Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Meet the new year, same as the last year … Lets jump right in.

With yesterday’s pre NFP note / thoughts in mind (options traders, CME FedWatch Tool and 5yy) I’d like to begin with an updated look at 5yr UST yields on a WEEKLY (so a medium term) basis) …

… zero for too long helped push me OUT of a front - row seat and while you can push the guy outta the FI markets you cannot take the FI markets outta the guy and looking at an updated WEEKLY visual of 5s, I’d have to say I’m more bearish than bullish (higher before lower) at least within an intermediate framework. I AM intrigued at how well Mr. Market fleshes out points of interest and STOPS on a dime. Doesn’t hurt that the belly here coincides with what maybe psychologically important 4.00%

Be that as it may we’ve got duration for sale this week and that is likely to be a challenge DESPITE / because of data clarity in the week just passed. Through the week just ahead I’ll attempt to focus on the here / now OF 3s, 10s and bonds when they are coming noting long bonds to be auctioned just after CPI Thursday …

Before we get THERE, let us consider some fresh FEDSPEAK from Laurie Logan, pres of Dallas Fed (non voter, per FOMC 101) just offered SOME fresh insights and while she’s NOT a voter, she WAS in charge of markets for FRBNY and so, as they say, all opinions are created equally BUT some are simply MORE equal than others.

FRB of Dallas: Opening remarks at panel on Market Monitoring and the Implementation of Monetary Policy (i’ll highlight just one funTERtaining fact)

… a lot of the effects of higher rates are already behind us, and the recent easing in conditions could start to push up on aggregate demand. The Chicago Fed’s FCI, which statistically combines 105 different financial variables, shows that conditions are modestly less restrictive than a year ago and than their average over the past half century.

As I said earlier, if we don’t maintain sufficiently tight financial conditions, there is a risk that inflation will pick back up and reverse the progress we’ve made. In light of the easing in financial conditions in recent months, we shouldn’t take the possibility of another rate increase off the table just yet…

Oh. Ok. But then … what about yesterday? Lets get to it and while there’s PLENTY of NOISE as opposed to signal out there, I’ll just caution we take it all in and recognize it for what it is. That said …

NFP and Markets to all of Global Wall Street: Heads I win, tails you lose (?)

Apparently there is some new math ‘out there’ and it’s something like this:

ISM > nfp = X (please solve for “X” and WHY — see visual just below)

… The payrolls data came in good enough to drag a few more people into the higher yields trade and then ISM dropped an absolute anvil on the market.

US 10-year yield, 5-minute chart this week

In the end, next week’s CPI matters much more …

… Never have truer words been spoken? SO,

CPI > ism + nfp = X (please solve for X … ? perhaps we should check in with OPTIONS TRADER(S)?

Now lets deal with a couple / few things NFP related items …

BondDad: December jobs report: consistent with a “soft landing,” despite discordance in household data CalculatedRisk: December Employment Report: 216 thousand Jobs, 3.7% Unemployment Rate

ZH: Jobs Shocker: December Payrolls Unexpectedly Surge As Unemployment Rate Slides, Wages Jump ZH: Stocks, Bonds, & Bullion Dump As Rate-Cut Hopes Plunge Post-Payrolls ZH: Inside The Catastrophic Jobs Report: Record 1.5 Million Crash In Full-Time Jobs, Multiple Jobholders Soar To Record, Native Born Workers Plunge And Much More WolfST: A Jobs Report of an Economy Plugging Along Just Fine Despite 5.5% Rates & Recession Fears. But Wage Growth Heats Up

Now with a few NFP related links in hand, on to some OTHER data which helped shape shift the trading post NFP

ZH: ISM Services Plunged In November, Employment Crashed ZH: US Factory Orders Surged In November - Biggest Jump Since Jan 2021, But...

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

THIS WEEKEND I’d note a couple / few things which stood out to ME from Global Wall Street’s research machine … I’ve carried forward same setup as LAST YEAR (here’s December edition for any / all having trouble sleeping at night and / or missed year ahead outlooks which have already had to be re written!). I will try to keep this (paywalled, protected) stuff separate and different (and so, down below with things you might very well have stumbled upon via the intertubes…)

Global Wall Street has a few words (recaps and victory laps) on NFP …

BMO- Strong enough to Challenge March Cut pricing (also note weekly writeup where they remain more BEARISH and are now SHORT 10s…while ALSO fading rate CUT pricing…) Bloomberg BNP jobs report: Cooler in details, but faint green shoots Goldilocks: Payroll Growth Picks Up to 216k; Unemployment Steady on Sharply Lower Participation; Average Hourly Earnings Stronger than Expected ING — Fed gonna wait ‘til MAY before cutting JEFF - Dec Employment: Payrolls and Wages Continue to Surprise to the Upside, but Household Survey Shows Signs of Cooling JPM took profits on ‘tactical 30yr shorts’ on THURSDAY (steeling defeat from the jaws of victory? just kiddin…) MS: December Employment - Tight Labor Market

… We do not think the labor market is showing the slowdown needed for the Fed to cut soon and think a bumpy path ahead on inflation will keep the Fed from cutting before June, when we expect the first 25bp cut…

