while WE slept: USTs firm, quiet overnight; 5yy monthly; data recaps / victory laps as day came / went without much drama; XTEND 10yy tgt (4.14); monthly performance review...

Good morning … what better way to celebrate the passing of another month than with an updated monthly chart … I’m NOT a technician, don’t play one on TV but know just enough to be dangerous — ok, no I don’t — so here’s one to consider …

5yy MONTHLY: middle of triangulating range, nearer resistance (3.66) …

… stochastics, bottom panel (yes, still, sort of a safety blanket of indicators) not YET suggesting overBOUGHT conditions to an extreme one needs to fade BUT worth watching, as we approach, for sure …

… More monthly visuals of consequence to follow (as soon as I figure out whatever they may be — feel free to chime in with your very own ideas) and for now, I’ll move along to the day that … well … wasn’t.

Don’t get me wrong … there was data and reFUNding supply announcements …

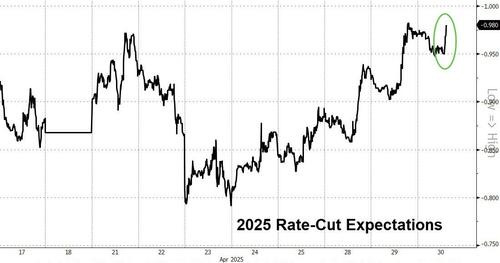

ZH: Rate-Cut Odds Jump After ADP Reports Weakest Job Growth Since July 2024

The market is moving that way - pricing in four cuts for 2025 now.

