Good morning and happy Boston Tea Party-A-versary !! … As we begin the final full trading week of 2024 (this will be my last regular week of communication until 2025), the markets are subdued and uninspired, which is understandable. Global Wall Street bonuses have been secured, and there's little motivation to take significant risks and jeopardize them. Consequently, most on Global Wall will likely leave trading to bots and amateurs in the coming days. This doesn't mean that extremes won't be addressed, but a quiet start to the week with magazine cover indicator and a well-telegraphed December rate cut is not unexpected.

And while, yes, it is true …

CNBC: Bitcoin rises to new record above $106,000 ahead of this week’s Fed decision

… I’m choosing to have an early look at the front-end of the yield curve as it appears ‘support’ (mentioned HERE over the weekend) is holding and so …

2yy: freshly redrawn TLINE (support) up nearer 4.25% into a rate CUT (think FF soft cap with eff fed funds band of 4.50 - 4.75 and coming down) …

… TLINE support coming in just above 4.25% and in these final few trading days of the year, history shown time and time again, anything can / will happen …

As such, I’m reminded of Sgt Phil Esterhaus of Hill Street Blues who reminded us …

AND … with that little said and in mind, here is a snapshot OF USTs as of 618a:

… and for some MORE of the news you might be able to use … INCLUDING A (relatively) NEW LINK … “Yield Hunting”, linked just below and it’s alongside other ‘news you can use’ as I can attest, after decades on Global Wall where I’ve learned how it is that desks sell their books (buyer beware) and ‘broker’ (ie non-risk biz) lots of things, IDEAS are always and forever, the most valuable of commods. This site “Yield Hunting” most def worth a point / click and with that in mind… some resources and curated links for your dining and dancing pleasure …

NEWSQUAWK: US Market Open: Tepid risk tone weighs on European indices, DXY flat ahead of US PMIs … EGBs softer with OATs underperforming slightly post-Moody's downgrade, PMIs in focus … USTs are rangebound in a tight 109-27+ to 109-31+ band ahead of Flash PMIs from the US but with the focus firmly on Wednesday’s FOMC. Given contained action for the benchmark yields are also relatively steady but are lower across the curve, which itself is marginally flatter.

Opening Bell Daily: Bitcoin enters QQQ … Investor all over the world are about to gain bitcoin exposure … The Nasdaq announced MicroStrategy will join one of the most heavily-traded indexes.

AlpineMacro: MACRO OUTLOOK 2025 Boom Or Bust? An Investor’s Playbook For 2025 & Beyond

Executive Summary Three big stories are likely to dominate the world economy and markets for 2025 and beyond:

The U.S. adopts supply-side policies

Increasing backlash against fiscal conservatism

The escalating battle between protectionism and globalism

… Treasury bonds will be constrained within a range, with 10-year Treasury yields fluctuating between 4% and 4.5% as the Federal Reserve recalibrates its policy. The central bank could drop rates to 4%, but likely not much lower before switching to a holding pattern …

… U.S. Fixed Income: A Higher R* … , the steady-state interest rate, or the so-called R*, has risen. Several factors contribute to the higher R* since the pandemic crisis …

… Regardless, there is limited upside potential for long-term bonds. We view current bond yields at 4.15% as very close to equilibrium.

If the Fed cuts rates to 4%, long bond yields should settle around 4.2-4.3%, with term premiums ranging between 20-30 basis points on top of short rates. If bond yields rise toward 5%, investors should add duration above the benchmark. Similarly, if yields fall toward 4% or lower, investors should reduce duration ...

AlpineMacro: U.S. Bond Strategy For 2025 (Part II)

Base Case macro and policy outlook is constructive for risk assets in 2025...

...but valuation is stretched and investor sentiment is frothy.

Rising risk of correction in risky spreads in first half of 2025.

Downgrade Corporate bonds to slightly underweight, equal with Treasurys.

Upgrade Agency MBS to max overweight.

Keep duration short in spread product and long in Treasurys.

… AND turning away from USofA with attention TOWARDS China, given (Nov)data out over weekend …

China's November activity data broadly painted a picture of weakened domestic demand, with visible moderation in retail sales growth and softer fixed asset investment. We maintain our below-consensus 2025 GDP growth forecast of 4.0%, with downside risks to consumption and housing.

