weekly observations (01/16/24): 2024 the year of the steepener; 20s comeback kid MEANS more supply warranted OR "The Bond Market Rally Is Overlooking a Soaring $2 Trillion Debt Problem"

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

My apologies for the headline into your inbox from a Bloomberg story just this past week (and clearly a story that has been litigated over the decades without much resolution …).

Still waiting for HIMCOs Q4 thoughts and perhaps some of what follows will help pass time between now and whenever it drops onto the intertubes, help you sleep at night OR fill some time between now and playoff football (Bills vs Steelers POSTPONED due to cold weather, now MONDAY …).

What a week. It seems to ME — now extremely far removed from a front-row seat and window to the Global Wall Street world (ie Bloomberg Terminal) — that Global Wall Street is determined to celebrate The Year Of The Steepening (again).

It would seem to me (and I’m not totally alone) a bit curious how we’ve been recently BULLISHLY reSTEEPENING and while I think there’s a very significant distinction(s) to be made — bullish unflattening / bearish steepening — I do NOT believe those on Global Wall Street with a strategerist role care much.

They will likely only focus on the outcome while the distinction, in my humble much less educated view, makes all the world of difference to how one may be positioned (short / medium / long term).

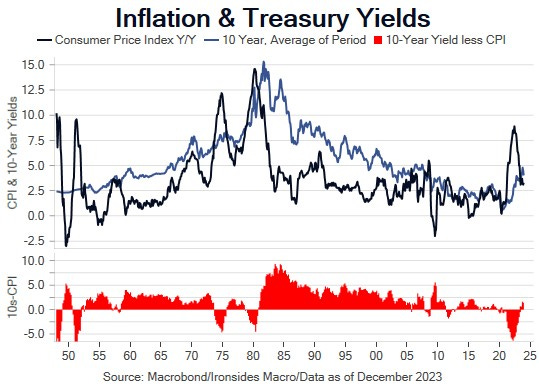

That said, a very mediocre look at 2s10s …

… there are those far smarter ‘out there’ looking at 5s30s un / dis inverted already …

… If I’m not mistaken, this was to be LAST YEARS ‘Trade of the Year’ and, like old Fed sayings, Mr. Market TO the world circa 2023, ‘when the facts change, I change, what do YOU do, sir …?’

So far this year we’ve got Laurie Logan LAST WEEKEND causing quite a stir with regards TO the balance sheet (last weekend’s note “… Logan SAYS …”) which was then followed by decisively INDECISIVE ‘flation data this week.

Team Transitory hanging hats and taking victory laps this weekend on PPI which they HOPE is sending a CLEAR message TO Fed’s favored PCE gauge…

… The sharp rally in 2-year Treasuries following an unfriendly CPI report on Thursday, was turbocharged by a soft PPI print on Friday, due to components from both reports that suggested the Fed’s preferred core personal consumption deflator would be cooler than CPI. The rally in 2s has the benchmark 2s10s curve within striking distance of disinversion at -22bp, 86bp steeper than the early July low at -1.08%. At the risk of sounding flippant, it appears the favorite fixed income 2024 trade is a steepener and traders are determined to press the bet whether the data and Fed communication is supportive, or not.

… lets HOPE (not a strategy) and only TIME will tell.

Thinking you KNOW the answer here and now, though, is likely a mistake (hence why they are called SURPRISES … refer, for example, back to ALL who said 2023 = The Year of the Steepening).

Or don’t. That’s fine.

NOW … lets deal with a couple / few things PPI and markets impact, related …

ZH: Core Producer Prices At Record High In December, Up 17% Since Biden Elected (great clickbait h’line BUT bullish steepening impulse cuz…)

… Excluding food and energy, the core PPI was unchanged MoM in December - the third month of unchanged in a row, which dfragged the Core PPI YoY down to +1.8% (the lowest since Dec 2020)...

