Good morning … Writing and wasting of time — yers and mine — in the moments here just ahead of the most important data point of the month (?) never feels write (see what I did there)?

Some news overnight …

ZH: Futures Jump After China Says It Is "Evaluating" Trade Talks

… and then there was this …

ZH: Japan's Finance Minister Threatens Liquidation Of US Treasuries, Sparking Shock, Confusion

… Addressing a question on a Tokyo TV program on Friday, Japan FinMin Kato said the country's $1.1 trillion in Treasury holdings - the highest of any foreign creditor - could be a "negotiation card" in its trade talks with Washington but "whether or not we use that card is a different decision." In other words, Japan is threatening to sell some/all of its $1.1 trillion in bonds if tariffs are imposed.

… and here we are.

Knicks won (although my internet connection went down mid Q4 :( and I had to watch on my phone … and it was a late night.. I’ve got little to NOTHING on my mind here / now, ahead of the data and given Global Wall has more than lots to say to us all just ahead of the NFP (see below), I’ll be brief … usual recaps / victory laps to follow over the weekend.

For now, I’m going to lead another MONTHLY visual (5s HERE) in effort to take more wholistic // bigger picture approach … stepping back in order to view view all of the day to day machinations with some greater context … lets jump to the longer end of the curve …

30yy MONTHLY: triangulating range between 4.95% (buy) and 4.55 (sell)…

… longer term, stochastics are looking to ME to be headed towards and overSOLD BUY (where momentum nears a peak, rolls over and then offers up a more bullish cross — see green circle / inset above) …

… to be sure, I’ll be watching the daily and WEEKLY close, too but for now, well I’m movin’ right and and useless as they may be, on claims just ahead of NFP …

CalculatedRISK: Weekly Initial Unemployment Claims Increase to 241,000

ZH: Jobless Claims Jumped Last Week As 'DOGE Actions' Spark Biggest YTD Layoffs Since 2020

… AND mfg …

ZH: 'Beneficial Switching Away From Imports' - US Manufacturing Surveys Signal No Recession In Q2

… AND I’ll be done, for now, and hope to doge some of the rain over the weekend but use it to my advantage and drop back into yer inbox with some of the NFP victory laps. For now, though … here is a snapshot OF USTs as of 652a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: USD softer whilst US equity futures gain ahead of US NFP, AMZN/AAPL dip post-earnings … USTs are contained into NFP. The headline is expected to show a marked cooling in the pace of Payrolls to 130k (prev. 228k), with a range of 25-195k. The report will be scoured for signs of Trump’s tariffs and associated reciprocal measures impacting the US labour market. USTs holding around 112-00 in 111-23+ to 112-01+ confines, a tick below Thursday’s base but some way clear of that session’s 112-20 peak; the high occurred in the early US morning, before the ISM release. On the trade front, US trade relations with constructive reports in the FT around EU concessions to address the trade deficit with the US in addition to reports that the US has reached out to China to seek talks alongside constructive MOFCOM language.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Manufacturing. Its whats for dinner AND more than meets the eye …

1 May 2025 Barclays: ISM manufacturing: More than meets the eye

The ISM manufacturing PMI deteriorated just 0.3pts in April, to 48.7. The details paint a more somber picture, with signs of fallout on supply chains, production, and external trade following tariff announcements. Comments point to intensifying fallout on demand and supply.

Claims ahead of NFP … worth a look? You decide …

1 May 2025 Barclays: Spring break head-fake in initial claims

Initial jobless claims under regular state programs rose 18k, to 241k, the highest level since mid-February. New York initial claims drove the increase on the back of a later-than-normal spring break that allowed school bus drivers to file unemployment claims they normally would not have.

Same shop with an excellent NOT NFP related read …

The sanctuary city funding standoff continues, with three new executive orders targeting these jurisdictions. Immigration data through March indicate a halt in humanitarian immigration and an annual pace of approximately 120,000 deportations.

14 sanctuary cities received a preliminary injunction prohibiting the administration from freezing funds. President Trump returned $2.2bn in FEMA SSP funds following a court order.

Trump's three new executive orders explicitly targeting sanctuary jurisdictions suggests that he will likely continue to threaten to claw back federal funding. Jurisdictions would face the onus of having to contest clawbacks in court, facing budget uncertainty in the interim.

Net immigration data through March shows a halt in irregular immigration post-Trump inauguration, with ICE detention data suggesting a modest rise in detentions and deportations compared to the Biden administration. Our thematic research team estimates deportations are currently running at an annual pace of 120k.

New York's FY2024 migrant costs came in lower than expected and the drop-off of immigration inflows should lower cost projections going forward, a credit positive.