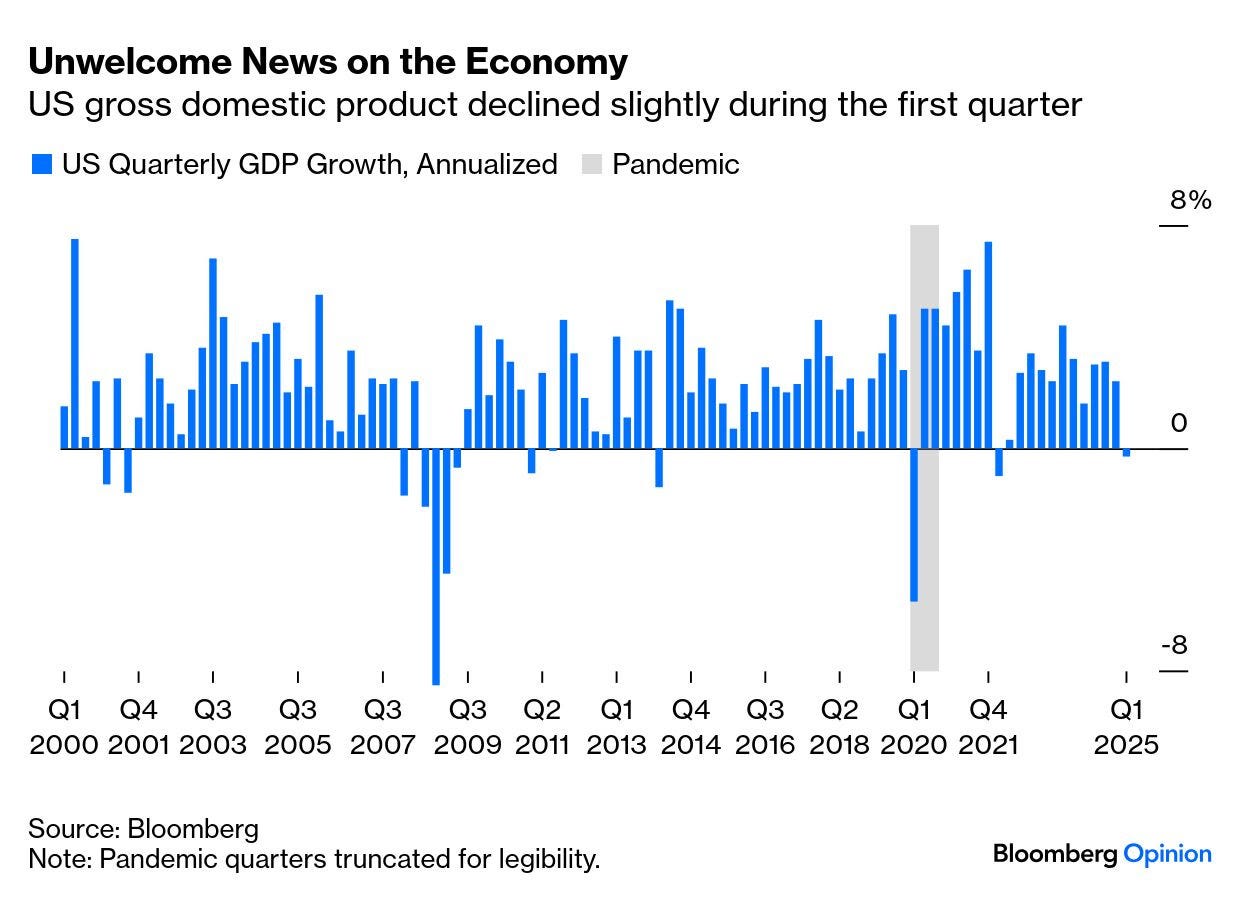

ZH: US Q1 GDP Contracts On Record Imports, Shrinking Govt, As Consumption Comes In Stronger Than Expected

ZH: Stagflation Scenario Slammed As Fed's Favorite Inflation Indicator Tumbles To Four Year Lows

ZH: Quarterly Refunding: Treasury Will "Maintain" Auction Sizes For "Several Quarters", May Boost Buybacks Size, Discusses Stablecoins As Source Of Bill Demand

… there just really wasn’t all that much drama. See BMOs view below for more of what I mean … but if you prefer …

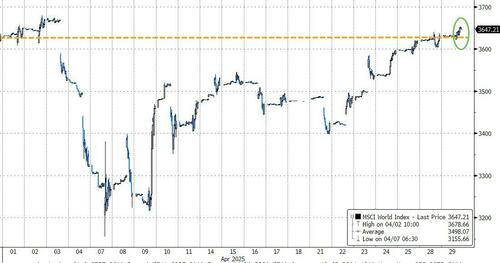

ZH: 'Much Ado About Nothing': Nasdaq Ends April Higher Despite 'End Of US Exceptionalism'

… If you'd taken the month of April off, you'd never know the world faced an existential crisis (the end of US exceptionalism etc...) due to Trump unleashing the biggest tariff increase in history as world equity indices closed marginally higher on the month (recovering from a 14% drawdown after 'Liberation Day')

…The weak US macro data today sparked a resurgence in rate-cut expectations (Fed Put back on the table)...

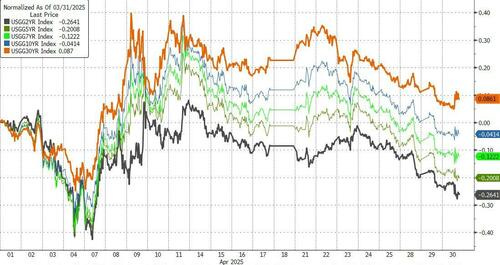

…Treasury yields were mixed on the month with the most of the curve lower in yield (led by a 26bps drop in the 2Y yield) as the 30Y ended up 8bps...

… here is a snapshot OF USTs as of 638a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures boosted after strong MSFT/META results, US ISM Manufacturing due … A very slow start to the session for USTs given the absence of European participants for Labour Day (China also away). USTs are firmer and at a 112-12 peak, but one that is shy of the 112-16 high from Wednesday. As was the case on Wednesday, any concerted move higher enters a patch of clean air before resistance at 114-03+ and 114-10 from early-April.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … lots of data to recap and victory lap, so lets get to it …

Not just US but EZ GDP up for review and recap / victory lap … but, um …

30 April 2025 ABN Amro: US and EZ GDP releases - Not just a frontloading story

US Macro: Import surge exaggerates GDP weakness. Eurozone upside surprise materializes before heading into a US tariff induced slowdown. France disappoints as underlying data looks worse. Germany solid start to the year moving into trade uncertainty German. Dutch growth slows to 0.1%, partly expected, partly unexpected.

