weekly observations (05.05.25): cuts pushed back; buyers of 2s on dips; buybacks @ record highs; "Bear Market Is Coming With S&P 500 Rally Stalling Soon" -DeMark; Barrons cover and more ...

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Wait, what? Did I miss THE memo?

Good news is, well, good, again?

USTs are, once again, acting as risk on / off hedge and stocks UP bonds down? Again?

Payrolls recapped and victory lapped below but first UP, a MONTHLY visual to compliment those offered earlier, last week (5yy and 30yy)

10yy MONTHLY: 4.25 - 4.05, triangulation of TLINES …

… momentum complete noise, no signal, middlin’ so lean on DAILY / WEEKLY charts and know the bigger TLINES triangulating and whatever your gut feel / sense most important — supply, USD, risk on / off, fiscal follies, USD strength / weakness etc…

Whatever … truth be told, this post and past weeks data / turn of events will be buried by the Uncle Warren news of the weekend …

May 3 20252:04 PM EDT CNBC: End of an era: Warren Buffett will ask Berkshire board to replace him as CEO with Greg Abel

May 3 202511:13 AM EDT CNBC: Buffett downplays recent market volatility as ‘really nothing,’ saying it’s part of investing

May 3 20259:30 AM EDT CNBC: Warren Buffett knocks tariffs and protectionism: ‘Trade should not be a weapon’

May 3, 2025 at 1:32 PM UTC Bloomberg: Buffett’s Berkshire Lifts Cash Pile to Record $347.7 Billion

… Alrighty, then. On to a few more mundane, NFP data recaps, visuals, and context for reference …

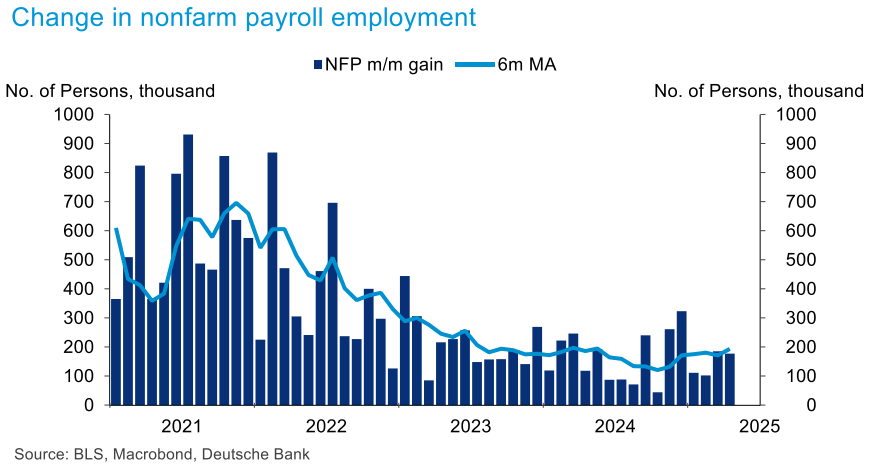

ZH: April Jobs Unexpectedly Jump By 177,000, Higher Than All Estimates

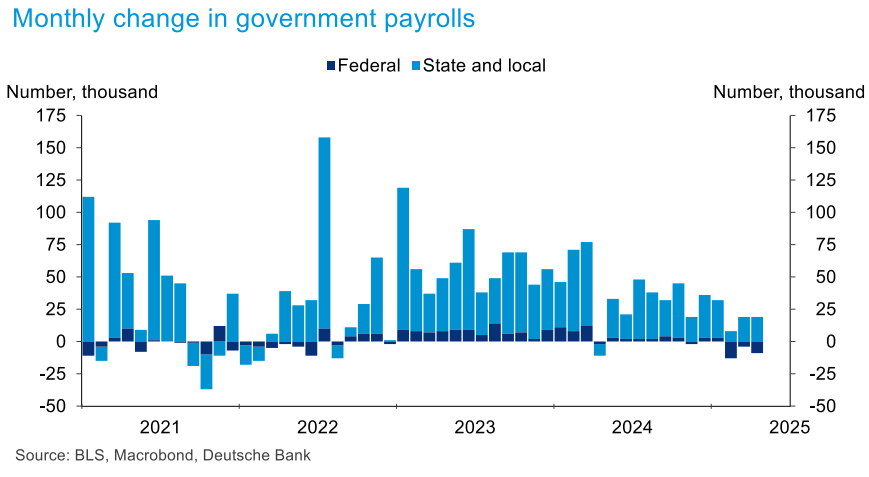

ZH: Native-Born Workers Surge By Over 1 Million, Back To All-Time High, As Govt Employees Tumble

ZH: Payrolls Post-Mortem: Stocks Soar, Rate-Cut Odds Plunge But There's Something 'Disturbing' Authored by Peter Tchir via Academy Securities,

CalculatedRISK: April Employment Report: 177 thousand Jobs, 4.2% Unemployment Rate

WolfST: Labor Market Is Just Fine Despite Dropping Federal Government Jobs, Media-Driven Moaning and Groaning, and Tariff Chaos

The millions of immigrants that arrived in 2021-2024 finally get picked up in the data for labor force and total employment, which continued to spike.

… I’ll quit while I’m behind and move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the Global Wall inbox …

The bank of the land says …

02 May 2025 BAML: Global Rates Weekly Deal or no ideal

The View: Central banks in the dark After today’s EA inflation and US NFP print, focus shifts to next week’s central banks and updated communication in light of “Liberation Day” tariffs. We stay bullish EUR rates and UK front-end, and bearish US front-end.

Rates: Signal miss => cheaper long end USTs US: Bad news is well priced, good news is underpriced. We look to re-engage soft duration long & curve steepeners on any rate rise. Sell 30Y spreads with refunding signal miss….

…We update our core rate views & adjust trade recommendations; our view is that our long duration & curve steepening bias has worked but current levels appear fair. Bad news is priced, as seen by Polymarket recession odds & Z6 (Exhibit 4). Good news is underpriced as evidenced by relatively stable economic surprises (Exhibit 5). We suggest waiting for some good news before re-engaging long rates & steepeners.