We extend our previous analysis of the effect of the drop-off of immigration flows to all states. We highlight the top 5 sectors that are most vulnerable from a labor force perspective: agriculture, construction, trucking, food and beverage services, and housekeeping sectors.

Notably, irregular immigrants make up 54% of the crop production labor force in California and 51% in Washington, 32% of the construction force in Texas, and 32% of the warehousing and storage force in New Jersey – a medium-term labor headwind.

A rather large French shop (after extending long / tgt on 10s) on RATES and separately, on 100yrs of tariffs and stocks …

01 May 2025 BNP US rates: Positioning for bimodal risks

Fed rate pricing appears to be reflecting bi-modal risks – a risk of non-linear repricing of more cuts in 2025, or the risk of gradually shifting out cuts to 2026. Given these bi-modal risks, and yet non-linear risks to the more cuts, we like positioning for lower yields, but with limited downside.

These bimodal risks are well reflected in history. When the Fed delivers rate cuts, they have invariably outpaced market pricing. However, recent history highlights the reason for caution, where the trade suffered amid an inflation fighting Fed.

We favor a mis-weighted 1y1y receiver ladder over a more typical 1 x – 1 x -1 implementation or a 1 x -1 receiver spread. The mis-weighted structure avoids short delta and vega exposure at the outset and offers a better terminal payoff profile, in our view.

Trade: Buy 1y1y A-50/A-125/A-150 receiver ladder (1.75 x -1 x -1) at 16bp. Target: 65bp. Stop-loss: 3bp. Carry: -1bp/1 month. 1y1y forward: 3.06%.

02 May 2025 BNP: Equities: 100 years of crashes - Tariff watch

Tariff crash: Market crashes that occur without a significant economic downturn can be large and volatile but tend to be relatively brief. Price action for equities this year is so far consistent with prior non-recessionary crashes. However, we think the rally off the lows is more a function of position capitulation than an ‘all clear’ signal for risk. Mega-cap Tech earnings have also helped. Our base case is that a combination of earnings downgrades and PE compression could see equities retest YTD lows.

A grind lower: In both the US and Europe, we think a spot leg lower might see skew underperform. Our US Equity Positioning Indicator (BNPEPUS) is in defensive territory, which has historically implied worse performance for skew. With spot back at pre-Liberation Day levels and vol at recent lows, timing looks attractive to revisit hedging. However, we would be mindful that a next leg lower could be much more of a grind lower, with less explosive downside moves. This drives our preference for hedges such as put spreads or VKOs, rather than more convex and explosive tail hedges such as VIX or V2X calls.

For the bulls: In the US, we think the rally off the lows has been a short-term positioning squeeze. For those looking at SPX upside, we would keep trades very short in maturity and tactical. For investors who want to position for a more sustained upside rally, optionality in Europe could be more attractive.

Here’s a quick recap of yesterday AND a counter-narrative narrative I think you’ll wanna spend time with at some point …

… Looking back at yesterday, the tech earnings the night before played a big role in the market rally, with the Magnificent 7 surging +2.79%, alongside a +1.52% move for the NASDAQ. Microsoft gained +7.63% and Meta +4.23% after their results. Nvidia posted a +2.47% advance, also helped by a Bloomberg report that the US is considering easing restrictions on Nvidia chip sales to the UAE…

…Yesterday’s data also triggered a notable rise in Treasury yields, which unwound their initial decline after the ISM manufacturing release. With the release better than expected alongside the wider risk-on tone, investors dialled back their expectations for Fed rate cuts, and the 2yr Treasury yield moved up +9.6bps on the day to 3.70%, whilst the 10yr yield was up +4.86bps to 4.22%.

The damage done to US assets in April gave us a rare opportunity to assess what investors say they want verses what they actually do.

This month, we look at the key narrative drivers around the sell-off in US markets. Our conclusion is rather contrarian – many of the recent moves, even after the sizzling volatility in early April, seem overdone and could mean revert. And even though more policy volatility is likely, the “Sell America” narrative may have passed its peak. That means there may be too much fear about the dollar’s status, US consumer health and broader confidence in American assets.

Key market-moving themes this month:

'Haven' assets? – The US equity and bond selloff that culminated in a tariff pause for most countries reignited the ‘haven asset’ narrative around gold and several FX crosses. We parse the sell-off and show whether that narrative held in practice and point to other, perhaps more plausible explanations.

Uncorrelated assets – Few assets proved to be havens from the equity sell-off in April. And the prospect of more volatility in the US is likely to keep investors focused on trying to diversify the risk. We look at how various assets performed last month relative to their correlation with S&P 500 and update our analysis on the least correlated and most attractively priced assets.

