while WE slept: USTs contained ahead of data deluge, "... twist-flattening after China ..." data; "Safe Haven Again?" (BMO); large options bet Fed UNCH

Good morning … With markets in a steady state of calm, I’m going to lead with updated rates visual ahead of GDP, ECI, Income, Spending, ADP and reFUNding …

10yy DAILY: I’m watching 20bp range (4.25% - 4.05%) …

… as we are in just about MIDDLE of aforementioned range, momentum, here, extending into overBOUGHT territory, might be ‘swing factor’ … some positively perceived data (good for stocks, that is … maybe so bad it’s good in as far as cuts??) COULD lead to a risk ON move funded by … USTs … something to consider …

… in as far as how things are going, you know, on the ground … well …

ZH: US Home Prices Hit A New Record High In February... Except In Tampa

… But as the average national home price rose to yet another record high, prices in Tampa continued to fall...

… depends which ‘ground’ you are ON, I suppose … We all movin’ to Tampa? In other SOFT DATA (not)news …

ZH: Conference Board Consumer ExpectationsPlunge To 14 Year Lows; Inflation Expectations Soar

… Worse still, consumer expectations for the next six months plunged to the lowest level since 2011, while a gauge of present conditions also fell.

… then, a pre jobs look at jobs ahead of TODAYS pre jobs look at jobs …

CalculatedRISK: BLS: Job Openings Decreased to 7.2 million in March

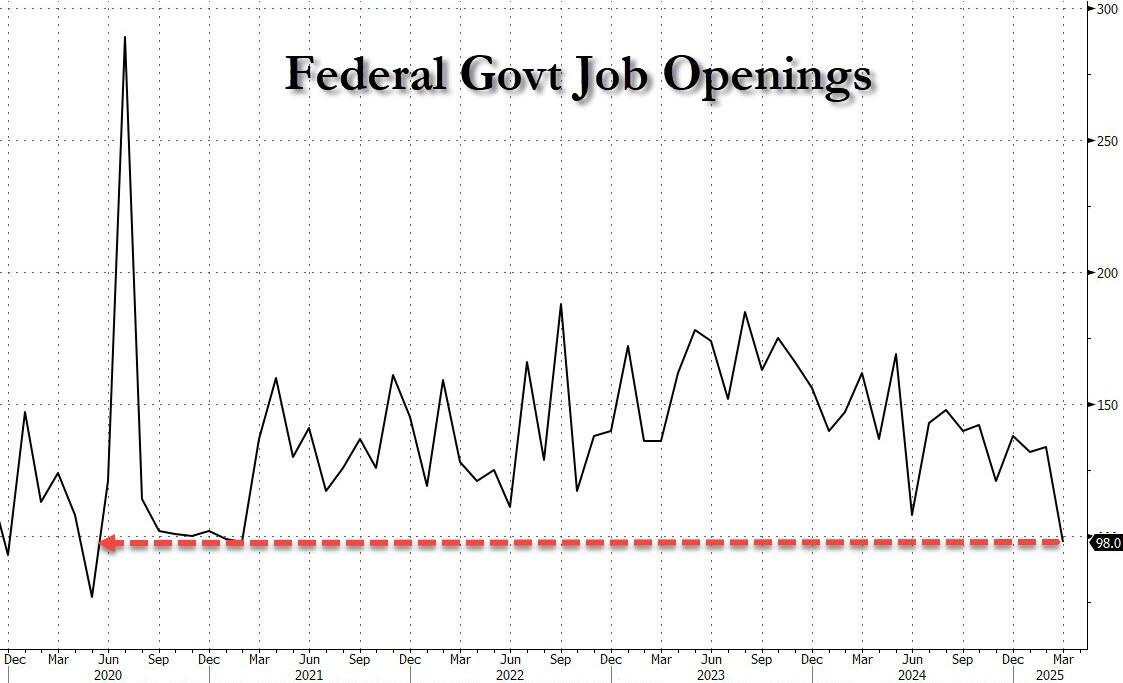

ZH: Deep State JOLTED: Government Job Openings Plummet To 5 Year Low As Total Hires, Quits Jump

… Well, not anymore, and in March, the number of government job openings plunged by 36K, from 134K to just 98K, the first sub-100K print since the covid crash, some five years ago!