ZH: Yield-Curve Dis-Inverts After 'Cool' PPI, Bullion & Bond Prices Bounce (so much for the h’line snark / spin, eh? note rate cut odds back UP and the bullish re steepening of the curve what caught my eye … )

… Ok I’ll move on AND right TO the reason many / most are here … some UPDATED WEEKLY NARRATIVES … some of THE VIEWS you might be able to use where, THIS WEEKEND, I’d note a couple / few things which stood out to ME this weekend …

BARCAP: Global Economics Weekly, “Disinflation now, supply-side risks later” (updated FED CALL — now MARCH — marking call to market pricing …)

We now expect a March Fed cut, with inflation data suggesting further softness in core PCE prints…

BMOs weekly, “Pressed for a Pivot” (covered short FedFunds — for small profit — better to be nimble and lucky AND good! except 10yr short still remains, stop not yet triggered :( )

DBsUS FI Weekly (joining the clarion calls for steepeners … this year will be diff, GOT to be, right?)

… Given our broader view that term premia are too low, we add a UST10s30s steepener (target 45bp, stop 0bp) to our macro portfolio.

Golidlocks: The Outsized Disinflationary Impact of Improved Supply (global economics strategery where a picture will help decide if you should click)

We Expect Core Inflation To Fall Meaningfully in 2024

MS: In a Bull Market for Bonds... (flat lookin’ to buy dips … stay LONG 10s vs 5s30s)

…one can only be long duration or neutral duration. We believe the bull market in core government bonds began late last year after Fedspeak and unfounded concerns about US Treasury supply created a picture-perfect bear trap. We stay tactically neutral, looking to buy dips, as downside risks arise…

MS: Friday Finish, “The Market Is Getting Ahead of Itself” (too many cuts priced)

NWM weekly (have cake, eat it too — standard ‘out there’ no matter what they can at some point say, they told us so…?)

…US Rates: Seeking a Tactical Pullback This week's data reinforces our near-term tactical view of a US rates consolidation in the least and potentially that of a measured pullback in yields. To be sure, the data was not significantly strong, but a slightly stronger than expected CPI report and ongoing resiliency in claims to us does not justify a further rally at this early stage, given what is priced in. We still see a tactical pullback as likely in the near term, reinforced by market technicals, though some flows are turning more supportive for US Treasuries.

Wells Fargo: Global Implications of a Soft U.S. Landing (don’t let yer friends fool ya, ain’t nobody like USofA when it comes to leaders — not individually speaking but rather as goes that saying, when the USA sneezes, the world catches cold … ok, so maybe NOT a saying but, well, you get the point)

… Stronger U.S. growth should allow the Eurozone and United Kingdom to recover more quickly from recession conditions, and given extensive trade linkages, should also offer support to activity in Canada and Mexico. Overall, we now see a more mild slowdown in global GDP growth from 2.9% in 2023 to 2.6% in 2024. Amid a firmer global growth backdrop, we also believe select central banks will adopt a more gradual approach to lowering interest rates. For the European Central Bank, Bank of England, Bank of Canada and Bank of Mexico, we expect rate cuts to now proceed at a more measured pace, with policy interest rates not leveling out until the second half of 2025.

Apollo: Why Is the Labor Market so Tight? (blame C19)

Foreign-born employment in the US is back at the pre-pandemic trend, and native-born employment is still 6 million jobs below the pre-pandemic trend, see the first two charts below.

In other words, the post-Covid normalization in the labor force participation rate has mainly been driven by immigration.

At the same time, the number of retired individuals has remained on trend, see the third chart.

The bottom line is that even taking into account that about 1 million died from Covid, there are still around 5 million native-born workers missing.

These 5 million missing workers are the reason why the labor market is tight and why wage inflation is likely to remain elevated.

Put differently, there is still plenty of room for job growth.

Bloomberg: Deutsche Bank Says US 20-Year Bond ‘Comeback’ Merits More Supply (good to know ahead of this coming weeks 20yr auction …)

Strategists say supply cuts since 2021 achieved their goal

February refunding ‘presents an opportune window’ for increase

… The 20-year “should win the comeback player of the year award if there was one for bonds,” Deutsche Bank strategists led by Steven Zeng wrote in a report Friday, adding the 20-year has occasionally become expensive for traders to borrow in the Treasury collateral market, signaling a scarcity of supply.

While the 20-year is once again the highest-yielding fixed-rate Treasury in the market following a steep drop in the two-year note’s yield on expectations for Federal Reserve interest rate cuts, it “saw a resurgence in popularity last year” marked by stronger demand for auctions, Zeng wrote.

