(USTs lower/steeper on SOLID VOLUMES)while WE slept; "Attempting to Put the Toothpaste Back in the Tube" -JEFF on FOMC mins; H.O.P.E. IS, in fact, a strategy?

Data PLUS FOMC minutes combined for another NO HIT / AT BAT as Global Wall Street currently 0-2. Futures are pointing higher this morning (phew) BUT this less than optimal start alluded to yesterday (worst start in 20yrs, HERE) combined to put long bonds back above a TLINE and on MY radar screen …

… where I’ve attempted to highlight momentum — overBOUGHT for quite awhile — has moved HIGHER and so, moderating conditions and moving towards overSOLD. Not quite there YET but working towards that direction (on the dailies) and back of the envelope math using some TLINES / LEVELS i’ve kept on the visual (4.42 and 3.82) it would appear to ME we’re right smack dab in the MIDDLE of this range (4.12).

Whether or not tomorrows NFP will be definitive (for markets and / or the Fed) remains to be seen. I hope to have some sorta NFP recap / victory lapAthon out of the weekend.

For NOW, though and with yields on the move, it is always a good time to ask IF … someone said rate CUTS? Why, yes …

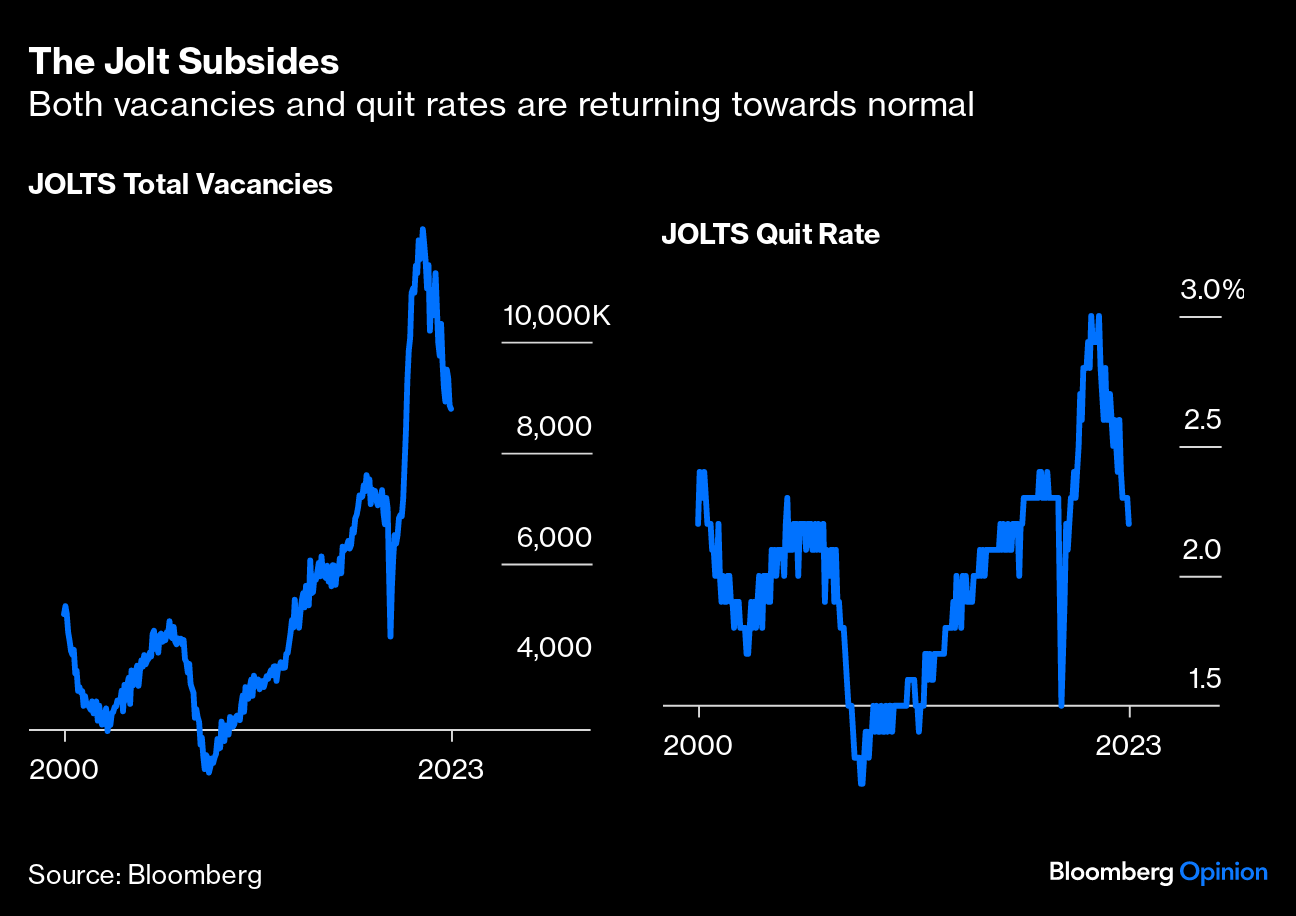

ZH: ISM Manufacturing Contracts For 14th Straight Month, New Orders Sink ZH: Job Openings Slide To Three Year Low As Hiring Suddenly Craters Below Pre-Covid Levels, Quits Tumble BMO: ISM improves, JOLTS disappoints -- TSY bounce off lows

… of course. I’ll take some, please … no matter the data or HOW it’s spun, or the message intended, the end result is and can only / always be, that rate cuts are the answer.

But … wait, data interpreted one way, and then the FOMC mins dropped …

ZH: Fed Minutes Push Back On Powell's Dovish Pivot

… These Minutes in no way support a 150bps rate-cut cycle next year …

CalulatedRISK: FOMC Minutes: "A lower target range for the federal funds rate would be appropriate by the end of 2024"

… its my blog post and I’ll conflate / confuse matters as much as I see fit and can? There will be more hemming, hawing and gnashing of teeth and over / mis interpretations below from Global Wall Street, rest assured but to me … well, the message delivered and heard seems, well clear (as mud)? FOMC mins wordcloud

ZH and I am not alone with interpretation that maybe, just maybe Mr. Market priced for too much in way of CUTS.

