Good morning … as we enter the very last week of August and so, the unofficial last week of the summer, I’d expect many out of office replies with much of Global Wall extending time away from Bloomberg machines for last minute getaways, returning of kiddos to school, UK bank holiday today etc and so, I’ll be brief …

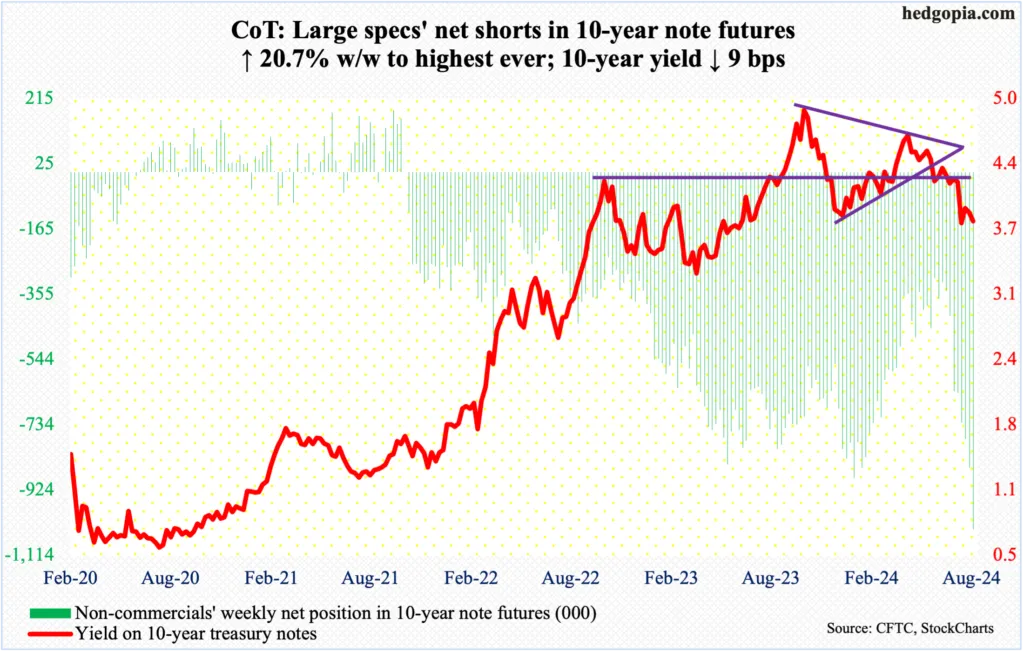

Over the weekend there were a couple of levels (2s, 10s) worth noting as ‘the time has come’ (see bottom of p3 of the speech for THE quote). Global Wall reacted (best in biz staying IN steepeners, others updating and minting NEW and improved Fed calls — adding OF rate cuts in Nov to their dance card) and it was ALSO noted some on the intertubes were buyin’ bonds (AGG) and how others (large speculators) have gotten record net SHORT (10yr futures) …

10yr futures (ZN1):

Resistance (double top) up near 115 and so I’ll be watching things like momentum (stochastics) and positioning upon approach of it …

… I may never have traded any futures (or options) but I have helped with related cash (basis) trades and had front row seat (paying Bloomberg fee as an add on for live feed from CBOT for years) and at the end of the day, not sure anything more to be gleaned from futures than cash, at this moment in time.

Speculators, on the other hand, are record net SHORT … and so I’d think a press up to / above levels noted would bring in short covering and we should be watching levels as well as positions over the next several weeks.

For NOW though, here is a snapshot OF USTs as of 645a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Geopols in focus with macro newsflow elsewhere light into a busy week … USTs are essentially flat with specifics light as the benchmarks has already reacted to Jackson Hole with attention now on upcoming inflation and jobs numbers. Holding at the low end of 113-22 to 113-30 parameters, support some way off at Friday's 113-08+ base.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in addition to what was offered over the weekend HERE)

MS: Sunday Start | What's Next in Global Macro: Party Conventional Wisdom

…So what can investors hang their hat on as we head into the final sprint to November 5?

The business cycle should influence markets more than the election ahead of the event. Our cross-asset strategy team’s study of the run-up to past elections shows no clear pattern of market behavior in election years, even when screening for different election and macro conditions. Further, polls and prediction markets continue to depict a very close race, and we’ve little reason to expect much change with a polarized electorate. Given these uncertainties, we don’t think investors’ near-term strategies will focus on the election.

In equity markets, we expect post-election impacts to be most pronounced in specific sectors. Differences in the parties’ approaches to the tax breaks set to expire at the end of 2025 are key here. Energy and telecom are among the sectors that could be relatively worse off under the most politically viable version of the Democrats’ plan for extending the tax breaks, but clean tech could do better as clean energy appropriations under the Inflation Reduction Act (IRA) would have more protection.

The US Treasury yield curve and the US dollar could also be affected by the election outcome. Underpinning our US rates strategy team’s call for a steeper yield curve driven by lower yields in shorter-maturity bonds is our economists’ long-standing view that inflation will ease enough for the Fed to cut rates this year. A Republican win that leads to higher tariffs and related growth pressures could boost curve steepening, though it’s not a requirement.

As for USD, investors shouldn’t assume that the dollar weakens if former President Trump wins. While he has called a strong US dollar "a disaster for our manufacturers and others," DXY rallied in the months after his 2016 victory, and our FX and economics teams think a repeat is likely if he wins again. Fresh tariffs would appear likely given Trump’s stated willingness to impose them, the president’s ability to execute them independent of Congress, and Trump’s track record of levying them in his first term. Tariffs could pressure economic growth, but possibly more so outside the US, potentially driving more dovish central bank policies overseas than at the Fed. Heightened geopolitical uncertainty from questions about the stability of US alliances could also increase safe-haven flows to the dollar. Conversely, if the Democrats hold on to the White House, USD may face headwinds. Less uncertainty about tariffs and trade policy generally could dampen safe-haven currency flows…

MS: The Weekly Worldview: Payrolls in the context of Migration

The immigration impulse has been a key part of our US outlook. Around the world, immigration affects economic growth through its effects on aggregate demand and labor supply.

