while WE slept: USTs a touch cheaper (China Yuan story, then 'rugpull'); "The GFC's long shadow" -DB; "110-year history of U.S. inflation and global conflicts" -PIMCO

Good morning … another short note ahead and I’ll begin with a look at 10yy …

… rangebound with a bearish lean, at least on the daily charts, best I reckon. On a positive note, there is a concession being put IN TO rates complex here for duration ahead of CPI … IF, say I were bearish today (I am), it would / should be noted not everyone else is …

Bloomberg: Bond Traders Trim Long Bets Before CPI Data Seen as Key for Fed

JPMorgan survey shows clients shift to neutral from long bias

This week also saw trimming of futures bets on Fed cuts

… trimming (not eliminating OF LONGS) with more below and in fact, there’s quite a bit of optimism ‘out there … example, before UST supply kicked off folks were apparently optimistic …

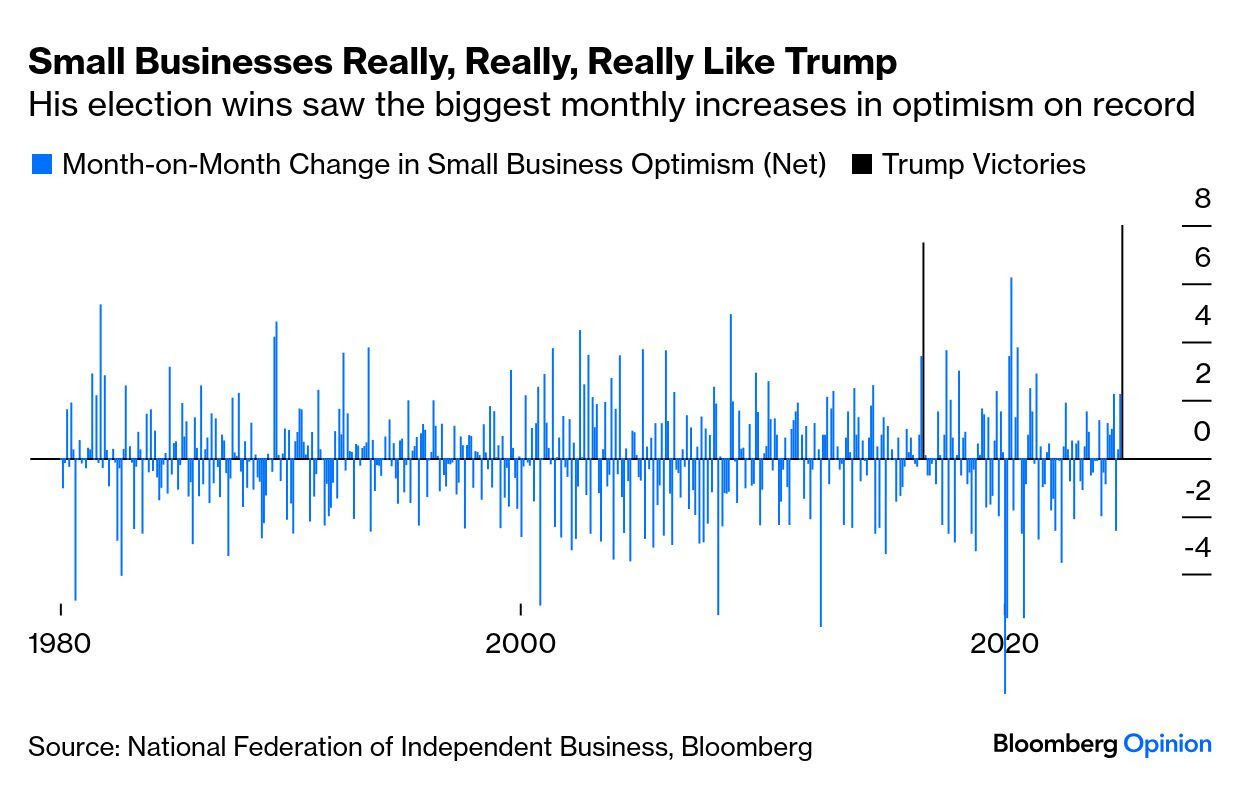

ZH: Trump Victory Sends Small Business Optimism Soaring Most In 44 Years

… apparently this optimism extended to bonds …

ZH: Treasury Yields Drop After 3Y Auction Tails But Is Otherwise Solid

… Overall, this was a solid if not stellar auction, and good enough to prevent more selling in the secondary market: the yield on the 10Y was flat after the auction and has since dipped 1bp to 4.22% after earlier rising as high as 4.24%, a one week high.