… AND I’m done here … let us see what the data and reFUNding brings but for now … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are twist-flattening after China April activity readings offer a starker glimpse of the trade war impact: official manufacturing PMI slipped to 49.0 vs estimates of 49.7, while new export orders came in at 44.7, just above there troughs seen in 2022 and 2020. EU data came in mixed but strong with better GDP (boosted by Ireland, Italy) and higher CPI (German states and Italy beating), though EGBs are outperforming on the fingerprints of a large month-end extension/rebalance flow. Our desk noted some offshore real$ demand in Asia, following by better two-way action in the belly/intermediates in the London morning. S&P futures are showing -0.4% here at 7am, Crude -1%, Copper -4.4%, and the DXY +0.2%. UST volumes are ~75% the 20d average.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Stocks & USTs trade tentatively ahead of a busy data slate and earnings from MSFT & META … USTs are contained into data & refunding, EGBs firmer but largely unaffected by a data deluge .. A relatively contained start to the session with USTs holding onto Tuesday’s spoils, firmer by a handful of ticks in a 112-03 to 112-09 band. Limited resistance in the near-term, nothing of particular note until 114-03+ from early April and thereafter 114-10. On the data front, the docket begins with ADP as a preview into Friday’s NFP. Thereafter, Q1 GDP, PCE and Employment Costs due. Afterwards, we get the monthly PCE figure.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

JOBS data ahead of today’s jobs data ahead of Fridays … never mind …

29 April 2025 Barclays: March JOLTS: Decline in openings seems premature

Job openings moved down from 7.5mn to 7.2mn in March, a second straight monthly decline. This came alongside declines in turnover, led by a diminished separation rate due to a decline in layoffs. Although job openings seem poised for deterioration, March's decline is probably more noise than signal.

Tariffs are not ONLY and forever a negative for USA and data overnight reminds …

30 April 2025 Barclays: China: Trade war starts to hit PMIs

The sharp deterioration in April official PMI was broad based, ranging from new (export) orders to employment to production, with negative spillovers to the services sector. With trade war escalating, we estimate 3% of total employment, or up to ~20mn export-related jobs, could be at risk.

… 10-year yields slipped below 4.17% on Tuesday, confirming the move below the 200-day moving-average of 4.222%. Having now closed below this technical level during two consecutive sessions, the next milestone will be the weekly close. The combination of a widening goods trade deficit, disappointing JOLTS data, and the lowest consumer confidence print since the depths of the pandemic drove a solid bid in the Treasury market that has overshadowed the inflationary angst associated with the higher tariff regime. While we’re cognizant that issuance concerns remain in place – particularly as Wednesday’s Refunding Announcement looms – the price action suggests that Treasuries haven’t lost their safe haven status. At least not yet. To be fair, foreign sponsorship for April’s marquee 10-year auction was strong and flows have not shown any reason to fear a buyers’ strike. Instead, the potential for a sharp drop in overseas buying has shifted into the category of a ‘hypothetical’ or ‘what if?’ As such, it isn’t surprising to see a drift lower in yields in light of the prevailing balance of risks.

Setting aside the potential for a pause in foreign buying of Treasuries, a decline in yields strikes us as the path of least resistance. The drag from net exports will be difficult for many market participants to ignore; particularly given the backdrop of the recent bearish repricing in US equities. April’s Conference Board figures reflect this sentiment and we’re reminded that the lack of confidence tends to curtail consumers’ willingness to spend – or at least spend beyond what’s needed. Given the downshift in the employment data as evidenced by the JOLTS series, there are mounting reasons to approach the 2025 growth outlook from a stance of greater caution and concern. Assuming that Q1 real GDP prints anywhere near the Atlanta Fed’s GDPNow tracker (i.e. a contraction of -2.7%), Trump will struggle to retain the ‘exceptionalism’ narrative for very long. A soft start to the year in terms of growth will also further reinforce concerns about a recession triggered by the trade war and the upswing in uncertainty…

Germany with a few notes of interest … First, a daily dose / recap, then a monthly chartbook celebrating 100d of DJT and finally, a GDP precap

… The main trigger for yesterday’s risk-on mood were headlines that Trump would announce some auto tariff relief ahead of tariffs on auto parts coming into force next weekend. The measures, signed later in day, prevent tariffs on autos and on steel and aluminium from stacking up on top of each other and provides partial rebates for domestic car makers on imported auto parts for the first two years. The President framed the move as giving companies “a little flexibility” at a rally yesterday evening, at which Trump also renewed his criticism of Fed Chair Powell, saying he's "not really doing a good job".

