Good morning … Before DJT (TIME Person of the YEAR) rang the opening bell yesterday at the NYSE …

ZH: ECB Cuts Rates As Expected, Euro Tumbles After Reference To "Restrictive Policy" Is Dropped

… THEN more domestically focused …

ZH: Producer Price Inflation Comes In 'Red Hot' In November ZH: Jobless Claims Explode Higher In First Week Of December

… apparently none of this — OR the current concession mentioned HERE — mattered at least as far as the days liquidity event was concerned …

ZH: Yields Spike To Session High After Ugly, Tailing 30Y Auction

… in as far as yields SPIKING to highs after yesterdays liquidity event it’s also worth some context AND a picture … First some context from a large German operation …

…The other release of potential concern were the weekly jobless claims, which saw initial claims at 242k over the week ending December 7 (vs. 220k expected), above every economist’s expectation on Bloomberg. Continuing claims for the previous week also surprised to the upside (1886k vs 1877k expected), though data may have been distorted by seasonal factors post-Thanksgiving. And while Treasuries initially rallied following the US data, the bond sell-off that has dominated so far this week resumed as the day wore on. By the close, 2yr (+3.9bps) and 10yr yields (+5.7bps) both posted a fourth consecutive increase to 4.19% and 4.33%, respectively. This leaves 10yr yields on course for their biggest weekly rise since early October (+17.5bps so far).

… AND it is on THAT note I’ll pause to add some context in as far as that BIGLY weekly rise in 10s …

… I’ve taken liberty to highlight October rise for some context and at same time note we’re approaching ‘support’ up nearer 4.35% … This is how we begin the end of the week and on a Friday the 13th, no less … I’ll quit while I’m behind and move right along TO a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries saw small buying at the Tokyo cash open, liquidity remaining scant with the market rangebound until a small selling wave was seen in London hours with energy prices rising (CL +1.1%) and risk-on moves in peripheral spreads (FR-GMY -2bps). German intermediates are leading the modest down-trade, with UK Gilts outperforming after a softer GDP report for October. The 2s10s curve is -0.5bps and S&P futures are showing +19pts here at 6:45am, with USDJPY +0.6% and Gold down -0.5%.

… and for some MORE of the news you might be able to use …INCLUDING A NEW LINK (mentioned YESTERDAY) and which I’d like to touch on once again, briefly … I’ve met the proprietor of this ‘Stack a while back and its title spoke VOLUMES to me at the time, “Yield Hunting”. After years on Global Wall where desks normally sell their own positions (buyer beware) and ‘broker’ lots of things (take an extra “+”, non-risk … so, extra credit!!), IDEAS are always and forever, one of the most valuable of commods. This site worth a point / click and that said … here are some resources and curated links for your dining and dancing pleasure …

NEWSQUAWK: Risk sentiment improves with havens on the backfoot, DXY around 107.00 … Fixed benchmarks in the red post-ECB and ahead of a blockbuster week … USTs are steady overnight with specifics light and the docket ahead also limited as the countdown to the FOMC begins. Action in the European morning limited to a 110-09+ to 110-14 range. Yields little changed overall with no overt flattening/steepening bias thus far.

Opening Bell Daily: $1 trillion boom … One of the oldest products on Wall Street just secured a $1 trillion year … Hype around bitcoin and investing veterans like Tom Lee and Jeremy Grantham fueled record ETF inflows in 2024.

Reuters Morning Bid: Wall St near records as central banks end 2024 with rate cuts

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use … here’s SOME of what Global Wall St is sayin’ … a small bit of curated links making the rounds, hitting inboxes and updating of narratives … lots of which is commentary ‘bout the ECB and the SNB …

First up some thoughts on ECBs step on the path towards ‘normal’

The ECB cut its key policy rates by 25bp, taking the deposit rate to 3%. The move was widely expected and priced in by financial markets. The communication around the rate cut suggests that the Governing Council is comfortable with the idea of bringing policy rates back to neutral levels, if its outlook continues to be confirmed.