Wells Fargo: December Employment: Still Chugging, but Losing Some Steam

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW … some of these may ALSO be NFP recaps / victory laps and just plain informational …

Bloomberg: Logan Says Fed Should Slow Asset Runoff as Reverse Repo Dwindles

Bloomberg: Treasury Market’s Wild Day Boosts, Then Batters, a Big Options Bet

Large options trade targeted 10-Year yield surge past 4.15%

Wager gained after jobs but turned lower after services data

Bloomberg TWEET by Anna Wong (chief econ) AT AnnaEconomist (ISM > nfp)

ISM employment plunge vs NFP blowout — which one will the Fed believe? Here is an employment intentions diffusion index we constructed from regional Fed surveys: it shows a similar steep drop as ISM.

Bloomberg(via ZH): The 10Y Yield Levels To Watch For After Payrolls (offered BEFORE NFP and with a bit of a Goldilocks — GS — reaction MATRIX for stocks, and so, am offering as a bit of a ‘howd they do’, if you will…)

This is a chart that people will be talking about for a long time now. This shows the ISM Services Employment Index. Services have been extremely strong for the last few years and it’s been a consistent bright spot in the economy. It’s been so strong that it’s forced the Fed to reconsider their position at times in the last few years as services inflation has remained stickier than the Fed is comfortable with. But we may be seeing the tide change and there’s a chance here that it’s changing in a big way. Now to the data….

…In the end I’d argue that this data marginally increases the odds of a rate cut in Q1. It raises the odds of an emergency rate cut from virtually 0% to something now materially higher. So, it’s not a sign to panic by any means, but it’s also a reason to be skeptical of what’s happening at a broader macro level because the digestion of the Covid excesses isn’t over just yet and we shouldn’t be surprised by…surprises.

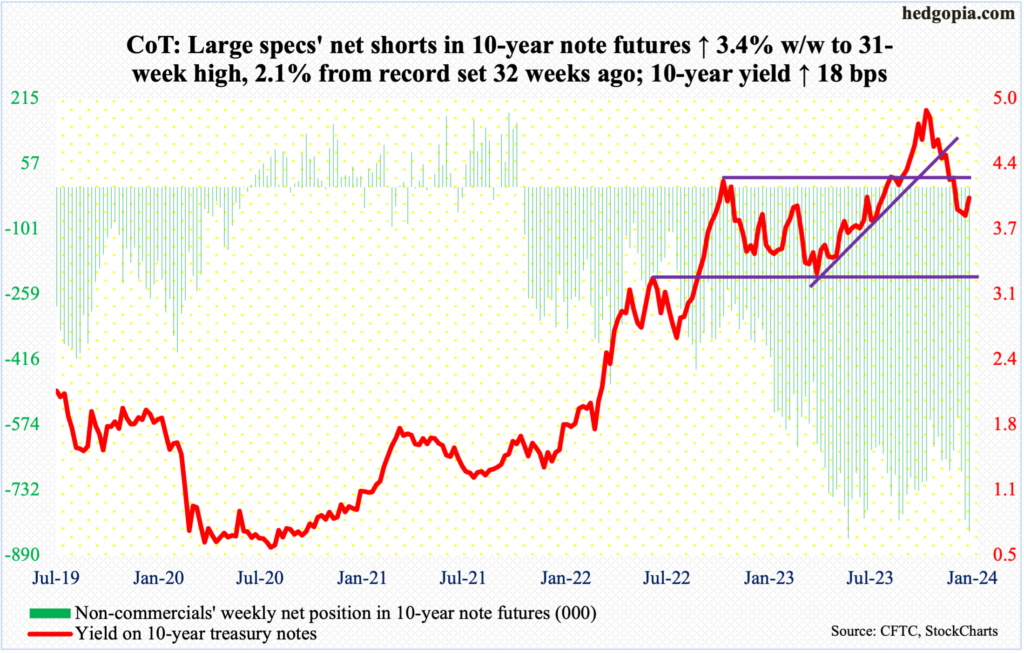

SHORTS REBUILDING … hmmm, seems ‘bout right to ME especially in light of SUPPLY in the week ahead, no? Moving on …

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Funny thing that Animal Farm, or 1984, or Orwell, Exec order 6102, Goebbles Principles of Propaganda, and Marx's Communist Manifesto, were excluded from my Public Education....

{kind=link}

A WEAK ISM and after a deeper dive, a "weaker" NFP....

The ISM maybe a "canary in the coal mine".

In January, there are always a lot of COLA to wages, not surprised at the slightly higher wage growth.

The BLS downward revision continue, on schedule.....The Politics of Headlines..

Is 4%, the new 5% ????

Be a fascinating week upcoming with the Bond auctions and the CPI and PPI eports.

Fed on Hold......March Cut seems early, unless things really deteriorate....

I always learn from reading your articles...

They are really great !!!

Thank you...

Funny thing that Animal Farm, or 1984, or Orwell, Exec order 6102, Goebbles Principles of Propaganda, and Marx's Communist Manifesto, were excluded from my Public Education....