while WE slept: USTs under 'modest pressure' BUT...; "Going short UST10Y" (DB); "The Sausage Indicator" (Bespoke); "Pensions versus stock market holdings of US household" (FRED)

… with momentum nearer overBOUGHT and looks to be crossing in favor of higher yields, perhaps a concession for this afternoons liquidity event would be welcomed by Team Rate Cut (and everyone else…)

… and the table was set by yesterdays data …

ZH: Boeing Bounce: US Durable Goods Orders Soar Most Since COVID After June Doom

… and with this bit of GOOD news (putting back into spotlight the question of whether 25bp OR 50bps required?) …

ZH: Dow Hits Record High But Nasdaq Dumps As Oil & Gold Jumps

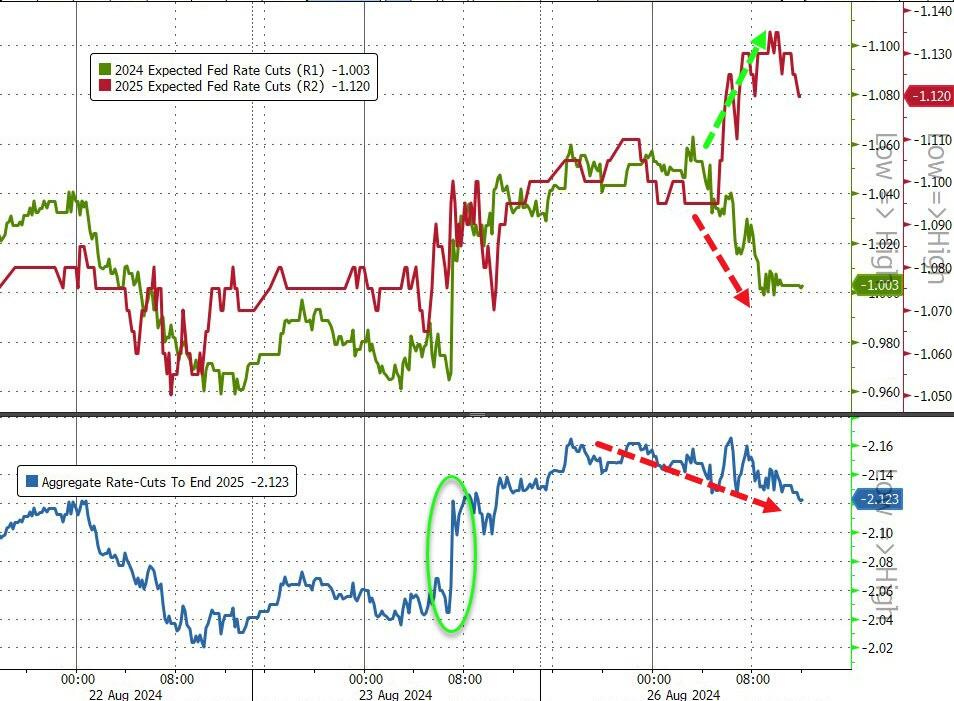

Amid the doldrums of summer liquidity, today saw some give back from Friday's euphoric response to Jay Powell's latest flip-flop.

Rate-cut expectations declined (most notably focused on a shift from 2024 to 2025)...

… Now not ALL ‘good news’ out there and despite / because how it is some of the time we can all debate whether good news is actually good or bad, I thought this visual was insightful …

… Since the summer of 2022, when CPI peaked, the 10Y yield and oil prices have been closely related. Treasury yields reflect the disinflation in CPI caused by the $40 decline in energy prices since the middle of 2022. On the other hand, oil prices have been declining due to lackluster demand.

The tight relationship between rates and oil has allowed markets to roam freely. Yields rising when energy prices rise is about good news; conversely, when each decline is about bad news (about the economy).

At the current low of the range, yields and oil have scope to rise in tandem, then good news = good news will dominate sentiment.