Bloomberg VIDEO: BlackRock’s Li:" Market ‘A bit Too Overly Hopeful’ on Fed Cuts

Stocks and bonds seem to have gotten a message …

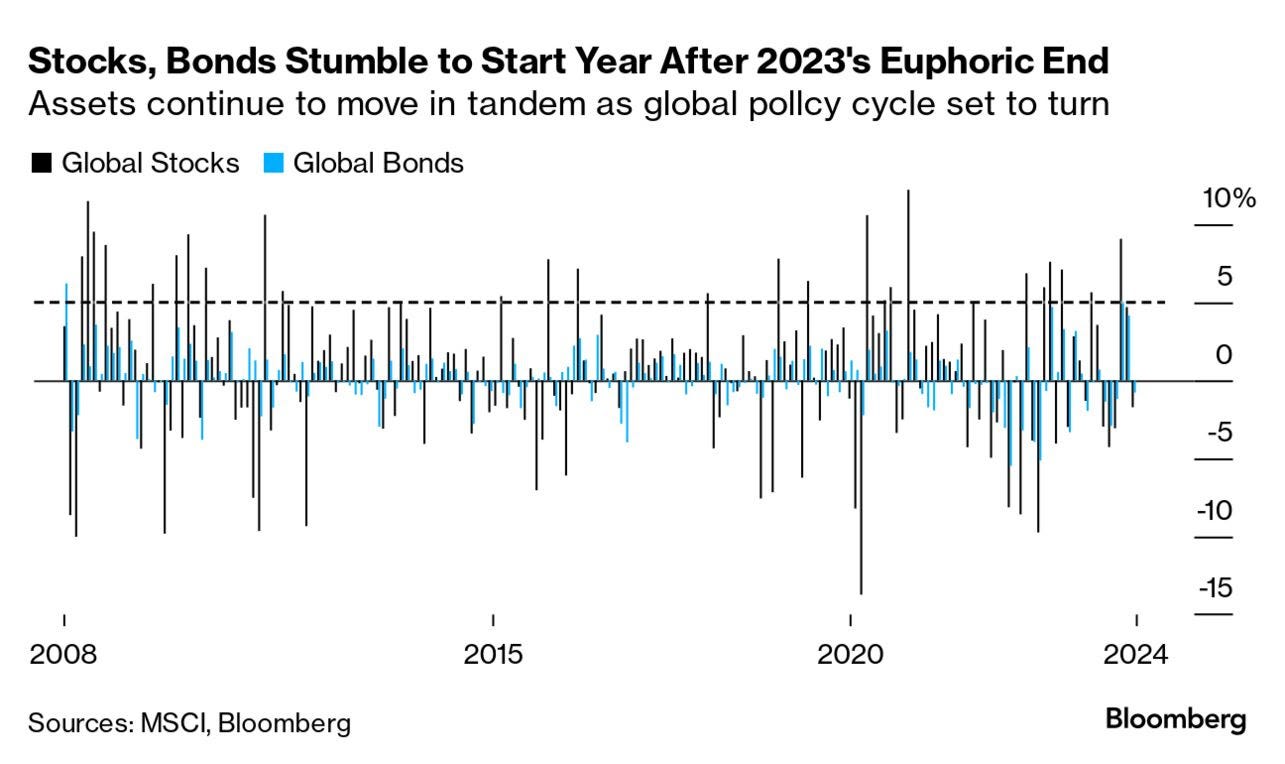

ZH: Global Bonds & Stocks Suffer Biggest Rout To Start A Year Since 1999

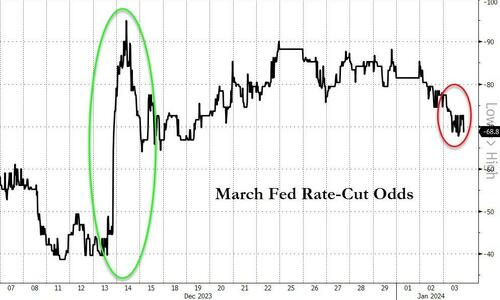

… The FOMC Minutes today were significantly less dovish than the market (and Jay Powell) suggested and March rate-cut odds faded modestly...

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with curves steeper again this morning as EU supply and PMI/flash CPI readings in Europe weighed a bit. DXY is lower (-0.2%) while front WTI futures are higher (+1.1%). Asian stocks were mixed, EU and UK share markets are also mixed while ES futures are little changed here at 6:50am. Our overnight US rates flows saw overall Asian session flows skewed toward selling in intermediates with decent real$ buying in the front-end noted as well. In London hours we saw early selling from real$ in 10's to 30's and later real$ buying in 5's to 7's with the front-end of the curve generally holding in well despite the back-end cheapening. Overnight Treasury volume was quite solid at ~180% of average overall with 30yrs (249%) seeing some relatively standout average volume this morning.

… and for some MORE of the news you can use » The Morning Hark - 4 Jan 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

The minutes of the December FOMC meeting show that policy makers noted the clear progress on inflation but were in no rush to cut rates. We continue to expect the FOMC will initiate an every-other-meeting rate cutting cycle starting in June…

… We retain our baseline rate call: We expect the FOMC will initiate an every-other-meeting rate cutting cycle in June, implying three 25bp cuts in 2024 to a target range of 4.50-4.75%, and four more cuts in 2025. This is much less than what is implied by market pricing, which shows six cuts through end-2024, starting in March. However, if core PCE inflation consistently runs below 0.2% m/m in the lead-up to the March meeting, the FOMC could begin cutting then.

Barcap: Another mixed manufacturing ISM to end 2023 (wait, MIXED? I thought it was an absolute trainwreck — 14mo in a row, etc…)

The ISM manufacturing composite improved slightly in December, consistent with renewed resilience following the UAW strike. Movements across major components were mixed, with production and employment firming, new orders softening, and indications that deflationary pressures were restored following a November lull.

