, and as imminently. On every occasion the Fed was already cutting rates or very close to doing so.

The Fed could, of course, decide to push back more forcefully on early rate-cut expectations (and the risk-reward for trading a March cut in any event is very poor; an April vs May Fed Funds flattener may be a better option). But the fact so much got priced so quickly when not justified by Fed-speak or the data indicates the market is perhaps conditioning on other factors. Financial stability risks from the Fed’s balance sheet and the heightened impact of Treasury funding decisions fit that bill.

The lesson of the curious case of the March cut is that anticipating the short-term interest outlook in this cycle requires acknowledging we may be in a new paradigm, where unemployment and inflation are only part of the picture.

Bloomberg: Trump will move markets more than the Fed (Authers OpED)

… So confidently has the market moved to discount a sweeping financial easing in 2024 that these words were enough to shift bond yields sharply upward. It made for a fun trading session in New York:

In the broader scheme of things, this can be seen as continuing readjustment after last year’s ramp up in rates and subsequent sudden turn. The 10-year yield is now bang in line with its 200-day moving average and where it started last year. Having overshot upward, and came down a bit too far, the Fed and the market are now edging to a level where both can be comfortable:

It would be unwise to call this much of a retreat…

1/ Good Overbought Condition January's pullback in stocks is consistent with how good overbought conditions typically resolve and have inflicted little damage to internal and external trends. As chart 1 illustrates, as a result of the numerous breadth thrusts since the October ’23 low, a good overbought condition occurred when the RSI on the S&P 500 index surpassed 82. Contrary to popular belief, there is such a thing as a “good overbought.” The chart highlights when these have occurred in the past, and the table shows the historical performance of the S&P 500 since 1980 after such good overbought conditions were met. The market underperformed for two months but has a +70% odds of being higher after that with very asymmetric positive payoffs. One year later, there is an 89% chance of seeing a higher tape, with an average return of 15%. The current setback is consistent with a near-term setback, and given that trends are still positive (see below), the current outlook is favorable for stocks.

Speculative positioning on 10-year Tsy futures remains comfortably net bearish (i.e. betting yields will go higher). Interesting paradox with bullish stock market signals...if falling yields were a tailwind for stocks, rising yields could be an unfriendly environment.

ZH: Empire Fed Manufacturing Survey Suffers Biggest 2-Month Collapse (Ex-COVID) In History

I have a theory. WS is Powell's, the Fed's, and Pres/Congress's Biggest Boss. Therefore, the latest 'Powell Pivot', could be his End of Yr Bonuses guarantee to WS. After all, Powell ain't known as PE Powell aka Private Equity Powell for nothin. Would explain all the Open Mouth Fed Operations since start of the new yr.

Thanks for the explanation of the Banking system/ Rep Mkt and QT.....

Not sure I completely understand it.....have to re-read it more slowly....

Sounds like it could be a significant factor in the FED's decision and timing of Rate Cuts.

A Dovish factor....

A lot of moving parts in the Banking System these days and massive amounts of Treasuries

underwater....Seems like there is a growing pressure at the Short End and that the Financial

Condition of the Regional Banks is getting more strained ???

The Big Banks with their Trading/Investment Banking and Too Big To Fail Doctrine, will

always survive and almost have what they used to call the "Greenspan Put"....

Don't think that's going to change anytime soon...

Although I wish legislation would be passed to trim back the Risks the Big Banks take and

strengthen the Regional banks........that's well above my Pay Grade....

MM funds are bleeding off the Regional Banks depositors.....that is an inherent flaw in the system

It introduces systemic risk to the Regional Banks.....

I have a theory. WS is Powell's, the Fed's, and Pres/Congress's Biggest Boss. Therefore, the latest 'Powell Pivot', could be his End of Yr Bonuses guarantee to WS. After all, Powell ain't known as PE Powell aka Private Equity Powell for nothin. Would explain all the Open Mouth Fed Operations since start of the new yr.