The ECB trimmed the deposit rate by 25bp and replaced the "sufficiently restrictive" tightening bias with a focus on setting an appropriate monetary stance, while remaining non-committal on future rate decisions. We continue to expect consecutive 25bp cuts until June.

…France weighin in on the ECB, SNB and on US and US rates …

The decision and accompanying communications at the European Central Bank’s December meeting reinforce our view that the Governing Council will continue to vote for a 25bp rate cut at each meeting until a more neutral policy setting is achieved.

The March meeting is a clear focus point, given potentially more clarity on some key uncertainties, and the fact that another cut then would take the policy rate to the higher end of neutral estimates.

We continue to see the ECB cutting until 2% is reached in June 2025, which is the middle of our estimated neutral range. Risks are skewed towards the ECB needing to take policy into accommodative territory, should the data weaken by more than we expect.

Rates: We would see a further rebound in yields as a good opportunity to re-enter long duration positions.

FX: We think EURUSD trends lower over the next twelve months due to policy divergence. However, with the passing of this catalyst we wait for opportunities to sell rallies in the EUR.

We see today’s 50bp rate cut and updated guidance by Switzerland’s central bank as implying a faster route to the 0.25% terminal policy rate we already expected, rather than a sign that it will go even lower.

We now see the SNB reaching that destination with a 25bp cut at its March policy meeting. That said, the balance of risk to our terminal rate forecast is to the downside, particularly if recent rate cuts are not sufficient to curb CHF strength.

FX: We take a small profit (0.34%; USD17k) on our EURCHF long given the lacklustre reaction in FX to today’s 50bp cut (spot ref: 0.93220; GMT 13:05)

We expect the FOMC to cut rates by 25bp at next week’s meeting, bringing the fed funds range down to 4.25%-4.50%.

Chair Powell will likely use the press conference to open up optionality for a pause in further easing of undefined length.

We view Fed officials as struggling to make (and discuss) monetary policy without being drawn into a debate about President-elect Trump’s potential economic policies. We think Powell will continue to refrain from any direct comment here, but the FOMC will make policy consistent with management of elevated inflation risks.

…USD rates: We see UST yields heading lower in Q1 to reprice a slowing growth path as markets incorporate the combination of hawkish tariff and immigration policies and modest fiscal impulse. In H2, the imposition of significant tariffs will likely raise inflation expectations, probably keeping the Fed on hold. This, coupled with increases in coupon supply, should push yields higher, in our view…

…USD rates: Growth-inflation tussle into 2025 We see Treasury yields heading low er in early 2025, before eventually moving higher in H2. 10y yields will likely end Q1 at around 4.10% and rise to 4.65% by year end.

Repricing the Red sweep: Our projection sees Treasury yields reprice to a cooler growth path in early 2025 as investors seek to incorporate the combination of hawkish tariff and immigration policies and a potential modest fiscal impulse from tax cuts, reversing the higher grow th expectations built around the Red sw eep outcome in Q4 2024. At the same time, inflation expectations should start to rise, which w e think could create favourable conditions to own TIPS in Q1 2025.

Higher yields with a Fed on hold: In H2 2025, the imposition of significant tariffs by the Trump administration will likely raise inflation expectations, both for investors and for the Fed. We think these conditions will mean the Fed not only keeps rates on hold in H1 2025, but through to the end of H2 as well.

Additionally, w e see rising Treasury coupon issuance in August driving term premium expansion, sending yields higher through H2 2025. Our current estimate is for the market to absorb close to USD2.1trn in net coupon supply next year, the highest on record. Fed balance sheet normalization is also set to continue next year (w ith QT ending in March), w hich should continue to push Treasury funding costs higher.

Breakevens should w iden through 2025 as real yields move low er or sidew ays, caught betw een a cooling grow th path and a hawkish Fed.

We see risks skew ed toward low er yields than in our base case. The Fed could continue to cut if potential dow nside growth effects from tariffs and immigration policy dominate, driving yields lower.

