Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note …

First up, some ‘housekeeping’.

This will be last weekend offering until the new year and while regular weekly spammation will continue in the week just ahead, there will be a break after Friday morning (12/20) until early 2025.

It is with that in mind I’d like to extend a welcome to any / all those who’ve somehow stumbled upon this spot on the intertubes over the past days / weeks and months. I’d also like to offer a heartfelt thanks to those likely sources.

I’m humbled by it all and ESPECIALLY so, by all who have joined along from Ms. DiMartino Booth’s site … not quite sure how I’ve wound up on the radar screen but am grateful.

I’d ALSO like to thank others who’ve directed traffic here and specifically shouting out to those out there ‘huntin’ yield’, originally mentioned HERE …

… and for some MORE of the news you might be able to use…INCLUDING A NEW LINK TODAY (Yield Hunting) which I’d like to mention briefly … I’ve met the proprietor of this ‘Stack while back and its title speaks VOLUMES to me, “Yield Hunting”. After years on Global Wall where desks normally sell their own positions (buyer beware) and broker lots of things, IDEAS are always and forever, one of the most valuable of commods. This site most def worth a point / click and that said … some resources and curated links for your dining and dancing pleasure …

… It takes a village.

The intertubes is a large collective and as that saying goes, ALL opinions are created equally, it’s just that SOME — couple mentioned here, for example — are more equal than others (in MY view) and so …

Thank you Daily Feather and ‘yield hunter’ !!

And to all who are here because of them (or however it is you’ve arrived) … My wish and hope is that you find whatever it is you may be searching for!!

On THAT note, my humble ‘2 cents’ of macro gobbly gook begins with a weekly look at long bonds …

Support (TLINE) appears close at hand BUT momentum remains an open question and trading into years end typically more for amateurs than the pros.

Books are closed and duration, portfolios and duration exposures are likely about where they want to be and only ‘risk event’ in week ahead is, frankly, not that risky sounding. The Fed is gonna cut rates despite or because of the news …

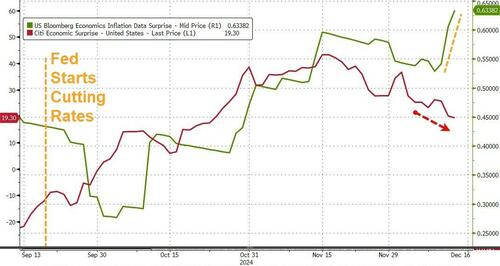

ZH: Stagflation Fears Spark Rate-Cut Rout; Tail-Risk Hedging Reaches Record High

…...as stagflation fears started to rise once again (inflation surprises soared while overall macro surprises disappointed for the fourth week in a row)...

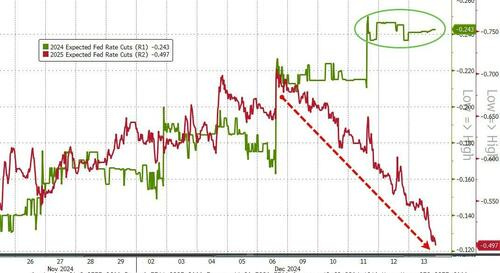

...and while a rate-cut next week is now a lock, the market is pricing in less than two cuts in 2025...

It should be no surprised that CPI, PPI, and today's Import/Export Prices are all re-accelerating as money supply has been pumping higher now for the last 18 months or so...

...and it appears bond vigilantes are well aware of it with the long-end of the curve soaring higher (yields) this week. Long-end yields are up for 6 straight days (+28bps is the fastest rise in yields since Oct 2023 - which marked the short-term peak in yields)..

… rate cut rout, bad breadth and stagflationary fears .. oh my …

Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use where THIS WEEKEND, a few things which stood out to ME from the inbox along with ALL things NFP recap and victory lap related …

The View: Sprinting to end 2024 Next week should still be busy. Price action is likely to be driven by: (1) the outcome of many central bank meetings (FOMC on Wed, BoJ, BoE, Riksbank and Norges on Thu), (2) soft data releases – esp. PMIs on Mon, and (3) preparations for Q1 supply.