30 April 2025 ABN Amro: Global trade - Frontloading precedes tariff shock

The recovery of global trade and industry seen in early 2025 was helped by trade frontloading in the run-up to higher US import tariffs.

Calm before the storm? US import tariff shock will hit global trade, with container bookings into/from US already nosediving, export PMIs falling sharply and IMF and WTO cutting their world trade growth forecasts.

Signs of trade frontloading preceding this tariff shock are evident – particularly in tariff epicentre US (shown by a dramatic turnaround of net exports’ contribution to Q1 GDP), but also for China and the eurozone. Evidence for the Netherlands is limited so far.

Following the escalation of the US-China trade war, fears of a new China supply shock hitting European markets have risen. However, besides risks, this also creates opportunities for European companies.

… don’t kid a kidder … ? don’t jump the gun …but, folks bot stuff ahead of and so, jumped the … never mind … and oh, yeah, an updated outlook

30 April 2025 Barclays: March PCE inflation: Don't let them fool you

Core PCE inflation slowed sharply in March, to just 0.03% m/m (2.6% y/y), lower than our below-consensus forecast, and headline PCE fell 0.04% m/m (2.3% y/y). However, upward revisions to the data for January and February led core PCE inflation to rise 3.5% q/q saar in Q1.

30 April 2025 Barclays Advance Q1 GDP: Measured decline likely jumps the gun on upcoming weakness

The BEA's advance accounting showed an abrupt 0.3% q/q saar decline in real GDP in Q1 on the heels of strong gains through 2024, with solid growth in private domestic spending more than offset by a surge in imports. Although GDP is poised for declines, the measured Q1 decline is likely premature.

Real consumer spending posted a strong gain in March, suggesting that tariff front-running was a stronger driver of spending than we had anticipated. Today's data provide indications of a solid carryover effect for Q2, which may help some households weather upcoming cost-push inflation.

30 April 2025 Barclays: Adjustments to our activity outlook

In light of today's weaker-than-expected GDP Q1 estimate, we adjust our call to assume a somewhat bigger rebound in growth in the current quarter. We retain our forecast for a mild recession in H2 2025, incorporating more adverse fallout on nonfarm payroll employment than before.

Yesterday, well, was a big fat nuthin’ burger … ‘twas much ado ‘bout nuthin …

April 30, 2025 BMO Close: Much Ado about Wednesday

… Wednesday’s price action proved to be far less dramatic than the data headlines would have implied. The real economy contracted in Q1, slipping -0.3% on a quarterly annualized basis. However, the reality is that the downshift in growth was a function of a surge in imports as looming tariffs prompted purchases in anticipation of the changes. It was encouraging to see the Treasury market’s disinterest in trading the growth report in light of the distortive impact from net exports. Within the details of the release, the consumer appeared to be on solid footing with Personal Consumption printing at 1.8% versus the 1.2% consensus, and Final Sales to Private Domestic Purchasers improving to 3.0% from 2.9% in Q4. Our takeaway was that in the absence of the trade moves, the quarter demonstrated an impressive departure point for the headwinds that will result from the trade war. It wasn’t surprising to see Trump downplay the drop in real growth and volatility in stocks as the responsibility of the previous Administration – even we recognize that as politics 101…