… a note from Germany on the ECB (and another on Da FED) …

DB: ECB Reaction: More easing ahead with maximal optionality

As expected, the ECB cut policy rates a further 25bp to 3.00%. Several Council members proposed a 50bp cut, but in the end there was unanimous support for the fourth quarter-point cut in this cycle. Also as expected and consistent with heightened uncertainty, the ECB dropped its inherently hawkish guidance and adopted more neutral language. This gives the ECB maximal optionality going forward on the timing, pace and destination of policy.

Our interpretation of the changes to the statement is that there is now an implicit easing bias. The bar for a 50bp cut at the next meeting in January feels high, but a larger cut or cuts beyond January cannot be ruled out. A group on the Council is already proposing 50, the policy stance is still restrictive, tariffs have not been factored into the ECB forecasts yet and the new language allows for the possibility of rates having to fall below neutral – which is far from the current level of rates.

If we are right about below trend growth and below target inflation, then we are on course to see sub-neutral policy rates in 2025. Our baseline is a 1.50% terminal rate at the end of 2025, achieved in 25bp increment cuts. 50bp cuts remain a risk, in our view. Macro uncertainty is high and we continue to emphasize a terminal rate landing zone of 1.00-1.75%.

Finally, we ask our AI tool to grade the degree of hawkishness of the ECB press conference statement. We present two complementary measures of hawkishness. The difference between the two may be a way of interpreting an underlying policy bias. Our AI tool says that ECB hawkishness dropped to the lowest level since before the hiking cycle, but there was no underlying policy bias in December. That is, the AI finds no signal beneath the surface consistent with an imminent 50bp cut

DB: Fed Notes - Do actions speak louder than words on neutral?

Recent Fed communications have indicated that the neutral policy rate has risen. Chair Powell emphasized this view in September, noting that r-star may be "significantly" above pre-covid levels. The upward migration of the long-run dot in the SEP – a trend we expect continues next week – confirms this signal.

In contrast, we show that the short-run neutral policy rate backed out of the Fed's median projections for the economy has fallen substantially over the past year.

… interrupting ECB talk with some words on PPI …

First Trust: The Producer Price Index (PPI) Rose 0.4% in November

The Producer Price Index (PPI) rose 0.4% in November, coming in above the consensus expected increase of 0.2%. Producer prices are up 3.0% versus a year ago.

Food prices surged 3.1% in November, while energy prices rose 0.2%. Producer prices excluding food and energy rose 0.2% in November and are up 3.4% versus a year ago.

In the past year, prices for goods are up 1.1%, while prices for services have increased 3.9%. Private capital equipment prices rose 0.4% in November and are up 3.6% in the past year.

Prices for intermediate processed goods were unchanged in November but are down 0.5% versus a year ago. Prices for intermediate unprocessed goods increased 0.6% in November but are down 1.9% versus a year ago.

… The direction of inflation moving forward is very likely to be dictated by 1) the services side of the economy, which suffered heavily during the COVID shutdowns but has since returned to the forefront and 2) changes in the money supply, which, after surging in 2020-21, peaked in early 2022. Although the M2 measure of money has been rising gradually since last November, it’s still down from the peak in April 2022. An epic battle to stem government spending is likely to unfold in Washington next year, and there is a very real risk that the Fed could get overly aggressive in cutting rates if a pullback in federal spending temporarily results in slower economic growth. In turn, lower interest rates could fan the embers of inflation, re-igniting the fire that the Fed has spent the last three years trying to extinguish. On the labor front this morning, initial jobless claims rose 17,000 last week to 242,000. Meanwhile, continuing claims increased 15,000 to 1.886 million. These figures are consistent with continued job growth in December, but at a slower pace than earlier this year.

The European Central Bank cut by 25bp as widely expected but EUR rates moved higher coming out of the press conference with the belly underperforming. Lagarde sounded more balanced than a central bank geared to supporting growth if pressed. Up next is the Fed next week. We look at a technical adjustment in the works for the Fed’s reverse repo rate

ING: Fed set to cut 25bp but to signal a slower, shallower path ahead

The Federal Reserve is expected to cut rates by a further 25bp on 18 December as it continues to move policy from restrictive territory to somewhere closer to neutral. However, with inflation remaining sticky, and President-elect Trump looking to strengthen the US growth performance, the Fed is set to signal a more cautious policy easing profile for 2025

… Keep an eye on their new economic forecasts though with President-elect Trump’s policy thrust of immigration controls, tariffs and personal and corporate tax cuts likely to mean the Fed signals a shallower, slower path of easing through 2025.