… will this translate through to today’s upcoming $39bb 10yr auction remains to be seen … ahead of today’s upcoming $58bb 3yr UST auction, a look at USTs from someone with A Terminal …

CHARTbeat: Fixed Income: Treasuries Weekly rotation of debt-based charts

… all told, news and views YESTERDAY in sum total, by days END …

ZH: Mega-Caps Pump'n'Dump Ahead Of CPI; Bitcoin Slumps As Gold Jumps

… Treasuries were sold today with the entire curve up around 2-3bps. Notably the selling started at the European open (after Asian session buying) once again...

I’ll quit while I’m behind and have already said too much ahead of CPI so get those bids in for 10s early and often … here is a snapshot OF USTs as of 626a:

… and for some MORE of the news you might be able to use…some curated links in case you’d like and do not have much more in the way of time …

NEWSQUAWK: US Market Open: DXY bid on reports that China is considering allowing the Yuan to weaken in 2025; US CPI due … USTs are back in negative territory after support from a Reuters report noting that China could be willing to let the Yuan devalue next year, proved to be short-lived. Mar'25 contract is currently tucked within yesterday's 110.26-111.09 range, ahead of US CPI.

Opening Bell Daily: Fed vs. Markets … Inflation isn't cooling but the Fed will likely cut rates anyway … None of the key economic data has fallen into the central bank's target range.

As anticipated, uncertainty around the neutral rate has featured in recent Fed communications as a reason to proceed cautiously with further rate cuts.

Our rates forecast assumes a neutral real rate of 1.75-2%, a bit above the midpoint of the range of model estimates we track. That level is elevated relative to estimates of r-star over the 2010s, but we view that as an anomalous period, largely due to the long shadow of the GFC. Recoveries from financial crises tend to be slow and halting, and US households and the financial sector undertook an unprecedented de-leveraging that boosted desired savings and weighed on short-term rates.

In making this point, a comment we often get back is that a decade seems a very long time for that balance sheet repair to have taken.

But as shown below, according to the Fed’s Survey of Consumer Finances – a triennial survey of US households – it wasn’t until 2022 that median real net worth across all income quantiles exceeded 2007 levels. Remarkably, in 2019, only the top decile had median net worth above where it was in 2007. That is, it did indeed take 15 years for the post-GFC balance sheet repair to play out, and the massive fiscal and monetary impulse from Covid policies gave it the final push.

This is a key reason we don’t expect to return to the low neutral-rate world that prevailed pre-Covid. And that would actually be a great outcome for the economy, as among other implications a higher normal level of short-term rates gives the Fed more conventional policy ammunition to respond to economic weakness.

US core CPI is expected to come in at 0.3% month-on-month, which on an annualised basis is not great. So despite cooling growth, this does push back against the bullish case for USTs. But the bigger market moves will come next year, which we outline in our Rates Outlook for 2025

…The landing zone of central banks is a key theme for 2025, but plenty of other drivers to watch Whilst markets will be watching the US CPI number on Wednesday, the bigger moves in rates will show up in 2025. In our Rates Outlook for 2025, we touch upon the drivers for rates going into next year, including our 5%+ target for the 10Y UST yield, a steeper euro swap curve, the latest on European government bonds and Sovereign, Supranational, and Agency spreads, and the rates implications from Dutch pension fund reforms.

