while WE slept: SNB SURPRISE! CUT, USTs offered; 'mkt is here' (higher growth & equities, lower 'flation, ylds a positive supply shock -DB); something new / different for those 'huntin yield'

Bloomberg: Inflation Gives Fed Green Light for Cut in December

Markets raise bets policymakers will lower rates next week

Officials expected to dial back projected cuts for next year

CalculatedRISK: BLS: CPI Increased 0.3% in November; Core CPI increased 0.3% CalcRISK: YoY Measures of Inflation: Services, Goods and Shelter

ZH: Re-Inflation Continues - November Consumer Prices Surge Most Since April ZH: Wall Street Reacts To CPI Report, Even As Markets Price In Certainty Of Dec Rate Cut

… in as far as any noticeable impact on prices, a look at how yesterday’s 10yr auction came and went …

ZH: Stellar 10Y Auction Has Highest Bid To Cover Since 2016 Amid Surge In Demand

… and one can understand a SURGE in demand as yields were / ARE on the rise which could also be considered a concession, 10s setup was a BEARISH one … Let us have a look at long bonds …

30yy DAILY: just above what I might have said was ‘support’ (4.45) …

… BUT momentum has shifted quickly from overBOUGHT and now registering overSOLD — not yet turning / rolling over — a sigh that it may be time to ‘go with’ but then again, for those looking to get ahead of the curve AND if you think nothing of the ‘flation, THEN now might actually be time to buy … get those bids in for long bonds early and often …? todays cheapening and BEARISH LEAN (still) may be considered a concession like 10s yest …

… and so the other side of THAT coin was Field of Dreams’esque — build it and they will come — let us HOPE — not a strategy — that continues with today’s long bond…

AND there you have it … as we look ahead, then, to the days business and prepare to get those long bond bids in early and often, a quick recap of the day just passed by snark central …

ZH: 'Sell Bonds, Buy Everything Else' - Rate-Cut Hopes Soar As Markets Shrug Off Hot-flation

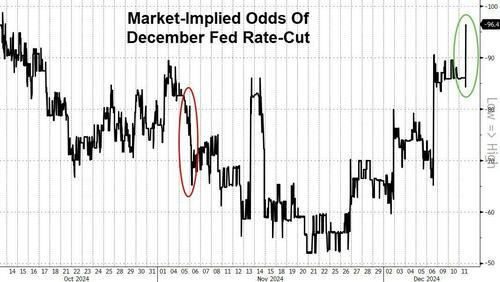

A rate-cut by The Fed next week is now a lock (according to the STIRs market)...

… here is a snapshot OF USTs as of 650a:

… and for some MORE of the news you might be able to use…INCLUDING A NEW LINK TODAY (Yield Hunting) which I’d like to mention briefly … I’ve met the proprietor of this ‘Stack while back and its title speaks VOLUMES to me, “Yield Hunting”. After years on Global Wall where desks normally sell their own positions (buyer beware) and broker lots of things, IDEAS are always and forever, one of the most valuable of commods. This site most def worth a point / click and that said … some resources and curated links for your dining and dancing pleasure …

NEWSQUAWK: SNB surprise with a 50bps cut, Euro steady ahead of ECB … Fixed benchmarks are at/towards session lows into the ECB and US data thereafter, stateside yields are bid and the curve steeper … USTs are in the red, but only modestly so. Action which came after a selloff emerged at the end of Wednesday’s US session into settlement, no specific driver behind this at the time. Currently at a low of 110-16 and continuing to slip from an initial 110-24 high print.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ about CPI and a couple / few other things …

… In this note, CPI detailed from a shop looking at the bright side of things …

BARCAP: US Economics Research: November CPI: More good than bad

Core CPI increased 0.31% m/m (3.3% y/y) amid firming core goods prices led by used cars and household furnishings. While core services inflation eased only modestly, the step-down in OER and rents CPI is encouraging. The data translate to a core PCE print of 0.20% m/m.

… The "supercore" measures of inflation stayed at 0.3% m/m. Our "PCE-equivalent" measure of core services, which excludes rents and OER CPI and adds back food-away-from home to be consistent with the composition of the PCE index, was 0.33% m/m, while core services ex shelter eased to 0.19% (from 0.30%) due to the exclusion of the strong lodging away from home print (+3.2%). The 3mma for supercore is at 0.3% m/m, about one-tenth higher than the pre-pandemic average (Figure 2)…

…We think today's CPI data carry more good news than bad. The step-down in rent and OER CPI is welcome news indeed and gives us more confidence that housing inflation is on track to move lower, especially after reviewing the regional breakdown, which indicates a fairly broad-based disinflationary trend across regions. In addition, we note that a lot of the recent strength in core CPI, including in today's report, has been led by volatile categories - namely, airline fares and lodging. These two categories together have contributed an average of 5bp to core CPI in October and November; and a run-up in used car prices has also played a key role, adding another 5bp to monthly core inflation over the same period.

In light of the latest CPI print, we continue to think the FOMC will cut rates 25bp next week. Although today's CPI reading is the fourth 0.3% print in a row, it translates to a rather benign core PCE print of 0.2% m/m, which suggests that underlying inflation is perhaps not as strong as the CPI indicates. While Fed speakers repeated that the pace of rate cuts is likely to slow in future meetings amid firmer inflation prints, resilient activity, and little labor-market slack, they did not push back against market expectations of a December cut. The committee likely continues to view policy as restrictive, and we think that it will view the latest increase in the unemployment rate to a solid 4.2% as further evidence that the labor market is cooling…

… same shop offering a(nother) thoughtful look ahead TO 2025 …

BARCAP: 2025 Outlook: A tale of tails We forecast 10y yields to end 2025 at 4.25% and the 2s10s curve at 50bp. Even as the Fed eases further, many of the forces arguing for elevated long-term yields should remain in place. However, Trump 2.0 creates significant uncertainty about the scope of easing, the neutral rate and term premium.