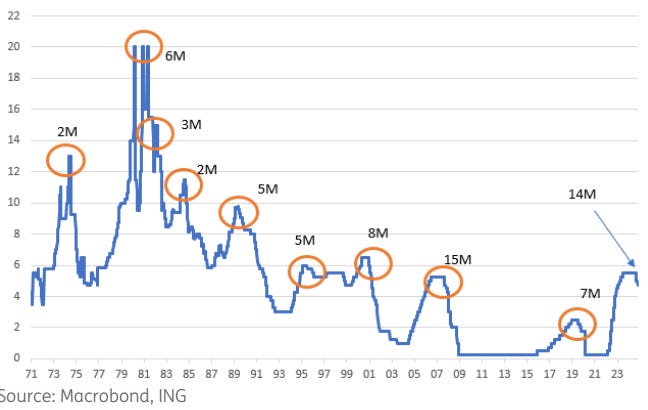

Fed funds target ceiling rate (%) with duration between last rate hike and first rate cut 1971-2024

Three 25bp cuts in 2025 Up until recently, the market had been fairly split on whether we would indeed get a rate cut in December. Inflation data has not been making any real progress towards the 2% target on the CPI methodology. Four consecutive 0.3% month-on-month prints are far too hot for comfort. However, there has been better news on the Fed’s favoured measure, the core personal consumer expenditure deflator. Key components from the CPI and PPI reports that feed through into this broader measure of inflation pressures offer encouragement of a favourable 0.2% MoM print when released on 20 December.

The Fed’s dual mandate means that it also needs to pay close attention to what is happening in the jobs market. Clear signs of cooling with payrolls growth slowing, full-time employment actually falling and unemployment shifting higher justifies the Fed moving policy closer towards neutral. With 23-24bp of a 25bp cut priced into futures contracts, it looks a done deal…

… AND yet MORE on DEC CUT …

MS: US Economics & Global Macro Strategy: FOMC Preview: December Meeting

Given the recent data flow, we expect the Fed to cut by 25bp. Chair Powell is likely to sound confident on disinflation but be cautious on removing policy restriction. Our strategists stay neutral on UST duration and curve shape, and maintain long MBS basis.

Key expectations

The FOMC cuts the fed funds rate by 25bp to 4.25-4.50%. Inflation continues to point to disinflation and the labor market has cooled.

We project minimal changes to the FOMC statement. The statement has taken a backseat to other forms of communication over time.

We expect the median of the dot plot to project four 25bp rate cuts in 2025 and one 25bp rate cut in 2026. Risks lie in the direction of fewer cuts.

In the press conference, Chair Powell is likely to sound confident on disinflation while saying the Fed will be more cautious in removing policy restriction.

Our rates strategists suggest investors remain neutral on US Treasury duration and yield curve shape, but remain positioned for a 25bp rate cut at the January FOMC meeting.

Our FX strategists expect the FOMC meeting to be a USD-negative catalyst, and recommend long AUD and long GBP positions.

On the agency MBS side, our strategists remain long the mortgage basis and prefer buying production coupon Ginnies and conventionals…

MS: US Economics Weekly: Disinflation supports cautious cuts

Uncertainty about fiscal, trade, and immigration policies continues to cloud the outlook. In the meantime, the positive signal in November inflation data will provide ample room for the Fed to cut in December. The Fed is likely to be more circumspect about what happens after that.

Key takeaways

A downshift in shelter inflation in the November CPI report should reduce concerns that progress on inflation is stalling out.

A 25bp rate cut in December is baked in the cake. The Fed will communicate more cuts are coming, but the question is when and how many.

We expect retail sales rose by a solid 0.5% m/m in November. Labor market income continues to outpace inflation and household net worth is surging.