…US: Trade 10y 4-4.5% with soft long bias; Dec FOMC risks hawkish tone. Stay short back end swap spreads w/ skepticism around de-reg & spending cuts …

…Bottomline: expect 10Y to be 4-4.5% & trade range with soft long bias. Dec FOMC unlikely to materially move markets but shift to slower cut pace risks sounding hawkish. ON RRP cut likely but low conviction & QT guidance welcomed. Stay short long-end spreads due to skepticism around big fin de-reg or large spending cuts.

… Technicals: 2024 cyclical bull lingers into 2025 US 10Y yield downtrend remains to =< 4%. If a repeat Jan-Feb 2024 double bottom forms, then 1H24 = 10Y to 4.70-5.00% by Memorial Day, then down to YE25.

…Since the start of November we’ve been looking for US 10Y yield to turn down from the trend line that has been guiding it lower since October 2023 at +/- 4.45% to about 4.05%. This is an important turn down because it implies wave E of the cyclical bull market is still underway with downside risks such as 3.75% maybe even 3.50-3.22%. A declining wedge pattern has implied a lower yield trend, but the impulsivity of the move higher in yield during Sept-Nov raises risk of a new pattern toward 5% in 1H25. For example, a test of +/- 4% and if a bottom pattern forms repeating Jan-Feb 2024, then it may mean 4.70-5.00% by Memorial Day 2025. This is what happened in 1Q24. Yield double bottomed at 3.80% and rose to 4.74%. Later on in 2H25 yields may fall.

… and more economically speaking, a different operation …

BARCAP: Global Economics Weekly The year ends mostly monetary

US Outlook The path of least resistance The November inflation estimates were a mixed bag, with another firm core CPI print and indications that November core PCE inflation is soft. We are revising up our GDP growth forecast amid stronger spending data. We expect the Fed to cut rates 25bp next week and indicate three cuts in 2025.

The November inflation estimates were a mixed bag, with core CPI registering its fourth consecutive solid 0.3% m/m increase, keeping the annual rate at 3.3% y/y, but the components of CPI and PPI translated into a soft 0.1% m/m (2.8% y/y) core PCE inflation print. Our Q4/Q4 forecast for 2024 core PCE inflation is 2.8%, about 0.2pp higher than the median FOMC projection in September.

In light of upwardly revised data on services consumption and solid spending around the Thanksgiving holiday, along with stronger carry-over effect and added momentum, we revise up our GDP growth forecast 0.5pp to 2.5% q/q saar in Q4 24 and in Q1 25.

Looking to next week's FOMC meeting, we expect a 25bp rate cut and Fed communication to signal that the committee intends to move more gradually toward a neutral policy stance. We expect the SEP to show stronger projections and the dot plot to indicate three 25bp cuts in 2025, although we retain our baseline projection that the FOMC will cut rates only twice next year amid sticky inflation, increased import tariffs and tighter immigration restrictions.

… BEST in the biz, literally just voted #1 in the inst investor poll and so when I say this is one to read a couple times, welp, I truly mean it … we’re all throwing darts and the same board, the institutional investor class continues to vote this operation as the best — think style and substance — and so, take that for whatever it’s worth …

… With the upper bound of policy rates now established in an ‘emergency’ hawkish context, investors can rest assured that more typical, pedestrian tightening cycles will be more contained. As a result, the range for 10- and 30-year yields has been well established and reinforces our assumption that investor demand will continue to emerge during any material backup in yields that puts 4.50% or even 5.00% 10s on the radar. The array of risks facing the US rates market in 2025 certainly won’t prevent bearish episodes and an increase in yields. If based solely on the seasonals, we anticipate the beginning of the year to be biased in favor of higher yields as green shoots and animal spirits create a temporary bearish underpinning for Treasuries. That being said, peak 10-year yields for the cycle have already been established and any subsequent selloff will conform with those parameters…

…A quick glance at the history of the 2s vs. EFFR spread since 2000 shows that the spread has been positive far more often than it has been negative. This trend was distorted by the Fed’s ZIRP that followed the Great Financial Crisis which implies less symmetry at zero than one should expect in the absence of hitting the lower bound for policy rates as the current cycle unfolds. We’ve been encouraged to see the pattern of EFFR capping 2-year yields persist as the Fed’s final move of 2024 is realized.

