If I missed thisand itis old news, well, sorry … Name THIStune ….

… The contractionary effects of monetary policy and the de-facto negative NNS policy stance of fiscal policy will serve to place increasing downward pressure on inflation and growth. A sharp 7% rate of decline in vehicle sales In the first quarter is a sign that the deflationary trend in big ticket consumer goods prices is more likely to gather speed than reverse. The inflation rate will likely undershoot the Fed's target, and the unemployment rate will move higher than anticipated by the Fed. Inflation and unemployment are lagging indicators, and much of their cyclicality occurs after, not before, recessions end. This declining inflation environment will continue to bring down inflationary expectations and long-term Treasury bond yields.

Full 4pg note HERE … He offers some further insight …

… Following the approach of the NBER, we created a series that takes the average of payroll and household measures weighted by the weekly hours worked from the payroll survey. Aggregate hours worked for this new indicator increased 0.6% in the first quarter versus a year ago, down from increases of 1.4% in 2023 and 0.9% in 2019 (Chart 3).

… draw whatever conclusions YOU’d like but please, please read THE NOTE … it’s only 4pgs and he writes but 4x per year, as opposed to some who tweet their view 4x an hour.

NOW … with a couple important developments past 24hrs …

RTRS: Fed policymakers agree: there's no urgency to cut rates ZH: Bitcoin & Bullion Bid As Hawkish FedSpeak Hammers Stocks & Bonds

CNBC: Stock futures fall as Israel conducts limited strike against Iran CNBC: Oil jumps 3%, spot gold hits record high after Israel launches strike in Iran RTRS: Tehran plays down reported Israeli attacks, signals no further retaliation

… leaving ME checkin’ on a couple visuals …

Earl: spiked on news BUT appears to be remaining ‘calm’ … a tweet

Oil reaction to reported Israel strike on Iran? Nothing Price now is $87, same as end of yesterday

5yy:

AND … moving right along, here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher with the belly outperforming after Israel attacked Iran in what appears to be a 'limited' attack. DXY is a hair lower (-0.7%) while front WTI futures are now lower (-0.3%) after prices spiked over $86/bl immediately after the attack hit the tape. Asian stocks fell (NKY -2.66%), EU and UK share markets are all in the red (SX5E -0.5%) while ES futures are showing -0.43% here at 6:30am. Our overnight US rates flows saw a 'smashmouth' session during Asian hours as yesterday's bond sell-off was completely reversed in just 15 minutes after the Iran headlines hit. Volumes were extreme in Asia (700% of average) and the desk saw net better buying in intermediates then. During London's morning hours, the drama subsided a bit amid light client activity. Overnight Treasury volume was ~250% of average as of 6:30am.

… At the other end of the curve, 30-year Treasuries probed deeper back into their former up-channel overnight, ultimately rejecting much of that risk-off spasm after Israel's strike appeared targeted/limited.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Sentiment hit after Israel strikes Iran, though has pared as Iran downplays the attacks; Crude now lower … Bonds are modestly firmer, though has pared the majority of the overnight advances … USTs have pulled back from overnight geopolitics-induced highs of 108-22+ with newsflow otherwise limited and the docket sparse as we approach the Fed blackout. USTs climbed over 20 ticks during the initial reporting of an Israel strike on Iran, before peaking and beginning to pullback as Iran downplayed the attacks.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: US Economics Research: March existing home sales show some pullback

Existing home sales posted a decline of 4.3% m/m in March, falling to 4.19mn. Single-family and multifamily sales both showed similar rates of decline, leading to an increase in the monthly supply of homes.

BARCAP U.S. Equity Strategy: Food for Thought: Rolling Off the Peak

Despite paving most of the SPX's road to its recent peak, Big Tech has been more resilient than the rest of the Tech sector through the MTD selloff, likely because Big Tech's gains were less dependent on multiple expansion. Overall, losses have been more evenly distributed than gains. 1Q earnings are the next overhang.