…it’s all BONKERS you say? maybe so and on THAT theme …

SocGEN: Global Strategy Weekly And the award for the most bonkers chart of the year goes to…(drumroll)…

Yes, ladies and gentlemen, after another extraordinary year for markets, my award for bonkers-on-stilts goes to the continued surge higher in US profit margins.

There has been much comment recently on the extent (or not) of the US stock market ‘bubble’, especially now the US equity market’s share of world market capitalisation has hit an extraordinary 75% (see chart in last GSW here).

Following on from that observation, an FT Opinion article this month entitled The mother of all bubbles: The US has never been so overhyped, relative to the rest of the world caught my eye (as you can imagine). To quote Ruchir Sharma “This is not a bubble in US markets, it’s mania in global markets. At the height of the dotcom bubble in 2000, US stocks were more expensively valued than they are now. But the US market did not trade at nearly so vast a premium to the rest of the world. Nor is this just AI mania by a new name. On indices that weight stocks equally regardless of size and correct for the domination of Big Tech, the US has outperformed the rest of the world by more than four to one since 2009.” – link.

But as Shama also notes, “…some of the premium is rational. Compared to Europe and Japan, the US economy is growing faster.” Indeed, it is easy to rationalise the US valuation excess. We all know the arguments because we hear and read them almost every day. In essence, the argument is that US stocks deserve a huge premium because profits are growing much faster in the US than in any another major economy, a trend likely to continue given its dominance in tech related companies. That makes some sense - even to a bear like me!

But one simple driver of the success of US inc is often overlooked. The US government deficit since Covid has remained super expansionary at around 7.5% of GDP in 2023, 2024 and forecast for 2025 (IMF data). This compares to the eurozone and even Japan (for example) with deficits of ‘only’ 3% of GDP. That’s a big gap.

We think many investors widely under-appreciate how crucial US fiscal dysentery is as the propellant of far superior US profits growth which in turn ‘justifies’ far higher equity market valuations. It is much ‘sexier’ to latch onto a story around US corporate exceptionalism in tech. Understanding the true (fiscal) source of US corporate superior profits growth gives us a handle on figuring out just how sustainable the US equity bubble is.

… Swiss weigh in (on the ECB and SNB) …

UBS: Swiss economy: SNB accelerates the easing pace

The Swiss National Bank (SNB) lowered its policy rate by 50bps to 0.50%, a larger move than expected.

We keep our forecast of an additional rate cut in 2025, bringing the policy rate down to 0.25%, and revise our inflation forecast down to 0.5% for 2025.

While a negative policy rate appears unlikely, it is no longer off the table. Should further monetary easing be necessary, the SNB may prioritize foreign exchange interventions before resorting to negative rates, in our view.

The ECB's decision to cut its main policy rate by 25bps was in line with expectations, even if some investors saw grounds for a larger move amid concerns about the economic outlook.

ECB staff downgraded their projection for economic growth, but they still expect a return to trend next year. The forecast for inflation was also lowered in the near term, with inflation expected to stabilize around its 2% target toward the end of 2025.

The market's reaction to the cut was muted. With investors already pricing in a steep cutting cycle, the bar for further dovish surprises is high. Still, with yields elevated we recommend investments in diversified medium-duration investment grade bonds and equity income strategies to enhance yields and benefit from diversification.

… AND again, interrupting ECB, SNB recap / victory laps for a look at DECEMBER with a DOWNGRADE (so, supportive of rate CUTS …)

We have revised our economic forecast for next year lower in light of the higher likelihood of new tariffs in 2025. Tariffs imposed during President Trump’s previous administration were met with retaliation from our trading partners, a combination apt to depress exports, real incomes and consumer spending. We assume that new tariffs will go into effect in the second half of next year, at which time we expect economic momentum to downshift.

Growth appears likely to pick up in 2026 once the initial impacts of the tariffs fade and the full suite of Republican policy changes go into effect. Specifically, the economy would receive a boost from a lighter regulatory touch and the prospect of additional modest tax relief for households.