Are concerns about the US consumer overdone? – Unsurprisingly, US consumer stocks sold off heavily last month amid concerns about US demand in the wake of tariffs. We take a look at whether, on a relative basis, US assets in the sector may now look attractive despite falling consumer sentiment in the surveys.

The dollar does not risk losing reserve status – The dollar’s selloff since the start of the year continues to fuel the narrative of its demise. We argue such concerns are overdone, putting recent moves in broader context as well as some implications for corporates.

Have markets priced in any medium-term fiscal stimulus creating greater risk? – The dumping of US assets last month has created downward pressure on other sovereign yields, especially in Europe. Widening credit risk in the US was part of the reason. But the magnitude of the move may well reverse, paving way for better pricing of risks from the need for European stimulus.

…It was the selloff in long-end USTs on April 8-9 that sparked the eventual U-turn on tariff announcements. But contrary to the narrative, there were no “haven assets” during the early April sell-off.

Same German shop with interesting note / thoughts on Fed now allowed to focuse solely on tariff impacts …

1 May 2025 DB: Data DBrief: Financial conditions allow Fed to focus on tariffs' inflation effects

In this note, we update our high-frequency version of the Fed's FCI-G to quantify the impact on expected growth from recent moves in asset prices. After spiking tighter due to the market turmoil in the wake of the April 2nd tariff announcements, financial conditions have eased back closer to where they started the year. As markets have calmed down some, conditions have returned to being a slight tailwind for growth.

The dollar depreciation has driven most of this easing, more than offsetting the tightening from lower equities and wider mortgage and corporate spreads. Though the weaker dollar may, at the margin, help on the growth front, it could end up exacerbating the tariffs’ passthrough to consumer prices (see “US outlook: Tariff-struck”). Indeed, absent a meaningful downside miss in tomorrow’s April jobs report, less headwinds to growth from financial conditions should keep the Fed more focused on the inflation outlook.

We think Treasuries have settled back to a more typical role, as the traditional comfort blanket should risk assets sell off, or on any negative news for the economy. Should Friday's payrolls come in as expected, little reaction is likely though. The biggest reaction would come from a materially weak number. But it just might a tad early to get that

We interrupt regularly scheduled NFP precap for a distant FOMC meeting precap … because, you know, that’s just what you need / wanna read ahead of the data today …

May 1, 2025 MS: Federal Reserve Monitor: May FOMC Preview: Well Positioned to Wait for Greater Clarity

We think the Fed will say the tariff shock is likely to create tension in the dual mandate (higher inflation and lower employment). We expect the Fed to lean in the direction of emphasizing price stability, though it will leave the door open to action if the labor market weakens unexpectedly.

Key expectations

We expect the Fed to stay on hold at its May meeting and make no change to its balance sheet policies.

The Fed is unlikely to act preemptively given its expectation that inflation will be firming, and the size of the tariff shock could produce persistent inflation effects.

A Fed that wants clarity before taking any action is likely to be on hold into the second half of the year, if not longer. We think the Fed is on hold in 2025 before moving to cuts in 2026.

Our rates strategists suggest investors maintain positions for a steeper yield curve - UST 3s30s steepeners and term SOFR 1y1y vs. 5y5y steepeners - as we expect a lower market-implied trough rate.

The agency MBS strategists stay neutral, acknowledging that the near-term uncertainty and possibly elevated vol is balanced by attractive valuations.

Munis: We think TOB activity remains elevated given that long-end spreads remain wide.

The outlook for the upcoming payroll figures is highly uncertain. After March’s blockbuster 228,000 advance in payrolls, we look for payrolls to have increased in April by just 25,000 (consensus 135,000), although the margin of error is high. The BLS says the initial estimate for payrolls is accurate to within +/-136,000, so markets routinely react to payroll numbers where the difference from the consensus forecast is indistinguishable from noise. In any case, if realized, the latest two-month average would be 127,000 and put the year-to-date average at 120,000. The median estimate among the Bloomberg consensus and our forecast is for the unemployment rate sticks at 4.2% (after 4.152% in March).

We attribute some of the expected slowing in April payrolls will reflect a giveback following outsized strength in March, but policy uncertainty also tends to delay hiring…

Construction spend as an input to GDP and so, important consideration going forward …

May 1, 2025 Wells Fargo: Construction Spending Slides in March Broad-Based Weakness Reflects Mounting Macroeconomic Headwinds

Summary Residential and Nonresidential Construction Edge Lower

Overall construction spending dipped 0.5% in March, a weaker-than-expected outturn propelled by declines in both residential and nonresidential spending. Residential construction spending registered its first slip in six months, largely driven by a drop in home improvement outlays. Single-family outlays also showed signs of waning momentum, posting a modest 0.1% upturn. Meanwhile, nonresidential construction spending worsened across both public and private projects as high interest rates and heightened economic uncertainty suppressed new building. If a silver lining can be gleaned, it is that multifamily construction appears to be stabilizing following a year-long downdraft, reflecting persistent affordability challenges facing single-family homebuyers.