BloombergBNP US Q1 GDP: Even stronger than top line will suggest

KEY MESSAGES We estimate annualized US real GDP growth of 2.7% in Q1 2024, as final sales to domestic purchasers (GDP excluding volatile trade and inventories, which better reflects underlying demand) continues to run above 3%.

Consumer spending likely propped up the quarter, as the robust labor market continues to generate a solid flow of paychecks to keep fueling consumer demand.

We believe the sturdy pace of economic growth to start the year would not dissuade the Fed from starting its rate cutting cycle in July, provided inflation cooperates and labor market conditions continue to rebalance. Positive supply shocks should continue to provide a tailwind to economic activity without boosting inflationary pressures, in our view. However, if inflation pressures prove more persistent, the probability for a July move could diminish.

BNP: US housing inflation: Moderation likely but not assured

KEY MESSAGES With goods deflation waning and non-shelter services inflation sticky, rents are key to continued moderation in US core inflation in 2024–25, in our view.

Our analysis suggests rent inflation will follow market rents and home prices and continue to move lower this year, albeit more gradually than a number of available forecasts indicate.

Booming apartment construction should also keep rent inflation easing next year, though we think the jump in immigration and a tight sales market tilt the balance of risks to the upside.

Given their outsized role in our base case of lower core inflation, rents realizing in line with our upside scenario would imply little further improvement in core inflation and, with it, fewer Fed rate cuts.

DB: A brief history of Gold in one chart (i’m a sucker for longer term charts even IF they are of Gold)

Goldilocks: Existing Home Somewhat Below Consensus Expectations; Leaving Q1 GDP Tracking Unchanged at +3.1%

BOTTOM LINE: Existing home sales decreased by 4.3% to a seasonally adjusted annualized rate of 4.19 million units in the March report, somewhat below consensus expectations. The median sales price of all existing homes decreased 0.5% month-over-month, and the imbalance between housing supply and demand improved somewhat. We left our Q1 GDP forecast unchanged at +3.1% (qoq ar) and our domestic final sales forecast also unchanged at +3.1% (qoq ar).

Financial markets are having to assess political risks—something markets are ill-equipped to do. US officials confirmed Israel had attacked Iran, with reports of an explosion in Isfahan. The market response was a classic (perhaps unthinking) safe-haven trade. Does Iran now respond? Iranian media is downplaying the attacks, and it might be difficult for Iran’s government to retaliate if the narrative in Isfahan is “nothing to see here”…

The Federal Open Market Committee can take the rest of the year off. Today, Federal Reserve Bank of New York President John Williams said: "Monetary policy is in a good place." He said so at the Semafor World Economy Summit in Washington. He added: "We've got interest rates in a place that is moving us gradually to our goals, so I definitely don't feel urgency to cut interest rates." In other words, the Fed is in no rush to lower interest rates. That was the theme of my March 25 FT article titled "The Fed should resist messing with success: If the economy is doing well with the current level of interest rates, why lower them?" At the time, the widespread consensus was four rate cuts this year.

Today, the 2-year Treasury note yield was 4.99%, implying one cut in the federal funds rate from a target range of 5.25%-5.50% to 5.00%-5.25% over the next 12 months (chart).

The price of a barrel of crude oil continued to slip today on a news that the US has approved a potential Israeli Rafah operation in exchange for the Jewish state not conducting counterstrikes on Iran. That's according to a Thursday report from the Qatari newspaper The New Arab.

On the economic front, initial unemployment claims continue to signal that the labor market is strong (chart). In our opinion, this is the best high-frequency indicator of the jobs market. It is signaling that the unemployment rate might have remained below 4.0% during April for the 27th month in a row!