Absent tariffs, the jobs market is already trending softer. Payroll growth is highly concentrated among industries and labor force growth has slowed considerably. Although the unemployment rate remains low, there is clear upward movement in the number of permanent job losers and the median duration of unemployment, trends that have historically predated recessions.

Meanwhile, dis-inflation is proceeding at a frustratingly slow pace. The Fed’s preferred inflation gauge has been more or less unchanged for the past six months amid a slowdown in goods deflation and still-firm price pressures in the services sector. The Consumer Price Index came in above expectations in November, but with an encouraging deceleration in services inflation.

Incoming inflation data likely warrant further Fed easing, but at a slower pace. Although new tariffs would trigger a temporary reacceleration in inflation, we suspect that the FOMC will disregard the inflationary bump and more heavily prioritize the tariff-driven hit to GDP and job growth. We anticipate that the FOMC will enact another 25 bps cut at its December meeting and then switch to an every-other-meeting cadence with cuts in March, June and September 2025, leaving the federal funds rate within a target range of 3.50%-3.75%

Wells Fargo: European Central Bank Maintains Steady Easing, Swiss National Bank Accelerates

Summary

The European Central Bank (ECB) lowered its Deposit Rate by 25 bps to 3.00% at today's monetary policy announcement, and the accompanying statement was noticeably dovish in tone. In particular, the ECB's medium-term forecasts for underlying inflation were slightly below the 2% target, and the central bank removed its pledge to keep policy rates "sufficiently restrictive for as long as necessary” to return inflation to target.

Overall, we view today's announcement as consistent with and supportive of our outlook for continued steady rate cuts from the European Central Bank. Our base case remains for 25 bps rate cuts in January, March, April and June, with a final 25 bps rate cut in September, for a terminal ECB policy rate of 1.75%. The announcement opens the door to a possible 50 bps rate cut during early 2025 if Eurozone growth and inflation were to prove especially weak.

The Swiss National Bank (SNB) surprised market participants by delivering a 50 bps reduction in its policy rate to 0.50%, citing a decrease in underlying inflation pressures. Given the outlook for further ECB easing and the potential for upward pressure on the franc, we expect the Swiss National Bank to cut rates again by 25 bps to 0.25% in March.

… finally, Dr Bond Vigilante talking about … bonds and their vigilantes …

After today's PPI, we won't be surprised if Fed officials plant a story in The Wall Street Journal over the weekend titled something like "Fed Officials Might Vote To Pause Rate Cutting Following Hot Inflation Data." The current consensus seems to be that the Fed will cut the federal funds rate (FFR) by 25bps on December 18. But it might be a "hawkish cut" with the FOMC's Statement and Summary of Economic Projections signaling a pause in rate cutting early next year.

If so, then Fed Chair Jerome Powell will amplify that signal at his December 18 presser. He certainly sounded somewhat less dovish on November 14 when he said, "The economy is not sending any signals that we need to be in a hurry to lower rates. The strength we are currently seeing in the economy gives us the ability to approach our decisions carefully."

The FFR futures market currently is anticipating a 25bps cut next week and two more similar cuts next year (chart).

The Fed cut the FFR by 75bps since September 18. Two days before that happened, the 10-year US Treasury bond yield was 3.62% (chart). It has increased 70bps since then to 4.32% today. We anticipated that the Bond Vigilantes might fight the Fed because the economy is strong and inflation might stop moderating north of 2.0% because the Fed is easing too much, too soon. Another rate cut next week might push the bond yield higher, again.

… And from Global Wall Street inbox TO the WWW … a former Fed INSIDER ...

Bloomberg: The Fed Can’t Ignore All of Trump’s Intentions By Bill Dudley, Columnist

… I expect the median projection to entail slightly stronger growth in 2025 and 2026 compared with the September median forecast, reflecting persistent momentum in the economy and a higher productivity growth trend. The unemployment rate will remain slightly above the level that Fed officials judge consistent with stable inflation. Inflation will decline to the Fed’s 2% objective, most likely in 2026. By 2026 or 2027, the federal funds rate will fall to what the Fed sees as the neutral level consistent with 2% inflation. This path will likely involve just 50 to 75 basis points of rate cuts in 2025 (compared with 100 basis points in the September 2024 projections), and a slightly higher neutral rate — probably 3% or more, but considerably below the level that futures prices currently imply.