Those tariff headlines supported markets in spite of a weak batch of economic data. That included the Conference Board’s latest consumer confidence indicator, which fell to 86.0 in April (vs. 88.0 expected). Not only is that the weakest since May 2020 at the height of the pandemic, but the expectations component saw an even bigger slump to 54.4, marking its lowest since October 2011 when the post-GFC recovery was stalling and the Euro Crisis was escalating. In the meantime, the latest JOLTS report also showed job openings fell to a 6-month low in March of 7.192m (vs. 7.5m expected). Obviously that’s covering a period before Liberation Day, so markets weren’t too focused on that, but it still meant that the ratio of vacancies per unemployed individuals fell to 1.02, which is its lowest so far this cycle.

The read across for risk assets was probably limited by the fact that the Conference Board reading is still a survey and while the surveys have been consistently negative of late, hard data have been mostly holding up. So it didn’t lead to a major re-assessment about the growth outlook in the way that a negative jobs report might have done. On top of that, the details of the JOLTS report did include some more positive elements, as the quits rate of those voluntarily quitting their job hit an 8-month high of 2.1%. It also didn’t show an escalation in layoffs, as the layoffs and discharges rate fell back to a 9-month low of 1.0%. So it meant investors could still plausibly believe the narrative that a recession would be avoided, even if sentiment had taken a big hit.

However, the more negative data immediately led investors to price in more Fed rate cuts this year. For instance, the amount of cuts priced by December moved up to 97bps, which is the highest since April 8, just before Trump announced the 90-day tariff extension. In turn, that led Treasury yields to fall across the curve, with the 2yr yield (-4.4bps) falling to 3.65%, its lowest level since October, whilst the 10yr yield (-3.6bps) fell to 4.17%…

30 April 2025 DB: Monthly Chartbook: The First 100 days of Trump 2.0...

We’re now 100 days into Trump’s second term, which has proved to be a seismic period for both financial markets and the entire world order. In this short pack we review global and US asset performance in this period and discuss how many things have changed.

Indeed Trump has wasted no time in actioning his agenda, signing an historic number of executive orders and re-orienting US policy across a range of areas.

Most notably, his tariff announcements have taken the average US tariff rate back to levels not seen since the early 20th century, and led to a complete reassessment of the US outlook. A US recession this year is now seen as a serious possibility, in a way that would have been unthinkable at the start of the year.

Europe has been one of the relative winners in this environment as investors have fled the US exceptionalism positions that were so prevalent as Trump's term started. As an example, in USD terms the German DAX has outperformed the S&P 500 by 25.5% since inauguration day.

From here, the next big milestone will be July 9, when the current 90-day tariff extension runs out. As it stands, investors still expect that some sort of trade deals or further extension will be reached. But if those reciprocal tariffs do come into force, then a US recession becomes an even more likely prospect, particularly as other countries would be likely to retaliate. But with the US administration now dialling back the trade rhetoric and talking up the prospect of deals with other countries, there’s still a lot of optimism that another trade shock can be avoided. Whether that proves correct will be the defining question for the entire global order.

The defining theme of the first 100 days of Trump 2.0 was a move to the highest tariff rate since the early 20th century. Even if the recent reprieve is maintained at this stage, it is still likely that the tariff rate will settle at post-WWII highs.

…Even though there were immense concerns about who’d buy Treasuries in the week after Liberation Day, this is actually the second largest rally post inauguration since daily 10yr UST data starts in 1965. 1993 was the largest at this stage

29 April 2025 DB: GDP preview: Imports surge to cause Q1 contraction

Factoring in the March advance goods trade data, we now expect Q1 real GDP to contract -0.9%, versus growth of +1.1%, previously. To be sure, the entirety of the downgrade to Q1 inflation-adjusted output is due to an expected 39.7% annualized surge in imports (ex-gold) ahead of anticipated tariffs – the largest since Q3 2020 (85.7%) which had the effect of subtracting roughly 5.4 ppts from Q1 growth.