Going forward, the degree to which this trend will hold in 2025 will be determined by investors' confidence in the Fed’s ability to keep normalizing rates and not entertain potential hikes in 2026 or 2027. In light of our expectations for the Fed to categorize tariff-inspired pockets of realized inflation as simply a tax on the consumer, we would fade any attempt to push 2-year yields within striking distance of EFFR. Said differently, as a gauge of when 2-year yields are cheap, the 2s/EFFR spread is as good of a barometer as anything else we’ve come across at this point in the cycle.

… a former Bear Stearns economist weighs in with a weekly note and a chart / point raised made ME pause …

… Furthermore, the easing in financial conditions since the Fed began cutting rates also brings into question the restrictiveness of monetary policy. For example, the Chicago Fed’s National Financial Conditions Index points to the easiest financial conditions in early December since July 2021.

Nevertheless, with interest rate futures markets putting the odds of a quarter-point rate cut on Wednesday at 98%—in large part due to the guidance of some policymakers—anything other than a quarter-point cut would be a shock. However, we suspect there will be policymakers in the meeting next week making similar arguments as ours about policy possibly not being particularly restrictive and, therefore, the Fed should take a cautious approach to further policy easing, especially given stalled inflation progress. We would be surprised if the vote to cut rates next week is unanimous, and we expect some non-voting FOMC participants will also voice their discomfort with the degree of rate cutting, given the lack of support for these actions from the data, in the coming weeks…

This outlook presents our forecast for UST and SOFR rates next year as well as expectations for Fed QT, funding markets, UST supply-demand, swap spreads, and inflation breakevens. We see rates as likely to be driven by a wide range of shifting policies that are, as of now, exceptionally uncertain.

The forecast assumes modest fiscal easing, higher tariffs, and deregulation leading to stronger growth, lower unemployment, and higher inflation than previously expected, in-line with US Econ’s outlook. Against that backdrop, after cutting at the December meeting we expect the Fed to hold rates unchanged next year before moving to neutral of 3.75% in 2026. Elevated deficits and lingering inflation pressures should boost term premia.

Based on these fundamentals, our outlook for duration is bearish, with swaps and USTs projected to realize 25-50bp above current market pricing and 10y UST peaking at 4.75%. About half of the gap to market pricing (as of 12/12) is due to our forecast of a higher neutral rate with the rest coming from the projected rise in TP. Similarly, our curve forecast is steeper than forwards out to 10y. Conviction in the forecast is tempered by what we see as exceptional uncertainty around the details and timing of tax, spending, tariff, immigration, regulatory, debt limit, and debt management policies…

…In short, we are bearish on duration, with the 10y UST peaking at 4.75% and yields across the UST and SOFR curves projected to be 25-50bp above current forward pricing. We expect the main catalyst for our view to be a realization that inflation and labor market conditions warrant a more restrictive Fed path than currently priced…

… here’s a 2025 outlook with a ‘bold call’ which caught MY attention and worth further research as it details an oldy but a goody — a tool not seen in DECADES … oh, wait, nevermind …

… Three calls for the global economy: Inflation waves and investment demands

…Call 2: Inflation will come in shorter but more frequent cycles

…Our bold call: Yield curve control as result of higher debt Debt-funded investments in the Western world could easily bring back debt sustainability concerns in the eurozone and the US. With much higher inflationary pressures than in the 2010s, central banks cannot go all-in with highly accommodative monetary policies across the board. The lower bound for interest rates will be higher this time around than in the 2010s.

Still, as the longer end of the curve is critical to mortgage and corporate borrowing costs, when push comes to shove, both the Federal Reserve and the European Central Bank could be forced to tackle elevated bond yields, trying to square the need for investment with price stability. This could lead to a new discussion on yield curve controls in the US and the eurozone, eventually forcing both central banks to start buying longer-dated government debt again. The ECB already has an instrument for it: the Transmission Protection Instrument (TPI). They might have to use it earlier than they had ever thought.

… from controlling of curves to entertaining idea Fed may be done (after this coming week?)

MS: A Slower Pace Already? | Global Macro Strategist

Throwing data-dependent caution to the wind, investors seem assured of an FOMC meeting that signals a reduction in the pace of rate cuts next year. The pace of rate cuts may slow in the end, but market prices already reflect that outcome – leaving risks skewed toward a message of measured continuity.