The underlying narrative will be the same as in September: As the labor market loosens and inflation recedes, monetary policy will gradually move from restrictive to neutral, likely achieving a soft landing. When the Trump administration’s tariff and deportation policies come into focus, that outlook may become less rosy.

…Collectively, the technical evidence does not mean a top on the CCMP is near but suggests investors should consider tactically buying dips within the longer-term rising price channel vs. chasing this latest breakout. In the event of a pullback, support for the index sets up at the 20-day moving average (dma), the recent November highs (19,287), and near the July highs (18,674).

Round numbers such as 20,000 can act as important milestones and psychological reference points, often making them key support and resistance levels to monitor. They also serve as a benchmark for progress, with investors usually comparing them to previous milestones. In the bar chart below, we highlight this progress based on the number of days for the Nasdaq to double, dating back to 1974. It took the index 1,644 days to double from the 10,000-point milestone to the 20,000-point milestone. While this may sound like an extended period, it is in line with the median number of days to double (1,687) — not to mention significantly shorter than the 7,397 days for the index to double from 5,000 to 10,000 during the March 2000 to June 2020 period….

… MORE on ECB …

NORDEA: ECB Watch: Still restrictive, but not for long

The ECB cut rates by 25bp, but now sees inflation risks more two-sided. More rate cuts lie ahead, but the ECB still seems to be on a path of normalisation and does not appear to be in a hurry on that path. We still see the bottom of rates at 2.25%.

The ECB cut rates by 25bp and dropped the pledge to keep rates restrictive for as long as necessary.

The reaction function was kept unchanged.

Lagarde emphasised that a lot of ground had already been covered with the four rate cuts delivered, suggesting the room for further cuts could be limited.

Growth forecasts were revised down.