Duration: we see current rate market pricing as fair; we have a long bias given downside growth risks but believe the market's Fed cutting trough around 3% (Fed LR median) is appropriate given balance of risks We recommend buying any rate sell-off with strong payrolls but are reluctant to chase rates lower at current levels…

…Bottom line: bad news is well priced, good news is underpriced. We look to re-engage soft duration long & curve steepeners on any rate rise, which could come after April payrolls. Trades: we pay June FOMC OIS, re-establish 30Y spread shorts, recommend short 1y & long 2y3y CPI swaps, hold July ’25 SOFR/FF long, favor 9-12m fwd 5s30s bear steepeners, enter a floor ladder in 2s10s & a receiver calendar in 1y tails.

…Technicals: Signals remain bullish USTs into June US 10Y yield declined in April which historically favors a lower bias into YE25. Since 1963, yield tended to move lower from a May peak to a June trough.

…US 10Y Yield: Down April favors a downtrend into YE25 Since 1963, the average trend ending April through July was flat but over the last ten years, the average decline in yield was down by about 10bps (Exhibit 28). US 10Y yield by week in May has shown no strong hit ratio for being up or down (Exhibit 29). If April is a down month (below 4.2053%) then US 10Y tended to be lower until December (Exhibit 29). From mid-May to mid-June in year 1 of the US Presidential cycle, yield declined about 20bps (Exhibit 29). Since 1963, when 10y yield is above the 200d SMA, it tended to rise on Mondays 59% of the time with average gain of 1.14bps. If below the 200d SMA, 10y yield tended to go down on Tuesday by -2.62bps and on Friday by - 1.34bps.

From across the pond, our very first recap / victory lap (supportive of a Fed on HOLD view, which was just UPDATED and 1st cut now July, from June … ) … … …

2 May 2025 Barclays: April employment: Still smooth sailing, but batten down the hatches

Nonfarm payroll gains surprised to the upside in April, rising 177k, while the March gain was revised lower, leaving the 3mma pace close to our estimate. Details showed a resilient labor market amid gains in employment, participation rate and steady hours worked, with no apparent sign of distress.

… We think today's employment report will support the Fed remaining on hold in the near term as it assesses incoming data on activity and inflation. With the data not really showing any imprint on the labor markets from the tariff announcements as yet, we think the FOMC should remain comfortable staying on the sidelines in the May meeting. Indeed, we delay the timing of our first FOMC rate cut from June to July, which allows for the committee to see more evidence of the deterioration we expect through year-end, as well as to gain more certainty about where tariffs and fiscal policy will settle (see Pushing back first cut from June to July, May 2025)…

2 May 2025 Barclays: FOMC forecast update: Pushing back first cut from June to July

In light of this morning's solid April employment data, we delay the timing of our first FOMC rate cut from June to July. Cutting in late July allows the committee to see more data on the evolution of the labor market, and should benefit from resolving uncertainty about tariffs and fiscal policy.

Today's April employment situation release was surprisingly solid, with nonfarm payroll employment registering a 177k gain, suggesting little fallout on the labor market, as yet, from recent tariff announcements, DOGE-related fiscal restraint, and soft indicators pointing to elevated uncertainty and declining sentiment.

Although we still think that conditions are likely in place for a mild recession in H2 2025, the FOMC is now very unlikely to see enough deterioration in the labor market data to warrant a cut at the June meeting (much less next week). In the meantime, the committee is most likely to remain in a holding pattern as it awaits policy developments, and incoming data on inflation, employment.

Absent the threat of cost-push inflation from tariffs, the committee could possibly contemplate precautionary cuts. However, uncertainty about the course of policy, and, particularly, the likelihood of cost-push inflation from new tariffs, makes such a course unlikely, in our view.

Consequently, we push back our assumption about the timing of the next 25bp fed rate cut from June to July. At that meeting, which occurs occurs July 29-30, we expect that the committee will have seen more data possibly pointing to deterioration in the labor market. This timing also should benefit from a resolving of policy uncertainty, both with regard to the timing of reciprocal tariffs (the three-month freeze on country-specific tariffs ends on July 9) and the upcoming budget legislation.

Apart from the June/July shift, we retain our assumptions about the trajectory of the funds rate. We expect an additional 25bp cut in September 2025, then two additional 25bp cuts in 2026 (June, September).

We regard the two incremental cuts in 2025 as a policy recalibration that carefully balances tensions between the inflation and full employment legs of the Fed's mandate. In doing so, we think the FOMC would maintain a policy stance that remains somewhat restrictive so that inflation ultimately returns to the target over time but would avoid having policy becoming increasingly restrictive as the economy slows and the labor market deteriorates. We doubt that the committee will be positioned to deliver the 3-4 cuts implied by market pricing through year-end, even under our recessionary outlook.

Best in show, buyin’ 2s on a dip (up above 3.90) …

In the week ahead, the refunding auctions will offer another barometer of investor demand for US Treasuries in the primary market. In the wake of the strong overseas allotment at April’s 10-year auction, the new 10-year benchmark results will undoubtedly be in focus as investors remain on guard for any evidence of flagging foreign demand for Treasuries. While 3s and 30s are also relevant, the implications from the trade war have left the underwriting of 10s as the true litmus test for the US rates market. Our expectations are that the auction will be well sponsored by both domestic and overseas participants, as we maintain that it is still too early in the trade war to expect a meaningful rotation away from Treasuries as a reserve asset – at least not on the part of official money. There is always the risk that the specter of a buyers’ strike keeps other potential auction participants on the sidelines as the prudence of ‘wait and see’ remains compelling in the current environment in which uncertainty Trumps clarity (pun intended).