Tariff-driven increases in materials prices and broader macroeconomic headwinds stand to constrain overall construction spending in the year ahead. Single-family housing starts contracted 14.2% in March as builders surveyed by the NAHB revealed that tariffs are likely to raise construction costs by $10.9K per single-family home. Ongoing softness in architecture billings, compounded by a stark decline in new project inquiries, also point to a weaker pace of nonresidential construction moving forward.

Finally, a question we MAY be on verge of getting AN (not THE) answer on …

The good news is that the Magnificent-7 are still magnificent. Three of them (Alphabet, Meta, and Microsoft) beat earnings expectations for Q1. We've been arguing that while AI may or may not make money for the providers of Large Language Models, the result will be more demand for cloud computing. That should be good news for at least four of the Mag-7.

The bad news is that recent economic reports have boosted the probability of a recession in recent days, according to Polymarket.com (chart). Our subjective probability of a recession remains at 45%. Let's review the latest relevant economic indicators:

(1) Consumer confidence. On Tuesday, we learned that the Consumer Confidence Index (CCI) fell to a nearly five-year low in April, down 8 points to 86.0. It's the fifth straight monthly decline, the worst such stretch since 2008. The decline has been led by the CCI's expectations component. The present situation component is relatively upbeat. However, the ratio of the present to the expectations components soared in April as it did prior to past recessions (chart)

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Positions and a couple of views from THE terminal dot com …

May 2, 2025 at 1:10 AM UTC Bloomberg: Bond Traders Bet on Tariff-Fueled Jobs Slowdown Before Payrolls

US bond investors have been piling into bets that President Donald Trump’s tariffs will slow the world’s largest economy and force the Federal Reserve to lower interest rates.

Ahead of Friday’s jobs report, money markets are pricing in almost four quarter-point rate cuts in 2025, one more than was anticipated before Trump’s big tariff announcement last month. Meanwhile, positioning data from Wednesday has shown growing long positions on shorter-dated US Treasuries. It’s a bet that the hit to economic growth from Trump’s sweeping tariff package will be bigger than its inflationary impact.

Yet the expectations of a sharp slowdown are also subject to ongoing reality checks from economic data: On Thursday, traders rushed to unwind some of their bets on rate cuts after a manufacturing survey came in stronger than anticipated. The tense atmosphere increases the focus on April’s non-farm payrolls report, which will offer an early glimpse into how the tariff uncertainty is playing into the labor market.

“Concerns over much weaker growth are more than offsetting the near-term upside risks to inflation from tariff hikes when market participants weigh up the implications for Fed policy,” said Lee Hardman, a strategist at MUFG.

The big question for bond investors is whether and if the economic pessimism that has been seen in recent surveys will seep into top-tier measures of employment and consumer spending. US consumer confidence fell in April to an almost five-year low, while a gauge of US manufacturing activity shrank in April by the most in five months.

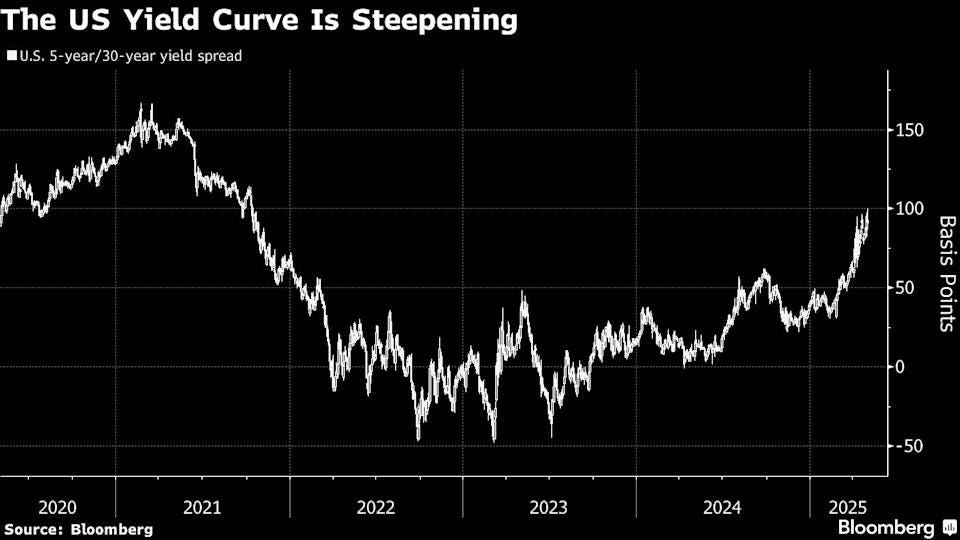

Signs of economic weakness have driven a rally in shorter-dated US Treasuries this month. That’s steepened the yield curve, with two- and five-year notes outperforming 30-year bonds in April by the most since early 2023.