That being said, we expect real final sales to private domestic purchasers – our favored gauge of underlying private sector demand – to increase 1.7% annualized. In short, aside from trade-related distortions to net exports, underlying private sector demand growth remained healthy in Q1, though notably lower than the robust 3.2% annualized pace over the back half of last year.

And a recap of the day which was AND yet another … JOBS data ahead of today’s jobs data ahead of Fridays … never mind …

April 29, 2025 MS: Global Macro Commentary: April 29

Carney and Liberals win Canada election; weaker-than-expected US economic data; USTs rally across the curve; USD gains amid auto tariff reprieve; Bunds rally despite Euro Area data beats; CNB members are cautious around future easing; DXY at 99.19 (0.2%); US 10y at 4.172% (-3.7bp)

…USTs rally ~4bp across the curve as the larger-than-expected trade deficit weighs on GDP expectations and the JOLTs data signals softening labor demand with a fall in the vacancy rate …

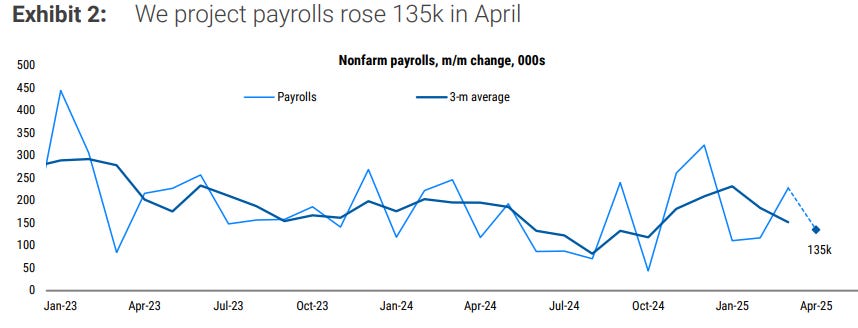

April 29, 2025 MS: US Economics: Employment Report Preview: A downshift in hiring

We trim our April payrolls forecast by 25k to 135k, on the noticeable fall in job openings. Private payrolls (130k) slow slightly from their trend and include one-time boost (20k) from the late-April Easter. Federal payrolls fall. We expect unemployment unchanged and AHE to rise 0.3%.

A French shop with some (US) tech analysis caught my eyes especially on heels of my attempts / focus (here, yest) on 2s) …

2y UST has failed to overcome the 50-DMA (now at 3.95%) in recent rebound attempts, resulting in a gradual down move. It is in the vicinity of last week’s trough of 3.71%. A short-term up move is likely but if 2y UST fails to overcome the MA at 3.95%, the phase of decline may extend.

Below 3.71%, the next objectives could be located at last year’s lows of 3.55%/3.50%.

10Y UST: DECLINE TOWARDS 4.10% LOOMS IF 200-DMA (4.22%) GIVES WAY

10y faced stiff resistance at 4.59% in the first half of April and carved out a lower peak at 4.44% last week. A gradual pullback is taking shape. 10y UST is now challenging the 200-DMA (4.22%) and the descending trend line drawn since January. A brief up move cannot be ruled out but the inability to cross last week’s high of 4.44% could result in a continuation of the down move.

The next potential supports are located at the December low of 4.10% and projections at 4.03%.

…S&P 500: APPROACHING HURDLE FROM 50-DMA AT 5640PTS

S&P 500 has staged a rebound after approaching the graphical level of 4800pts representing highs of 2021/2022/2023. It is now approaching the 50-DMA at 5640pts, which could be an interim resistance.

The index has formed a series of higher peaks and troughs in daily timeframe chart. It will be interesting to see if S&P 500 can establish above the MA at 5640pts. Failure to cross this hurdle can result in a pullback. Recent gap at 5355pts and last week low of 5100pts are short-term supports.

An interesting question which we soon may all be able to answer …

30 Apr 2025 UBS: Did Amazon increase inflation risks?

Online retailer Amazon denied reports it would publish the tariff impact on the price of each item sold on its US website. The general lack of tariff transparency risks higher US inflation by enabling retailers to indulge in profit-led inflation—blaming tariffs for price increases that actually raise profit margin. Lack of transparency also risks consumers blaming tariffs for every price increase, reducing confidence and threatening growth.