… stay long’er … er … and oh, ‘bout USTs, and the Fed … and everything …

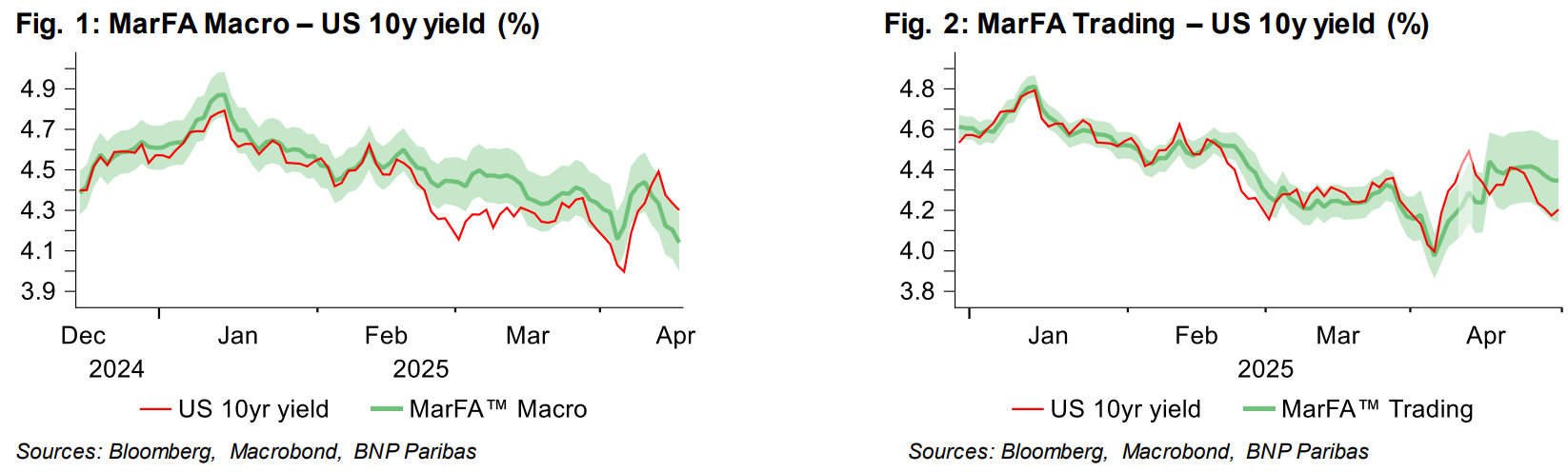

30 Apr 2025 BNP QTOW: Extending target again on long UST 10Y

Our long US 10y Treasury trade idea (see Quant trades of the week, dated 14 April) has performed well since inception. We initiated the trade as signals from both our MarFA™ Macro and our faster MarFA™ Trading (3m lookback) suggested the US rates selloff was overdone. Further, we saw US 10y nominals as having decoupled from the current softness of data and data surprises. Since then we have extended our target to 4.14% (see QTOW: Extend US 10y yield target and move trailing stop loss, dated 16 April) – which has now been reached – and trailed our stop loss to 4.45%.

MarFA™ Macro UST 10y fair value continued to trail lower and now suggests a more ambitious target of 4.0%, while shorter term MarFA™ Trading is now suggesting UST 10y is too rich with the fair value of 4.33%. Our projections for data remain negative, but not at the same magnitude as previously (see QTOW:Five mispricing signals from a week of normalisation, dated 28 April), and so we continue to like long UST 10y but now see risks as more balanced.

We extend our target to an ambitious 4.0% as per MarFA™ Macro but move our stop loss to 4.22%.

<BPMR14 INDEX> is our Bloomberg ticker to live track the MarFA™ Macro fair value of US 10y Treasuries.

30 Apr 2025 BNP US rates: Treasury, Fed, and everything in between

KEY MESSAGES

Treasury continued to suggest there is no need for any increase in coupons in the coming quarters, hinted at enhancements to its buyback program, and flagged the “cost of issuance”. All of this supports our view that US Treasury could favor higher T-bills over coupons to fund incremental deficits.

We take profits on our long 30y swap spreads trade for the time being (Entry: -92bp, Close : -86bp, PNL: +6bp), though we see spreads supported in the medium term with help from the administration.

Tax receipts and tariff revenues push our X-date estimate to early September, with a debt ceiling resolution likely to materialize a few weeks before. T-bill paydowns should continue for an extended period, albeit at a slower pace than initially expected.

We expect the Fed to announce the end of QT at the September FOMC meeting, with liquidity seen remaining abundant until mid-Q4.

Interrupting data recap / victory lap for this next MONTHLY performance review and recap … nuthin’ burger?