… The prices paid index returned to the deflationary range it had occupied since midyear after having firmed briefly in November…

Bloomberg BNP: US December FOMC minutes: Cuts coming? Not so fast

KEY MESSAGES

The December FOMC meeting minutes showed broad consensus that the current policy setting is appropriate, but a high degree of uncertainty about the outlook.

Fed officials agreed about inflation’s recent progress, but not about the extent to which that would continue.

The minutes lean against notions that rate cuts are imminent, emphasizing potential reasons to hike further or hold for longer as opposed to cutting earlier or faster.

The data will have the final word. Provided conditions play out in line with our base case, we think Fed officials will want to see more evidence before making an initial cut, ultimately in May, in our view.

… Looking further afield, divergence grows. Specifically, “participants generally perceived a high degree of uncertainty surrounding the economic outlook.” Later in the minutes, participants noted an “unusually elevated” amount of uncertainty with respect to their outlooks. They cited upside risks to economic activity and inflation including the easing in financial conditions ahead of the meeting, with “many” remarking that easing [financial conditions] “beyond what is appropriate” could make it harder to achieve the inflation target. To the downside, there was the possibility that lagged effects of past policy changes may be larger than expected.

BloombergBNP: US December jobs preview: Modest cooling may stir, not shake Fed

KEY MESSAGES

Our base case is for the December jobs report to show enough resilience across key dimensions to stave off expectations of an imminent Fed rate cut.

We estimate companies added 165k jobs, down from 199k prior. That would put job creation back onto a gradual downward trajectory after strike-distorted October-November readings.

Layoff activity tailed off into year-end, likely reflecting the pickup in economic growth seen in H2 2023.

We project the unemployment rate to bounce back to 3.9% from 3.7% prior, possibly exaggerated by normalization after strike effects in October-November.

FirstTrust: The ISM Manufacturing Index Increased to 47.4 in December

… Implications: The December ISM report tied a bow on what was a lousy year for the US manufacturing sector, as activity contracted for the fourteenth consecutive month, the longest streak since the aftermath of the 2000-2001 recession…We continue to believe a recession is lurking in the year ahead and the details of today’s report suggest the goods sector of the economy is likely to lead the way…Despite sluggish activity, survey comments were surprisingly upbeat, largely due to optimism around the Federal Reserve effectively declaring “mission accomplished” at their meetings in December, which they believe will encourage more companies to resume spending on capital investments …

BOTTOM LINE: The minutes to the December FOMC meeting noted deletion that participants viewed the policy rate as “likely at or near its peak for this tightening cycle.” We saw comments in the minutes on inflation progress to date and the inflation outlook, risks to growth from keeping rates too high, and how long the policy rate would need to remain restrictive as dovish. We continue to expectthe first rate cut in March and 5 cuts total in 2024.

Goldilocks: ISM Manufacturing Rises but New Orders Measure Falls Further; Job Openings Broadly in Line With Expectations

BOTTOM LINE: The ISM manufacturing index rebounded slightly more than expected to 47.4 in December. The composition of the report was softer, with decline in the forward-looking new orders component. Job openings declined by 62k to 8,790k in November from an upwardly revised 8,852k in October, broadly in line with expectations. Job openings have remained stable in recent months. After incorporating today’s JOLTS data, our jobs-workers gap based on the JOLTS, Indeed, and LinkUp measures of job openings stands at 2.5mn workers in December.

JEFF: FOMC Minutes: Attempting to Put the Toothpaste Back in the Tube

■ The Minutes to the Dec 12-13 FOMC Meeting read quite a bit more hawkish than Chair Powell's post-meeting press conference. ■ Powell said that the question of "when to begin reducing accommodation" was discussed at the meeting, but the language of the Minutes seems intentionally contorted around avoiding such dovish phrasing. Instead, the Minutes described "risk-management considerations" that would be appropriate if they were to "face a tradeoff between its dualmandate goals". ■ Powell's indications that the Fed was likely done with rate hikes after the November and December FOMC Meetings have caused a dramatic easing in financial conditions that the Committee is clearly not comfortable with. They indicated that "an easing in financial conditions beyond what is appropriate could make it more difficult for the Committee to reach its inflation goal". ■ Earlier this morning, Richmond Fed President Barkin noted that a soft landing was becoming increasingly likely, though by no means guaranteed. He also gave no indication that the Fed would cut any time soon. The Minutes convey a similar tone that acknowledges reality, but does not cause financial conditions to ease further.