… from China, a move back to a look at Fed from a Germain shop and fan favorite stratEgerist and his morning call / thoughts …

…Let’s expand on some of these highlights now and start with the Fed. Our economists’ preview is here but in brief they expect a 25bps cut and then for them to be on hold for the entirety of 2025 as the SEP should show meaningful revisions to the 2024 economic forecasts, with growth and inflation revised higher and the unemployment rate lower. The median dot is likely to show three additional rate cuts but we think Powell will likely deemphasis this signal in the press conference and be as data dependant as he can be. Powell will also likely emphasise that it is still too early for officials to build any major policy changes from the new Trump administration into their outlook. The long-run dot will likely continue its upward migration, rising to 3.1%. Our economists' estimates of neutral are notably above the Fed’s and we think they will likely continue to move this higher…

… more ‘bout China data over weekend …

ING: China's November data showed mixed signals as 2024 winds down

Encouraging property price developments for a second straight month, but key activity data came in a little softer than expected in November

… Jamie Dimon’s operations SAY … hold on to 10s30s steepeners …

…Governments OIS forwards appear too hawkish and intermediate Treasuries too cheap, but we stay tactically neutral on duration, given Powell may strike a more neutral tone and as liquidity remains poor. Maintain 10s/30s steepeners as a low-beta expression of our medium-term bullish view and ahead of 20-year supply. We review demand trends during 3Q24. Hold 5-year breakeven wideners on a hedged basis and 10Yx20Y inflation swap longs.

…Treasuries Maintain 10s/30s steepeners

Treasury yields are back near the upper end of the range they’ve held since the election and the curve has steepened due to mean reversion, global factors, and Treasury supply

We look for the Fed to deliver another 25bp ease next week, but this is largely priced in. We expect the 2025 median dot to show three cuts and a neutral tone from Chair Powell after having eased policy by 100bp since the summer

While OIS forwards appear too hawkish and intermediate Treasuries appear too cheap, we stay neutral on duration for now: our expectations for next week’s meeting suggest the Fed path is unlikely to reprice dovishly, there’s no first-tier inflation or labor market data before the new year, and liquidity should remain seasonally depressed, which could result in weak auction results

The long end is now fairly valued, but we recommend maintaining 10s/30s curve steepeners as a low-beta duration trade that is aligned with our medium-term bullish view and as next week’s long-end supply could support some further steepening in an environment of weak liquidity

… Turning to the curve, we’ve been recommending 10s/30s steepeners for almost one month as we think the long end should steepen even in a more gradual easing cycle, and we recommend maintaining 10s/30s steepeners for a couple of reasons. First, we continue to see long-end steepeners as a low beta long duration trade, and this exposure is consistent with our medium-term bullish view. Moreover, curve steepeners should benefit from structurally rising term premium, as we discussed in our Outlook. Second, Treasury will auction $13bn reopened 20-year bonds next Tuesday, and this will likely require a further concession in this weakened liquidity environment, supporting further long-end steepening. On the other hand, we acknowledge the valuation backdrop is no longer supportive of steeper curves— as Figure 18Foreign vstorped histronge quartof buyingsce 201in3Q4 shows, the 10s/30s curve now appears fairly valued after controlling for medium-term Fed policy and inflation expectations, as well as the size of the Fed’s balance sheet—in contrast to European government bond markets, where the 10s/30s curve remains excessively flat (see Steady ECB easing, tactically take profit on duration longs, Francis Diamond, 12/12/24). Nonetheless, while the valuation argument is less compelling in US markets on this basis, we maintain 10s/30s curve steepeners in the current environment as a low-beta expression of our medium-term bullish view, for all the reasons discussed.

The Fed’s Z.1 report indicates $512bn of Treasuries were purchased in 3Q24, with foreign investors representing the largest source of demand. The price-insensitive share of the Treasury market, which represents the Fed, commercial banks, and foreign investors, increased only slightly to 51% last quarter

… As always, there are more questions than answers and taking a holistic look at and identifying QUESTIONS clients are gonna ask, seems like a great approach. That IS, by definition, almost, what Global Wall DOES … answer questions investors (aka the buy side) didn’t ask and create new and different ways / products to help one shop outperform it’s peers, outright OR on a relative-to-benchmark perspective. This next note touches on a view of the BIG questions …

MS: Sunday Start | What's Next in Global Macro: Asking the Big Questions

A core element of the research process is asking the right question at the right time. Each December, senior Morgan Stanley analysts from around the world gather to discuss the biggest questions their industries face and the debates that will shape returns in the years ahead. Looking back on our gathering this past week, here are five investment questions our teams will zero in on next year.