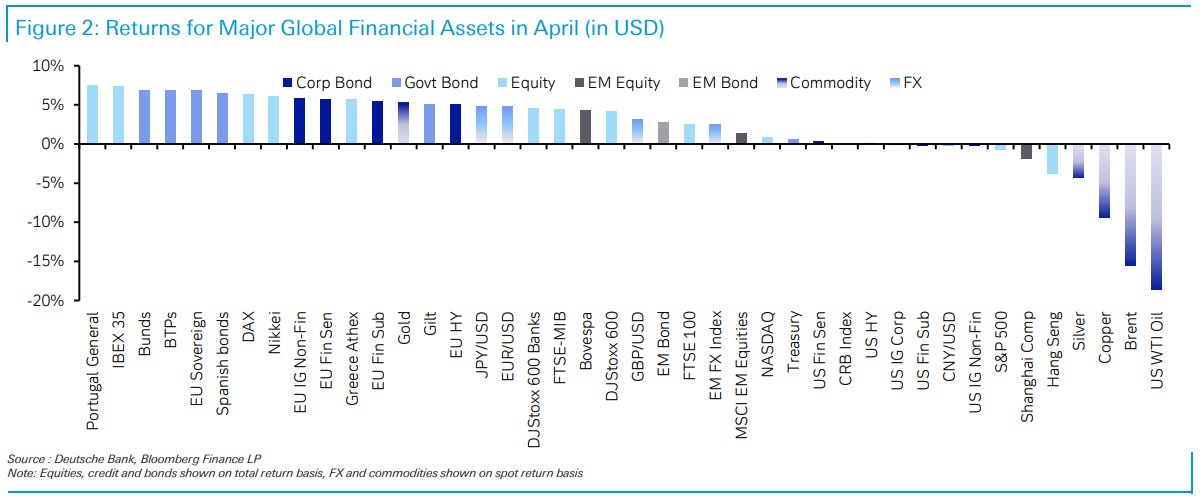

April was an absolutely seismic month in financial markets, as the announcement of US reciprocal tariffs led to a huge global sell-off. The initial moves were truly historic in their speed, and straight after the announcement, the S&P 500 posted its 5th-worst two-day decline since WWII. That turmoil also spread to the bond market, where the 30yr Treasury yield briefly surpassed 5% intraday. Meanwhile, the VIX index closed above 50, something we’ve only seen this century at the height of the GFC and during the initial Covid-19 turmoil. However, calm began to return to markets after President Trump announced a 90-day extension to the reciprocal tariffs, and US officials began to negotiate deals with other countries. So that meant market stress began to ease, and the aggregate performance in April wasn’t as bad as the headlines might suggest, with the S&P 500 only down -0.7% in total return terms.

So if you just looked at the monthly equity returns in local currency terms, you could be forgiven for thinking it was a relatively uneventful month. But in reality it was historic, and it included the best day for the S&P 500 since October 2008, as well as its worst day since March 2020. Otherwise, we saw the biggest weekly widening in the 10yr UST-bund spread in data back to German reunification in 1990. The dollar index has now seen its worst two-month performance since June 2002. And gold prices have seen their strongest start to a year since 2006.

The (foreign)lion roars ‘bout shrinking US GDP …

30 April 2025 ING: US economy shrinks on import surge

The economy contracted in the first three months of the year as importers desperately tried to bring in as many goods as possible ahead of tariffs. Inflation was also more elevated, fuelling the stagflation narrative and limiting what the Federal Reserve can do to help as economic sentiment sours

Here we have a global MACRO recap, an inflation monitor and a Treasury reFUNDING victory lap …

April 30, 2025 MS: Global Macro Commentary: April 30

Front-end USTs rally after mixed data; long-end USTs lag amid unchanged coupon auction sizes in May QRA; AUD gains after CPI beat; Bunds rally despite strong EA growth; BanRep unexpectedy cuts rates; miss in China Manufacturing PMI; DXY at 99.62 (0.4%); US 10y at 4.162% (-1.0bp)

Front-end USTs rally (2y: -5bp)after 1Q25 US GDP contracts due to import front-loading and March Core PCE comes in softer than expected, despite the resilient spending and consumption data.

Long-end USTs underperform (30y: -3bp) after Treasury keeps nominal coupon and FRN auction sizes unchanged over the May refunding quarter and still anticipates maintaining current sizes “for at least the next several quarters,” while saying it is evaluating potential enhancements to its buyback program…

April 30, 2025 MS: US Inflation Monitor: Tracking tariffs' inflationary impulse

We estimated the inflationary impact of individual PCE component, and separated components more vs less exposed to tariffs to keep track of the inflationary impulse. There is no evidence of a tariff driven push yet. Soft data might be useful to identify risks of a turning point.