…Interest Rate Strategy United States We discuss the upcoming FOMC meeting and think that investors will focus on three things: the 2025 dots; Powell's characterization of the likely pace of rate cuts in 2025 and its implication for the January 2025 meeting; and the decision on the overnight reverse repo facility rate. We think some investors have "shrugged off" encouraging inflation data and instead have focused on Fed-speak. Therefore, if there are few references to a reduction in pace, investors may be more comfortable with a January cut.

We think softer housing inflation will give the Fed more confidence that the disinflation trend remains intact and keeps them on a path to deliver consecutive rate cuts at the next two policy meetings. We continue to suggest investors position for a higher market-implied probability of a 25bp rate cut at the January 29 FOMC meeting via being received fixed January FOMC OIS or long the FFG5 contract.

As we are neutral overall on duration and the curve, we suggest investors receive the belly of the 3s7s30s PCA weighted SOFR swap fly to benefit from momentum and technical signals. The trade additionally has attractive properties such as positive carry.

…The MACD technical indicators also support receiving the belly of this fly. The MACD line is below the indicator line, which denotes a good time to position for a belly richening. Additionally, the MACD line is about to turn negative – another momentum signal that would work in favor of this trade.

… from the covered wagon operation a snappy title on a weekly …

United States: Sticky Inflation, Sticky Wicket for the Fed…

…Interest Rate Watch: A Year in Review for Rates: Exiting Inversion … Looking ahead to 2025, we expect next week's FOMC meeting to include signals from policymakers that the pace of rate cuts will be slower going in the year ahead. We project three 25 bps rate cuts from the FOMC next year, and financial markets are priced for a similar outcome. These rate cuts may put some additional downward pressure on shorter-term rates, similar to what occurred this year, but we do not anticipate a major decline in longer-term interest rates. Our forecast for the 10-year Treasury yield at yearend 2025 is 4.00%, not too much below the current spot rate of 4.37%.

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW … Batting in the lead off spot is the question nobody’s asked …

… rate CUT comin in week ahead but what ‘bout year ahead? This next note and visual stood out to me as it reminds ME of what another of Global Wall’s popular kids called BONKERS …

Apollo: 2025 Economic Outlook: Firing on All Cylinders

The US economy has charted its own path in the post-pandemic world and is expected to continue to do so in 2025. Why? First, the economy has proven much less sensitive to interest rate hikes than in years past. Second, the US is experiencing a surge in corporate and research spending on the back of the Artificial Intelligence (AI) boom. And third, fiscal policy has been much more stimulative than anywhere else in the world. We see strong GDP growth, moderate unemployment, and persistent inflation in 2025. We believe the Fed will lower interest rates at a slower pace than the market expects.

…How strong are corporates? If we were only given space for one chart to answer this question, it would be Exhibit 23. American businesses are in the midst of an historic profit boom.

As is the case with the aggregate consumer picture, corporate profits, as a whole, have not felt the pinch of Fed rate hikes to any remarkable degree. To be sure, firms with weak earnings, weak revenue, and weak cash flows have been hit by Fed hikes. But from a macro perspective, the effects of Fed hikes on corporates have been small…

… and while i don’t normally believe all I see on the intertubes, this tweet verified as it was a bad week for the bond market …

The bottom line: One can reasonably debate whether the stock market has risen exponentially but there is no arguing that the surge in the S&P 500 these past two years has been nothing short of extraordinary. And it has clearly gone much further than I thought it would, especially in these past twelve months, and so at this point, it is worth the time and effort to discuss and interpret the message from the market; tip the hat to the bulls who have, after all, been on the right side of the trade, and provide some rationale behind this powerful surge. This is not some attempt at a mea culpa or a throwing in of any towel, as much as the lament of a bear who has come to grips with the premise that while the market has definitely been exuberant, it may not actually be altogether that irrational. Read on…

… Turning a Bit More Positive on Bonds Too As for the bond market implications, this is a wash: higher productivity growth ipso facto means a higher real interest rate, but it also means lower inflation expectations. It is extremely difficult at the present time to statistically determine which one will dominate the other, but there is no doubt that higher productivity growth reduces business costs, improves margins, and is a structural positive underpinning to the stock market. This has never been a point of debate with me, but I come back to this significant point, which is that this is what investors are pricing in: the future, and not just 2025 and 2026, but the next decade. Again, this is not abnormal in the context of an inflection point in the technology curve, and we will only likely find out in the course of time whether or not what we are experiencing today is indeed a true bubble. This is where my thinking has changed. I have shifted from my view that we are in a classic bubble to now questioning — not totally abandoning, but indeed questioning — that thesis.