Could AI focus shift from infrastructure to agents and embodied AI? …

How do we allocate the energy we have and increase supply? …

What do protectionist policies mean for the United States? …

What do longer lifespans mean for society? …

How will lower rates impact markets? We expect lower interest rates to have a wide range of impacts across the market. As rates decline, there is an intense debate on whether the high balances in money market funds will get reallocated towards higher return assets, and the sequencing of such a reallocation. We expect significant differences between institutional and retail investors in this context. We expect a material rebound in M&A next year. With year-to-date announcements up 25% versus 2023, cyclical and structural factors support an even larger 50%Y increase in 2025, driven by the return of sponsors and large-cap deals. Lower rates also provide support for increased M&A activity. We believe that the rates environment, and by extension the financing markets, will play a crucial role in enabling the transformation under way in both AI and energy markets.

We see more balanced EPS growth in 2025 for the S&P 500. This should lead to better breadth, something that has been absent over the last 2 years. We expect this broadening to be more prevalent in large cap quality as we're entering a late cycle extension as opposed to a new cycle.

… As We Head into Next Year, Here Are 3 Key Considerations:

A mix of mid-single-digit revenue growth (based on our economists' nominal GDP growth estimates) and margin expansion should lead to double-digit EPS growth in 2025 and 2026 for the S&P 500.

Assuming rates fall (in line with our rate strategists' 2025 forecast) in the context of a healthy EPS growth backdrop, it is unlikely the market multiple will compress much. As such, we are forecasting only a modest decline in forward P/E to 21.5x from 22.1x today.

Stick with a barbell of quality cyclicals and quality growth unless growth concerns return; Financials, Software, and Industrials remain our top sector/industry picks as we head into the new year.

…Is Better Breadth on the Horizon? The cadence of earnings growth offers insightful perspective on where we are in the business cycle. As Exhibit 1 shows, S&P 500 EPS growth tends to either make a durable trough at ~0% or at -15-25% (small caps tend to form troughs/peaks of greater magnitude). The key differentiating factor that determines the outcome is whether a labor cycle hits the economy (dotted circles in Exhibit 1) or not (solid circles). The inflection in growth we are currently seeing is off the zero bound and wasn't preceded by an unemployment cycle. Thus, it represents an extension of the current cycle (i.e., a soft landing and subsequent growth acceleration), in our view. It's also worth pointing out that we believe this is a late cycle extension given the tightness in the labor market. These late cycle earnings growth reaccelerations are typically driven by some feature unique to that particular cycle. In the late 1990s it was the excess spending on tech equipment that ultimately rolled over before a wider broadening out could arrive…

…Turning to the bond market, rates pushed higher last week with the 10-year Treasury yield reaching 4.40% on Friday. It's now just ~10bps below the level it reached shortly after the election. While Wednesday's in-line CPI report solidified the bond market's expectation for a cut in December (the market is now pricing in a 97% probability), market participants are increasingly uncertain about the Fed path in 2025. As our economists discussed last week, "We think the Fed will retain optimism about inflation remaining in a downward trend and, in turn, reinforce its guidance that the funds rate is likely to move lower over time. That said, Chair Powell noted that the economic activity and labor markets appear stronger than the committee thought in September, and inflation in prior months had shown signs of unexpected firmness. As a result, he is likely to say that the Fed will proceed with more caution on rate cuts going forward." It appears this dynamic is influencing expectations for the rate cutting path in 2025 as the cumulative number of cuts priced into the bond market through the end of next year went from 3.6 on 12/6 to 2.9 on 12/13. Despite this move in the rates market, equities held up relatively well all things considered, closing the week about flat although breadth deteriorated further on the week. We think this confirms the dynamic we talked about last week—high quality equities can tolerate moderately higher rates for now as long as they come with solid macro growth data and are not the result of hotter inflation that leads to a more hawkish Fed or a higher term premium as bond market participants push back…

… and as we near the end of the year, a look (at stonks) ahead …

UBS: More to go in stocks Chief Investment Office GWM

Why? We rate US equities as Attractive due to robust growth, lower Fed rates ahead, and AI exposure. The Asia ex-Japan region is also favored for firm local growth and youthful demographics. China and Europe face tariffs threats, but we like smaller Eurozone companies for their wide discounts. Swiss dividend stocks offer quality exposure and better income prospects than local bonds.