The key theme is the normalisation of policy rates, but the ride down to the landing zone could be bumpy. Inflation remains stubborn in many countries and yet growth seems to be cooling down. The European Central Bank is clearly taking a dovish stance and we expect a landing zone of 1.75%, just below the neutral estimate of 2-2.25%. But in the meantime, markets may get too greedy and we could see some undershooting in terms of EUR rates to the downside.

Besides monetary policy, we see US fiscal dynamics as an important driver for the UST yield curve, and with spillovers to global yields. Higher issuance will be expressed in a steepening of the curve from the back end and wider swap spreads, keeping UST rates well above most other developed markets. The higher US rates will have spillovers to other jurisdictions, and for the euro swap curve we forecast that 10y rates could actually be pulled higher by the end of 2025 than current levels. Having said that, the downside risks to EUR rates cannot be ignored, and with plenty of (geo)political risks in the region risk sentiment may be challenged…

… a longer-term perspective and a question …

PIMCO Macro Signposts: Global Inflation: Is the Tide Turning?

U.S. inflation has dropped from a staggering peak of 9.1% during the height of COVID-19 to a more manageable 2.6% as of October 2024, as measured by the headline Consumer Price Index (CPI). This dramatic shift raises important questions about the trajectory of inflation: Are we on the cusp of a return to the golden era of low and stable inflation that characterized the economy from the 1990s to the mid-2010s? Or are we reverting to a historical norm marked by inflation averaging above 2% and heightened volatility?

The upshot is we believe the tide has most likely turned: Inflation may be more volatile and linger above central bank targets. Several global macroeconomic trends drive this view. And for investors, this means assessing portfolios’ resilience to inflation – and to inflation surprises. Real assets, such as inflation-linked bonds, may offer attractive real yields and inflation hedging.

The golden era of low and stable inflation The period from 1990s to mid-2010s had remarkably low headline inflation in the U.S., averaging just 2.4% (see Figure 1). This compares with an average inflation rate of 3.6% over the 75 years prior and 3.4% since 2016. More remarkably, the volatility of inflation during this period was a mere 1.2%, versus 5.6% and 2.2% in the other two periods. When viewed from the lens of a 110-year history, the era of calm appears more as an anomaly than a standard (see Figure 1, top panel).

Figure 1: 110-year history of U.S. inflation and global conflicts

A closer examination of this unique period reveals key macro trends underpinning lower inflation…

…What lies ahead for inflation? The reversal of conditions means we could stay in a higher inflation and higher volatility world. The trend of goods disinflation that characterized the previous era is likely coming to an end as deglobalization takes hold. Simultaneously, services inflation may be boosted by populist anti-immigration policies, potentially leading to less labor supply and higher prices.

In the near term – or longer, depending on future governments – fiscal policies, trade policies, and geopolitical tensions also pose significant risks to inflation. With the U.S. fiscal deficit projected to remain above 6% (according to the Congressional Budget Office), and the potential for tariffs to increase significantly across the board (as U.S. President-elect Donald Trump has indicated he intends to do), the inflation landscape is fraught with uncertainty. Additionally, geopolitical risks in Europe, the Middle East, and Asia – particularly concerning Taiwan – could disrupt supply chains and accelerate inflation.

Central banks will seek to keep inflation (and inflation expectations) near target via ordinary and perhaps extraordinary means, but these global trends could pose clear challenges.

Investment implications The potential return of elevated inflation volatility carries several important implications.

Long-term breakeven inflation rates are currently priced at 2.3% (according to Bloomberg), exactly the same as the average inflation during the golden era (and just above the Federal Reserve’s target), indicating a lack of risk premium despite recent inflation spikes, the near-term inflation risks, and a potential return to a higher inflation and higher volatility regime. As inflation surprises become more likely, the risk premium should rise.

Given the evolving inflation landscape, investors may need to reassess their strategies. Real yields on U.S. Treasury Inflation-Protected Securities (TIPS) are currently at 15-year highs (see Figure 3), exceeding the Fed’s model estimates of neutral rates by 75–125 basis points (according to the New York Fed), presenting an attractive opportunity for those seeking to hedge inflation.