US President Trump celebrated their 100 days in office with the expected partial auto tariff retreat, and an attack on Federal Reserve Chair Powell. Trump asserted they knew more about rates than Powell—investors worry Trump’s corporate bankruptcy experience may skew their view on rates toward excess accommodation. US Commerce Secretary Lutnick said a trade deal had been done; the counterpart is still secret, but economists are rooting for the penguins of the Heard and Macdonald Islands.

US March personal income and spending data reflect spending from the before times, but are likely to show consumers bringing forward purchases to beat the tariffs (strongly suggested by the record trade deficit in March)…

JOBS data ahead of today’s jobs data ahead of Fridays … never mind …

April 29, 2025 Wells Fargo: Cautiously Pessimistic: Job Openings Slide, But Layoffs Remain Low

Summary The March JOLTS report showed employers growing cautiously pessimistic about the outlook. Job openings fell to 7.2 million as policy uncertainty intensified, while the hiring rate was unchanged despite a slight pickup in quits garnering the need to backfill more positions. Even as interest in bringing on new workers cooled, businesses are still reluctant to pare back current staff; the layoff & discharge rate slipped in March and remains below its pre-pandemic rate.

April 29, 2025 Wells Fargo: Lost Confidence: Consumers Increasingly Worried About Job Prospects

Summary The drop in April Consumer Confidence tells us that while households are not overly pessimistic on current conditions, they're growing increasingly worried about the future—particularly when it comes to employment prospects and their income.

Finally …

Apr 29, 2025 Yardeni: Consumers Go Shopping To Beat Depression & Tariffs

Stock prices rose and bond yields edged lower today on hopes that the Trump administration will soon start to deliver trade deals and the Fed might deliver cuts in the federal funds rate if the labor market shows signs of weakening. Commerce Secretary Howard Lutnick said today that the administration has its first trade deal, but it is not fully finalized. He declined to name the country involved (Freedonia?).

Today's Consumer Confidence Index (CCI) survey for April showed that current labor market conditions remain solid this month but are expected to get weaker. The March JOLTS report confirmed that the labor market remained robust last month. Let's review the implications of today's data:

(1) Consumer Confidence. As we've long argued, Americans tend to go shopping when they're happy. They also go shopping when they are depressed—the idea being that even the dourest of consumers will pull out the plastic as long as they have jobs. Shopping releases dopamine in our brains, which makes us feel better.

Judging from the Conference Board's CCI, consumers have become more depressed in recent months (chart). The index fell to a nearly five-year low in April, down 8 points to 86.0. It's the fifth straight monthly decline, the worst such stretch since 2008. The decline has been led by the CCI's expectations component. The present situation component is relatively upbeat!

Current assessments of the availability of jobs are holding up relatively well. The ratio of respondents saying jobs are plentiful is roughly double the number saying jobs are hard to get—31.7% and 16.6%, respectively (chart).

Roughly 32.1% of respondents think there will be fewer jobs in September. About half that many—13.7%—expect there to be more jobs in six months (chart). This, however, is balanced by 54.2% thinking conditions will be roughly the same. Considering the bull market in negativity emanating from the economics community, that's a reasonably upbeat scenario.

Also holding up well, all things considered, are stocks. A key reason is that investors believe that the Fed will cut rates if necessary. We aren't in this camp. But it is possible if the "stag-" gets more attention than the "-flation" component of the stagflation risk confronting policymakers….

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Positions matter as they reflect those out there on Global Wall (perhaps it is YOU) putting their money where their mouths are and so, this guy …