Key takeaways

Coming into the year, we had forecast 10y yields to be at 4.35% in Q4 24, well above the consensus at the time of 3.75%. We believed that the economy was likely to remain resilient and inflation progress would likely be slower. We noted that the neutral rate had shifted higher, arguing for a shallow easing cycle, and investors were also likely to demand a healthy term premium for taking duration risk. 10y yields have averaged 4.2% in Q4 so far, as well as YTD.

In our baseline outlook of a soft landing, we forecast 2y and 10y yields to end 2025 at 3.75% and 4.25%, respectively, and the 2s10s yield curve to steepen to 50bp. Even as the Fed is likely to continue lowering the policy rate, pulling front-end yields lower, many of the forces that argue for longer-term yields to remain elevated are still in place: a high neutral rate, elevated rate volatility, the inflation risk premium, and large net issuance amid price-sensitive demand.

We see Trump 2.0 as creating significant uncertainty about this baseline, as proposed policies have uncertain and conflicting effects on the outlook. Higher tariffs and tighter immigration controls argue for slower growth but higher inflation. Deregulation would do the opposite. Deficit reduction argues for lower growth and inflation. A unified government should be able to maintain a robust economy, but these policies create uncertainty about the scope of easing, the level of the neutral rate and the term premium.

We see two tail risks to our baseline. In our view, 10y yields could rise to 5% if a pickup in underlying inflation forces the Fed to be on hold for 2025 and unfunded new tax cuts push the term premium higher. But 10y yields could fall to 3.25% if continued cooling in the labor market coupled with meaningful budget deficit reduction push the Fed to deliver significant cuts over time. When compared with market levels, the skew is towards lower yields up to the intermediate sector.

We expect the Treasury to keep coupon auction sizes unchanged for almost all of 2025, as the Treasury is well funded and the share of T-bills should drift lower; any increase would be "deftly handled," to borrow a phrase from Treasury Secretary nominee Scott Bessent. We expect net coupon issuance to investors to decline to $1.6trn in 2025 from $1.8trn in 2024, due primarily to swings in the Fed's Treasury holdings as it ends QT early next year. An unfunded tax cut would create upside risk for issuance, with implications for the US sovereign rating.

Demand for US Treasuries has been broad-based, driven by foreign private investors, domestic mutual funds, commercial banks and long-term accounts such as pension and insurance funds. Foreign official institutions have been net sellers. The Fed is likely to be a buyer of USTs next year, and a positively sloping curve should spur price-sensitive demand, such as from households, even as there is likely to be heightened sensitivity to newsflow…

… in this next note, a large German bank and very popular stratEgerist RECAPS CPI and separately asks / attempts to answer a very good question … keeping in mind, too, this was written and distributed BEFORE CPI report …