Figure 3: Real yield on 10-year U.S. TIPS at 15-year high

US consumer price inflation data is due for November. These numbers are something of a mess. A quarter of the index is a fantasy price no one pays. Income inequality means the average price is less representative of most US households’ experience. The threat of taxes on US consumers from the next administration means this inflation data is not necessarily a good guide to 2025 trends.

The market consensus is for more or less stable headline and core inflation rates. However, roughly half the US metropolitan areas had inflation below 2.5% in the past two months. Calculated using European methods (which ignores the fantasy housing measures) US inflation has been below 2% for six months. This numbers are important; if inflation reality is less than the headline, spending power for US households is enhanced giving a firm foundation for US economic growth…

… ‘bout NFIB …

Wells Fargo: Small Business Optimism Surges in November Expectations Bolstered by a Decided Election and Ongoing Rate Cuts

Summary Compensation Pressures Not Helping Inflation

Small business optimism surged in November alongside a promptly decided election outcome. The headline index soared eight points to 101.7, its highest reading since June 2021. After years of elevated inflation and interest rate hikes, November marked the first month since January 2022 that NFIB small optimism rose above its longer-term average of 98. While the election outcome likely bolstered confidence, back-to-back rate cuts from the Federal Reserve also improved lending conditions for small businesses. The share of firms anticipating better economic conditions, better lending conditions and better sales all improved over the month. Although job openings continued to trend lower through the monthly volatility, hiring plans made a notable jump, reaching its highest reading over the past year. More resilient small business labor demand seems to be putting upward pressure on compensation plans, which may add a complication to inflation’s already stubborn descent. The percent of small firms raising selling prices rebounded to 24% on net, just one point shy of the share one year ago.

… finally, ahead of CPI, a few words from Dr. Bond Vigilante …

The stock market appeared calm ahead of tomorrow's November CPI report, which is likely to show that supercore inflation (i.e., CPI services less shelter) remains stuck around 4.5% (chart).

However, there was plenty of action just below the surface of the stock market's calm. Oracle dropped 6.7% on disappointing earnings results. Google rallied 5.3% on a new state-of-the-art chip "Willow," which promises to be a quantum leap in quantum computing. It reportedly outpaces today's supercomputers by several orders of magnitude. To us, this is the latest evolution of the Digital Revolution, which is all about data processing, i.e., processing more and more data, faster and faster. AI is likewise an evolutionary technology in the Digital Revolution.

Tech companies continue to find ways to accelerate the pace and volume of processing data. As a result, the forward earnings per share of the S&P 500 Information Technology sector and its stock price index continue rising in record high territory (chart).