… on another source of demand … the consumer and their confidence …

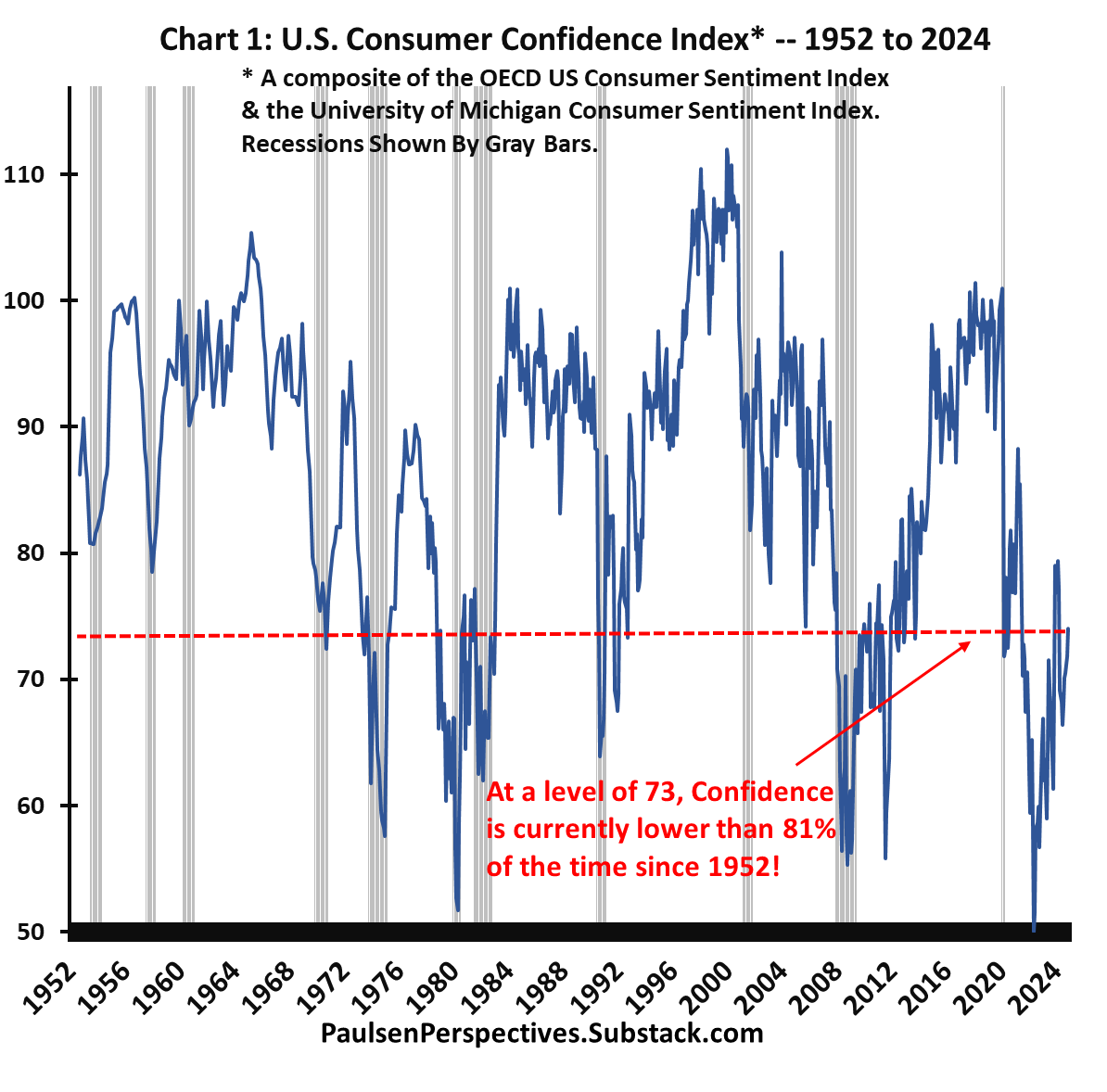

Paulsen Perspectives: The BIG Untapped Asset -- Confidence Don’t underestimate the power of something we have not yet witnessed in this recovery/Bull market cycle – the potential emergence of “Animal Spirits”!

…Main Street confidence is a dominant factor in every economic expansion but has proved particularly meaningful in the cotemporary recovery. Normally, as demonstrated in chart 1, confidence collapses during recessions and then revives once a new economic expansion begins. However, since the 2020 pandemic recession, U.S. confidence has never really recovered. After more than four years since the last recession and over two years since the last Bear market, Main Street confidence remains lower than 81% of the time since 1952. Unique to the post-war era, the post-pandemic economic expansion and its corollary Bull market have yet to revive U.S. confidence.

This is unfortunate because confidence may be the biggest economic & Bull market weapon in the arsenal. Typically, the degree of improvement in Main Street confidence plays a huge role in the success of the economic cycle and the size of returns for equity investors. But fortunately, since this asset has not yet been tapped, if something or someone could boost U.S. cultural sentiment, both the performance of the economy and the current stock market run could be elongated and enhanced. Traditionally, four years into an economic recovery, Main Street confidence would already be near historic highs, leaving little room for improvement. Normally at this point, excessively strong confidence among private sector players (exhibiting overly exuberant private player risky behaviors) would represent a recession and bear market risk. Instead, today, because Main Street confidence remains conservative and pessimistic those risks remain surprisingly low.

Consequently, the rest of this economic expansion and its Bull market may depend less on what the Congress, or the Federal Reserve does than on what happens with Main Street confidence. It is worthwhile, therefore, to examine the recent improvements in confidence measures, what factors may continue helping to restore confidence, and what this implies about the future of the economic recovery and its Bull market.

… finally …

WolfST: PPI, “Core” PPI, “Core Services” PPI Inflation Much Hotter after Whopper Up-Revisions Going Back Months

The problem is in services, which account for 67% of PPI. But goods prices are re-accelerating too. The whole inflation scenario has changed.

… AND, IF, big IF, there is ever to be a real bear market in stocks, i’d imagine this to become commonplace …