… And from Global Wall Street inbox TO the WWW,

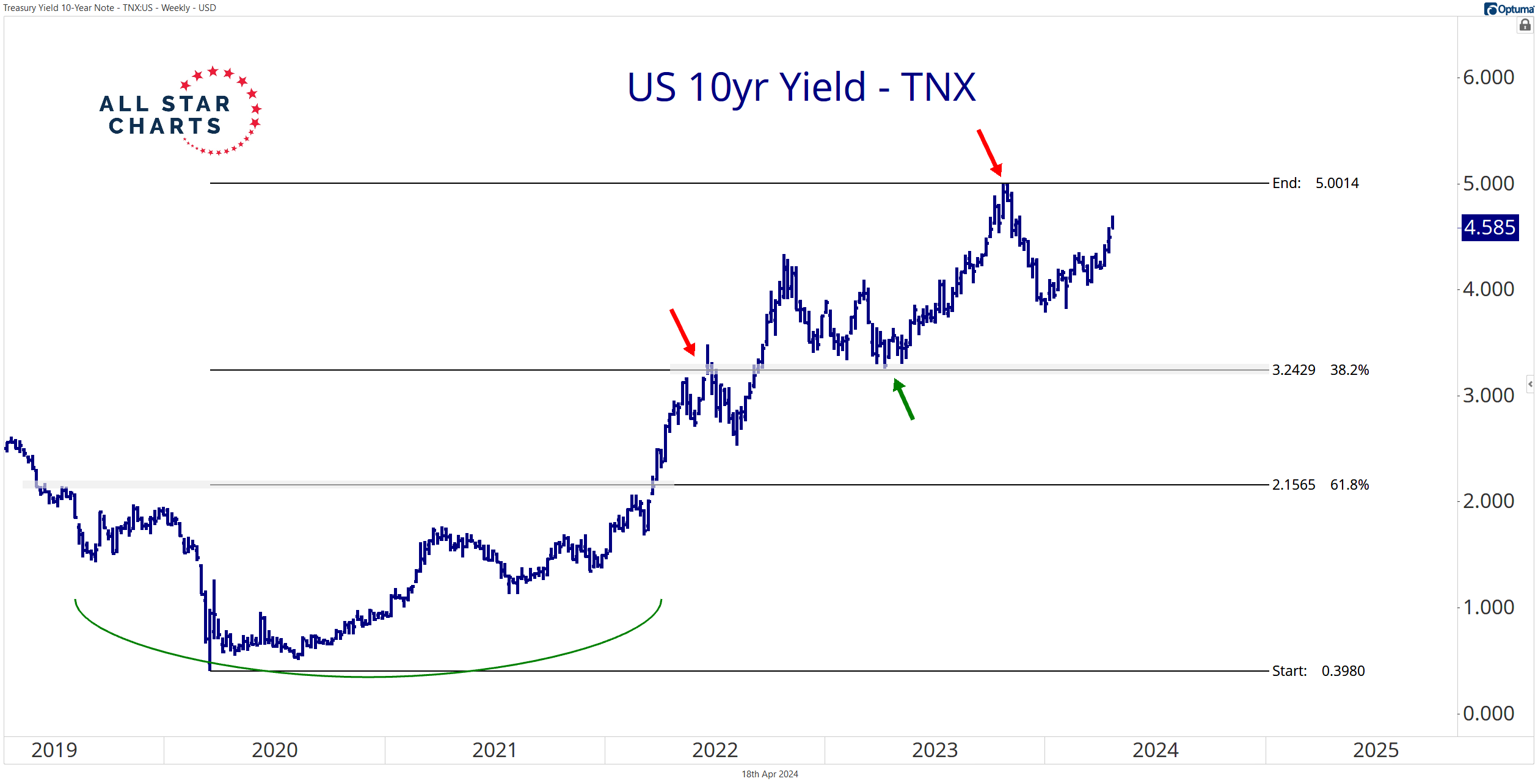

AllStarCharts: Interest Rates Zig and Zag (not sure if this post is to relay how smart he is becoming ‘on his journey to CMT’ship’ and don’t wanna ruin the parade, but am not certain am a fan of TNX as representation OF 10s … but then, these days, without a Terminal … I suppose it’s all we got? whatever, over to th e soon to be smartest guy he knows, just ask him? …)

… Nevertheless, my journey to earning the CMT designation exposed me to the Elliott Theory, and I find it prudent when examining the US 10-year yield.