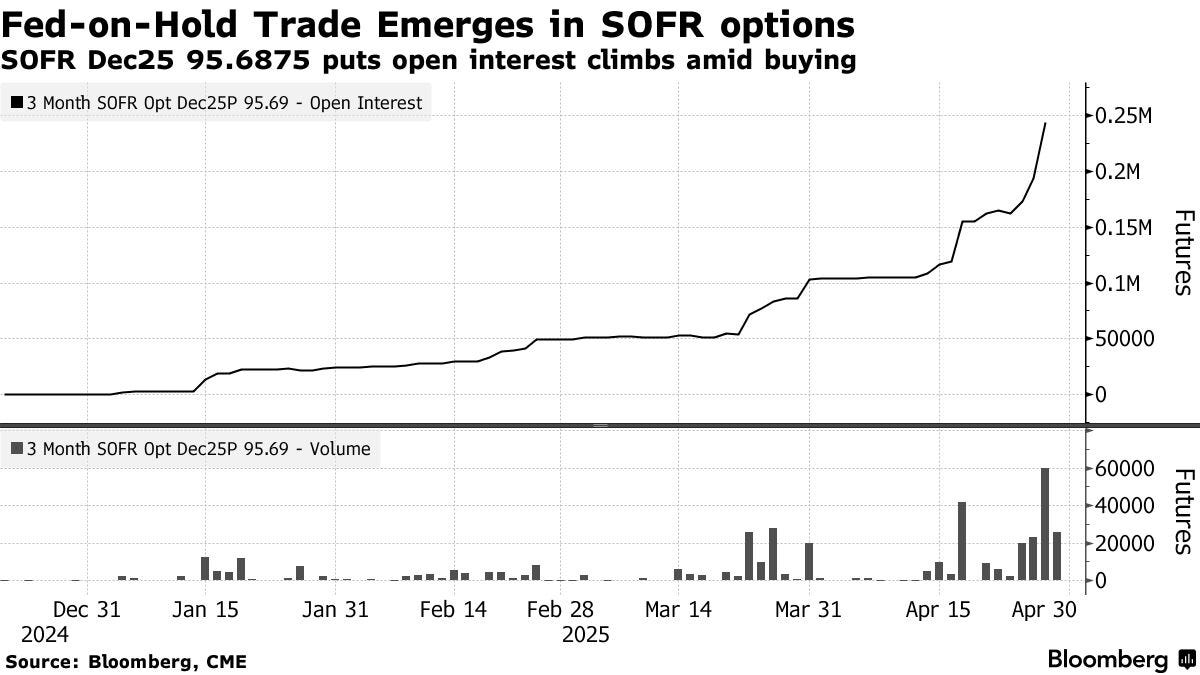

April 29, 2025 at 8:30 PM UTC Bloomberg: $18 Million Options Bet Targets Fed Holding Rates Still All Year By Edward Bolingbroke

At least one big option trader has dialed up an $18 million bet that the Federal Reserve will avoid cutting interest rates any time this year.

Investors in the futures and options markets are, on the whole, still pricing in a rate reduction at the Fed’s July meeting and at least two more this year. But over the last few weeks, a significant position has been building up in an options contract that will pay off if the Fed either keeps rates stable or raises them in 2025.

The open interest, or amount of new risk linked to the trade, has jumped this week, CME data released on Tuesday showed. The wager is tied to the Secured Overnight Financing Rate contracts that track the Fed’s policy path by the end of the year.

Just since last Thursday, one, or at most a few traders, opened up 80,000 contracts betting that the SOFR will remain elevated, according to people familiar with the wager, who asked not to be identified discussing the matter. Trading in many of these contracts is anonymous, making it difficult to identify the firms involved and the exact details of the trade.

Over the last few weeks, the position has grown to approximately 180,000 contracts — or roughly 75% of the total open interest, the traders said. A position of that size equates to a premium of approximately $18 million, based on the price when the position was purchased.

The wager strikes an interesting contrarian note at a time when investors are gaming out where rates and inflation are likely to go as President Donald Trump’s tariffs begin to ripple through the economy. Many on Wall Street have been ramping up bets that the Fed will need to cut rates if the economy begins to slow as a result of tariffs. The recent trade on the December contract is fading those expectations.

Meanwhile, investors have been returning to the cash markets for Treasury bonds after the selloff that initially greeted Trump’s tariffs announcement, with both long and short positions rising slightly over the last week, according to a survey of JPMorgan Chase & Co. clients…

And from placing of actual dollars down on the table TO … a man with a view … of Canada as well as SOFT and some hard data … excerpt / visual of the HARD data which caught MY attention …

April 30, 2025 at 5:00 AM UTC Bloomberg: Canada escaped a Trump trap, but Carney's boxed in He’ll need to keep everybody happy with higher spending to survive, and forget compromise.