Key takeaways

April's CPI is unlikely to show sharp goods inflation acceleration despite tariff concerns.

We developed a model that predicts tariff impact on PCE categories, used it to separate most exposed components and track the inflationary push from tariffs.

There is no clear evidence of tariff-driven price increases in goods or services yet.

Soft data might be useful to identify a turning point. S&P manufacturing PMI output prices is a better predictor of core goods inflation than ISM prices.

April 30, 2025 MS May US Treasury Refunding Takeaways | US Rates Strategy

Treasury delivers no coupon increases and retains guidance for maintaining current auction sizes “for at least the next several quarters.” Our conviction for no coupon increases over the remainder of 2025 rises. We still see reason for more, not less, T-bill issuance.

Key takeaways

Treasury announced it plans to keep coupon sizes unchanged over the May quarter, increasing our conviction in no coupon increases throughout 2025.

The refunding statement continued to guide current nominal coupon and FRN auction sizes are likely maintained for "at least the next several quarters."

We view discussion on Treasury buyback program enhancements as a clear intent to improve the program's efficacy in helping address significant market stress.

Treasury will give an x-date estimate in 1H May. Robust tax receipts make late 3Q likely; risks skew later from tariff revenue and student loan repayments.

A TBAC charge concludes that large increases in stablecoin issuance would provide increased demand for T-bills.

Here’s an interesting read about recession that hasn’t YET happened and so, a note about rate cuts which are grossly over priced …

Despite very weak confidence readings, hard activity data from the US is still holding up while prices are increasing. We think the current market expectations for Fed cuts will be proven wrong once more.

…The Trump administration has put a serious dent in the long held trust in US foreign relations and institutions, and it is no wonder that we are seeing international investors starting to unwind some of their allocation to US markets. This will go on for a long time in our view, and the risk is that the process could snowball too quickly, leading to an abrupt fall in asset prices, both for US equities and bonds. US government bonds are still the backbone of global financial markets and if investors starts to seriously question their value, of if price discovery becomes hard over loner periods, it will have ripple effects across the world that are not pleasant. This is perhaps the largest risk emanating from US politics as we see it.

Intraday US Treasury volatility reached historical peaks earlier this months, showing a strained market

Ever wonder what Canadians think of OUR economy …

April 30, 2025 RBC: Q1 US GDP: In-line with expectations for a weak starting point

The Bottom Line: Today’s Q1 GDP print gives us an idea of the health of the US economy ahead of tariff whiplash and policy uncertainty – and this starting point was broadly in line with expectations (-0.3% QoQ annualized vs. -0.2% consensus) for a weak start to the year. Of note, the print has some large pre-tariff distortions: a surge in imports drove the trade gap wider and this was only partially offset by a ramp up in inventories.

An important upside surprise: US consumer performed better than we expected and services spending appeared to hold up. As we've discussed, we're monitoring for signs of a slowdown in high income households moving forward and a bleed from soft data into hard data.

Quarterly deflators are still too hot - with the GDP price index at 3.7% and core PCE QoQ at 3.5%, both upside surprises. Monthly PCE data will matter more, particularly as we go further into April, but the story is clear: inflation was too hot even before Liberation Day came into play.

? This next one seems to be more than clickbait and, well, I dunno … times like these when I see stuff like this, well, I lose faith in ‘economists’ and ability to look through ‘the man’ and see the data …

The only certainty economists have about yesterday’s first-quarter GDP data is that it is wrong. Declining survey response rates and economies that structurally change more rapidly than statisticians can measure have conspired to make GDP everywhere subject to more frequent and larger revisions. Nonetheless, broad trends show an economy being rapidly shaped by US President Trump’s policy.

The broad patterns—surging imports, rising inventories, consumer spending spikes—are consistent with US companies and consumers rushing to buy before trade taxes hit. Separate data shows consumers in Democrat states have been more likely to accelerate buying of electronics and furniture than consumers in Republican states (reflecting different narratives in different media bubbles).

