Good morning … as the week ahead contains some liquidity events (aka Treasury auctions) with 2s TODAY, 5s tomorrow and 7s on Wednesday — all moved forward a day to accommodate an early close Thursday and full closer of the US bond markets on Good Friday — I’m going to start with a look at 2yy

2yy: 4.50% as resistance … trend exhausted, momentum stalling …

…bullish momentum waning AND with supply dead ahead, NOT often a compelling mix for a setup or concession BUT with a Fed affirming 3 CUTS (despite or because the news, we must remember CUTS are not same as EASING), there’s room for decline … RESISTANCE on my daily chart nearer 4.50% and presumably a move there would come with momentum (stochastics, bottom panel) moving further into overBOUGHT territory…) … for more weekly, MONTHLY context see this weekends post HERE

… here is a snapshot OF USTs as of 713a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower this morning heading into the next three days of Treasury coupon auctions and Friday's PCE/Powell events. DXY is modestly lower too (-0.1%0 while front WTI futures are higher (+0.6%). Asian stocks saw declines in Japanese and Chinese markets, EU and UK share markets are modestly lower (SX5E -0.2%) on balance while ES futures are showing -0.3% here at 7am. Treasury prices opened higher in Asian hours amid very light volumes- though prices drifted lower during London's AM session. Our flows have seen buying in intermediates (7's)- though not at the pace seen last week. Overnight Treasury volume was ~60% of average with 2yrs (50%) seeing surprisingly light turnover ahead of today's $66bn auction of the same…

… Treasury 2yrs: Here's how we'd frame the picture: solid range support seen above at 4.735% and resistance below beginning at 4.483% or so. We're smack in the middle of those presumed boundaries with short-term momentum (lower panel) mixed and uninteresting. The message here seems to be: more range trading ahead.

… THEY do it (2yy visuals with a Terminal) far better than I … and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities modestly softer, Antipodeans benefit from a stronger CNH, Crude bid; Central bank speak due … Bonds are incrementally softer ahead of a 2yr US auction

The latest FOMC meeting suggests that this is a Fed that wants to cut rates in the face of strong economic growth.

We like SFRZ4/Z5 steepeners, as they should react asymmetrically to various growth outcomes this year.

The Fed outcome is pro-risk. We like EURBRL lower, EURMXN lower and SPX topside calls.

…. The main risk to the trade we believe is not on the growth side, but rather on the inflation side. Specifically, much stickier-than-expected inflation over the next few months would prompt a more hawkish reassessment of the Fed’s reaction function, in our view. As such, one way of hedging the steepener is via paying 1y inflation swaps. Although they are at the high end of the recent range, our forecasts do see scope for them to move even higher (Figure 2).

DB Early Morning Reid (on the weeks’ most important data happening once week is OVER …)

… On a very related theme, the most exciting event of the week happens once markets are actually closed for the month and Q1 is done and dusted in performance terms. Strangely, the monthly US personal income and spending report, which contains the crucial core PCE, is released on Good Friday when bond and equity markets are closed. The flash CPIs in Italy and France also come out on Friday, with the Spanish print due on Wednesday. Staying on the inflation theme, Tokyo CPI is out on Thursday, with the summary of opinions from last week's BoJ meeting on Wednesday. This will garner some attention given the once-in-a-generation shift in policy. Australian CPI is out on Wednesday…

…In terms of that core PCE print on Good Friday, DB expects +0.27% vs. 0.42% last month. In Powell's press conference, he remarked that the month-over-month print for core PCE could be "well below 30bps" at the end of the month. Taking him at his word does offer downside risk to our economists' forecast. They believe upward revisions to the January healthcare services prices could square these two numbers…

By the end of 2024, “no landing” (45%) eclipses “soft landing” (38%) as the most likely US economy outcome with only 17% thinking “hard landing”.

Our respondents suggest equities (84%) and credit (83%) price in a high probability of a US soft landing, up around 10% since December.

Maybe one of the reasons that markets are still buoyant even with a “no landing” view in the ascendancy is perhaps because 47% believe that central banks should tolerate an extended inflation overshoot before trying to return to 2%.

However, 5yr inflation expectations continue to edge down which may have also helped recent market buoyancy. The implied suggestion being that the economy is allowed to run hot in the near term but with central banks having things under control over the medium term.

"Only" 26% think we'll see negative rates in the next decade for a major economy now the BoJ has removed that policy.

We also look at whether there are bubbles in various assets classes including tech, the Mag-7 and Bitcoin, and whether the next big move in the S&P and 10yr USTs will be up or down. We also show where you think productivity will be in a decade, and whether WFH trends have continued to edge down.