JEFF: Dec ISM Mfg PMI Shows 14th Straight Month of Contraction, and Little Hope for a Near-Term Turnaround (14mo in a row and NO HOPE aka RATE CUTS NOW!!)

■ The December ISM Manufacturing PMI improved to 47.4 from 46.7, which was the lowest level since July. This is the 14th month in a row below 50. Broadly, the manufacturing data has been weak for quit a while and today's ISM report show no signs of any significant changes. ■ The ongoing 14-month streak of sub-50 readings is the longest since August 2000 through January 2002 (18 months). The environment for capex investment remains very challenging due to high rates and uncertainty about the economy. The feint hope of rate cuts coming around the corner offers some upside risk for the sector going forward, but it is still a long way off from recovery. ■ Supplier deliveries remain well under 50 for the fifteenth straight month, and the index remains near the lowest level since 2012. This is a good sign of further improvement in supply chain problems but it also likely represents further weakness in current demand as well. ■ The Prices Paid index fell to 45.2 from 49.9 returning to just above the bottom-end of the range since Q3 2022. The index has been below 50 in 13 of the last 15 months. The data show no strong signs of any change in the ongoing trend of goods disinflation.

We estimate payrolls rose 180k in December (172k excluding strike effects). The unemployment rate likely rose to 3.8%, but is on the cusp of an unchanged 3.7%, amid further labor force gains.AHE increased 0.3%. Retail and transport payrolls are risks, along with unstable seasonal adjustments.

Watching, waiting but the FOMC seeing progress on inflation As we wrote in the preview of these minutes, we expected the FOMC to continue to note monetary policy would need to remain restrictive for some time and that the Committee remained resolute in their determination to restore price stability. Check and check.

"Participants generally stressed the importance of maintaining a careful and datadependent approach to making monetary policy decisions and reaffirmed that it would be appropriate for policy to remain at a restrictive stance for some time," wrote the minutes.

"Participants continued to be resolute in their commitment to bring inflation down to the Committee’s 2 percent objective," wrote the minutes.

We also noted this would be balanced by acknowledging the progress on inflation, and noting the Summary of Economic Projections, which showed only rate cuts were assumed to be appropriate policy going forward. "...almost all participants indicated that, reflecting the improvements in their inflation outlooks, their baseline projections implied that a lower target range for the federal funds rate would be appropriate by the end of 2024." …

UBS (Donovan): Whatever you thought about the Fed is confirmed (thanks)

The Federal Reserve minutes of the December FOMC meeting suggested rate cuts were self-congratulatory about the decline in US inflation (though this was only partly due to the Fed). They signalled rate cuts this year. They also signaled no rush to cut rates, and interestingly mentioned that activity may be stronger than reported. Economic indicators designed in the 1920s struggle to accurately measure modern ways of working in the 2020s.

The minutes confirm whatever you wanted to think about the direction of US interest rates before the release. I would suggest they are consistent with three rate cuts, starting later than March—but that was my bias before the minutes…

Job openings fall to 8.79 million in November; quits drop too Job openings fell a modest 62K in November to 8.79 million. The job openings rate held steady at 5.3%, and for the private sector held steady at 5.5%, remaining elevated relative to history (see Figure 1). Today's estimate from the BLS' Job Openings and Labor Turnover Survey left openings at the lowest level since March 2021 and down 27% from the peak in March 2022.

Wells Fargo: ISM: There Was no Soft Landing for Manufacturing in 2023

Summary December marked the 14th month of contraction for ISM manufacturing, at least it was a slightly milder pace of contraction. Production is back above 50 and November's jump in prices proved to be the anomaly we suspected it would be. Labor prospects remain dim.