… and as you may / may not know by now, I’m a big fan of visuals and here’s a great source as pictures, they say, are worth a thousand words …

Spectra Markets: Sticky Prices Q1 2025 is looking rather binary.

…Interest Rates

The US 2-year yield is imitating a beach ball under water as NFP, CPI, and Initial Claims data all tried to submerge it, but it snapped back higher thrice.

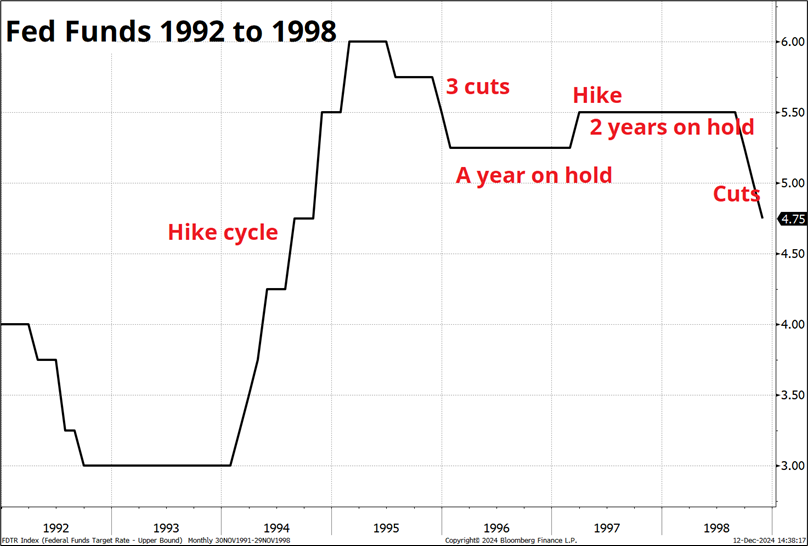

I think that yields have sniffed out the fact that inflation remains way too sticky and further Fed cuts are not justified. The FOMC will cut next week just because it’s priced in, but then you can be open to the idea that there might not be another Fed cut for a long time. A small mid-cycle adjustment like this is not unheard of. It happened in the late 1990s.

There are enough similarities between the 1995 soft landing and the 2023/2024/2025 soft landing to think that “Fed on hold for all of 2025” is a scenario worth considering, if not the base case.

Elsewhere around the world, the ECB cut 25 as expected, the Bank of Canada cut 50 as expected, and the Swiss National Bank cut 50bps as expected by some people, but not by me. The currency didn’t respond much, and the SNB remains trapped in a situation similar to the one faced by the Bank of Japan before Abenomics: Strong currency + low inflation + no credible weapons.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Wishing one and all very merry merry xmas, happy holidays and a happy / healthy new year!! Hope 2024 treated you well and 2025 is to be your collectively BEST EVER.

THAT is all for now. Enjoy whatever is left of YOUR weekend …

Hold steadfast Rosie! The capitulation of a noteworthy Bear is a contrary indicator imho....was fondly remembering your offer of Free Snow Shoveling Lessons as I was helping my friend in Truckee shovel for 3 hrs Thurs night. Hey bed & breakfast at my skiing mentor's place ain't free! Enjoy your break & holiday thanks for always increasing my knowledge & providing Funtertainment! May you and yours have a wonderful Christmas & holiday. Rest up 2025 likely to have many curveballs!

Hold steadfast Rosie! The capitulation of a noteworthy Bear is a contrary indicator imho....was fondly remembering your offer of Free Snow Shoveling Lessons as I was helping my friend in Truckee shovel for 3 hrs Thurs night. Hey bed & breakfast at my skiing mentor's place ain't free! Enjoy your break & holiday thanks for always increasing my knowledge & providing Funtertainment! May you and yours have a wonderful Christmas & holiday. Rest up 2025 likely to have many curveballs!

Merry Christmas, Happy Hanukkah and Happy Holidays to all !!