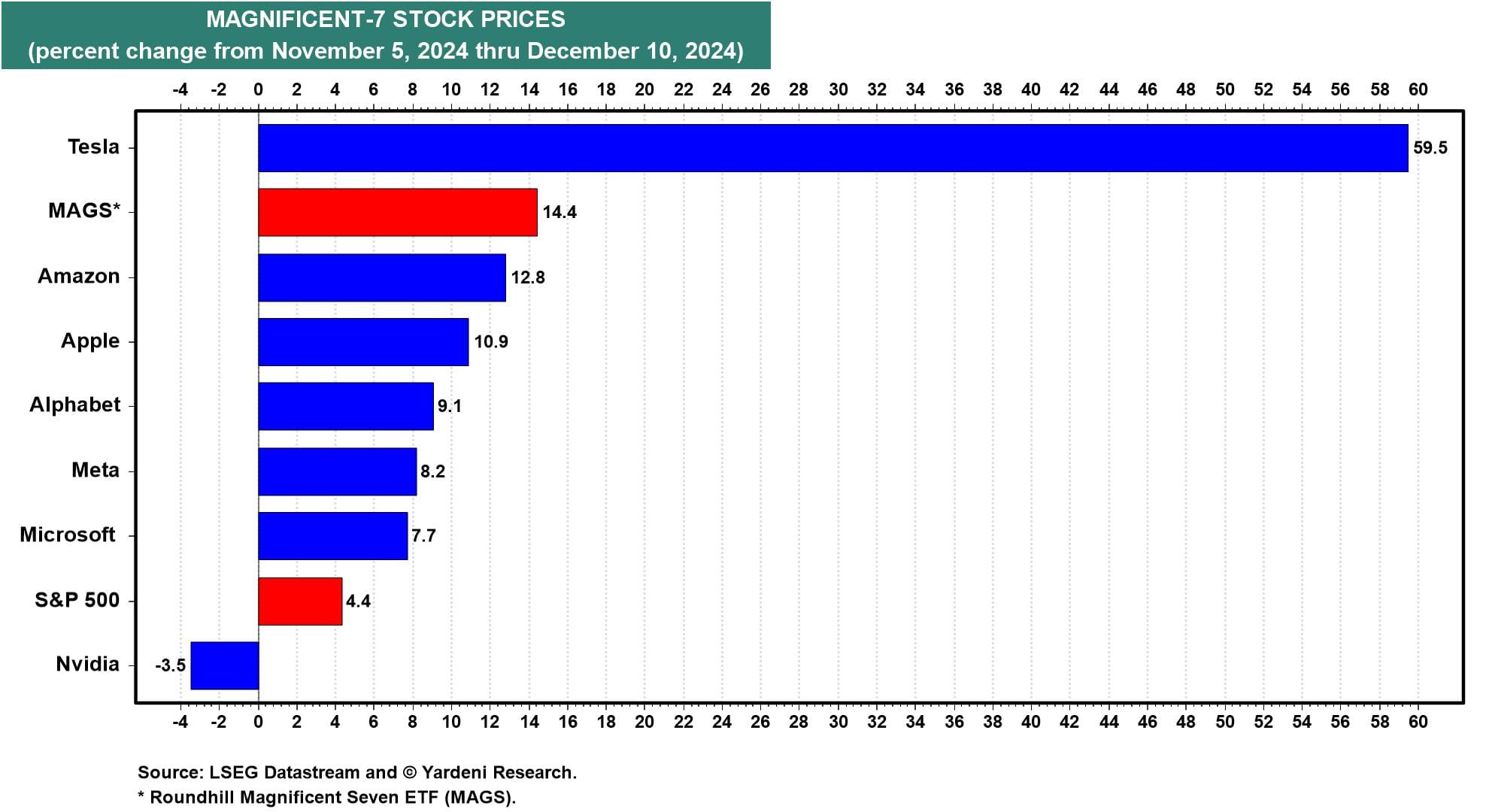

Tesla is a tech company that makes cars. It was up another 2.9% today to extend its post-election rally to 59.5% (chart). Much of the recent exuberance stems from Elon Musk's bromance with President Trump. That said, US and EU tariffs on China's EV exports are just one tangible outcome that should support its growth expectations (chart). Because Tesla can remotely update its fleet's software, its ability to scale and grow are more similar to the other tech companies in the Magnificent-7 than an auto manufacturer.

… And from Global Wall Street inbox TO the WWW …

… Here’s an interesting visual interpretation from yesterdays NFIB survey …

BESPOKE: Small Business Sentiment Surges Post Election

… In the charts below, we have taken each category of the report (standardizing using a z-score) and averaged whether they are based on hard or soft data. As shown, although November did see stronger hard data, the jump in soft data was much larger. In other words, businesses did see improvements, but their expectations and feelings are much more rosy than more substantiated data may imply. Taking a spread of the two, soft data now leads hard data to the widest degree since the end of the last Trump administration. Looking back historically, that's normal. On average, the spread has tended to be modestly positive (+0.07) during Republican administrations versus a firmly negative (-0.23) average reading when the Democratic party was in power.

That's it for our latest look at small business sentiment.