… hmm, that stinks was almost kind of enjoying lower / not rising gas prices at the pump … and oh, yea, funTERtaining the thought of aggressive rate cuts. Might there be a forced rethink? Said / visualized another way and WHY this matters, Yahoo …

Which suggests perhaps no institution would benefit more than the Fed from the auto industry's shift toward electric vehicles and away from internal combustion engines…

I suppose, as always, this one one(s) worth watchin’ and as for now, well … here is a snapshot OF USTs as of 648a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities gain, DXY flat & GBP bid whilst crude is on the backfoot … Bonds hold a bearish bias, with Bunds unreactive to the poor German GDP/GfK metrics … USTs are under modest pressure but very much towards the top-end of the bullish-move that has been in-play since early-July. Docket ahead is devoid of Fed speak but does feature a handful of data points and then 2yr supply. At a 113-14+ WTD low, support comes into play at Friday's 113-08+ and then Thursday's 113-05+ base.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: Aircraft lift durable goods orders in July

New durable goods orders jumped 9.9% m/m in July, as orders in the volatile nondefense aircraft category rebounded from an exceptionally weak June. This strength also carried through to shipments, implying stronger final goods spending and some feed-through to GDP growth.

Durable Goods Orders during July were mixed with the headline print at +9.9% MoM far outpacing expectations for a +5.0% gain. The June move was revised to -6.9% compared to the -6.7% initial print. However, orders of nondefense ex-aircrafts dropped -0.1% MoM vs. 0.0% forecast in July, while June was revised to 0.5% vs. 0.9% initial. Moreover, shipments of nondefense ex-air dropped more sharply at -0.4% MoM vs. +0.1% consensus and 0.0% prior. The driver of the headline strength was the volatile transportation series which gained +34.8% in July with Defense Aircraft orders +12.9%. On net, it was an update that didn't materially influence the macro narrative -- certainly not to the point of an impact on near-term policy expectations.

That said, the Treasury market cheapened in the long-end following the print and has stabilized within the prevailing range. Limited conviction as summertime trading conditions set it is the path of least resistance. From here, there isn't anything of note on the data calendar and we'll be watching the price action in risk assets for any incremental trading bias …

DB: Going short UST10Y (joining evil speculators detailed both HERE and HERE)

Late May, we outlined the rationale behind our bias to receive the US front-end. After the significant rally that occurred early August, we argued that such rationale was no longer valid. We now follow suit on the arguments presented earlier this month and enter a short UST10Y (indicative target 4.10%, indicative stop 3.65%).

Our trade is motivated by the following observations.

First, while the quit rate is consistent with the unemployment rate rising over time above 4.5%, jobless claims have remained stable or even declined in the last few weeks. Second, the Fed's dovish pivot, which culminated with Powell's Jackson Hole speech, is now well priced: the market is pricing one 50bp cut this year and the trough in Fed funds is close to 3%, which is arguably 25-50bp below plausible estimates of neutral. Third, term premia are at the bottom of the narrow range observed this year and remain too low relative to fundamentals. Finally, from a tactical perspective, the seasonal August rally, which often culminates with Jackson Hole, tends to reverse early September as supply resumes.

… Third, term premia are at the bottom of their (relatively narrow) year-to-date range and remain structurally too low relative to the underlying shift in supply/demand…

The most obvious risk to the trade would come from a very weak payroll next week justifying back-to-back 50bp rate cuts. Given the clear nod to rate cuts provided by Powell, this should be mostly reflected in the front-end. The scope for a UST10Y rally should be constrained by the fact that the curve is likely to steepen considerably given the low level of term premia.

UBS US economy: Rate cuts will help achieve a soft landing

We maintain our view that the US economy is headed for a soft landing, but risks are skewed to the downside.

Consumer spending will largely determine the fate of the economic recovery.

The Fed has made it clear that it is prepared to start cutting rates at the next FOMC meeting

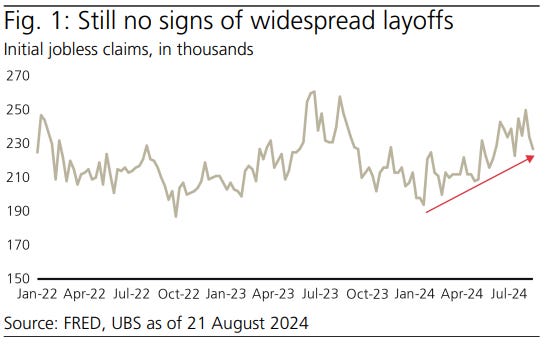

… As shown in Fig. 1, claims appear to be on a rising trend, but we could have said the same a year ago, and like the unemployment rate, the level of claims is still low from a historical perspective. The jury is still out, in our view, and we caution against overreacting to any one week’s worth of data.