Why now? 1) In the past, when the Fed cut rates and the US avoided recession, US equities rose 18% on average in the following year. 2) Asia ex-Japan is expected to have an appealing earnings growth profile, with 13% growth forecast in USD for 2025. 3) Eurozone small- and mid-caps' P/E ratios are trading near two-decade lows compared to large caps.

… and the same shop offering insights on demand (and China) …

China’s November retail sales disappointed. Some of this can be blamed on the timing of the singles shopping festival. The pattern of sales showed consumers spending in areas with government support, but in doing so cut back on areas without government support. This demand switching in an overall subdued demand environment has parallels to Japan’s “spending voucher” initiatives in the 1990s. The data keeps up pressure for fiscal policy to tackle consumers’ apprehensions about the future…

…Assorted business sentiment polls are due out. With the rise of social media, sensationalism, and political polarization, a skeptical filter of “they would say that, wouldn’t they?” should probably be applied to these numbers. A sense of general disquiet may be reported as individual catastrophe, even if individual circumstances are fine.

The Federal Reserve is in speaker blackout ahead of this week’s policy decision—but European central bankers (fearlessly led by ECB President Lagarde) are rushing to fill the void. Markets are not likely to care to much what ECB speakers say.

… finally, from Dr. Bond Vigilante, an economic calendar for the week ahead …

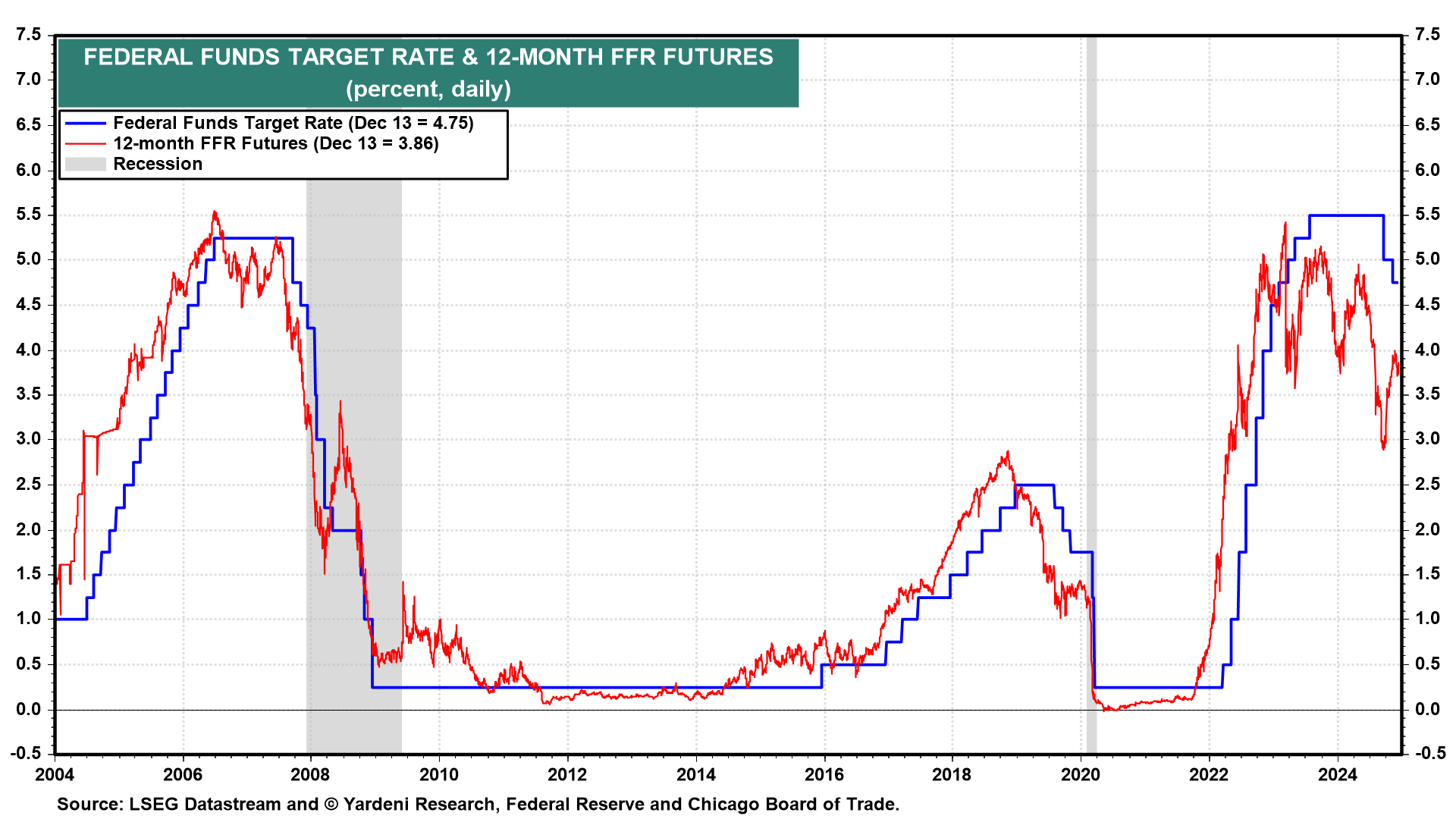

The main focus of the economic week ahead is the FOMC's interest-rate decision on Wednesday. The most likely outcome will be a 25bps cut of the federal funds rate (FFR) to a target range of 4.25% -4.50%. After a full 100bps of cuts since September 18, we expect Fed Chair Jerome Powell will use his press conference after the FOMC meets to signal that the Fed is on pause from further easing for now. The FOMC's updated quarterly Summary of Economic Projections will likely support the case for a pause by showing expectations for stronger growth and higher inflation over the next two years.

Our guess is that a few FOMC participants likely agree with us that the FFR doesn't need to be cut any further for now. However, the FOMC may be handcuffed by the near 100% odds of a rate cut expected by the FFR futures market (chart).