Complicating matters for the economic outlook is uncertainty over what tariffs will eventually be instated and when, with US negotiations with key trading partners underway or being planned. On Friday, China said it is assessing the possibility of trade talks after weeks of stalemate, while Japan said discussions will likely gain momentum in mid-May.

Japanese Finance Minister Katsunobu Kato even hinted at the possibility of using its vast Treasuries holdings of US for leverage, although it’s unclear how serious he was about the idea. With some $1.1 trillion in holdings, investors in the East Asian nation are the biggest overseas owners of US debt.

Ten-year Treasury yields edged higher in Asia trading Friday, up two basis points to around 4.24%.

Hard Data For now, Fed officials have been waiting to see what the ‘hard’ data reveals, while remaining an guard against the possibility that tariffs will push up inflation. Speaking last week, Fed Governor Christopher Waller said that he’d support rate cuts if there’s a significant rise in unemployment, which could happen if Trump reinstates more aggressive tariff levels and firms begin laying off more workers.

“The labor market slowing down is necessary for the Fed to continue their easing process,” said Gargi Chaudhuri, chief investment and portfolio strategist, Americas at BlackRock.

While a weaker jobs print for April would be “a step in that direction,” she said the Fed needs to see further weakness beyond one piece of data. “They have to take the totality of the data and I don’t think one weak data print will be sufficient for them to hint at, or continue their rate cutting cycle.”

The Fed is currently observing a communications blackout ahead of its meeting beginning on May 6. Traders are betting on around four quarter-point cuts in 2025, with the first likely in June. As recently as mid-March, only two cuts were priced in for the year.

“If we start to see the economy turn in a meaningful way,” that sets the stage for the Fed to react “and probably quite forcefully,” later this year, Michael Cudzil, portfolio manager at Pimco told Bloomberg Television on Wednesday. Pimco has been increasing its exposure to the belly of the Treasury curve, between the five and 10-year maturities, said Cudzil.

Economists expect the jobs report to show 135,000 new positions in April compared to 228,000 in March. Most, however, believe the data will only offer a limited insight into the impact of higher US tariffs. Even if the report comes in strong, investors may view the data as backward-looking and continue to expect layoffs in the coming months.

The April data due Friday will be the “last solid reading before the storm,” a Bloomberg Economics team including Anna Wongwrote. “The labor market may begin to deteriorate more visibly as soon as May.”

An options trade focused on price action around the payrolls event — the one-day Treasury 10-year options straddle that expires at the end of Friday — is currently implying a roughly nine basis point move in the 10-year yield for the session, broadly in line with prior payroll readings.

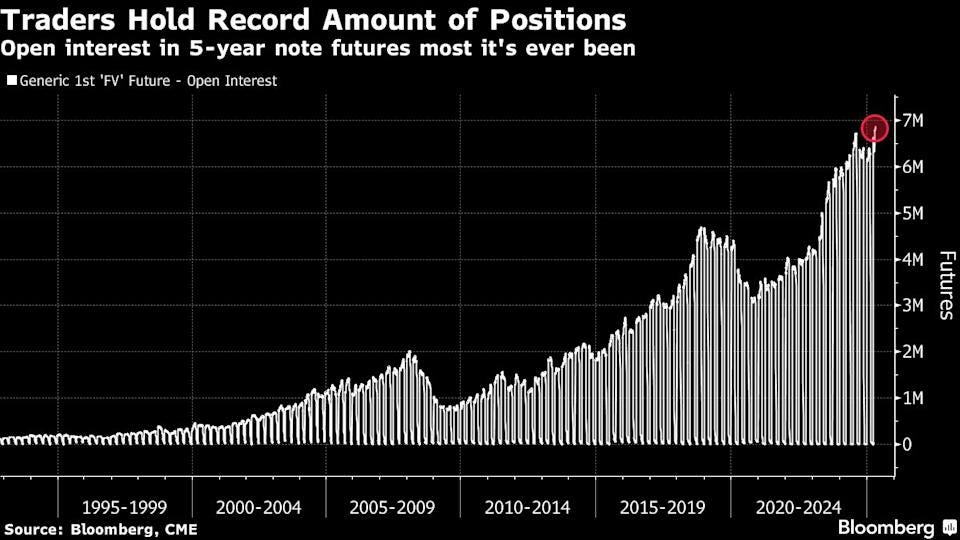

In Treasury futures, open interest, or the amount of risk held by traders, has risen sharply over recent sessions after the selloff that initially greeted the tariffs announcement. In the five-year tenor, open interest has climbed to the most on record since the first data collection in the early 1990s…