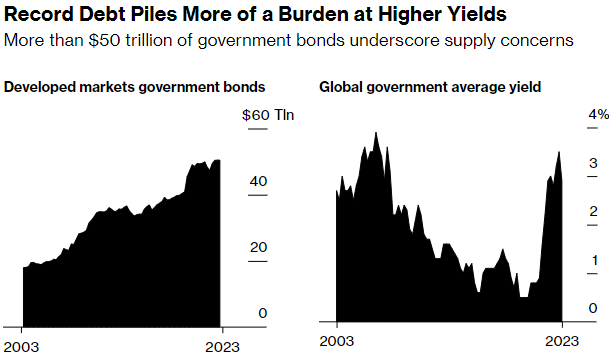

Bloomberg: The Bond Market Rally Is Overlooking a Soaring $2 Trillion Debt Problem

Investors are ignoring the cloud of rising deficits around the world.

… Public finances aren’t quite as bleak elsewhere but countries including the UK, Italy and France are all expected to post larger-than-normal deficits again this year. And a plethora of elections will keep those shortfalls in focus; BlackRock Inc. this week warned that Britain’s politicians could spark a selloff in the nation’s bonds if they try to win votes by pledging greater spending.

… “The Treasury has shown us that they are going to try to be pragmatic about where they issue on the curve and when,” said Rebecca Patterson, formerly chief investment strategist at Bridgewater Associates from 2020 to 2022, and an early proponent of the case for higher yields. “That’s reassuring at the margin but it doesn’t change the bigger picture. The supply of debt we need to issue to fund the government spending and to fund the deficit absolutely is an ingredient in where bond yields settle.”

It’s also a driving force in how investors decide which bonds they want to own. So far, one of the big trades for 2024 is a bet that US debt with a lifespan of 10 years or more will return less than shorter-term securities, because longer-dated bonds are more sensitive to worries over the deficit.

DC Lite #46 (equity returns in week ahead via BESPOKE — food for thought)

… MLK week returns. "The holiday-shortened MLK Jr week hasn't been a particularly good time for the market."

Guggenheim: 11 Macro Themes for 2024 (where #8 and 10 caught MY eyes)

Guggenheim Investments’ Macroeconomic and Investment Research Group identifies 11 trends we believe are likely to shape monetary policy and investment performance this year.

Record Global Elections and Geopolitical Instability Will Lift Economic Uncertainty

Technological Innovation and Competition Will Continue to Transform the Economy

Massive Treasury Issuance Will Continue to Weigh on Rates and Crowd Out Other Issuers

The End of the ‘Free Money’ Era Will Burst Lingering Asset Price Bubbles

Commercial Real Estate Stress Will Intensify and Spill Over to Small Banks

Private Credit Will Cannibalize Banks' Role in Leveraged Credit Further

Resilience Gives Way to Bifurcation

Negative Money Supply Growth and Draining of RRP Are Key Risks and May Usher in Deflation

Soft Landing Hopes Will Give Way to (Mild) Recession

Fed Easing Cycle Will Drive Long-End Rates Lower Than Anticipated

Morningstar: Stocks Have Not Always Beaten Bonds. Should You Care?

How relevant are the experiences of other countries and other eras?

WolfST: Fed Reports Operating Loss of $114 billion for 2023, as Interest Expense Blows Out (ruh roh, RelRoy … govt gonna have to find some other source of funding other than USTs owned and oh, by the by … not just SVB with losses to contend with but thankfully, Fed can / does simply HTM them all, unless, of course, Laurie Logan has other ideas?)

Yardeni DEEP DIVE: The True Story About Long & Variable Lags In Monetary Policy (here’s a look at 3 of his top 7 focal points)

How long is the lag between monetary policy tightening and recessions? In the past, the answer to that question depended on how long it took the federal funds rate to rise to levels that triggered financial crises that morphed into credit crunches, which quickly caused recessions. Past federal funds rate hiking cycles tended to peak when financial crises resulted from rising interest rates and tightening credit conditions (Fig. 1 below).

