Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP — and I apologize ahead of time — ‘the time has come’ (see bottom of p3 of the speech for THE quote) and …

2yy WEEKLY: a good week and I’ll ask rather than state, has ‘the time come?’

I’ll continue wo watch 3.65% as a(nother) decisive sign it has in fact come and for now, I’ll note momentum once again approaching extremely overBOUGHT … Will there be any concession for this weeks 2s, 5s and 7s OR will folks take the signal from JHOLE and start gobbling up 2s in Tokyo and never look back … 3.65% next stop?

… Looking further out the curve

10yy DAILY: 3.77% will be on MY radar screen in the days / weeks ahead as what may be resistance NOW to become support …

… further supporting the longer-end of the curve in the week ahead will be front-end supply AND month-end (extension needs detailed below) AND AND … record spec net SHORT … fuel to the bond market fire …

ZH: "Powell Pivot Is Complete": Gold, Stocks, Bitcoin, & Bonds Surge As Fed Chair Powell Says "Time Has Come For Policy To Adjust"

ZH: Powell Vows To Cut Rates With Stocks, Home Prices, Rents And Food At All Time Highs

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW … Mostly all JHOLE all the time and so, as the saying goes, ‘‘the time has come’ …

BARCAP: Global Economics Weekly: Policy easing amid political uncertainty

Initial messages from Jackson Hole confirm that progress on disinflation has paved the way for the Fed to join the global easing cycle. Meanwhile, data suggest a gradual easing, in our view, and political uncertainty could still complicate the policy outlook. Next week, the focus turns to US PCE and European inflation.

…US Outlook Hang gliding from the Tetons Incoming data and Fed communications clearly signal that the FOMC is poised to initiate gradual cuts in September. This week's preliminary benchmark revision estimate suggests that job gains through March were not as robust as previously estimated, though these estimates likely overstate the eventual revision.

At Jackson Hole, Fed Chair Powell all but confirmed that the FOMC will initiate rate cuts in September, given his confidence that inflation is moving sustainably toward 2% and the "unmistakable" cooling in the labor market. The size and timing will be conditioned on data developments. We expect 25bp cuts, though unexpectedly weak labor market data, such as another 20bp jump in the unemployment rate, could shift the focus to more aggressive easing.

This week's preliminary benchmark announcement pointed to a downward revision to the monthly pace of payroll gains from April 2023 through March 2024 of nearly 70k/m, though revision patterns in the QCEW suggest that this downward revision will likely be substantially smaller. Moreover, we view July's 3mma payroll employment gain of 170k/m as accurate.

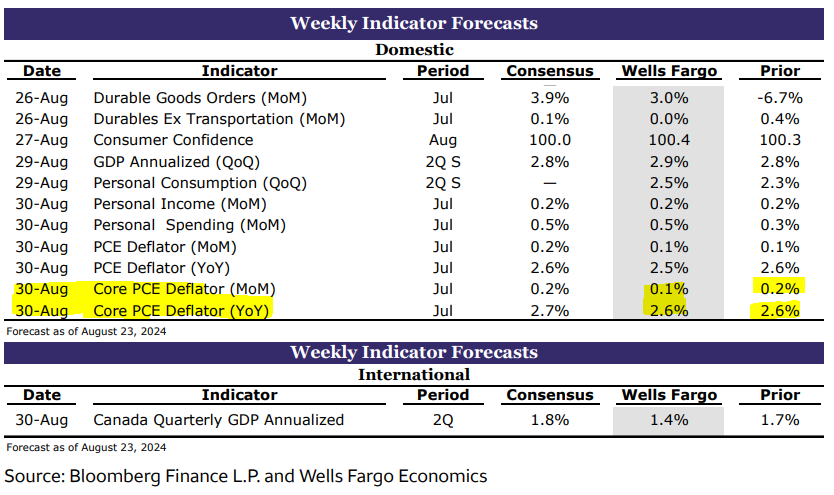

Next week's data will be highlighted by the BEA's second Q2 GDP estimate and July personal income. We expect GDP growth to remain close to the advance estimate of 2.9% q/q saar, and we think that PCE (+0.4% m/m) likely posted a faster increase than personal income (+0.2% m/m) amid July's hurricane disruptions. We estimate that core PCE prices rose 0.18% m/m (2.7% y/y).