at AnnaEconomist

If April jobs report tomorrow is weak, markets will freak. If it is strong, markets simply will already move on to May and June's jobs report.

The reason why we think May and June jobs reports are going to be very weak is because three sectors basically drive all of seasonal job growth in those two months, and at least 2 of those 3 sectors (leisure and hospitality, and logistics) will undershoot.

As at FreightAlley has already covered extensively, the logistics sector employment will be hit in May. So another way to look at this is, that the number of container ships departing China for US peaked on 4/16 and plunged 45% since...it takes 21 days to arrive at US...so this means that May's payroll period exactly falls in this period of import volume plunge.

But above all, it's the leisure and hospitality sector that will be account for the weakness in May and June.

May 2, 2025 at 5:02 AM UTC Bloomberg: Markets Can’t See a Recession Through the Tariffs In all this confusion, a clearcut indicator isn’t ringing the alarm bells it should. By John Authers

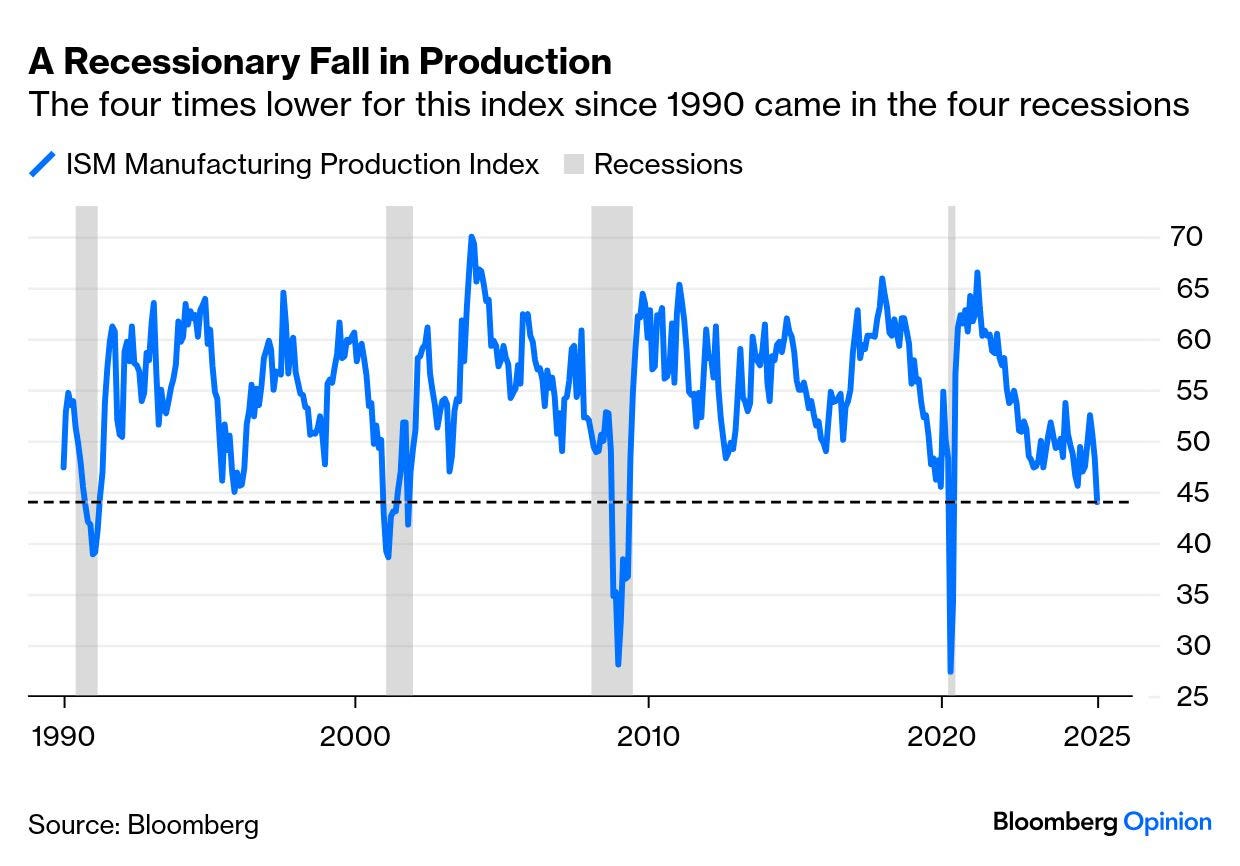

…When is an unambiguous recession indicator something investors can completely ignore? Answer: When tariffs are clouding perception so badly that nobody is quite sure of anything. That at any rate seems the conclusion as we approach the end of the first-quarter earnings season, while the hard economic data for April begin to roll in.