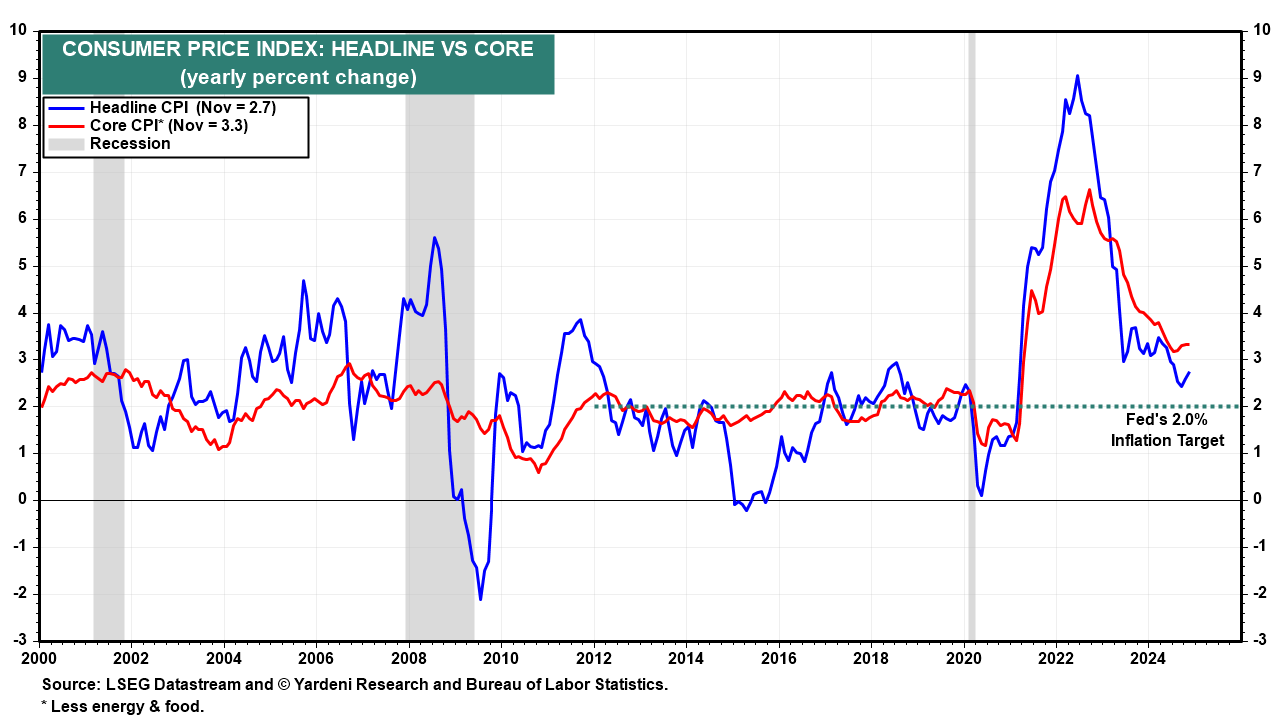

… In terms of the details of that CPI print, the monthly headline and core CPI readings were both at +0.31% in November. So that was basically in line with the +0.3% print the consensus was expecting. So even though inflation was still running a bit too fast for the Fed to be comfortable, markets were relieved that it wasn’t an even higher number that would prevent the Fed cutting rates next week. After all, core CPI has now been running at +0.3% for four consecutive months, and the 3-month annualised rate for core CPI ticked up to +3.7%, so this isn’t just a case of one strong print. And in turn, that’s led to growing concern that inflation is becoming sticky above target, even if we’re not seeing the really high numbers of a couple of years ago. For the year-on-year numbers, the latest release meant headline CPI ticked up to +2.7%, whilst the core CPI print was steady at 3.3%, where it’s been for the last three months now.

Admittedly, one piece of good news was that shelter and services inflation moderated, and those are fairly sticky categories, even if this decline was offset by stronger goods prices. But even though Treasury yields fell by several basis points after the CPI print, lingering inflation concerns saw this move reverse later on. For instance, 10yr yields closed near the session highs (+4.5bps to 4.27%), rising for a third consecutive day despite a solid 10yr auction.

Nevertheless, when it comes to the Fed, the CPI print left little doubt among investors that another rate cut will happen next week. Indeed, futures moved up the likelihood of a cut from 86% right before the CPI came out to 99% by the close. It’s true that inflation is still too fast for their liking, but last week’s jobs report also saw a fresh rise in the unemployment rate, so our US economists think that will still enable them to cut next week…

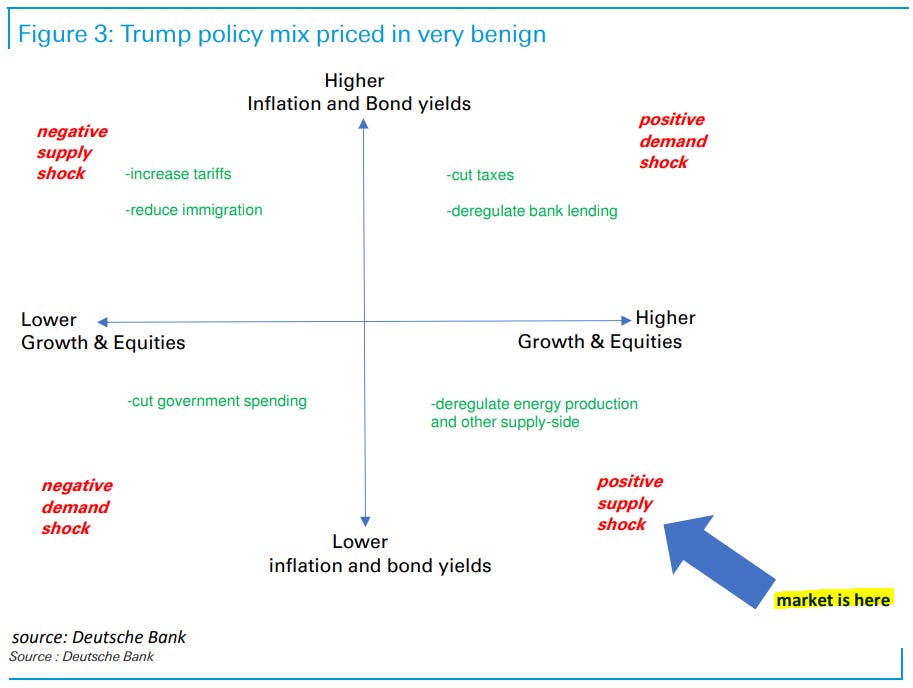

We have been writing extensively about why we think the Trump policy mix that is priced in to the market is ambitiously benign. Leaving this aside however, it is important to note that the US data is already pointing in a significantly more inflationary direction than just a few months ago. First, as highlighted by our fixed income colleagues, forward-looking indicators of housing inflation have started to turn back up (chart 1). Second, immigration flows into the US have recently slowed very sharply, even before President-elect Trump comes into office (chart 2, job done?). As we have argued, the immigration positive supply shock played a dominant role in allowing the Fed to turn more dovish this year. But by extension, a reversal of this shock, combined with more housing inflation, will have the opposite effect.

The bottom line is that the two key drivers of services inflation are now pointing to upside inflation risks, even before the new Trump administration comes into office. We fully agree with our House View that after a (possible) Fed cut this month, the FOMC will enter a very long pause throughout next year. On the flipside, we also fully agree with our House View that the ECB should be priced to cut significantly more. Three-month annualized core inflation is close to 1% and, more importantly, the broadest measure of inflation (GDP deflator) is already close to 2% this year. We are only a couple of inflation prints away from the ECB worrying about sub-target inflation. Bottom line, even without Trump, there is more Fed - ECB repricing to go and EUR/USD pressures remain to the downside…

… finally, same firm offering some longer-term perspective on TRADE ahead of Jan 20th handoff …

We share five key points on global trade as we look towards 2025 taking the lens of economic history, which sheds a different light on many topics.