Wells Fargo: Jump in July Durable Goods Orders Clouds Sluggish Underlying Demand

Summary New orders of durable goods surged 9.9% in July, coming on the heels of a 6.9% contraction the prior month. The month-to-month volatility has been driven primarily by aircraft. Excluding transportation goods, orders slipped 0.2% in July. Today's data confirm the ongoing trend that manufacturers are largely standing idle until looser policy comes to fruition and supports broad-based capital expenditures.

… (1) Middle East. Imagine a country where two rival governments fight over their central bank. Today's Bloomberg reported: "Libya's eastern government said it will shut down crude output and exports, as a struggle with its Tripoli-based rival for control of the central bank and the nation's oil riches threatens a new round of conflict." The country produced 1.15 million barrels a day last month.

Brent crude jumped as much as 3.2% to above $81 a barrel on the news that the eastern authorities issued a statement on Facebook that a "force majeure" applies to all fields, terminals and oil facilities (chart).

Contributing to the jump in the oil price was a preemptive strike by Israel against Hezbollah on Sunday. Around 100 Israeli jets hit dozens of Hezbollah launch sites in southern Lebanon, destroying thousands of rockets the military said were aimed at Israel.

… And from Global Wall Street inbox TO the WWW,

BESPOKE: The Sausage Indicator … (Dallas Fed survey HERE)

… The Dallas Fed's monthly regional manufacturing survey was released this morning, and within the report, the Fed publishes some of the notable comments made by survey respondents. One comment that caught our eye is highlighted below. "As the economy weakens, we are seeing modest growth in our category of dinner sausage. This category tends to grow when the economy weakens."

Sausage sales as an "off-track" economic indicator? We love these!

Bloomberg: Nvidia's Nnot Nnormal, never mind earnings (Authers’ OpED chart on what impacting ‘Earl)

Monopoly power has a price. The chipmaker’s weight in the S&P 500 will make for a twitchy end-of-summer earnings report.

… The weekend brought news of Israel’s preemptive strike against Hezbollah in Lebanon, and of retaliatory missile attacks. That aroused fears that that conflict could expand, and might come to involve Iran, Hezbollah’s chief supporter. That’s important because Iran might be able to close the Strait of Hormuz and choke global oil supplies. Acknowledging that risk, the price of crude ticked up about 0.5% as trading got underway in Asia. About 12 hours later, the eastern Libyan government that operates from Benghazi said that it was closing all oil production in areas under its control. That news seemed to blindside the market, and oil shot up:

This has its roots in a dispute over Libya’s cental bank. The internationally recognized government for western Libya wants to replace the governor, and this might make it harder for its rivals in Benghazi to maintain their flows of oil revenue.

FRED: Pensions versus stock market holdings of US households

Two of the largest financial assets for US households are pensions and direct holdings of stocks.

Pension funds, such as IRAs and 401(k)s, tend to be less liquid, as they generally have restrictions on converting the assets to cash. Of course, they often include tax benefits and contributions from employers.

More direct participation in the stock market (either through direct holdings of corporate equity or through mutual funds) provides more liquidity, since the assets are easier to sell and convert quickly to cash.

In the FRED graph above, the blue line shows US households’ pension entitlements (including IRA and 401(k) holdings) as a share of their net worth; the red line shows their holdings of stocks (corporate equity plus mutual fund shares) as a share of their net worth.*

In the 1950s and 1960s, stock holdings exceeded pensions.

In the 1970s, this relationship reversed and stock holdings remained consistently below pensions for most of the time.

In the 1990s, stock holdings began steadily increasing and have exceeded pensions since about 2018.

This trend may be related to the rise of mutual funds and the decline in trading commissions, which would lower the transaction costs in holding stocks. More recently, financial technology such as app-based electronic trading platforms and micro-investing have made it even easier for households to participate in the stock market, which likely has also been contributing to the rise of stock holdings over pensions as households’ preferred financial asset.

*The data also include the holdings of nonprofit organizations, but this is a small fraction relative to the household sector.