The reason for not cutting the FFR again early next year is not just because growth and inflation remain strong, but they might both get hotter. This week's regional manufacturing surveys may show that even the weak patches of the economy are getting stronger thanks to rate cuts, fiscal spending, and Trump 2.0…

Will we see a repeat of the 1970s with the Fed easing policy too quickly, triggering a rise in inflation in 2025?

Recent inflation readings show signs that the decline in inflation has stalled, and there is a risk of reacceleration, see charts below. Fed and market-implied measures of inflation are all above the Fed’s 2% target and not showing signs of moving down toward the Fed’s 2% inflation target. Short-run and long-run inflation expectations are also moving higher.

The recent uptrend, combined with strong economic momentum, is pointing towards a rebound in inflation in 2025 and not a softening to justify Fed cuts. The probability is rising that the Fed may have to raise interest rates in 2025.

For investors, the risk is a repeat of 2022, where the 60/40 portfolio underperformed significantly.

Our chartbook with recent measures of inflation is available here.

Wall Street’s market forecasts are too tepid. The S&P 500 could rally next year on a combination of AI growth and deregulation. But investors should prepare for a wilder ride.

… SAME outlet and a related story (?) …

BARRONS: Inflation, Trump, and More: What’s Ahead for the Economy in 2025

The U.S. economy is ending 2024 on a high note, and things look promising for 2025. Real gross domestic product is on pace to expand by 2.7% this year, bolstered by consumer spending and productivity growth, and economists have penciled in gains in the mid-2% range for next year. Talk of recession, so rampant a year ago, is just about nil, and frothy financial markets aren’t pricing in any hint of a slowdown…

… The Fed also will conduct a review of its monetary-policy strategy, tools, and communications in 2025, five years after its last so-called framework review. The central bank will host a research conference in May in Washington, D.C., to bring in outside perspectives on monetary policy and the economy. Conclusions from the review may be presented at the Kansas City Fed’s Economic Policy Symposium in Jackson Hole, Wyo., in August.