BMO: Labor Data Dependent (stay in 2s10s steepener and with increased confidence now…)

In the week ahead, the Treasury market will continue to digest Powell’s observation that "We do not seek or welcome further cooling in labor market conditions,” and anything else that emerges from Jackson Hole over the weekend. The dovish tone was reinforced and as we look at the limited data offerings ahead, we anticipate that a range-trading theme will emerge as the process of enjoying the final days of summer overshadows the few data releases of note. In this context, there are two releases that could result in more durable price action. The first is Thursday’s release of initial jobless claims. While the recent 232k print matched expectations and was interpreted by the market as good-enough, the series has settled into higher lows. The upcoming claims print won’t be influential for nonfarm payrolls forecasts, but it will contribute to the debate as to whether the employment market has stabilized or is poised for another leg lower. Summer trading conditions could contribute to an outsized response in US rates, a dynamic that has become all too familiar as we’ve recently watched the market trading on both sides of 4.0% across the curve.

The second potential market-mover on the data-front comes in the form of Friday’s inflation update…

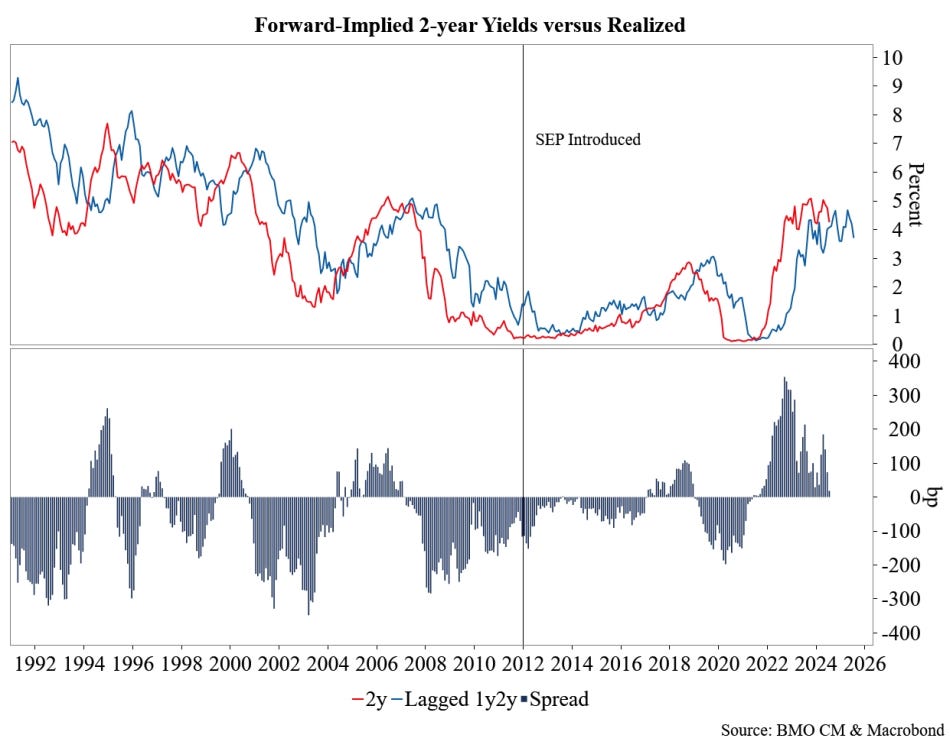

…Strategic Bias …With Jackson Hole behind us, we'll offer the observation that the next few months will be the moment in which market emphasis will appropriately been focused on the front end of the curve. The included chart illustrates the relationship between forward implied 2-year yields and the realized rates. During the period between 1991 and 2012 when the Fed started publishing the beloved dotplot, there was a strong tendency for the forwards to overestimates where 2-year yields would ultimately trade. To some extent, this resonates given that this period was generally characterized by falling rates and increased transparency on the part of monetary policymakers.

BNP: US: New Fed call after Jackson Hole as further cooling “not welcome”

KEY MESSAGES

Fed Chair Powell displayed even more sensitivity to the labor market side of the mandate than we expected at Jackson Hole.

In turn, we are adding a 25bp rate cut in November to our base case (we now expect the Fed to cut 25bp in September, November, and December). The path beyond is under review.

We read Powell as setting a low bar to a 50bp cut in September or thereafter. As a result, we see 75bp of cuts through year-end as a minimum.

Our read of recent Fedspeak is that finding a consensus for a larger than 25bp cut in September will require a clearly poor August jobs report.

In the attached Weekly we discuss Fed Chair Powell’s speech at the Kansas City Fed’s annual economic symposium in Jackson Hole. We also provide some thoughts on the preliminary estimate of the benchmark revision to nonfarm payrolls that was published this week.