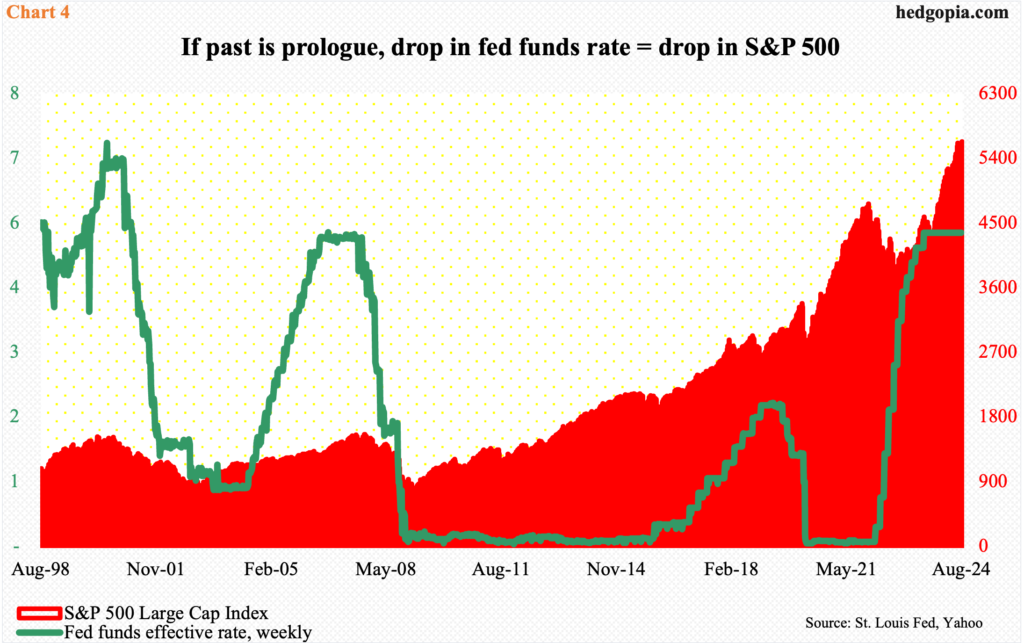

Hedgopia: Easing Cycle Set To Begin Next Month; Historically, Equities React By Declining

… As things stand, fed funds futures have priced in a 25-basis-point cut next month, slated for 17-18. And markets being markets, anytime there is macro data that suits – perceived or actual – their bias, they aggressively jack up easing expectations. These traders currently expect 100 basis points of cuts this year and another 100 basis points’ worth next year, ending 2025 between 300 basis points and 325 basis points (Chart 2)…

… Historically, the S&P 500 has shown a tendency to rally into the beginning of an easing cycle and then take a breather (Chart 4). This could very well be occurring in the tech land. The sector inherently leads when investor mood is decisively risk-on, which was the case until not too long ago. This is changing as investors seek the protection of defensives. This will only pick up speed in the months and quarters to come.

at JamieSaettele

10 yr note positioning (COT) is interesting. Despite the recent rally, the ownership profile is extremely bullish (similar to the 2018 fixed income low)

Peter Schiff: The "Good Ship Transitory" Sank, And Now The Captain Is Joking About It... (sorry but the visual … had me at hello)

It almost sounded like an apology. Almost...

WolfST: Manufacturing (beyond Boeing) Not Dead: Orders Rose to New Highs in 2024, after a Little Dip in 2023, after Pandemic Boom

And the order backlog has started rising again.

Finally, as this ‘research’ note comes to an end, I’ll let you decide which kind it is …

… AND quick schedule update … travelling tomorrow and so, regular spammation hopefully to resume on Thursday … IF you should require a refund, well, have your girl call my girl … THAT is all for now. Off to the day job…

My gurl ain't happy w/ur gurl LOL....guess I missed that 2 yr intraday dip to 3.6% while living in a shoebox 3wks ago....off to Tahoe overnight myself it's the last wk of free summer music, last night of Bluesday at Squaw Valley tonight, Bluesday ROCKS, Peace Out!

My gurl ain't happy w/ur gurl LOL....guess I missed that 2 yr intraday dip to 3.6% while living in a shoebox 3wks ago....off to Tahoe overnight myself it's the last wk of free summer music, last night of Bluesday at Squaw Valley tonight, Bluesday ROCKS, Peace Out!

The Consequences of the Biden/Harris Economics policies and the Gaslighting of the American Public

by the dishonest Corporate Media

https://www.zerohedge.com/personal-finance/if-everything-so-great-why-are-millions-americans-sleeping-their-vehicles