Over the past four years, there has been a dramatic increase in US factory building. This reflected localization, and those factories will likely be filled with more robots than people. First-quarter data showed a small but definite slowdown in factory building—perhaps reflecting companies’ uncertainty about erratic policy…

… Sorry BUT there seems to me to be more a political view and effort to sell this view with readers and essentially tell them what he thinks they wanna hear … Don’t get me wrong … economy could very well be less than meets the eye and headed for recession. Others far smarter than HIM have said as much (and are quite long of bonds …) but simply offering a politically charged bit of click bait … well … seems to me to make at least HIM more uncredible …

Just one man’s un-informed view.

Covered wagon rolls in talkin’ GDP, ECI and …

April 30, 2025 Wells Fargo: GDP Contracts as Import Surge Brings Record Drag from Trade

Summary The U.S. economy is at a greater risk of recession now than it was a month ago, but this 0.3% contraction in Q1 GDP is not the start of one. It reflects instead the sudden change in trade policy that culminated in the biggest drag from net exports in data going back more than a half-century.

April 30, 2025 Wells Fargo: Some Goods News for the Inflation Outlook: Q1 ECI

Summary The first quarter's employment cost index reflected the ongoing softening in the labor market. Labor costs advanced 0.9% in Q1, bringing the year-over-rate down to nearly a four-year low of 3.6%. While concern about inflation has picked up amid dramatic changes to trade policy, inflationary pressures from the labor market continue to subside.

April 30, 2025 Wells Fargo: March Consumer Spending About More than Just Tariffs

Summary A March spending pick-up was about more than getting ahead of tariffs, although a surge in auto sales was the biggest driver. The next five largest increases were all services categories. Ultimately, income will determine the capacity for spending and that's holding up, for now.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