The Institute of Supply Managers’ manufacturing index, long regarded as one of the best leading indicators of economic growth, was on the face of it alarming. The overall headline number is below the 50 that separates expansion from recession. Within it, the report on how much manufacturers were producing was downright alarming:

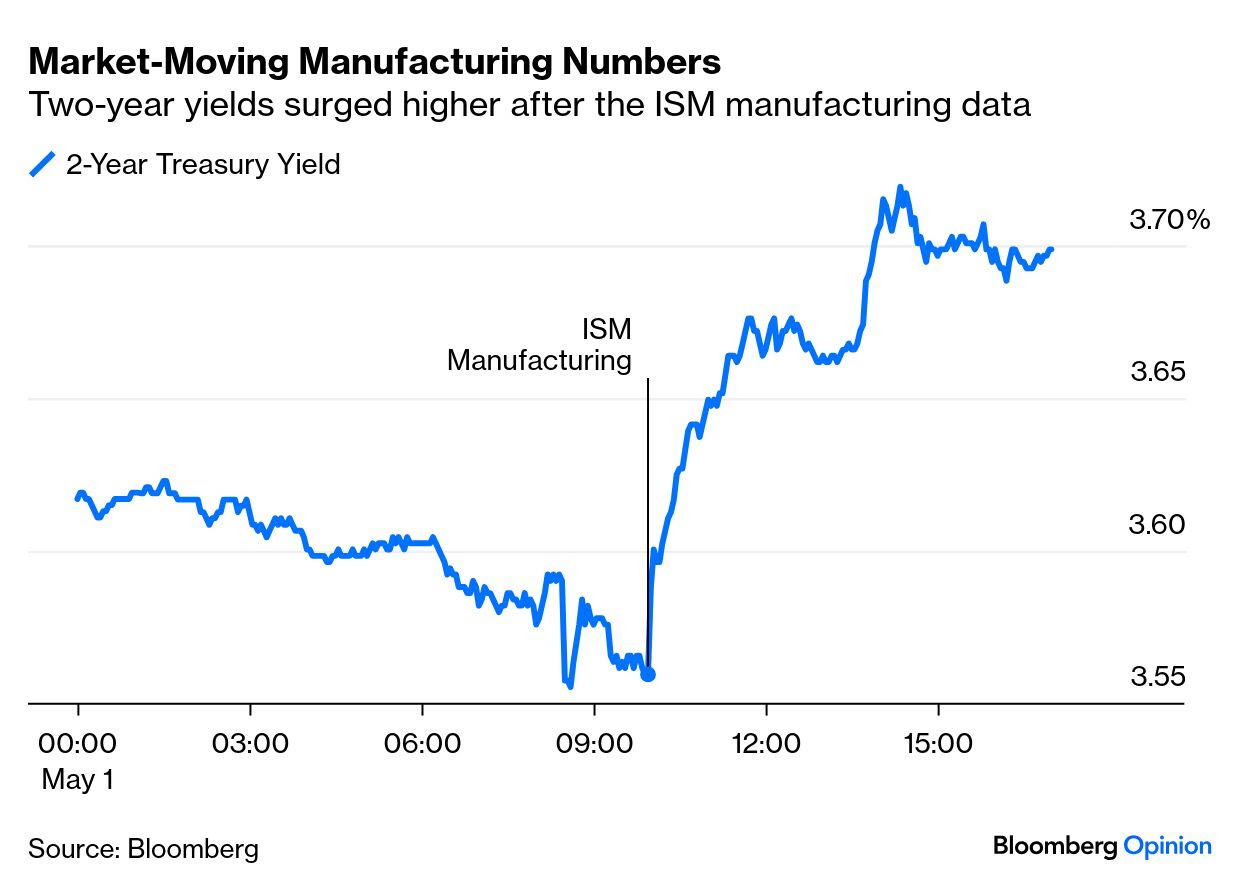

These numbers don’t prove a recession is imminent, but they should certainly prompt risk managers and allocators to shift toward assets that do best in a downturn. That should mean bond yields go down. This is what happened to the two-year Treasury yield on Thursday:

So, unmistakably negative manufacturing numbers caused a sharp rise in bond yields. Why? Mainly because of some bizarre inconsistencies in the report. The overall number wasn’t as bad as the consensus had predicted, largely because new orders were way ahead of estimates. What’s strange is that those estimates had been compiled by comparing with data from new orders coming out of the industrial surveys run by different branches of the Federal Reserve.