The FOMC announcement on Wednesday holds the potential for a dovish lean in the event that the Committee is contemplating lowering rates next month. That being said, our assumption is that Powell stays on message and doesn’t comment on any future policy changes and reiterates the idea that Liberation Day (and the subsequent 90- day pause) has created more questions than it answered…

…With uncertainty as the unifying theme at the moment, there is a bullish underpinning to the Treasury market that we suspect will be reinforced by this week’s developments. A steady Fed combined with solid auction results is a compelling environment to add duration exposure – especially in the event of a classic pre-auction concession (our base case). The data calendar isn’t particularly inspired, with ISM Services and Jobless Claims the two highlights. However, Friday’s full docket of Fedspeakers holds the potential not only to reiterate Powell’s messaging, but also to provide further guidance regarding the Committee’s response function to future trade war evolutions and the interim performance of the real economy…

…As a brief summary of our recent trading activity:

Booked profits on part of our long position in 5-year notes (entered 4/23 at 4.02%) on Wednesday at our initial target of 3.71%.

Stopped out for a profit on the remaining portion of our long position in 5-year notes (entered 4/23 at 4.02%) on Friday at 3.903%

This week, we'll continue to look for an opportunity to fade a rally in 10-year breakevens, although we've bumped our target entry level down to the month-end close from March 31st at 237 bp. We maintain that a data-driven breakout higher would be a fadeable event given the prevailing disconnect between the leading indicators and risks that continue to stem from the global trade war. We'll also be on the lookout for a dip-buying opportunity in the 2-year sector with yields climbing back above 3.80% in the wake of Friday's payrolls report. We'd be buyers of 2-year notes if rates climb back above 3.90%, the opening level from 'Liberation Day' on April 2nd…

The April jobs report showed steady hiring and a flat unemployment rate, which we think keeps the Fed in a holding pattern near term.

Although hourly pay growth decelerated, total labor income followed a stronger trajectory as hours worked rose, a positive for consumers as tariffs take effect.

Tariffs and accompanying uncertainty are likely to have greater effect ahead, including reverberations in GDP statistics.

Positions matter. Even those in stocks ( :) ) …

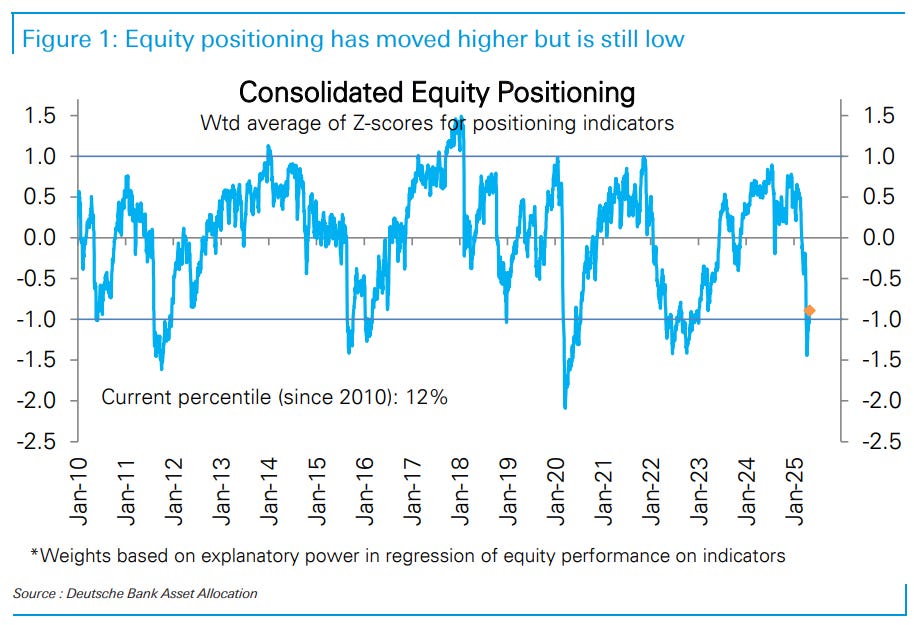

02 May 2025 DB: Investor Positioning and Flows - Moving Higher But Still Low

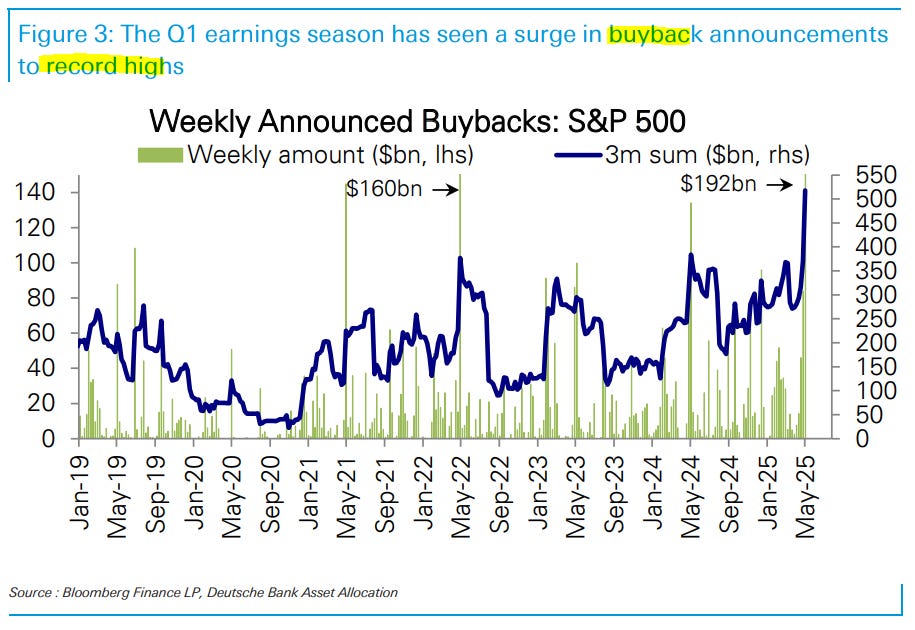

What stood out this week: Our measure of equity positioning has continued to move up but remains low (z score -0.89, 12th percentile), with a large gap between the positioning of discretionary investors (z score -0.26, 30th percentile) which is close to neutral and that of systematic strategies which is still very low (z score -1.37, 9th percentile). Equity fund flows ($8bn) continued to roll in but now with a clear rotation away from the US (-$9bn) and into the rest of the world ($17bn). Within bonds, HY ($3.9bn) and IG ($0.5bn) saw inflows returns while government bonds saw outflows (-$4.5bn). As we wrote in a piece earlier today, earnings beats and growth for Q1 remained solid, and companies indicated they are not going into the bunker just yet (Q1 Earnings Takes: Only A Modest Slowing In Growth). Underlining this is a record setting surge in buyback announcements, running at over $500bn over the last 3 months. While Q1s usually see a seasonal bump, this quarter is clearly a step up relative to history.

… same German shop with monthly chartbook / recap of jobs AND another item on allocation of assets (BINKY) …

02 May 2025 DB: US Economic Chartbook - April employment: Teflon to tariffs (so far)

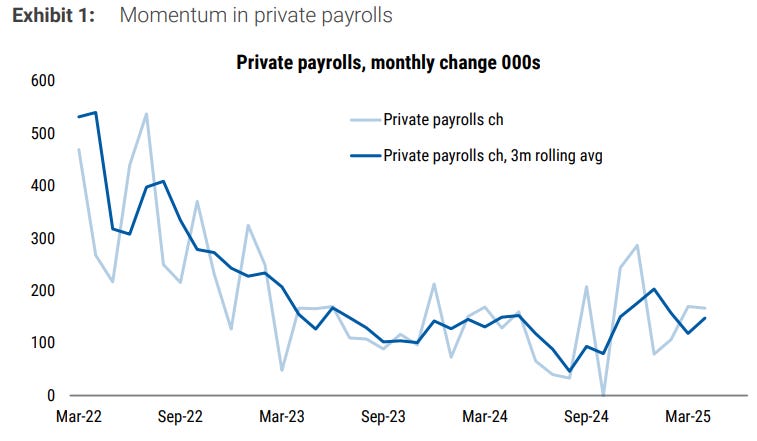

The April employment report modestly surprised to the upside relative to expectations. Outperformance on headline (177k vs. 185k) and private (167k vs. 170k) payroll gains relative to our 125k estimates for both was somewhat offset by 58k in cumulative downward revisions to the prior two months. However, the uptick in hours worked to 34.3hrs and 0.2% increase in AHEs resulted in the year-over-year growth rate of our payroll proxy for income rising by nearly 60bps to 5.3% – the highest level since March 2024. Household survey results were equally as sturdy. The April household employment gain of 436k far exceeded the 82k increase in unemployment resulting in the unemployment rate remaining at 4.2% amidst a 15bps rise in labor force participation (to 62.63%).

In general, the recent labor data point to stable trends leading up to the Trump Administration’s tariff announcements. For Fed officials, the latest data will reinforce their view of “solid” labor market conditions ahead of the trade shocks, leaving them in no hurry to cut rates amidst elevated uncertainty on the outlooks for growth and inflation.

April headline payrolls (177k) slightly below the 6-month average but still solid

…Federal government employment excluding postal workers (-9k) declined, more cuts likely ahead

02 May 2025 DB: Asset Allocation - Q1 Earnings Takes: Only A Modest Slowing In Growth

Well into the Q1 2025 reporting season, we see solid beats so far and only a modest slowing in earnings growth from 13.5% in Q4 to 10.2% in Q1. The accompanying cuts to the bottom-up consensus for Q2 have been a little sharper than is typical but are far from extreme, with both companies and analysts looking to be waiting for more clarity before adjusting numbers. In our reading, a combination of pre-buying and inventory rundowns should give companies a buffer of about 1 to 2 months before the tariff impacts start to bite.

As we wrote last week, if sustained, we see the potential impact of the announced tariffs as large and likely to fall disproportionately on US companies. We see growth falling sharply from 10% in Q1 to negative 4% in Q2. The consensus is currently at 4.4%, suggesting plenty of room for further downgrades. Further out, we see growth falling to double-digit negative rates in Q3 (-10%) and Q4 (-13%) while the consensus sees it picking back up to 7-8%.

We also present a collection of management quotes and the key themes that emerged. Companies plan to first engage with the administration to reduce the tariff rates or to get exemptions, and then to mitigate any burden essentially by passing it along the value chain either to suppliers or to customers, although direct consumer-facing businesses are wary of doing the latter. Notably though, companies have not yet adopted a bunker mentality and remain committed to their capital plans.

… One last note from Germany, ahead of this weeks FOMC meeting …

02 May 2025 DB: FOMC preview: Stay in May and see if trade turmoil goes away

We expect the Fed to keep rates steady and avoid explicit forward guidance about the policy path ahead. The overall tone of the meeting is likely to echo comments from Chair Powell and his colleagues in recent weeks. In particular, the administration's policies are likely to push the economy away from the Fed's dual mandate objectives for a period of time but that monetary policy is "well positioned" to respond to the evolving outlook.

With the labor market still "solid", Powell is likely to continue to emphasize the inflation side of the dual mandate. This could include repeating that it is the Fed's "obligation" to ensure tariff-driven inflation does not become more persistent and that sustainable maximum employment requires price stability. The signal will be that the labor market needs to weaken for the Fed to contemplate cuts.

Our base case remains that the next rate cut is in December, followed by two more 25bp cuts in Q1 2026 (see "US outlook: Tariff-struck"). These reductions will bring the fed funds rate into the 3.5-3.75% range, consistent with our view of neutral. Risks are tilted towards earlier cuts if unemployment rises more sharply.

AND …

First Trust: Nonfarm Payrolls Increased 177,000 in April

…Over the past three months federal employment has dropped by 26,000 (the most outside of the COVID pandemic since the 2013 budget sequestration), and the BLS points out that employees on paid leave or receiving severance aren’t included in these declines. Given the Trump Administration’s goal of reducing the federal workforce, we expect more of this in the months ahead, potentially much more. That may cause some short-term pain for the US economy, but we expect long-term gains from reducing the size and scope of the federal government, including more jobs gains in the private sector. In other recent news, cars and light trucks were sold at a 17.3 million annual rate in April, down 3.1% from March but up 7.8% from a year ago, but was likely affected by buyers front running tariffs.

… something which IS and something which is NOT (directly)NFP related but ahead of this weeks FOMC meeting …

2 May 2025 ING: US jobs market holds firm ahead of the tariff storm

The US economy added 177k jobs in April, but with business and consumer surveys suggesting tariffs and trade policy uncertainty is hurting sentiment, there is the strong likelihood that a cooling in economic activity translates into a weaker jobs market over the summer

2 May 2025 ING: Fed to push back against calls for rate cuts

Presidential demands for lower interest rates are falling on deaf ears at the Fed as near-term inflation concerns limit the scope for action. Nonetheless, the US economy is cooling and that can pave the way for major rate cuts in the second half of the year

Some better than average (top 5 institutional investor survey) … rate stratEgery (choosing to be neutral duration IS a choice and one that is noted) …

May 2, 2025 MS: The Primary Trend Remains Toward A Steeper Curve | US Rates Strategy

We continue to suggest a neutral stance toward duration and an embrace of yield curve steepeners as the curve continues along its primary trend. Foreign investor exposure to longer-duration US fixed income has increased over recent years – raising risks to a steeper curve should that sponsorship soften.

Key takeaways

US Treasury data through June 2023 show foreign official and foreign private investors increased exposure to longer-maturity USTs over the past decade.

Foreign private investors hold more long-end USTs than foreign official investors, but foreign official investors increased long-end exposure to new highs.

With exposure to long-end USTs at or above 20-year highs, any sustained foreign buyers' strike should impact long-end Treasuries more than short-end.

The market should struggle to price out more rate cuts until the 90-day pause on reciprocal tariffs becomes more permanent – making curve flattening difficult.

We suggest staying in UST 3s30s steepeners and term SOFR 1y1y vs. 5y5y curve steepeners given long-end outflow risks and Fed policy pricing risks.

… in as far as what former Barclays econ says, Gapen’s latest on NFP and …

May 2, 2025 MS: U.S. Economics: Strong April labor gains despite policy turmoil

The 177k rise in payrolls suggest continued business labor demand in April despite policy turmoil. The unemployment rate stalled but would have fallen except for higher participation. There's no sign of any slowdown ahead of tariff effects, which supports the Fed's tilt toward holding policy steady.

Key takeaways

Payrolls accelerated from 133k per month in 1Q to 177k in April. We think Easter timing probably added ~20k to private payrolls.

Some hint of tariff-related pull-forward as transport payrolls rose 29k, about 2x their recent pace.

Soft retail but strong leisure payrolls. Business services rebounded. Federal government fell 9k, a 3rd straight decline.

The unemployment rate, at 4.19% after 4.15%, would have fallen to 4.0% but for higher participation.

No sign of slowing in labor demand: This report supports a steady Fed at next week's FOMC meeting.

May 2, 2025 MS: US Economics Weekly: The data says the Fed should wait

A "sudden stop" in trade flows and loss of confidence remains the primary risk to the outlook, but we think that risk remains in front of us. The data should give the Fed confidence to wait for clarity and we think markets overestimate the likelihood of near-term Fed rate cuts.

Key takeaways

The hiring rate in the economy has moderated, but signs of layoffs remain scarce. Labor market income growth continues to outpace pre-tariff inflation.

The decline in Q1 real GDP overstates weakness. Front-running of tariffs boosts imports, equipment spending, and inventories. We think this reverses in Q2.

The Fed should stay on hold in May while signaling it needs clarity from the data to know which way to move. We still expect no rate cuts until 2026.

As Yogi Berra once said, when describing route to his home … when you get to the fork in the road, take it, and so …

2 May 2025 NatWEST: Trades for the Fed's Fork in the Road

The Fed must triage simultaneous adverse shocks to growth and inflation. Markets now price roughly 90 bp of cuts by year end. Our view remains that the Fed will be more inclined to do nothing whilst assessing the final form of tariffs implemented and the impact on the economy. We suspect in the end the Fed will attempt to look through both shocks and allow passive tightening to return inflation the rest of the way to target.

The first implication is that the Fed will not be willing or able to deliver the rate cuts currently priced in the near-term forwards. We favor payer spreads on short tails to capture the roll up available if these forwards are not met.

We think a Fed pivot to growth would unleash a torrent of higher expected inflation potentially exacerbated by the likelihood of fiscal expansion and concerns about Fed independence. We favor buying 1y10y high strike payers as a hedge to our core view that the Fed will defend the inflation mandate before turning to growth.

Average hourly earnings:+0.2%m/m (consensus +0.3%, Natwest +0.2%)/ 3.8% y/y

The April employment report was another solid report, which should allow the Fed to remain in its "wait-and-watch" mode. We don't expect any action from the Fed at next week's meeting (see FOMC preview here). While there were downward revisions to the tune of 58,000 to the prior two months, overall payroll still increased by 177,000 (consensus +138,000, NatWest +25,000) in April. That puts the year-to-date average for total nonfarm payroll growth at 144,000, just a touch lower than the average gain of 168,000 in 2024- reflective of a slowing (not collapsing) labor market amidst ongoing economic uncertainty….

… which then seguay’s into the firms FOMC precap …

We expect no action on interest rates from the Fed at the conclusion of the upcoming week’s FOMC meeting. The policy statement will be released on Wednesday at 2:00pm (EDT) and the post-meeting press conference will begin at 2:30pm (EDT). No updated FOMC forecasts will be submitted. The main takeaways we expect include:

No change in interest rates (target funds range 4.25%-4.50%)

Limited changes to policy statement

Powell to emphasize “wait-and-see” approach and uncertain outlook

Our neighbours to the North on OUR NFP data …

May 2, 2025 RBC: Downward revisions take shine off of upside US payrolls surprise in April By Carrie Freestone

The Bottom Line: This morning’s nonfarm payroll report was an upside surprise for April (+177K), although following downward revised growth in both March (+185K vs. initial 228K) and February (102K vs. previously 117k).