… Our respondents remain much more convinced that the next 100bps move for 10yr USTs will be 100bps lower and not higher. Indeed, 69% maintain this bullish view even though yields have already fallen 61bps since our last survey in October

… The question for investors at this stage is whether the market can finally broaden out in a more sustainable fashion. As we noted last week, we’re starting to see breadth improve for several sectors. Looking forward, we believe a durable broadening comes down to whether other stocks/sectors can deliver on earnings growth. One sector showing strong breadth is Industrials, a classic late-cycle winner and a beneficiary of major fiscal outlays (e.g., IRA and the CHIPS Act) and the AI-driven data center buildout. A new sector displaying strong breadth is Energy, which is the best performer over the last month but is still lagging considerably since the October rally began. Taking the Fed’s recent messaging into account and assuming it is less concerned about inflation or looser financial conditions, commodity-oriented cyclicals and Energy in particular could be due for a catch-up. The sector’s relative performance versus the S&P has lagged crude oil prices, and valuation looks compelling. Relative earnings revisions appear to be inflecting as well. It may also surprise some readers that Energy has contributed more to the change in S&P earnings since the pandemic than any other sector, yet it remains one of the cheapest and most under-owned areas of the market. Please see our Weekly Warm-up tomorrow for more details on this analysis and the potential opportunity.

We upgrade the Energy sector to overweight amid a combination of inflecting relative earnings revisions, strong breadth and compelling valuation. The recent stability of crude prices also points to a catch up in both relative performance and earnings growth, in our view.

The interest rate hike in Japan is historic and marks a new beginning for Japanese monetary policy. The technical details of the decision affirm our call for a structural shift in inflation behavior but also signal negative rates are unlikely to return, even in a downside scenario.

… Federal Reserve’s Bostic is also speaking. Bostic has been suggesting only one rate cut is needed this year—just one rate cut would leave debt increasingly unaffordable for consumers as income growth would then fall faster than interest rates…

… And from Global Wall Street inbox TO the WWW,

Apollo: Trend Wage Inflation Is 5% (um, Team Rate Cut … over to you?)

The New York Fed has constructed a new measure of trend wage inflation, which currently is running at 5%, see chart below and here.

Wage inflation at 5% is not consistent with the Fed’s 2% inflation target. The Fed will keep interest rates higher for longer.

This is not surprising given the ongoing reacceleration in both nonfarm payrolls and CPI and PPI inflation, likely driven by the significant easing of financial conditions since the December 13 FOMC meeting and Chris Waller’s hawkish-to-dovish speech in November.

Bloomberg: Burned Before, Bond Markets Resume Rate-Cutting Trades Worldwide (kindly note the language and point DBs Jim EARLY MORNIN’ Reid makes … the outcome < the BET … read a couple times make sure that sinks in…)

Pimco, BlackRock among managers favoring short-dated debt

Investors lean toward cuts from Fed, BOE, ECB starting in June

… Among money managers such as Pimco and BlackRock Inc., and one-time bond king Bill Gross, the prospect of lower rates is boosting the allure of shorter-dated obligations due in around five years or less, which stand to gain the most as rate-cut speculation builds.

That sort of outperformance relative to longer maturities is a recipe for so-called steepener bets, where the yield curve returns to a traditional upward slope. Of course, there’s still the risk that central banks again fail to vindicate the bullishness around shorter tenors given inflation remains sticky and labor markets continue to hold up.

“Whether we actually get what is priced in is a moot point, but for the current direction of travel, the promise is all that matters for now,” said Jim Reid, Deutsche Bank AG’s global head of economics and thematic research. While markets are focused on a “dovish narrative, it’s worth bearing in mind that sentiment on rates has switched back and forth over 2024,” he said.

Calafia Beach Pundit(former WAMCO econ…weighs in on Financial Conditions — excellent meaning NOT one for Team Rate Cut? whatever the case may be HE is using the BFCI and NOT the BCFI+ which is the index INCLUDING BONDS and IMO — as a bond guy — far more important and INCLUSIVE but then again, I’m no longer in a bond seat so … whatever HE says … as HEs apparently got the Terminal … )

Here’s a very short post to highlight the excellent shape of today’s financial conditions. At the very least this adds up to one important conclusion: there is NO shortage of liquidity, and financial markets are thus free to do what they do best: namely, to redistribute risk away from those that don’t want it to those who value risk. This is a very important function of free markets, since it reduces the market’s overall level of anxiety, thus minimizing the risk of disrupting influences and panic.

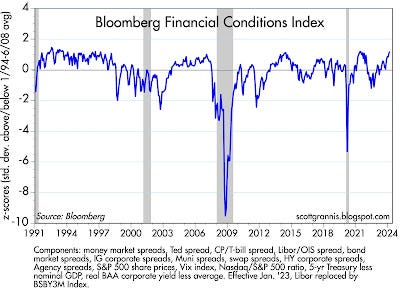

Chart #1

Chart #1 shows Bloomberg’s index of financial conditions. The components of this index are at the bottom in fine print, and they represent a comprehensive array of risk indicators. By this measure, today’s markets have almost never been so healthy.