… a couple from Bloomberg … first on positions and THEN a note on private assets with an interesting NFIB visual …

Bloomberg: Bond Traders Trim Long Bets Before CPI Data Seen as Key for Fed

JPMorgan survey shows clients shift to neutral from long bias

This week also saw trimming of futures bets on Fed cuts

Bond traders are taking chips off the table, opting for a more neutral stance before Wednesday’s US consumer-price data, which will be decisive in setting expectations for whether the Federal Reserve cuts interest rates again this month.

JPMorgan Chase & Co.’s weekly survey on Tuesday showed the bank’s clients have shifted to a neutral stance on Treasuries from the strongest long bias this year, stepping back following a three-week rally in US government debt.

The November consumer-inflation reading due Wednesday is expected to show a small acceleration on both a monthly and annual basis. The report is in focus after Fed Governor Christopher Waller earlier this month said that data due before officials meet Dec. 17-18 could make the case for holding rates steady, although he’s inclined to reduce rates again for the third consecutive time.

While swaps markets are pricing in a roughly 80% chance of a quarter-point Fed cut this month, the resilient US economy — and speculation that the policies of President-elect Donald Trump will spur quicker inflation — have opened the door to bets on a pause at some point. Beyond Dec. 18, markets are reflecting roughly two additional quarter-point reductions by the end of next year.

The market for fed funds futures, which closely tracks expectations for the Fed, showed a similar move to trim wagers on a rate cut this month. The latest open interest data dropped in both the January and February futures, in a sign that investors are unwinding long positions.

…JPMorgan Treasury Client Survey In the week to Dec. 9, JPMorgan clients shifted positioning into neutral and out of longs, while the level of short positions was steady. Over the period, bullish positioning dropped 6 percentage points and neutrals increased the same amount. Outright long positions dropped back to the same level seen a couple of weeks ago, while neutrals are the most elevated in two weeks.

Bloomberg: You’ll Take Private Assets, and Like It Pension fund managers increasingly find that TINA has been privatized. There’s no choice but to go along, even if returns disappoint.

…More Fun with Political Sentiments Economic surveys have been made increasingly harder by political polarization. But one critical segment of the economy has always been driven by a firm view that a particular partisan approach (from Republicans) will benefit them — small businesses. And the election’s impact on the optimism of those who run them is extraordinary.

The National Federation of Independent Business’ index of such sentimenthas just enjoyed its biggest month-on-month increase since 1980. It beats the previous record increase, set in the month Trump won the first time:

…Small business owners matter greatly. They may or may not be right to have such confidence that a Trump administration will improve the environment for them. And it’s possible that they’re simply loyally telling pollsters that things will be better now. But animal spirits like this, in a crucial sector of the economy, should be a great tailwind for Trump. If companies think it’s safe to invest and do so, that’s the administration’s battle won, no matter what policies they eventually enact.

… important labor mkt sectors detailed by a very bright guy …

EPB Research: The Two Most Important Labor Market Sectors Analyzing the two biggest sectors that drive the overall labor market.