1. Protectionism has been positive for industrial development through history…

…2. Economic security could be more important than inflation…. …3. Trade is booming down some corridors… …4. China is picking up the mantle of the global trading power… …5. China is more likely to retaliate than accommodate US trade pressure given the lessons from Japan…

… finally, a very interesting question posed, unanswered (and dealt with more below from The Terminal) …

Yardeni: Will Rate Cuts Continue Unless Inflation Behaves Badly?

Today's CPI report for November matched expectations. The CME FedWatch tool shows 95% odds that the FOMC will cut the federal funds rate (FFR) by 25bps next week, and the Fed doesn't like to surprise market expectations.

The Nasdaq front-ran our forecast to reach 20,000 by mid-2025 by reaching that milestone today (chart). Now we are aiming for 22,000 by mid-2025. Our yearend target of 6100 for the S&P 500 may also soon be exceeded ahead of schedule. Perversely, the big gains piling up in stock portfolios could trigger a significant pullback in January as investors rebalance in 2025 rather than now to defer capital gains taxes.

Today's inflation report suggests that it is still heading in the right direction towards the Fed's 2.0% target. However, it's not there yet, while the labor market remains strong. Further easing by the Fed risks heating up price inflation and speculative excesses in the financial markets.

Let's review today's CPI report:

(1) November's headline and core CPI inflation rates were 2.7% and 3.3% y/y (chart). Both exceed the Fed's 2.0% inflation target, though it actually applies to the PCED inflation rate, which tends to be lower than the CPI inflation measure. Indeed, October's headline and core PCED inflation rates were 2.3% and 2.8%.

Rent inflation still remains high, but it is moderating. Excluding shelter, the headline and core CPI were up just 1.6% y/y and 2.2% in November. Inflation has moderated as we predicted during the summer of 2022…

… And from Global Wall Street inbox TO the WWW … to turn a phrase, Houston, we’ve got a problem …

Bloomberg: DC, We Have A Problem... Inflation Is Not Going Away

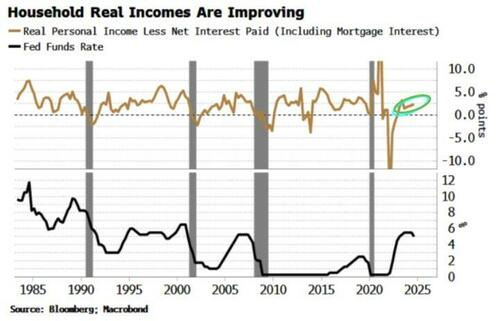

… The household sector (brown line in the chart above) has been shielded from the worst effects of rising rates by long fixed-rate mortgages, as well as rising purchases of money market funds. The net interest received by the household sector has remained largely stable since the Fed started tightening policy.

Households’ real personal income, even after netting out interest payments (including mortgage interest), is positive and rising. It is very unusual for Fed to be cutting rates when real income is improving.

It’s also incongruous for the Fed to ease when leading data is becoming consistent with a cyclical upturn in the economy. Growth has persistently outperformed most expectations this year, but manufacturing has been sluggish. It’s the much larger services sector that has kept growth on track.

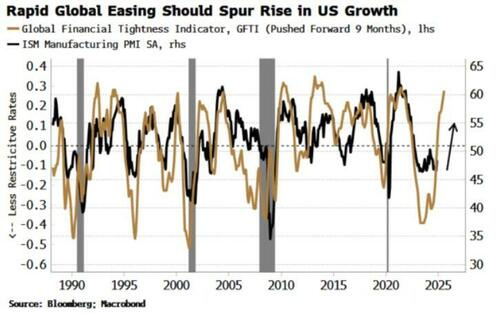

However, a global easing in monetary policy points to a renewed rise in manufacturing, the most cyclical and leading part of the economy. The Global Financial Tightness Indicator – a diffusion of central-bank rate hikes – has risen sharply as central banks around the world eased policy at one of the most rapid clips on record, indicating a significant loosening in monetary conditions and pointing to a stronger ISM.

The jobs market was the most plausible reason for the Fed cutting this year, the thinking being that the bank wanted to get in front of a slowdown. Employment has clearly softened, but has not decisively weakened to a point that demands imminent easing, especially as inflation risks linger and speculative froth returns to the market, 2021-style (trading on memes is most definitely back)…

… another of Bloomberg’s ‘popular kids’ discussing the flation …

Bloomberg / Authers OpED: Inflation took a licking. Why's it still ticking? It’s stubbornly settling above the desired 2.0%, which won’t stop a Fed cut next week but should put the Trump team on notice.