Wells Fargo: FOMC 101 (I actually keep this one printed on my desk so as I can refer TO whoever is speaking and verify … while we KNOW all opinions are created equally, SOME are more equal than others)

… And from Global Wall Street inbox TO the WWW,

Bloomberg Five Things You Need to Know to Start Your Day (Asia … reminder 2,456,777 of how bad first couple days of year have been so far)

… Stocks and bonds are off to a poor start for 2024, but so far that simply helps to underscore the perception that the rallies at the end of last year went careening too far, too fast. Bloomberg’s global bond index jumped 5% in December for its biggest gain since the final month of 2008 when the Federal Reserve slashed its interest rate to the zero bound and signaled a willingness to pump money into the economy. MSCI’s All-Country World Index of shares had a more modest advance last month, but coming on top of November’s fireworks it posted the best two-month surge since the end of 2020.

We are well and truly in hangover territory, it seems, after the wild party to end 2023. The more sobering thought is that bonds and stocks look to be extending the trend of moving strongly together, in rallies and in routs. At some stage, that dynamic is likely to break, and investors are nervously waiting to see whether bonds or stocks end up losing out when the two part ways.

Bloomberg (via ZH): Treasuries Send Out An Early Message of Caution On 2024 Trades

By Ven Ram, Bloomberg Markets Live analyst and reporter

As traders prepare for the release of Fed minutes, the markets are telegraphing an early, if somber, message: so much of the putative trades of 2024 were front-run in the past two months that chasing that theme may no longer be as rewarding.

Consider Treasuries.

The yield on two-year notes declined by almost 85 basis points through November and December. If you take the Fed at its word that it intends to cut its benchmark rate three times this year, you have to wonder how much further the emphatic rally can go.

Further out the curve, the 10-year yield slumped by more than 100 basis points over the same period. Even so, given rapidly crumbling inflation in the US and a Fed bracing itself to cut rates, this maturity is trading more or less around where it ought to. However, because the tenor is fully valued now, further gains will be hard to come by.

Stocks tell much the same story.

Equities seem to have won a prescriptive right in recent years to rally regardless of what happens to interest rates, an untenable script that can’t be glossed over forever. The Nasdaq 100 surged more than 15% through the last two months of 2023, and despite Tuesday’s correction, technology stocks are already trading as though their valuations are discounted by Fed rates that are far lower than current levels. Hence it should be challenging to drive valuations higher and higher. While the S&P 500 was far less exuberant through November and December, the basket is also mildly overvalued given a fair value of 4,632.

The extraordinary moves in Treasuries and stocks of the past two months provide the context for the minutes of the Fed’s December meeting.

With Chair Jerome Powell having expressly stated that policymakers discussed a time line for reducing rates, traders will be keen to find out whether a March cut is still in play. Indications from New York Fed President John Williams suggest a reduction in March may be too early.

If the minutes reinforce that message, a continuation of the correction in Treasuries is likely.

Bloomberg: If Only We Knew the Problems Facing America's Banks (Bill DUDLEY — former FED insider — OpED and a reason for PAUSE …)

Almost a year after Silicon Valley Bank's failure, the Federal Reserve is still keeping the public in the dark about the deficiencies it finds at US lenders.

Bloomberg: Coming Rate Cuts Portend a 1980s-Style Economic Resurgence (see ‘toon below for synopsis?)

Bloomberg: Goldilocks has markets coming and going (Authers OpED)

… The latest bulletin from the US labor market is also almost perfectly in line with a Goldilocks outcome. The rate at which US workers are quitting their jobs, which hit an all-time high during the post-pandemic Great Resignation, is now back in line with the norm. The total number of vacancies remains elevated, but is falling fast. That suggests heat leaving the jobs market (“not too hot”), but no serious decline (“not too cold”):

To add to this, manufacturing supply manager surveys show a slight recovery. The PMI data remain just below 50, intended as the demarcation point between expansion and contraction, and new orders are also unimpressive. But the survey suggests that both a recession and an overheating can be avoided:

So comforting was this data that 10-year bond yields even managed to fall after the publication of the minutes from December’s Federal Open Market Committee meeting provided no hints that Federal Reserve was really prepared to cut as early March. Belief in Goldilocks is strong. And that’s important because the market, by betting on Goldilocks, has made it easier for such a scenario to happen. Rising prices for stocks and bonds tend to ease financial conditions. Judging by Bloomberg’s own measure for the US, they are now their easiest (expressed in positive territory in the chart below) in almost two years, since before Russia’s invasion of Ukraine.