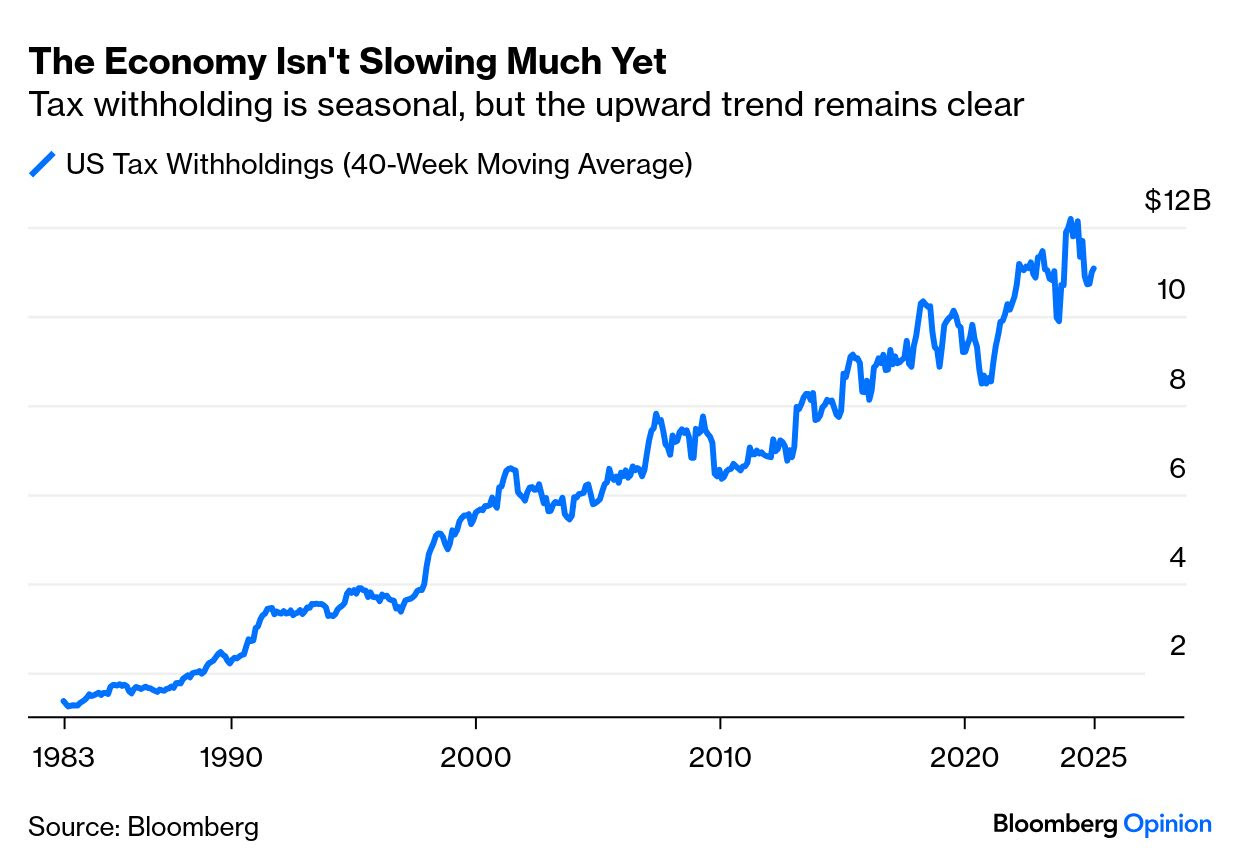

… eal-time data are very noisy but also suggest that the economy hasn’t stopped humming along yet. Larry Adam, chief investment officer of Raymond James, points to tax withholding numbers, which show that tax receipts are continuing on an upward trend. That wouldn’t be happening if the economy was already contracting:

Put all of this together, however, and the chance of a recession looks much higher, with everyone now waiting to find out the impact tariffs have on deliveries, particularly from China. The recent import splurge means it will be a while before we have empty shelves, which could be deadly for the economy. But another almost real-time indicator, of container ship departures from China, suggests that it will come to that eventually unless there’s a climbdown.