Prior to these events, the yield curve tended to invert, reflecting investors’ anticipation that restrictive monetary policy likely wouldcause something to break in the financial system, forcing the Fed to ease (Fig. 2). Inverted yield curves indicated that bonds were becoming more appealing to investors than money market instruments, as they reasoned that locking in long-term rates in bonds made more sense than getting caught in short-term instruments when their interest rates came tumbling down.

Research by Melissa and me, which we’ve discussed often in recent years, supports our thesis that inverted yield curves forecast a process that often—but not inevitably—leads to a recession. Tighter money eventually causes a financial crisis, which turns into an economywide credit crunch. It is the credit crunch that causes the subsequent recession, not higher interest rates per se nor inverted yield curves. (Download a free copy of our 2019 study titled The Yield Curve: What Is It Really Predicting? for a deeper explanation of our thesis.)

The alternative and widely held thesis—that there are long and variable lags between the tightening of monetary policy and a recession—assumes that rising interest rates depress demand, which inevitably sets off a recession. We disagree. In our opinion, the timing question boils down to this: “When the Fed is raising the federal funds rate, how long will it take before it gets high enough to break something in the financial system?”

So far, the latest round of Fed tightening did cause three banks to fail last March, attesting to the vulnerability of links in the financial system chain when rates are rising. But the Fed averted a credit crunch by rapidly providing liquidity through a new emergency lending facility dubbed the “Bank Term Funding Program” on March 12, 2023. As of the week of January 3, it had provided $132.8 billion of liquidity to support the banking system (Fig. 3 below). Averting a credit crunch also avoided a recession, so far at least.

Meanwhile, Fed officials signaled in their December Summary of Economic Projections that they are done raising the federal funds rate and expect to be lowering it three times in increments of 25bps this year. The financial markets have been discounting this easing scenario since October 19, when the 2-year and 10-year Treasury yields peaked at 5.19% and 4.98% (Fig. 4). They were down to 4.40% and 4.05% on Friday. The 30-year mortgage rate is down by about 100bps since early November.

So now the question is whether the recent easing of financial conditions will offset any of the long and variable lags of the Fed’s restrictive policy over the past two years. We think so. Let’s have a look at this issue with the help of past and current relevant data. Before doing so, we want to reiterate that we are proponents of our credit crunch theory of recessions rather than the widely held notion that the long and variable lags of monetary policy can still cause a recession this year. Consider the following:

(1/7) Consumer durable goods. Real consumer spending on durable goods is one of the most interest-rate sensitive components of real GDP. Its growth rate tends to slow during monetary policy tightening periods (Fig. 5 below). Interestingly, it then tends to turn negative during the initial period of monetary easing, which usually coincides with a recession. So in the short term, it slows and then turns negative at about the same time that the Fed starts easing.

This could conceivably happen now. However, consumers were already slowing the pace of their durable goods purchases in late 2021, before the Fed started to tighten. As we’ve noted recently, the data suggest that the rolling recession in the goods sector is bottoming and could morph into a rolling recovery for goods producer and distributors this year. Indeed, the growth rate of real spending on durable goods rose to 6.7% in November.

(2/7) Housing starts. The most interest-rate sensitive component of real GDP is residential construction. Housing starts often has peaked early during monetary policy tightening periods and then plummeted. Home building then rebounded sharply once the Fed started cutting interest rates.

This time, the Fed hasn’t started to cut interest rates, but the mortgage rate is down sharply, and housing starts is showing clear signs of bottoming. If the rolling recession in housing activity morphs into a rolling recovery this year, as we expect, then the housing-related retail sales should rebound too (Fig. 6 below).