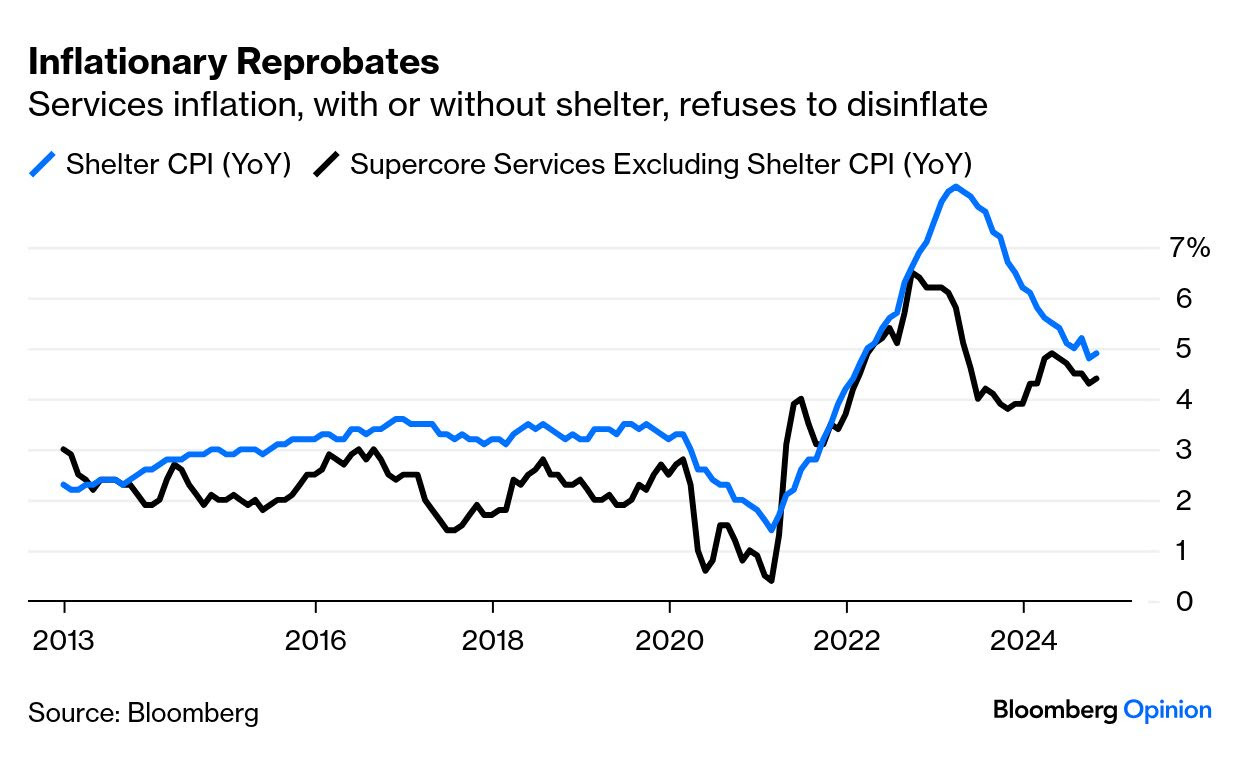

… Within services, both the Fed’s recently targeted “supercore” (services excluding shelter), and shelter itself have ticked up on a year-on-year basis. Shelter price rises fell over the last year but remain at about 5%, while the supercore bottomed a year ago. It remains above 4%:

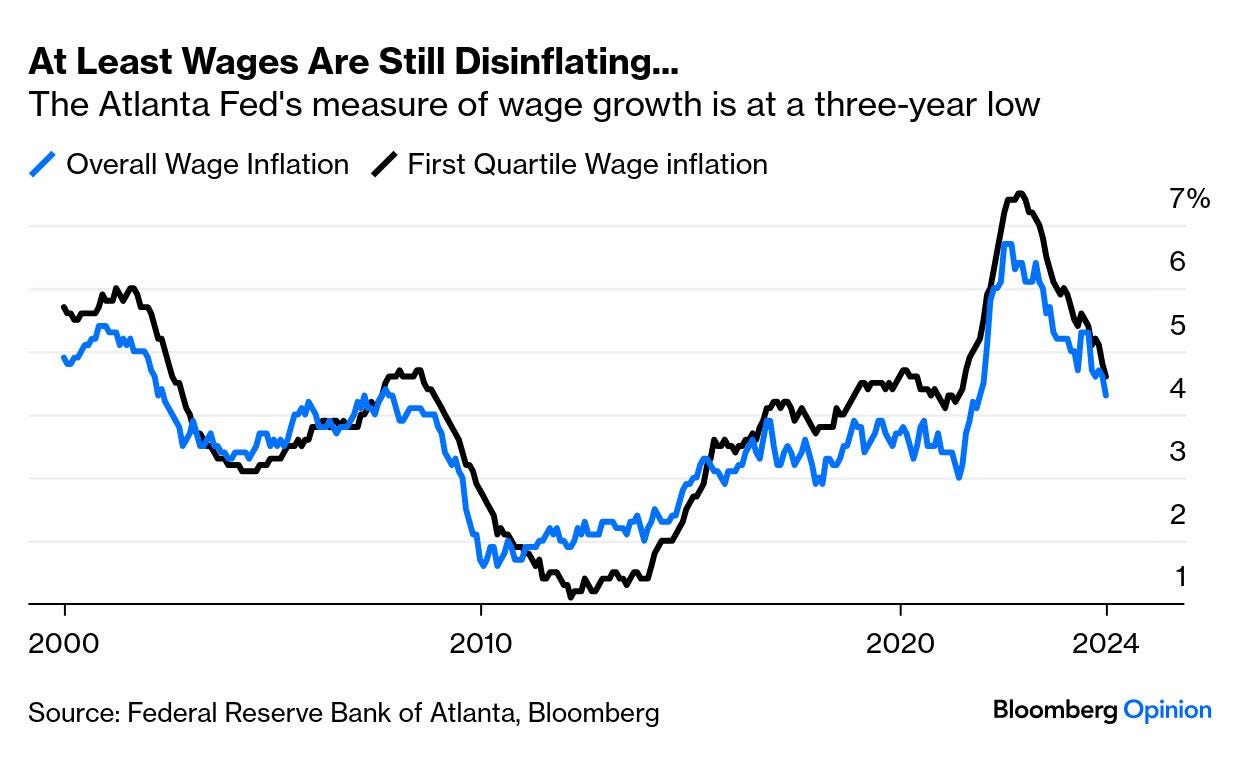

Perhaps the most encouraging news of the day for the central bank came from the Atlanta Fed’s monthly survey of wage growth, based on census data. It’s dropped to a three-year low, and the same is true of the lowest paid (those in the first quartile of earnings), who are most likely to spend any increase they receive. While not great news for workers, this is encouraging for central bankers:

It’s difficult therefore to attribute stubborn inflation solely to the way the Bureau of Labor Statistics calculates rent inflation, but complaints are valid. The BLS uses an average of all leases in force, so inevitably lags private sector indexes of rents that have been negotiated in the last month. Zillow’s rent index on this basis showed rental inflation taking off ahead of the official number, and identified the peak perfectly. Sadly, it now implies that rental disinflation is over…

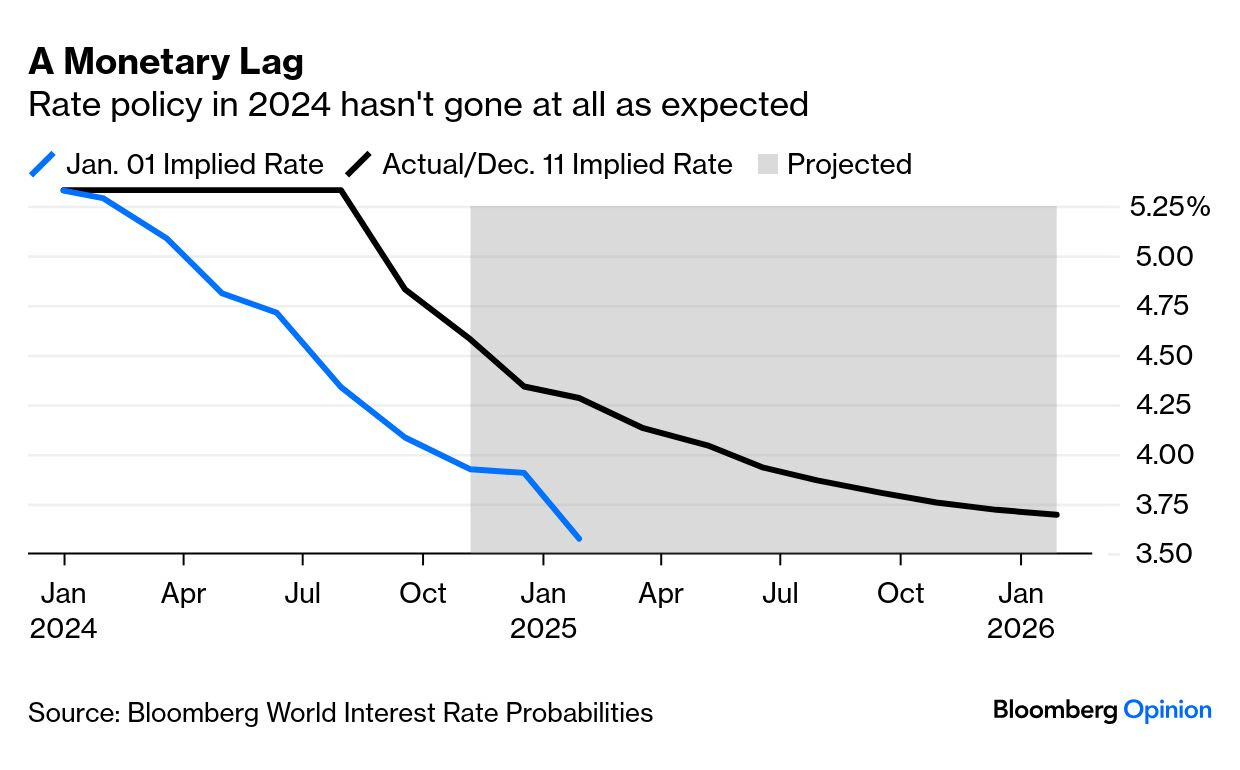

… So, Will They Cut Rates?

The one question that most exercised dealers was: “Is this high enough to force the Fed not to cut rates next week?” Their answer wasno. So fed funds futures put the odds of a cut at 100%. But that certainty shouldn’t obscure growing uncertainty over what comes next. This chart shows futures’ projected path at the start of this year,along with what actually happened and current predictions for what lies ahead. Two points stand out. First, this year has gone nothing like expectation, and second, the prevailing belief remains that the fed funds rate will get below 3.75%; it’s just that it will take a year longer to get there:

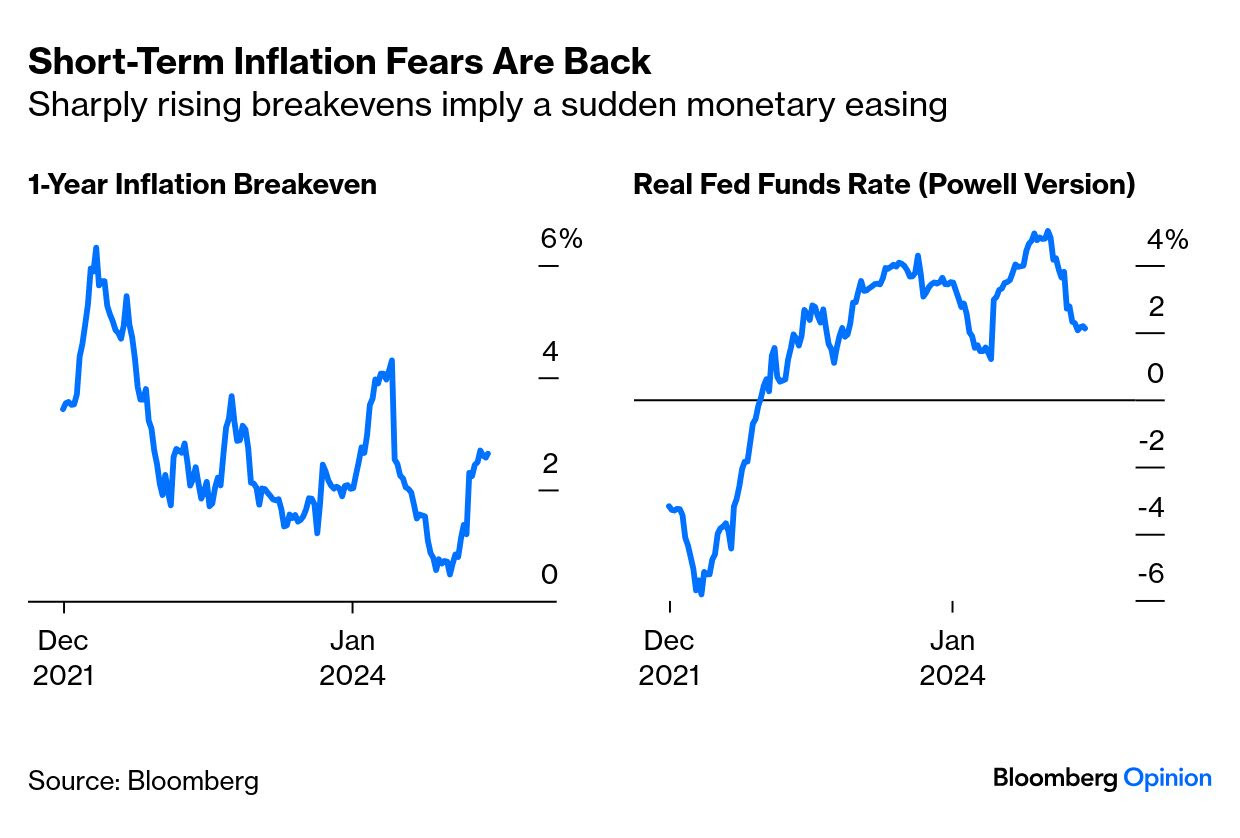

As futures traders are confident that the Fed will pause in January to await developments, this is surprising. At the margin, Trump 2.0 policies of tariffs and tax cuts would tend to push prices up, not down. That shows up in one-year bond market inflation expectations, which at one point had dropped below 1% yet have doubled since the election. This shouldn’t be any great concern for the central bank, but shows that the perception of risks has changed. It also means that Jerome Powell’s favored measure of real rates — subtracting the one-year breakeven from fed funds — has dropped sharply. If the Fed wants to keep rates where they are, it has license to do so:

The most likely outcome is that the Fed has to accept inflation above 2%, and set rates higher than many in the market had hoped, to keep it from getting out of control at that level. There are many worse outcomes, but even this one isn’t currently priced in by the market. Tom Tzitzouris of Strategas Research Partners argues:

Today’s CPI tells us that the sticky level is not 2.0%, it’s more like 2.5%, or greater, and that means bonds could eventually have at least one more round of pain if breakevens correct to reflect this higher long-run level of inflation. This won’t stop the Fed from easing next week, but sticky inflation tells us that a pause is coming, and if breakevens surge too, expect the Fed to stop cold.