Paradoxically, from a structural perspective, record retirements mean that a shortage of labour supply remains an issue. The unemployment rate held steady in April at 4.2%. We saw an uptick in job losers, fewer quits, and a bump in re-entrants which nudged the participation rate up by one-tenth (to 62.6% from 62.5%).

But this morning’s print drives home the point that hiring has slowed as firms grapple with significant uncertainty from tariffs, and is expected to weaken further in the back half of the year as the impact of tariffs permeates.

Solid. Like a rock … so says those from the covered wagons …

May 2, 2025 Wells Fargo: Powering Through: A Solid April Employment Report

Summary The April employment report showed that the U.S. labor market remained resilient in April despite the turmoil that swept financial markets. Nonfarm payrolls increased by 177K, although downward revisions to job growth in February and March took some shine off of the April number and left the recent pace of hiring little changed at a three-month average pace of 155K. The breadth of hiring across industries was solid, with only a few modest weak spots in areas such as retail trade, manufacturing and the federal government. The separate household survey painted an even rosier picture. The unemployment rate held steady at 4.2% despite a robust increase in the labor force.

Higher tariffs threaten both sides of the Fed's dual mandate of full employment and price stability. With spot inflation already above the central bank's 2% target and the labor market still seemingly hanging on, we do not expect the FOMC to signal imminent policy easing at its meeting next week. There is just one more employment report to be released between now and the June meeting, and with nonfarm payrolls still growing at a solid pace and the unemployment flat lining around 4.2%, the odds of a June rate cut have fallen, in our view.

That said, with monetary policy still somewhat restrictive and weaker economic growth expected to weigh on the labor market in the months ahead, we still think the FOMC will reduce the federal funds rate this year by more than the 50 bps implied by the median projection in the March meeting's Summary of Economic Projections. We will update our fed funds forecast and broader economic projections next week.

…The strength in the hiring data was not paired with an acceleration in wages. Average hourly earnings moderated to a 0.2% rise in April, allowing the year-ago rate to hold steady at 3.8%. This reading is consistent with the separate Employment Cost Index report released earlier this week that showed a continuation of the trend in decelerating labor compensation costs. Despite the slowdown in wage growth in April, the rise in total hours worked points to stronger income growth in the aggregate (chart). Solid income gains, if sustained, will support household spending even as consumer optimism has softened amid tariff fears.

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

Since the trade war began in March, consensus expectations for growth have been revised down, and consensus expectations for inflation have been revised up, see the first chart below. This is the definition of stagflation: higher inflation and lower growth.

Under stagflation, with higher rates and slower growth, investors should stay away from growth equity and growth credit and be up in quality and invest in companies with earnings to protect against the downside risk of a recession, see the second chart.

This happens to also be how investors in public markets are positioned. Short interest in small-cap companies is at the highest level seen in many years, see the third chart. This is not surprising as 40% of companies in the Russell 2000 have negative earnings, and middle market and small-cap companies are hit by the triple whammy of higher tariffs, slower growth, and higher rates because of inflation staying higher for longer.

For more on STAGFLATION and records … see latest from Jesse Felder …

… Um … buy stocks? Be greedy when everyone is fearful and fearful when everyone is … nevermind … cover indicator suggesting they are … reading DeMark (below) …

May 2, 2025, 11:46 AM BESPOKE: Getting Back to Even

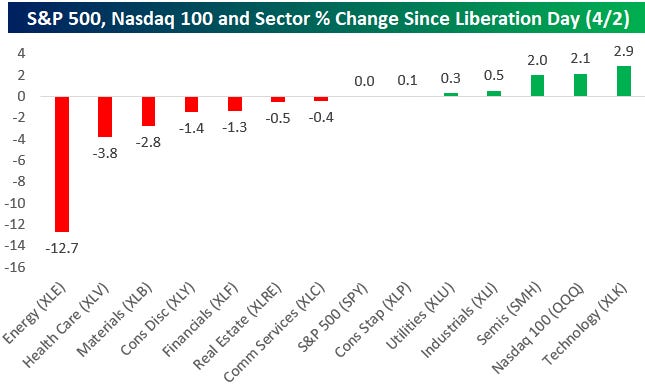

It's been exactly a month since "Liberation Day" on April 2nd when President Trump announced massive reciprocal tariffs on the rest of the world. At its intraday low on April 8th, the S&P 500 ETF (SPY) was down 14.7% from its closing level on April 2nd. Since that low, SPY has now rallied 17.4%, and as of this morning, SPY has fully recovered all of its post-Liberation Day declines.

Below is a look at the performance of key index and sector ETFs since the close on Liberation Day (4/2). Technology (XLK) is now the best performing sector since 4/2 with a gain of 2.9%, followed by the Nasdaq 100 (QQQ), Semis (SMH), and Industrials (XLI). On the downside, the Energy sector (XLE) has been by far the biggest laggard with a decline of 12.7%.

We'd note that even though the stock market has fully recovered its post-Liberation Day drop, investor sentiment remains extremely bearish. This week marked a record 10th consecutive week where AAII Bearish Sentiment was above 50%. The prior record was seven straight weeks back in 1990. Will the bulls finally re-emerge next week? We won't find out until next Thursday when the weekly AAII numbers get posted.

Back in early 2023, we created the Bespoke AI Basket to track key stocks in the space. We broke the basket into two sub-groups: one for AI Infrastructure stocks and one for AI Implementation stocks. The AI Infrastructure basket contains stocks that power the AI Boom like NVIDIA (NVDA), while the AI Implementation basket contains stocks like Meta (META) that are implementing AI to boost the user experience and increase margins and productivity.

As shown below, the AI Implementation basket has outperformed the AI Infrastructure basket since the end of 2022 by quite a wide margin.

There have been periods of significant out- and underperformance for each basket, however. Below is a look at the ratio between the AI Infrastructure and AI Implementation baskets. When the line is rising, AI Infrastructure is outperforming, and vice versa.