Powell’s legacy is bound up with the economy’s performance, specifically with the Fed’s ability to tame inflation without a recession. If the good times keep rolling through ’25, as expected, he may depart a hero. So far, so good, but the job isn’t done yet.

AND … Bloomberg, a couple interesting / funTERtaining headlines / story / reads …

Bloomberg: The 24 Hours of Rate Cuts That End Year of Global Central-Bank Easing

Likely Fed rate cut takes center stage in flurry of decisions

Chinese data, UK inflation, euro-zone sentiment gauges due

Bloomberg (OpED): The Fed Faces an Important Choice After This Rate Cut Opinion |Mohamed A. El-Erian , Columnist Emerging economic realities should force the central bank to rethink its policy approach.

… To navigate well what I think may be an inevitable decision point, the Fed will have to change how it formulates policy. It will need to move from what is currently an excessive dependence on historical data to incorporating more of a strategic forward-looking approach. Where it ends up in its choice will have significant implications for growth, as well as market valuations and volatility — in America and well beyond.

… With rate CUTS in mind, a story in the FT struck me as funTERtaining …

FT: Economists trim Fed rate cut estimates on fear of Trump inflation surge

Deregulation, tax cuts and tariffs stoke probability of stubbornly high price growth, FT-Chicago Booth poll finds

… Just over 80 per cent of the 47 economists polled said that inflation over the next year, as measured by the personal expenditures price index once food and energy prices are stripped out, would not dip below 2 per cent until January 2026 or later. In September, only about 35 per cent of polled respondents made the same estimate …

… AND in as far as it relates TO best in biz (BMO 2025 outlook noted HERE), whereby FedFunds may act as a ‘soft CAP’ on yields … this next one offers further visual context ….

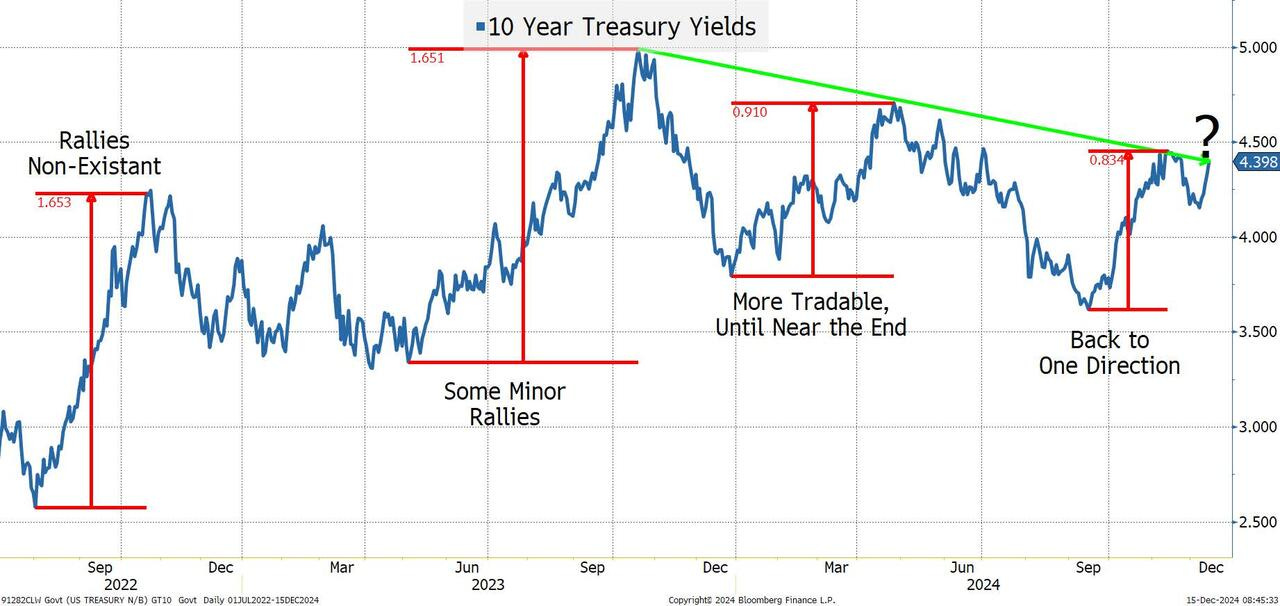

WolfST: Treasury Yield Curve Un-Inverts Further on Surging Longer-Term Yields: 10-Year Yield Now Higher than All Shorter Yields. Mortgage Rates Resurge

Fed cut by 75 basis points since September while 10-year Treasury yield rose by 75 basis points to 4.40%, as Bond Market frets about Inflation & Supply.