The benchmark revisions to payrolls data released by the BLS last week suggest the trend of labor market growth last year was closer to 168k rather than 242k initially reported. While that pace is slower, it is not “slow.” The revisions also prompt renewed questions about US immigration. Implicit in the BLS revisions is part of the story for the US. The immigration boost to labor supply was part of our view on the disinflation last year and this. The lower level of payroll growth might question how durable the disinflation will be given the extra supply of labor appears to be less than we thought. We are not worried for a couple of reasons. First, the payrolls number shows the intersection of labor supply and demand, not just a fall in supply, so the softening in wage inflation and the realized disinflation leaves the basics of the story intact. Moreover, the BLS revisions likely revised the data down too much because the revision is based on administrative data from unemployment insurance files, which probably do not capture many of the increased jobs filled by undocumented workers. The fact that consumption growth remained strong also cautions against too pessimistic an interpretation of the revision. Ultimately, however, we retain our view that both growth and inflation will soften over the coming months, even with the data revisions…

… And from Global Wall Street inbox TO the WWW (also in addition to what was offered over the weekend HERE — note EPB Macro on the evils of corporations and being in it for profits :))

Bloomberg: Fed’s Preferred Price Gauge to Reinforce Rate Cuts: Eco Week (inflation trending lower but … consumption expected to climb and be ‘strongest in 4mos’ ??)

Euro-zone inflation to help ECB decide on September rate cut

The focus in Asia will be on China’s new monetary framework

… Economists see the personal consumption expenditures price index excluding food and energy — the Fed’s preferred measure of underlying inflation — rising 0.2% in July for a second month. That would pull the three-month annualized rate of so-called core inflation down to 2.1%, a smidgen above the central bank’s 2% goal.

Economists in the Bloomberg survey also expect consumer outlays, unadjusted for price changes, to climb 0.5% — the strongest advance in four months — in Friday’s report…

Fed chair says ‘time has come’ for easing in clearest signal

His remarks came before a flare-up of conflict in Middle East

Bloomberg: Milton Friedman's shower scene is back (Authers OpED)

As the Fed fiddles with the monetary taps, expect scalding and freezing while markets overshoot.

… At this point, the fed funds futures market — as gauged by Bloomberg’s trusty World Interest Rates Probabilities function — is pricing more than 100 basis points of cuts between now and the end of the year. In other words, it’s priced as a certainty that the Fed will have to cut by 50 basis points at least once in the three meetings left for 2024. In early July, the market was 100% certain that there would be at least one meeting when the Fed didn’t cut at all, as there would only be a total of 50 basis points in cuts by year-end. At the beginning of this month, a jumbo-cut was still rated as a zero chance. If the chart below reminds you of the fool in the scalding shower, you’d be right:

The critical question now is the speed of the cuts. Eric Robertsen of Standard Chartered PLC argues that there are two key questions:

How disappointed would markets be if the FOMC sticks to 25 basis-point moves at the first meetings? Or will hopes for a 50 basis-point cut simply be pushed out?

The US dollar has weakened in recent weeks as US rates have fallen. Implicit in the dollar’s decline is an expectation of a US soft landing. What if the US economic slowdown is worse than that? How does the dollar react?

InvestMacroCOT Bonds Charts: Speculator Bets led by Ultra Treasury Bonds & Ultra 10-Year Bonds

…10-Year Treasury Note Futures:

The 10-Year Treasury Note large speculator standing this week was a net position of -1,038,112 contracts in the data reported through Tuesday. This was a weekly decrease of -177,869 contracts from the previous week which had a total of -860,243 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 0.0 percent. The commercials are Bullish-Extreme with a score of 100.0 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 99.0 percent.

Reading the excellent article by Brian Meehan of Bloomberg Intelligence, “Basis Trade Growth Is Massive”, I was reminded just how stupid clearinghouses really are. If you ever meet a head of a clearinghouse, I can assure it was not brains that got them to this key position in global finance. As the article points out, their is now a USD 1.2 trillion notional short position in US treasury futures. You should not read this as the market being bearish on treasuries. It is a levered trade to make a “risk free” return on the difference in price between off the run treasuries and treasury future positions. For every short position in the treasury futures, there should be a long position in the physical market…

WolfST: The Rate Cuts Powell Dangled in Front of Markets May Slam into Inflationary Fiscal & Economic Policies of Whoever Is in the White House Next Year

For the Treasury market, Powell’s speech was a nothingburger. A Sep rate cut has been priced in since the Aug 2 jobs report.

… The six-month Treasury yield, which is an indicator of market expectations of Fed policy rates over the next several months, ticked down 4 basis points on Friday to 4.92%, back where it had been on Wednesday, but above the post-jobs-report plunge to 4.88% on August 2.

Note that the six-month yield falsely started pricing in rate cuts in early 2024 that didn’t come. In April-May, it rose again to the no-rate-cut scenario within its six-month window.

The one-year Treasury yield, which looks into the future through mid-2025 ended on Friday where it had been on Wednesday, at 4.36%, and up from the August 2 low of 4.33%. It’s beginning to price in four rate cuts in the early portion of its one-year window.

AND before hitting SEND just a note of upcoming schedule — I will be travelling on Wednesday and so there will be no regularly scheduled spammation, hopefully returning to overflow your inbox on Thursday. Thanks in advance for your patience and as far as the time having come, from an FX perspective …

{kind=link}