The first half of 2024 saw AI Infrastructure outperform quite dramatically, but since mid-2024 for about the last year now, AI Implementation stocks have been outperforming. Are we now due for a reversal that sees AI Infrastructure start to bounce again?

… a couple from The Terminal Dot COM …

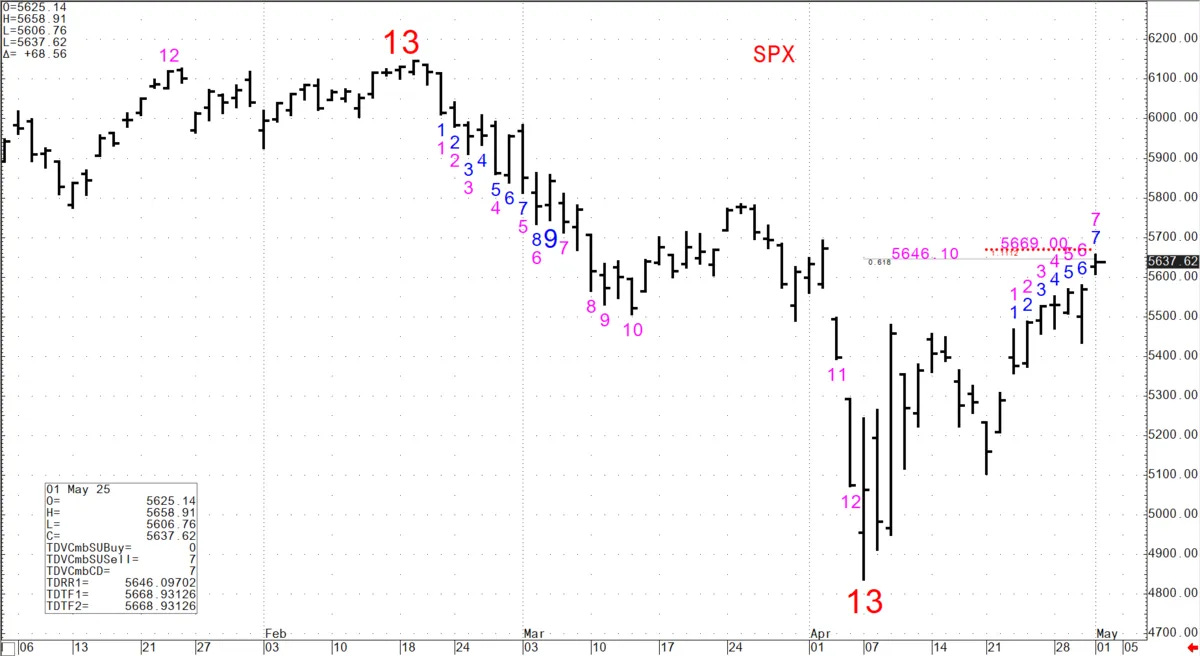

May 2, 2025 at 3:16 PM UTC Bloomberg: Bear Market Is Coming With S&P 500 Rally Stalling Soon, DeMark Says

US stocks are in for another drop that will eventually lead to a bear market in the coming months, according to veteran technical strategist Tom DeMark, who accurately called this year’s top in February and subsequent April low.

DeMark — a closely-followed analyst who’s advised billionaire investors including Paul Tudor Jones, Leon Cooperman and Steve Cohen — uses a system for predicting where markets will move, divined from a half century of chart gazing that’s based on mathematical relationships. He focuses on trend exhaustion, with his mantra being markets top on good news and bottom on bad news.

A confluence of technical indicators, sentiment shifts and cyclical timing models are flashing caution signs, suggesting a drop in the S&P 500 below 4,835, this year’s intraday low in early April. That would represent a more than 20% drop from the gauge’s February peak, pushing the index into a bear market.

“A top is imminent. Too much technical damage has been done,” DeMark said by phone. “Stocks are vulnerable right now and can easily get hit pretty badly if anything quickly changes on the global trade outlook.”

DeMark’s warning comes amid a stock-market rebound that’s put the S&P 500 Index on track to erase all of its losses suffered after President Donald Trump’s tariff announcement last month. The gauge is up for a ninth straight day Friday, which would mark its longest winning streak since 2004.

Source: Market WITSource: Market WIT

A near-term top in the market may happen within days, says DeMark, whose firm DeMark Analytics LLC specializes in identifying market turning points. Specifically, the 5,669 level — which is right around where the gauge is currently trading — will likely leave buyers exhausted, said DeMark.

The prediction is based on DeMark’s “countdown” study that involves comparing a security’s closing price to its highest or lowest levels four days earlier. Cycles of “exhaustion” develop when a pattern continues nine times. The S&P 500 just produced its seventh count on Thursday. DeMark focuses on a string of nine daily moves, which don’t have to be consecutive, but do have to be better than four sessions ago.

That means two new closing highs for the S&P 500 would likely trigger sell signals, DeMark said. Once that happens, weak technicals will pressure the index to resume its prior decline and eventually push the S&P 500 below 4,835.

“Historically, markets don’t bottom on good news, like last month on positive trade developments,” DeMark said. “Stocks typically bottom when everything is terrible and everyone is forced to throw in the towel — but that hasn’t happened yet. Stocks were just way oversold and overdue for a bounce. Ever since then, equities have struggled technically underneath the surface and are in danger of a big drop.”