And That Means We Can Buy Stocks…

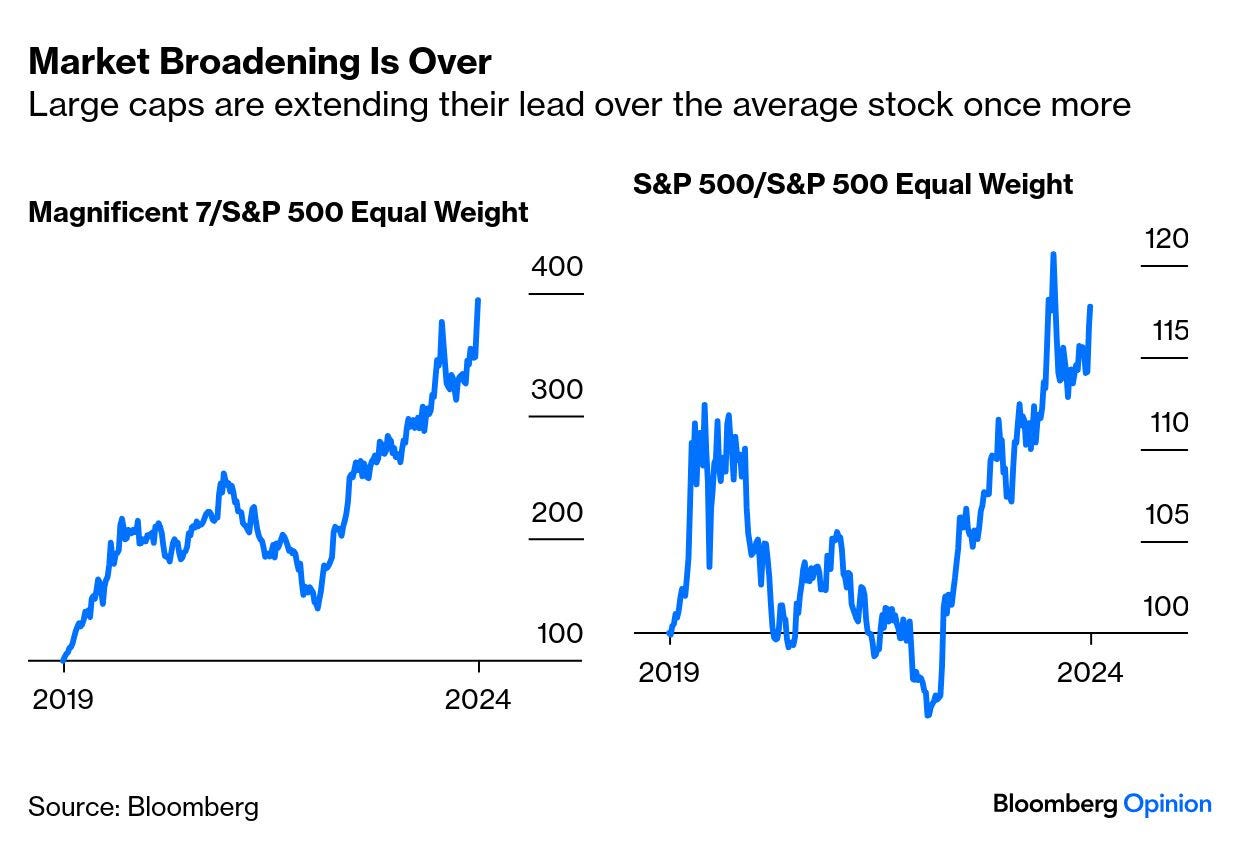

For the medium term, November CPI settles nothing. But it appears that equity investors are only concerned about the last remaining uncertainty over what happens next week. CPI was the most plausible catalyst to explain a surge that brought the Nasdaq 100 and Bloomberg Magnificent Seven indexes to all-time highs, while the Nasdaq Composite topped 20,000 for the first time. The US equity market had been broadening, but the big tech names are dominating once more:

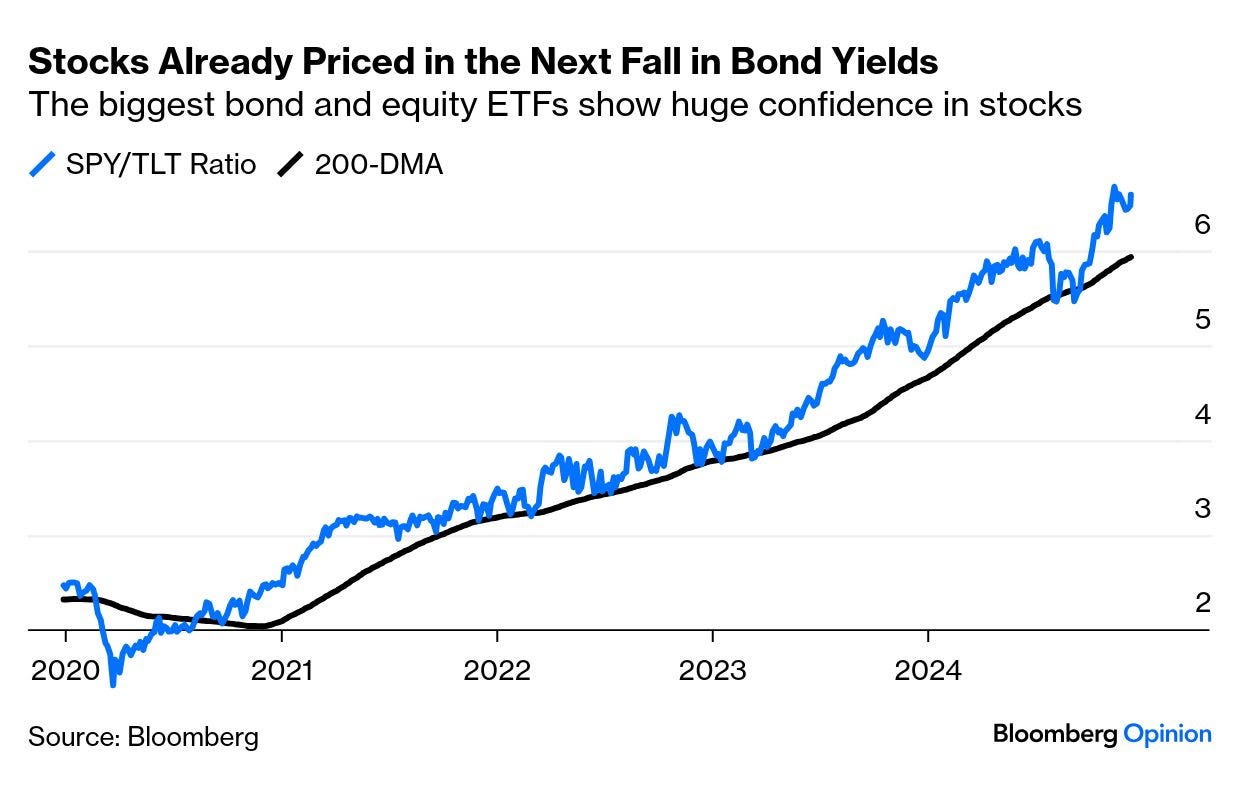

Analysts who spoke to Bloomberg suggested that certainty over the next rate cut was helping share prices. It’s highly questionable whether this is a good reason to buy stocks. Using an old-fashioned rule of thumb, we can compare the earnings yield (inverse of the price/earnings multiple) of the Nasdaq 100 with the 10-year Treasury yield. The more stocks yield relative to bonds, the more attractive they are, and vice versa. This is how the spread between the two has moved since the Nasdaq 100 returned to profitability in 2002:

It’s not clear that bond yields’ next move will be down (which would justify paying more for stocks). Even if it is, the outperformance of bonds by stocks (proxied in the chart by the exchange-traded funds tickered SPY and TLT) suggests that stocks have already priced in that move:

In absolute terms, it bears repeating, tech stocks are really, really expensive.