The 10-year Treasury yield jumped by 7 basis points on Friday, to 4.40%, having risen five trading days in a row. It’s now just 4 basis points below the post-rate-cut closing high on November 13 (4.44%). These yields are the highest since June.

Since the eve of the Fed’s September 18 rate cut, the 10-year yield has risen by 75 basis points, while the Fed has cut by 75 basis points. The difference is 150 basis points! The 10-year yield is now higher than all shorter-term yields.

… in as far as Rosie’s Lament of a Bear (listen to latest MacroVoices HERE) and the lack of buyers readily available if / when stocks sell off goes …

WolfST: Money Market Funds, Large CDs, Small CDs, and Total Deposits: Americans’ Huge Piles of Interest-Earning Cash as Rates Drop

Household cash in money market funds jumps to a record but CD balances begin to decline.

…These MMF balances include retail MMFs that households buy directly from their broker or bank, and institutional MMFs that households hold indirectly through their employers, trustees, and fiduciaries who buy those funds on behalf of their clients, employees, or owners.

MMFs are mutual funds that invest in relatively safe short-term instruments, such as Treasury bills, high-grade commercial paper, high-grade asset-backed commercial paper, repos in the repo market, and repos with the Fed – the Fed’s “Overnight Reverse Repos” (ON RRPs).

Total MMFs (held by households and institutions) jumped by $291 billion in the quarter to $6.84 trillion at the end of Q3, having ballooned by 53% since Q1 2022 when the rate hikes started from near 0%, and having more than doubled since 2018, when the prior rate-hike cycle took the Fed’s policy rates to 2.25%.

But even after the Fed started cutting rates in 2019 and slashed rates to near 0% in Q1 2020, cash continued to pour into MMFs. It wasn’t until Q3 2020, that relatively small amounts of cash left MMFs, and then balances remained essentially stable. When yields started rising again in 2022, a tsunami of cash washed over the funds. And that has continued so far despite lower yields:

When MMF yields began to move higher in 2022, banks had to respond by offering higher yields on CDs and savings accounts in order to motivate new customers to put their cash into the bank and to motivate existing customers to not yank their cash out. But paying higher interest rates on deposits increases banks’ cost of funding, and they don’t do it unless they have to in order to hang on to their customers’ cash (deposits)….

… AND ‘bout that there disinflation, welp, was nice while it lasted ??

ZH: RIP December 16th 2024: The Death of Disinflation

… and Peter Tchir / Academy on upcoming FOMC meeting …

ZH: This Week's Fed Meeting Is Barely On The Radar Screen …

While I don’t care that much about this week’s FOMC, I do care a lot about where longer dated yields are headed.

I haven’t liked how the moves to higher yields have generally been unidirectional (if that is a word). Despite all the positive messaging from DOGE, there is renewed concern about the path of the deficit.

I did enjoy Treasury Secretary Yellen expressing “regret” that they didn’t do more to contain the deficit, since it wasn’t very apparent that any time was spent on trying to control the deficit. Until the voters make it clear that the deficit scares them (and I don’t really think that was part of the message that voters sent at this election), both sides will continue to spend, because it generally helps them.

If we are correct on inflation, jobs, and seasonal effects, there are some more problems out there for the rates market. We thought 4.4% and higher in the aftermath of the election was overdone and highly susceptible to a short squeeze. I don’t see that right now (and we haven’t seen it since it was at 4.2%). If anything, while we have been steadfast that the risk of a gap higher of 50 bps is far more likely than a similar gap to lower yields, we must take our range up to the 4.4% to 4.6% area on 10s.

Bearish the longer end of the yield curve (10s through 30s), though we will see how the market responds here to what seems like resistance…

…. finally, as the day and week get underway — there is to be a scheduled interruption of service whereby normal daily and weekend spammation shall resume shortly after the new year … saw this tweet and visual and it made ME pause for an extra moment and so i’m sharing …

NOTED and moving on … THAT is all for now. Off to the day job…

Thank you !!!!