Chart #2

Chart #2 shows corporate credit spreads, the difference between the yield on corporate bonds of different quality and Treasury yields of comparable maturity. Spreads have rarely been tighter than they are today, which adds up to a strong vote of confidence on the part of the market regarding the future health of corporate profits, and by extensions, the prospective health of the economy.

I would only add that the Vix Index (aka the Fear Index) is about as low as it gets. We are living in “untroubled” times by these measures.

Sam Ro from TKer: When two popular recession indicators failed (i’d point out here some thoughts from DB — aka The Horses Mouth — in as far as the curve as failed recession indicator … has it really failed and whatever the case may be … WHY they believe it all matters…)

… The inverted yield curve The yield curve represents the shape that forms on a chart when you plot the interest rate, or yield, for Treasury debt securities with various maturities. Typically, shorter-term rates like the yield on the 2-year Treasury note will be lower than the yield on the 10-year Treasury note.

The yield curve inverts when a longer term rate is lower than a shorter term rate (e.g., when the yield on the 10-year note is lower than yield on the 2-year note).

Historically, when the yield on the 10-year note falls below the yield on the 2-year note (i.e., when the “2s10s” yield curve inverts), recessions have been somewhat soon to follow.

When the line dipped below the X-axis, a recession usually followed. (Source: FRED)

Deutsche Bank’s Jim Reid noted that on Wednesday “we passed the longest continuous U.S. 2s10s inversion in history. Although the 2s10s first inverted at the end of March 2022, it has now been continuously inverted for 625 days since July 5th 2022. That exceeds the 624 day inversion from August 1978, which previously held the record.“

This has been the longest 2s10s inversion in history. (Source: Deutsche Bank)

While the inverted yield curve may have a good track record of predicting recessions, it’s not very precise in predicting when recessions will start. According to a Goldman Sachs analysis of 2s10s inversions since 1965, seven to 49 months passed before recessions occurred, with a median of 20 months.

So, the economy could go into recession a week, a month, or a year from now, which would arguably confirm the inverted yield curve’s signal.

That said, one has to question the value of an indicator that sometimes leads events by two to four years.

As Oaktree Capital’s Howard Marks says, “Being too far ahead of your time is indistinguishable from being wrong.“

The falling Leading Economic Index…

… On Wednesday, The Conference Board confirmed that the positive developments continued into February.

“The U.S. LEI rose in February 2024 for the first time since February 2022,” Zabinska-La Monica said. “Strength in weekly hours worked in manufacturing, stock prices, the Leading Credit Index, and residential construction drove the LEI’s first monthly increase in two years.“

The LEI’s recession signal hasn’t worked out this time. (Source: The Conference Board)

*Saw somewhere the difference in the public's Perceived Economic/Inflation conditions vs MSM hypnotic drug-hazed mantra of 'Everything's GREAT' is/was the removal of Auto Loans & Housing Expenditure from CPI. If reincluded CPLie goes from 3% to 8%; perception problem explained.

*Some NATO country(s) want to start WWIII. Islamic terrorists DON'T get captured...ALIVE anyways!

*ISIS/ISIS-K is a CIA/MI6 offspring/proxy. Don't be fooled people!

*When the head starts spinning, and the voices start taunting, and the walls start closing in, do as I did Friday afternoon and FLEE THE SCREEN. Was my plan anyways but then the Russian concert hit sent me mind spinning. The gym induced those positive brain chemicals I needed. Then follow your truest passion-mines Skiing, and answer the call. Take it from a young man on the ski lift Saturday who told me [I'm already familiar :( w/this lesson], if you don't pull yourself away from the rabbit hole, you may not climb out. Alive anyways. Remain Calm and Have Fun, amidst the madness, as my online friend Tom Luongo says.

I love some of the comments by the different firms: " when doves fly"

"Fed data shows 5 % wage growth,

Over to you team Rate Cut"

Paraphrasing, "being excessively

early is indistinguishable from

being WRONG "

Cracks me up !!!

What a pleasure to read...

*Saw somewhere the difference in the public's Perceived Economic/Inflation conditions vs MSM hypnotic drug-hazed mantra of 'Everything's GREAT' is/was the removal of Auto Loans & Housing Expenditure from CPI. If reincluded CPLie goes from 3% to 8%; perception problem explained.

*Some NATO country(s) want to start WWIII. Islamic terrorists DON'T get captured...ALIVE anyways!

*ISIS/ISIS-K is a CIA/MI6 offspring/proxy. Don't be fooled people!

*When the head starts spinning, and the voices start taunting, and the walls start closing in, do as I did Friday afternoon and FLEE THE SCREEN. Was my plan anyways but then the Russian concert hit sent me mind spinning. The gym induced those positive brain chemicals I needed. Then follow your truest passion-mines Skiing, and answer the call. Take it from a young man on the ski lift Saturday who told me [I'm already familiar :( w/this lesson], if you don't pull yourself away from the rabbit hole, you may not climb out. Alive anyways. Remain Calm and Have Fun, amidst the madness, as my online friend Tom Luongo says.