What then are the problems with Goldilocks? Conceptually, such an economy generally only delivers great returns if nobody expects it. When markets have already set themselves up for just such an outcome, as we’ve just covered, not too hot, not too cold outcomes don’t help that much.

Investopedia Chart Advisor: Evaluating Exogenous Factors (where it appears that H.O.P.E. IS in fact a strategy?)

… 3/ H.O.P.E

Source: StayVigilant.Substack.com, Bloomberg

A simple way that strategists have tried to capture this housing dynamic is in the acronym H.O.P.E. This stands for housing -> orders -> profits -> employment. The acronym covers how money/stimulus flows into and out of the economy. As lower rates make housing more appealing, the housing market picks up. This leads to a range of new orders for lumber, roofing, windows, copper and even furniture and landscaping. As companies start to process these new orders, they will start to generate profits. It is only after a company has been profitable for some time, that it starts to add workers and employment improves. This works in reverse too as a housing slowdown leads to a reduction in orders, declining profitability and then layoffs.

The third chart shows you visually this H.O.P.E. dynamic using the NAHB Index for housing, the ISM New Orders measure, S&P adjusted earnings per share and finally the yearly change in US labor force. As we look back through time, we can see that housing in white leads new orders in green. The next line to move is the profits in red and finally the employment in blue. The employment data is the most lagging of all of these, which is why I get less excited about it the first week of every month than everyone you may see in the media or politics.

Is the recent slowdown in housing a foreshadowing of tougher times ahead or was this just a blip in the data that will be reversed as mortgage rates come lower? This is a critical question that investors need to ask themselves.

Kimble Charting: Are Junk Bonds Starting To Weaken? Stock Bulls Hope Not!

Several risk on indicators surged higher into year-end, such as small-cap stocks and junk bonds.

And as we typically see, this coincided with a big year-end stock market rally.

Today, we take a look at the Junk Bonds ETF (JNK) to see if this is sustainable into Q1 of 2024.

Above is a weekly chart of the JNK. As you can see, the Junk Bonds ETF has tested the Q1 2023 highs (resistance) for the past three weeks at (1). $JNK is also testing this important price level while its RSI is the highest in a few years at (2).

To sum it up, junk bonds are overbought and testing price resistance… and starting to slip a bit. Stock market bulls hope $JNK doesn’t continue lower.

Finally, in effort to attempt to lighten the mood here given rough start TO global markets,

You hooked me w/the opening paragraphs today, your whit & sarcasm are in top form! But then you joined in my madness going full rabbit-hole w/The Burning Platform Bingo card LOL! I hadn't been on the site in a whiles, but I do read Quinn's articles on the Hedge. He's got a real LONG interesting multi part multi hr read about origins of Capitalism & Socialism (long story short-2 sides of the same coin. Sound $$$ and FREE Markets are the CURE IMHO). Would've never taken you for a Burning Platform reader Steve. I'm quite glad to have VERY wrong about you early on. I'm a work in Progress, never a work of Art! Peace!

TBP reader damn it won't let me edit that!

You hooked me w/the opening paragraphs today, your whit & sarcasm are in top form! But then you joined in my madness going full rabbit-hole w/The Burning Platform Bingo card LOL! I hadn't been on the site in a whiles, but I do read Quinn's articles on the Hedge. He's got a real LONG interesting multi part multi hr read about origins of Capitalism & Socialism (long story short-2 sides of the same coin. Sound $$$ and FREE Markets are the CURE IMHO). Would've never taken you for a Burning Platform reader Steve. I'm quite glad to have VERY wrong about you early on. I'm a work in Progress, never a work of Art! Peace!