So here we go…

I can’t ignore the impulse wave on the US benchmark interest rate (highlighted in bright blue):

I will not cover the dizzying rules and notation that define these waves (for more information, check out the Elliott Wave Principle by Frost and Prechter.)

A new year-to-date low for the benchmark yield wouldn’t negate the underlying uptrend for interest rates. Plus, it seems logical considering the intermediate mean-reverting environment.

Most assets are correcting within a sideways mess, including interest rates. Embrace it.

Bloomberg (via ZH): It's Time To Pay Attention To Funding Risks Again Bloomberg (via ZH): Stocks Will Face Resistance While Liquidity Backdrop Is Weak

ZH: Is China's 'Dumping' Driving US Treasury Yields Higher? ZH: Huge Bond Wagers Make Some Hedge Funds Too-Big-To-Fail, IMF Warns

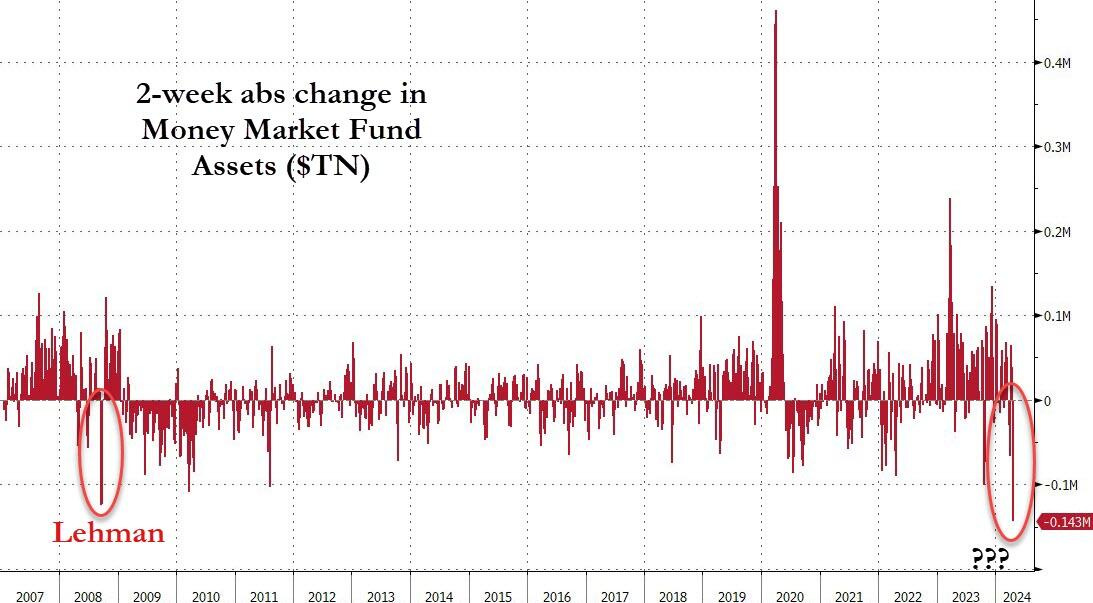

ZH: Money-Market Fund Assets See Largest Outflows Since 'Lehman' (they’ve been growing so much a large decline SHOULD be somewhat less meaningful, no?)

… Corporate taxes collected from April 11 through April 17 totaled $100.7 billion, Treasury data show.

While Tax-Day's impact matters obviously, we note that this is the largest weekly drop in money-market fund assets since Lehman (Sept 2008) and the biggest two-week drop (-$143BN) on record...

AND while I’m HOPEFUL to have something out over the weekend ahead of markets OPEN Sunday evening BUT with family in town for the next several days, well, I will do the best I can…… THAT is all for now. Off to the day job …

{kind=link}