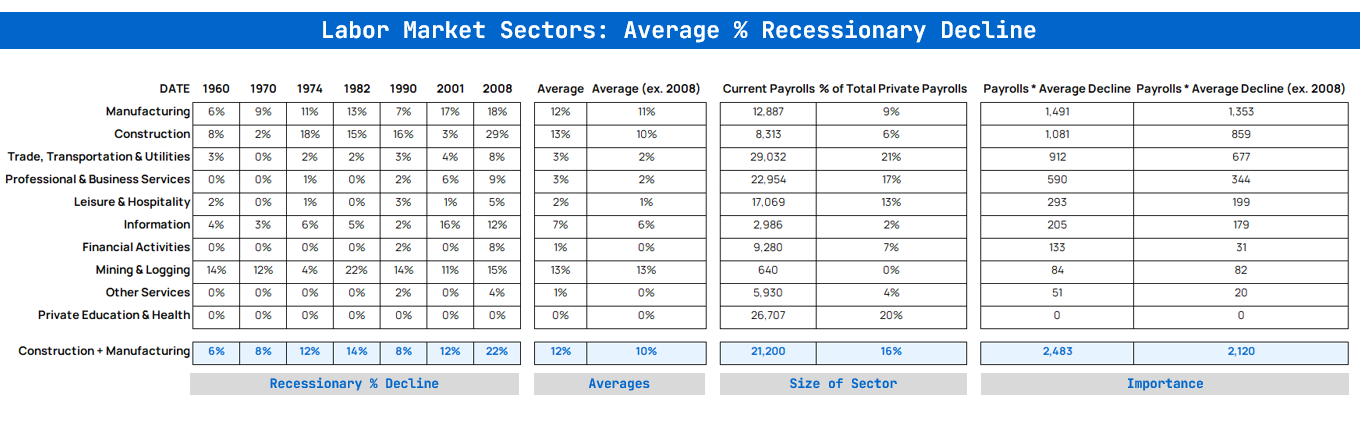

… Manufacturing and construction are still the two most important sectors of the labor market, even though currently they represent just 16% of private sector payrolls.

Trade, Transportation & Utilities ranks third, followed by Professional & Business Services fourth.

The chart below shows the combination of construction and manufacturing payrolls and the percentage decline around economic downturns.

These sectors have not lost any cyclicality or volatility in more modern downturns. They have lost size but not cyclicality.

Even at the current size, the amplitude or the swings in these two sectors is the overwhelming driver of the ups and downs in the labor market.

If every sector had an *average* decline in payrolls, based on history, construction and manufacturing would still represent 52% of all job losses despite being just 16% of the total size.

Don’t let the shrinking size of these sectors convince you that they are less important to the overall economy.

If the economy has a downturn in construction and manufacturing jobs, it will still be extremely difficult to avoid a recession.

However, without a downturn in these two sectors, no other sector will be able to have enough force to create a downward spiral.

… 2025 …

LPL: Expect Stocks to Go Higher in 2025, but No One-Way Street

…Current market pricing suggests the Fed will take the fed funds rate back to around 3.75–4.0% in 2025. If markets are right, and the U.S. Treasury yield curve eventually reflects its historical upward-sloping shape, that likely means the 10-year yield should remain around current levels. The spread between the fed funds rate and the 10-year Treasury yield has averaged around +1.1% in non-recession periods, meaning the 10-year yield, on average, has been higher than the fed funds rate by around 1.1%, albeit with a large range when not in a recession. [Fig.10] So, unless or until economic data starts to show signs of a sustained slowdown, the 10-year could fluctuate between 4.0–4.5% to start 2025. But if the economy does start to show signs of slowing, the Fed could cut rates more than what is priced in, which would mean the 10-year Treasury yield could get back into the 3.75–4.25% range to end the year, which is our expectation.

That said, the risk for the bond market is a Fed that cuts too aggressively into a still-growing economy, which could then potentially rekindle inflation concerns. Moreover, as it relates to the Donald Trump presidency, there is a concern that deficit spending (which would have likely happened under a Harris presidency as well) and tariffs could help growth but also keep inflationary pressures elevated. Better economic growth and perhaps a too dovish Fed, along with more policy details from the Trump administration, could push Treasury yields higher. It will likely take negative economic surprises for yields to fall meaningfully from current levels, so investors should continue to prioritize income opportunities, which remain plentiful…

…THE BOTTOM LINE Bond yields are expected to remain elevated, with the 10-year Treasury yield likely to remain in a range between 3.75–4.25% in 2025. Over the next 12 months, we see roughly equal upside and downside risks to yields as the markets grapple with the true impacts of budget deficits, increasing Treasury supply and the scope of the Fed’s current easing cycle. For fixed income investors, a focus on income generation and duration management is advised, and we believe the most attractive opportunities lie in the five-year maturity range.

… finally ahead of this mornings CPI …

where HOPE may not be a strategy, but those bidding on 10s today and bonds tomorrow (and betting on future rate CUTS), well, it may be all they got … THAT is all for now. Off to the day job…

https://youtu.be/B5iaV989_5M?si=20kTT6PYrrbAJgui

Andrea Bocelli - Angels We Have Heard On High