Vizion keeps a handy tariff-tracking blog to monitor weekly traffic. This chart is from Elisabeth Werenskiold of Fathom Consulting, and demonstrates a total collapse in shipments earlier this month, once the 145% tariff rate had been announced:

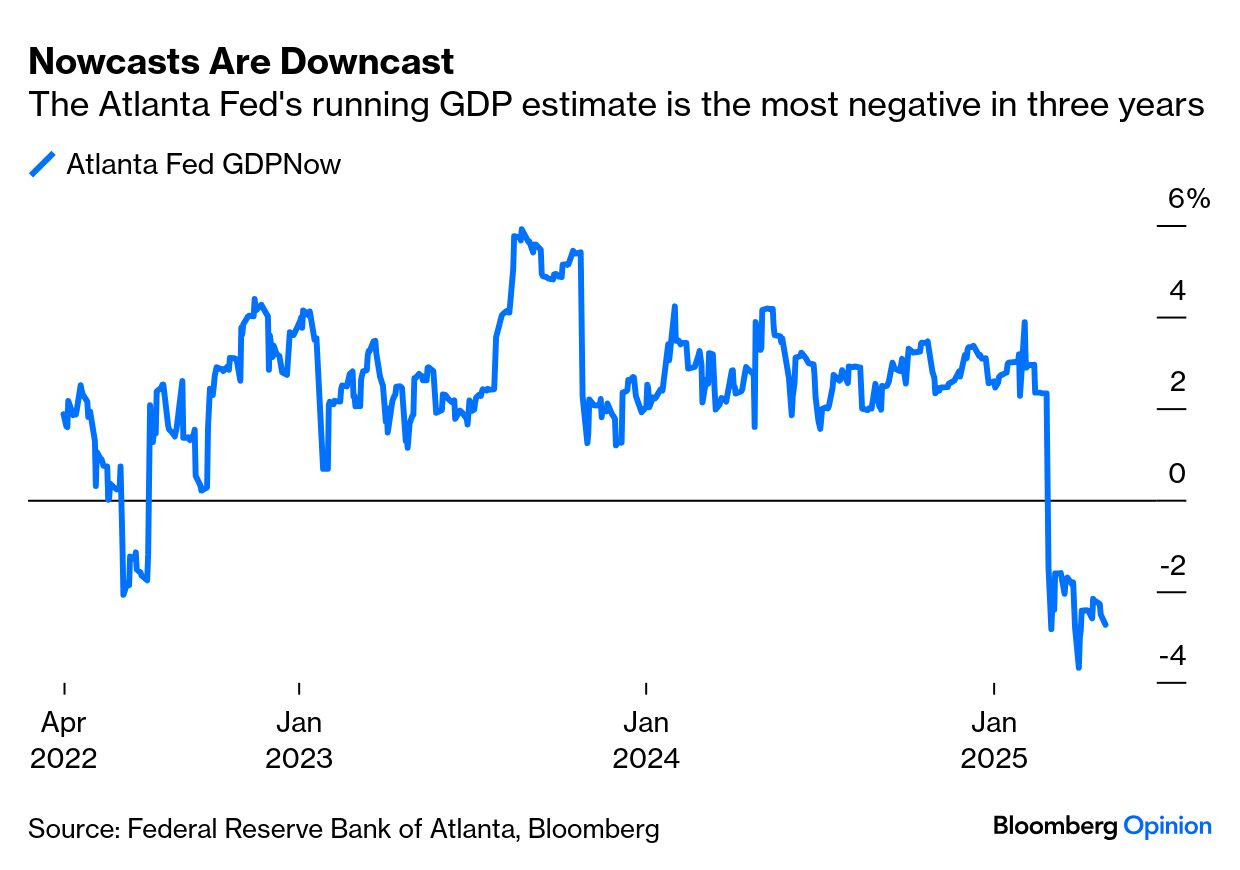

Companies have taken enough evasive action to suggest that it will be some time before all of this shows up in truly current hard data. But the Atlanta Fed’s widely followed GDPNow nowcast seems confident that the point of no return has been passed:

If in a few months the hard data don’t confirm a slowdown after such a nosedive in sentiment, markets should rebound in a big way. But certainty is a way off…

AND I’m nearly done … a friendly reminder … NEVER resist a REST …

https://www.zerohedge.com/news/2025-04-30/common-sense-dictates-fed-will-cut-fed-funds-may

Somebody wake up Jerome Powell.....