… What was unsaid: A strategy for lowering rates Something of an ex-post strategy for hiking rates emerged in late 2022, which was compared to a flight on an airplane. Phase I was taking off with the engines at maximum thrust to gain altitude (or the how fast phase), which anyone who has flown out of John Wayne Airport would be familiar with. Phase II was throttling back to find the cruising altitude (the how high phase). Phase III was settling back and flying at the cruising altitude (the how long phase). What the Fed has not addressed in any clear way is the descent into the destination airport of price stability. We offered an outline for such a strategy on October 18, 2023 in a note titled Towards a Theory of Monetary Policy—Reflections About 2022-23. In that note we wrote “there is a fourth and a fifth phase of the monetary policy adjustment and those are the descent of rates to neutral as the economy approaches 2% inflation and then the final approach for landing, which is finding the rate setting to keep inflation at 2%.” At the end of his speech Powell said, “there remains much to be learned from this extraordinary period” and he added “we will be open to criticism and new ideas, while preserving the strengths of our framework” as the Fed enters a new fiveyear framework review. As a first salvo in our contribution to that process, we summarize our suggestions from our October 2023 note for policy adjustments as inflation approaches the target rate…

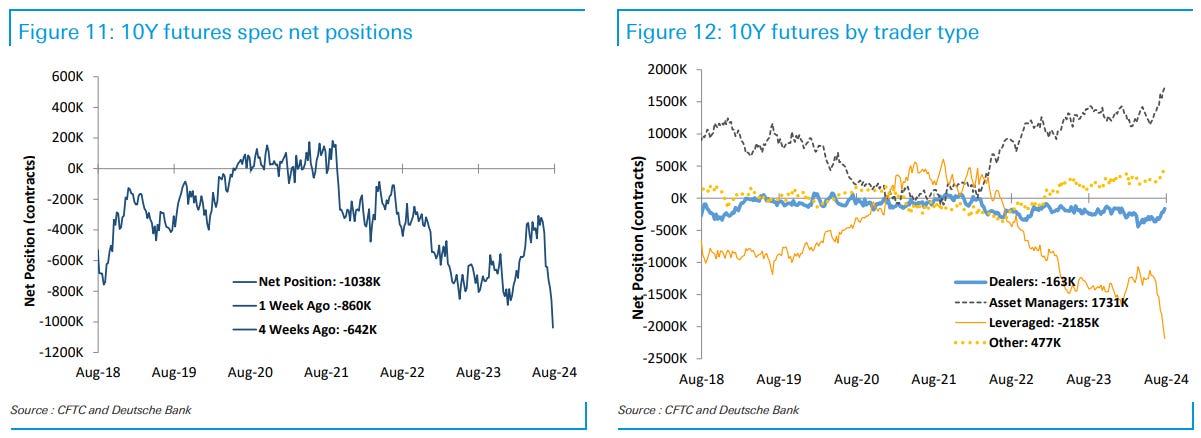

Interest Rates: Speculators were bearish in Treasury futures, extending their net short positions by 172K contracts in TY equivalents over the week prior to August 20 (Tuesday).

Asset managers lowered their net long positions in Treasury futures by 69K contracts in TY equivalents, while leveraged investors added 148K contracts to their net short positions in TY equivalents. All Treasury future contracts except for TY saw reduced asset manager long positions, while leveraged investors extended their net shorts in all Treasury future contracts except for FV, UXY and WN. Dealers removed 212K contracts in TY equivalents from their net short positions.

Speculators continued to sell contracts in FV and TY, with net short positions in both contracts reaching new highs.

Fed funds futures: Speculators sold 45K contracts, boosting their net short positions to 137K contracts.

SOFR futures: Speculators sold 18K 1M SOFR contracts, leading to a net position of -2K contracts. They sold 63K 3M SOFR contracts, lowering their net long positions to 382K contracts.

A September interest rate cut is coming with Fed Chair Powell telling us that "the time has come for policy to adjust. The direction of travel is clear." The market favours it being a 25bp move, but the 6 September jobs report will determine what happens. They don't want further weakness so another rise in unemployment to 4.4% or 4.5% could trigger a 50bp move

MS: August Index Extensions (month end coming Friday and could cap the week off with buying / selling <please choose one>)

…United States We expect the 1y+ UST index to extend by ~0.056y, compared to an average August (0.099y) and an average month (0.075y) – Exhibit 8 . A total of about US$324 billion of supply (offered amount) will affect the extension, and US$282 billion market value of bonds will fall out of the index. The monthly issuance of 2y, 3y, 5y, 7y, 10y, 20y, and 30y will affect the respective maturity-wise indices.

Trahan: Interesting Charts To Ponder For The Last Weeks Of Summer

…How bad could it get for housing? That’s a million dollar question. The chart below gives us a good sense of just how stretched affordability metrics are, and the University of Michigan survey of consumer confidence shows that housing sentiment is near historic lows. That’s a lot of potential gravity for this early cycle industry. At the end of the day, a lot of this will depend on just how high and sustained the rise in the unemployment rate is. Thus far, the unemployment rate seems to be following its traditional relationship with past policy trends, which argues that the trend is higher into 2026 and possibly beyond. That would give housing a lot of time to correct to more acceptable levels.