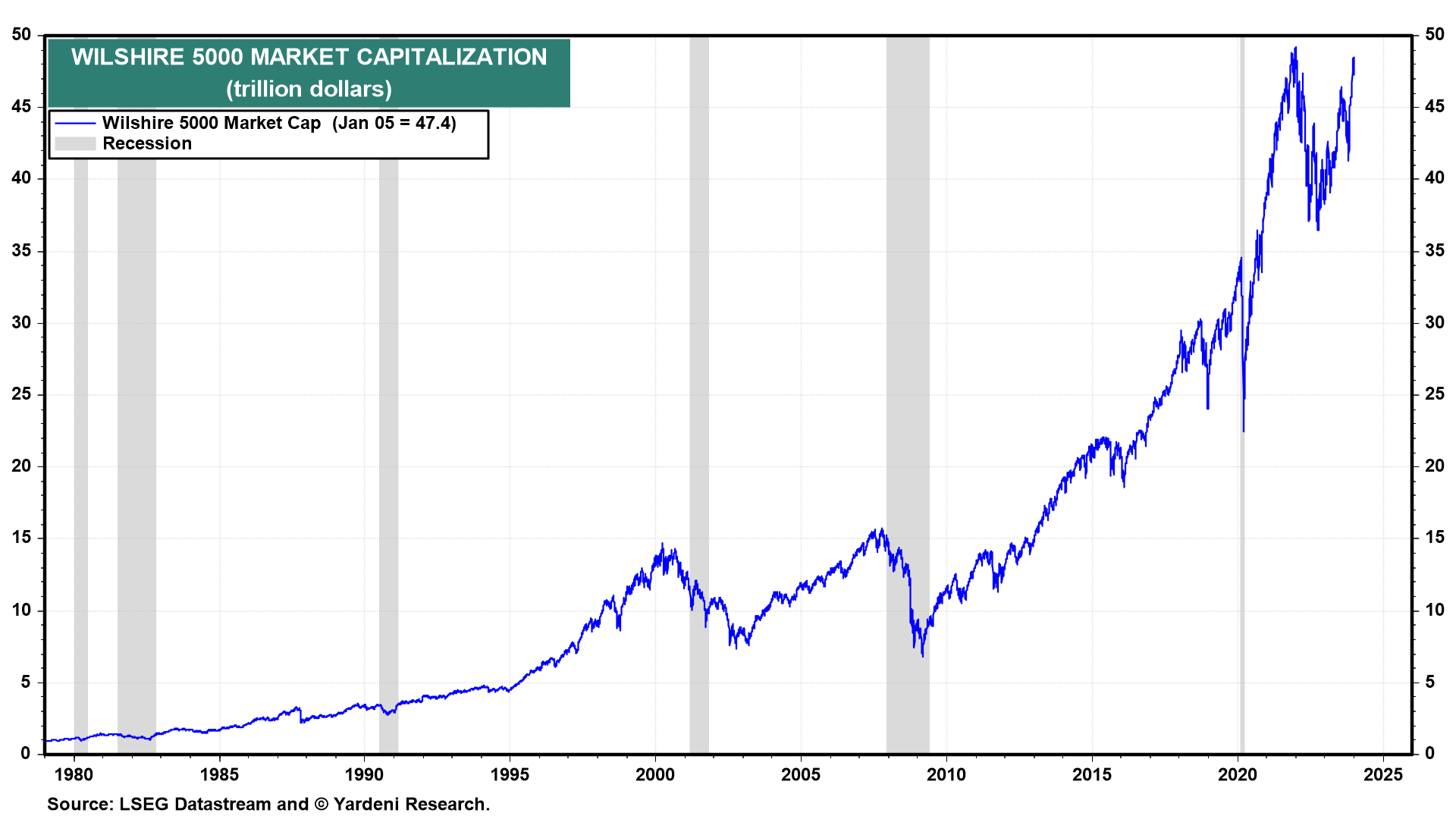

(3/7) Wealth effects. During the 1960s through the 1990s, financial crises invariably were followed by significant rallies in the stock and bond markets (Fig. 7 and Fig. 8). Such rallies have wealth effects that should boost consumer spending. This time, the Wilshire 5000 rose to $47.4 trillion on Friday (Fig. 9 below). That’s up $12.9 trillion since February 20, 2020, just when the pandemic started, and almost matches its record high during January 3, 2022.

… AND for any / all (still) here, reading — you’ve got bigger issues than I suspected (and likely why you subscribe :)) and interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

The amount of 60+ White Guys working as Cashiers or Mechanics is interesting....being not too far behind it's comforting to see employment's still available!

{kind=link}

Agree, with Labor Market thoughts...

Lots of FI paper being auctioned this week....the New Normal....

Great newsletter !!!

The amount of 60+ White Guys working as Cashiers or Mechanics is interesting....being not too far behind it's comforting to see employment's still available!