May 3, 2025 Bloomberg: Stock Market Bull Charges On, Question Is When It Meets the Bear

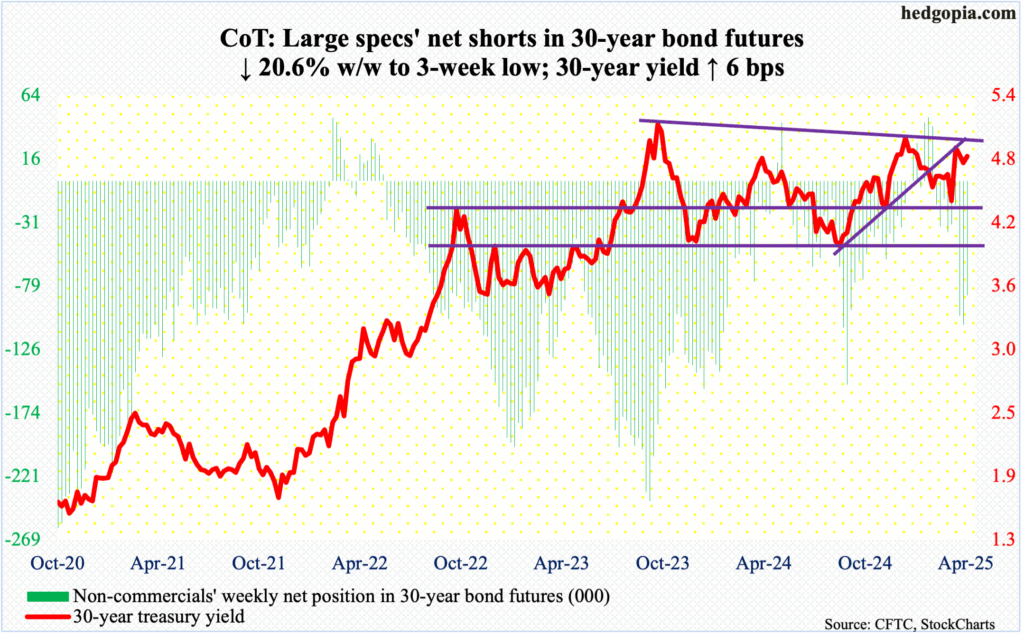

Positions. Lives. Matter. Especially those detailed here … generally speaking, specs are somewhat LESS SHORT 10s and bonds …

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned …

… a stock jockey now retired, on NFP …

at jimwpaulsen

Since 1960, US employment growth has never been below 1.2% when it wasn't either in a recession or imminently headed to one. See chart below. How can the Fed be so confident the job market remains healthy and needs no policy assistance?

That bottom was at 4.11% and we are now 4.32%. Yields are moving as foreign selling of bonds picked up again, NFP was not weak, and Japan’s Kato said the unthinkable. I am surprised this story didn’t get more coverage. Not that Japan will sell treasuries in retaliation for tariff policy, but this is something people would normally never say out loud. Especially not Japan! I suppose this is what happens when you feel threatened by a nation that was one of your closest allies for 50+ years.

Also, I suppose Japan knows that rising bond yields keep Donald Trump awake at night and make him panic on policy.

The overall picture for bonds is confusing because we may be on the front edge of a recession, some prices are falling (crude oil) and other prices are rocketing higher. E.g., this email TW received yesterday …

… great minds think alike OR fools never differ (“…overbought momentum…” was noted Wednesday morning HERE … and up up we went, closing the week just north of 4.30!). I don’t know Brent personally but I like him and his output quite a bit…just sayin! From his latest post above …

Finally, from the intertubes, ZERO with a note from Bloomberg’s Simon White AND picking up on Apollo notes / thoughts and adding a bit of ZEST and so …

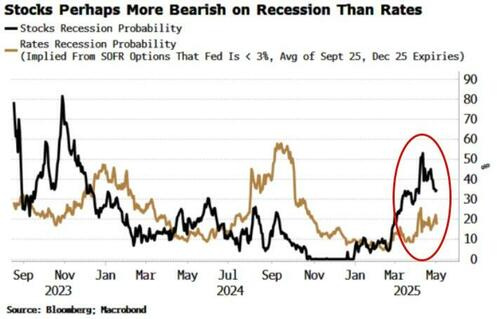

Friday, May 02, 2025 - 08:05 AM ZH: Are Stocks Pricing In A Recession More Aggressively Than Bonds? Authored by Simon White, Bloomberg macro strategist,

Stocks looks to be implying a higher chance of a recession than the rates market.

Given burgeoning inflation pressures, the yield curve could therefore see significant steepening in a downturn.

The spectre of a recession will remain with us through the summer, and probably longer, as tariff policy upends current economic normality.

A recession is increasingly becoming consensus, at least based on the latest MLIV Pulse survey, where 86% of respondents saw a downturn this year as probably likely or a certitude.

It looks like the stock market is leaning in that direction, with it being more expectant of a recession than the rates market (explanation is below).

The S&P is inferring about a 34% of a recession, higher than the 18% implied by the rates market.

The latter is easier to estimate, as one can make a reasonably realistic assumption about where rates would be if it looks like a recession was soon imminent (I’ve assumed the Fed would cut below 3% and took the average of options with September and December expiries).

Then we can infer what the probability the SOFR option market is ascribing to that outcome.

Inferring a similar probability for the stock market is trickier. It’s not as obvious what levels to pick as being consistent with a recession. Instead I looked at the high-low range of the S&P in prior soft and hard landings then compared that to where we are within that range today. At the top of the range is defined as 100% chance of a soft landing, and at the bottom it’s a 100% chance of a recession.

Using S&P options to infer a probability directly yields about 14%, if we assume a recession means the S&P is below 5000 at the end of September.

This estimate was much higher and in line with the range-based estimate in early April, with it falling sharply as implied vol fell.

However, if there was an imminent recession, it’s conceivable stocks could have already bottomed and be above 5000 again by the end of September. Hence none of this is straightforward, but it’s not too outlandish to say rates could move more than stocks if a recession becomes the base case.

That could mean an outsized move in the yield curve.

As we have seen, Treasuries are alive to inflation risks that have been inflamed by tariffs so longer-term yields might not fall as much as expected if a recession hits.

Friday, May 02, 2025 - 10:55 AM ZH: Apollo's Torsten Slok Unveils Timeline For Trade War Fallout

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

My impression is that magazine covers are usually Contrary Indicators.

The content you cover in your post is amazingly comprehensive !!!

I'm more optimistic about trade agreements, than some people.

The Chinese are hurting.

US Exceptionalism is still alive.

Slow growth, not a bad thing.

Inflation is fading.

Interest rate well behaved.

Crude oil way down.

There's a Bull market in the making.