To The Terminal dot com for a couple of VIEWS …

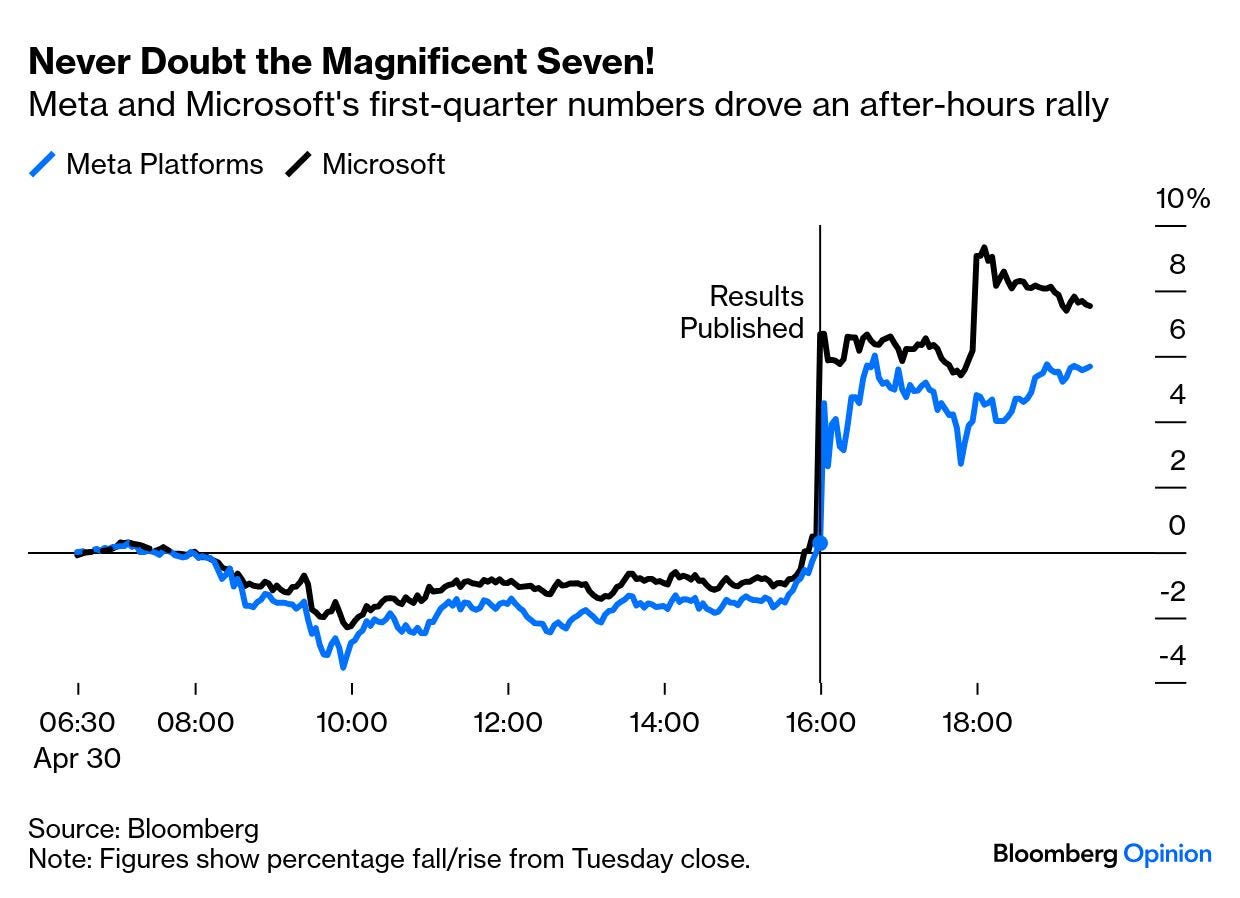

May 1, 2025 at 4:09 AM UTC Bloomberg: Liberated But Not Yet Free There are good reasons stocks have recovered since April 2. But a new date looms and the risks are to the downside.

… Barring really bad news to start the American day, the S&P 500 has a good chance to complete the recovery Thursday, thanks to the latest download of second-quarter corporate results. After Wednesday’s close, Microsoft Corp. and Meta Platforms Inc., both members of the Magnificent Seven, unveiled earnings. Their performance in after-hours trading shows what the market thought of them:

You can find the full details of the earnings here, but the key points included that the companies werestill growing revenues, they claimed that their artificial intelligence offerings were growing in profitability, and they weren’t relenting on their capital expenditures. Faith in the ability of the tech platforms to continue to make money without let or hindrance has been shaken since the Magnificents surged compared to the rest of the market in the post-election Trump Trade. As the seven are all US-based, the doubts about their business models also fed into the retreat from the so-called American Exceptionalism trade. Their results so far (with Amazon.com Inc. and Apple Inc. to look forward to tomorrow), suggest that it’s still unwise to doubt them:

All the more impressive is that as the stock market has managed to stage this rally despite gathering evidence that US economic growth is faltering, as Points of Return covered yesterday. Wednesday brought the news that the first estimate of gross domestic product for the quarter ended Marchdeclined 0.3%, only the second quarterly fall since the pandemic and the first in three years:

GDP is backward-looking, and many data matter less now if they pre-date the point at which the tariffs begin to have an impact. Nevertheless, growing evidence that a recession is approaching would, in normal circumstances, be expected to bring share prices down rather than up. That stocks have looked through the economic figures is in part thanks to a strong earnings season so far — and also to growing confidence that the tariffs will be far less draconian than currently planned. Which brings us to another topic…

May 1, 2025 at 9:00 AM UTC Bloomberg: US Economic Weakness Is Being Exaggerated – For Now Sentiment surveys have taken a dive, but the data on consumption and the labor market won’t catch up until much later this year.

One of the better, well known techies out there on twitter …

at PeterLBRANDT

One of my favorite trades all 2025 has been long Treasury futures contracts. My line down to 2.5% on 2-Yr Bonds was put on chart in Feb $USO2Y

Finally, an alternative view of the ‘flation data …

Apr 30, 2025 WolfST: Inflation Is in the Revisions? What Stands Out Once Again in the PCE Price Index? Sharp Up-Revisions of Prior Month’s Inflation

Up-revisions pushed the 12-month core PCE price index for February to +3.0%, and the 6-month index to +3.4%, worst since July 2023. But March was benign?