In a widely anticipated speech in Jackson Hole, Wyo., today, the Fed Chair signaled that the FOMC will be cutting rates at its next meeting on Sept. 18. The question is 25 bps or 50 bps?

… In short, the FOMC will cut rates on September 18. The question is by how much? We currently look for a 50 bps rate cut on September 18, but we readily acknowledge that the size of the cut (25 bps or 50 bps) will depend crucially on economic data between now and September 18. In that regard, Powell noted in today's speech that "the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks." In our view, the most important data release between now and the next FOMC meeting will be the August labor market report, which is slated for release on September 6. If the report shows continued weakening in the labor market in August, then a 50 bps rate cut will likely be in play. On the other hand, signs that the labor market has remained solid likely would lead the FOMC to opt for only 25 bps.

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AllStarCharts: Who’s Buying Bonds With Me? (written asked and sent before THE speech)

For the first time in my career, I’m buying bonds…

…Here’s the US Aggregate Bond ETF $AGG:

This fund holds treasury securities, corporate bonds, mortgage-backed securities, and municipal bonds. It is exactly what it sounds like. A diversified bond fund. It also offers investors a 3.4% yield.

The US Aggregate Bond ETF is pressing against the upper bounds of a multi-year accumulation pattern. With the 200-day moving average curling higher, we expect this base to resolve in the near future.

We’re buying AGG on strength above 101, with a target of 109 and 119.75…

EPB Macro: All Eyes On Profit Margins (Chart of the Week)

The dynamics in corporate profits and corporate profit margins have become one of the most critical variables to watch in the progression of the Business Cycle.

At EPB Research, we look at corporate profits from the National Income and Product Accounts rather than company earning statements.

Pre-tax corporate profit margins for the entire economy sit at nearly 12%, down a touch from the cycle peak but still at very elevated levels compared to the last few Business Cycles.

Elevated profit margins have been a key factor in allowing businesses to retain labor and delay layoffs despite objectively slowing business conditions.

More margin degradation is needed before companies make the final, most costly, and most binding decision to make large-scale layoffs.

Rather than corporate profit margins, we can also examine real or inflation-adjusted corporate profits, which show virtually the same picture…

HedgopiaCoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (spec net short is the HIGHEST EVER…)

Following futures positions of non-commercials are as of August 20, 2024.

10-year note: Currently net short 1.04mn, up 177.9k.

NORDEA: Macro & Markets: Wall Street, We Have an Expectation Problem (written before THE speech)

The combination of stocks reflecting an economy that will stay strong and bonds reflecting an economy with falling inflation and slowing economic activity will likely create a bearish environment which will be bullish for the safe haven US dollar.

…Chart 1. Inflation versus labor

…Storm clouds are gathering over the financial market. The combination of the stock market reflecting an economy that will stay strong in the coming years and the bond market reflecting an economy with falling inflation and slowing economic activity will likely create a bearish environment in the coming quarters. The expectation of the best economic outcomes in each asset class has raised the bar for positive surprises going forward and the fact that the two asset classes reflect different economic outcomes also present a big challenge. Falling interest rates have helped lift stocks back towards historically high levels, but after a 100 basis point bond rally over the summer it is hard to imagine that interest rates can fall much more on a sustained basis unless it is due to economic deterioration, which would be bad news for stocks that reflect a strong economy. It is also hard to imagine that stock prices which are close to historically high levels and already reflect a strong economy could rise much more on a sustained basis, unless it is due to economic reacceleration from an already strong starting point, which would be bad news for bonds which reflect falling inflation and slowing economic activity.

Chart 3. Stocks versus bonds

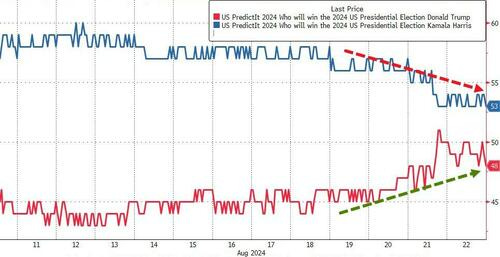

ZH: Protests, Pandering, Past-Presidents, But No Policies: Summing Up The 2024 DNC In 2 Words - 'Not Trump' (seems ‘bout right … and NOW heavy lifting from both sides begins in earnest)

Objectively, if prediction sites can be trusted in any way (perhaps more so than biased polls), the last four days of speeches, musical performances, and delegate celebrations were a 'failure' of sorts for the Democratic Party as during the DNC, Kamala Harris odds of success in November dropped while Trump's improved (though we note the incumbent VP remains a favorite)...

Source: Bloomberg

ZH: Money-Market Funds & Bank Deposits See Huge Inflows As Stocks Rebounded

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Excellent !!!