In the following chart, from Omair Sharif of Inflation Insights LLC, the red line is the official ISM new orders number, while the dark blue shows the implied figure generated by the regional Fed surveys

Sharif suggests the discrepancy may come from the survey’s different weightings, as the overall ISM is driven by sectors’ overall contribution to gross domestic product — so sectors such as chemicals or computers will take a greater weight.

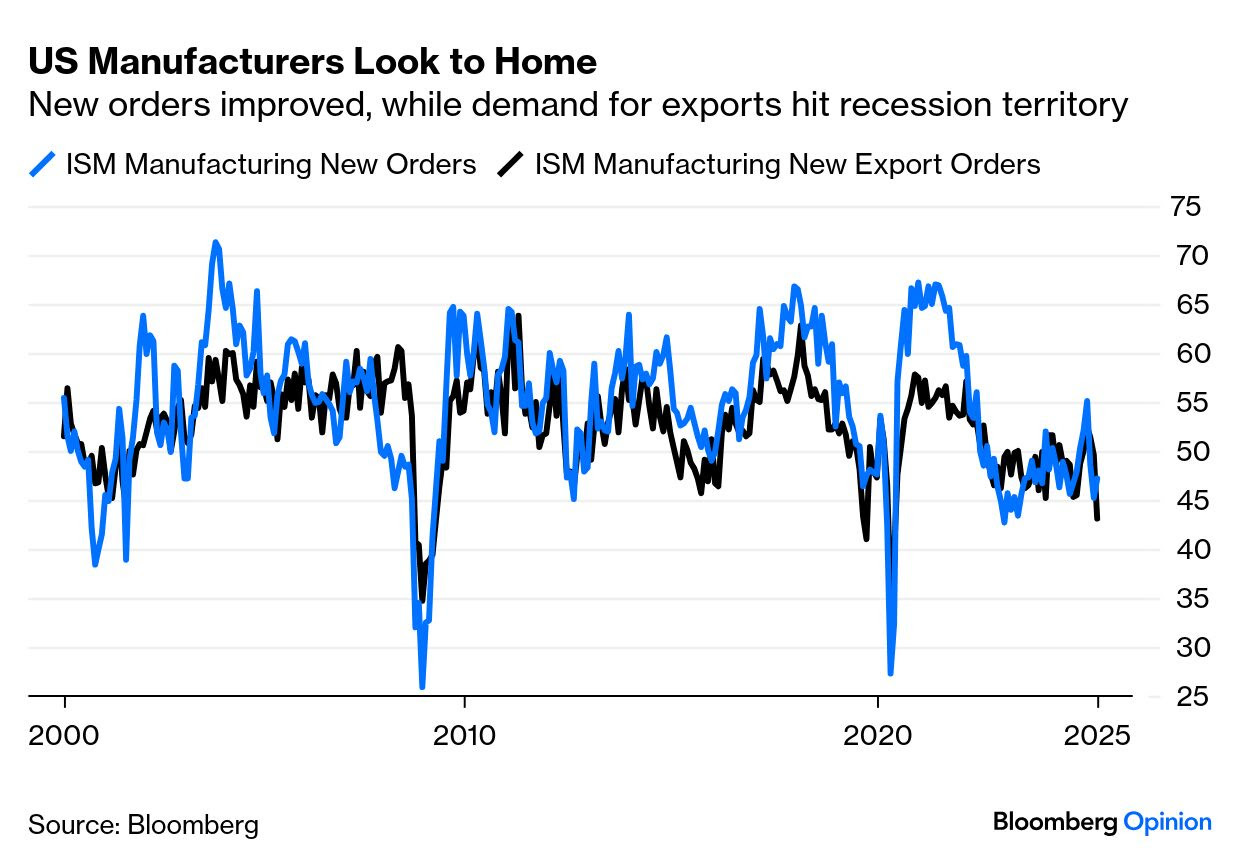

Another problem interpreting the data comes, inevitably, from tariffs. The overall new orders index improved slightly, but dropped for exports to a low previously seen only in recessions. Tariffs are meant to stimulate a shift of demand from exporters to domestic manufacturers, and they are perhaps already having that effect. It does make it harder to gauge the overall direction of the economy: