while WE slept: USTs higher, led by GILTS on above avg volumes; "Worst of Both Worlds: Are the Risks of Stagflation Elevated?"; "What Went Wrong With US Inflation"; and ... cloud seeding?

Good morning … turns out, 20s were in fact, ‘buyable’ and it would seem that momentum turning on daily basis as rates stabilized a touch …

… To be fair, there was a recovery for bonds, but that was partly a risk-off move into safe havens, which pushed the 10yr Treasury yield (-8.0bps) down from its 5-month high the previous day to 4.59%. Lower oil which we'll discuss below also helped. Yields are another couple of basis points lower across the curve in Asia…

… The bond rally we discussed above has been helped by the latest decline in oil prices, with Brent Crude (-3.03%) closing at a 3-week low of $87.29/bbl, which came as the latest EIA report showed US crude inventories at their highest level in 9 months. And in Europe, natural gas futures also fell back after their recent advance, with a decline of -6.43% on the day. So a wild ride in commodities this week.

The decline in oil prices played out even as uncertainty remains over the direction of the conflict in the Middle East. Yesterday, Israeli PM Netanyahu met with UK Foreign Secretary Cameron and German Foreign Minister Baerbock yesterday, but he also said that “I want to make it clear - we will make our own decisions, and the State of Israel will do everything necessary to defend itself." The comments raised the prospect that some sort of response would still happen, and Cameron said that “It’s right to have made our views clear about what should happen next, but it’s clear the Israelis are making a decision to act”… -DBs Early Morning Reid (18 April 2024)

… And while bond rally GOOD, a chart — best I can — of EARL struck me as worth noting even IF out of my wheelhouse …

USOIL (via TradingView): triangulation continues to matter as does momentum which appears to ME to be now very overBOUGHT …

… Moving on to another development which is inflation relates — EARL is inflation related, right? Yesterday, shortly after hitting SEND the current admin decided to voice concerns and plans to increase costs for ‘Merica …

At least way I read what is transpiring … so, to be clear, on heels of JPOW saying NOTSOFAST to Team Rate Cut (and Team Biden?), Team Biden out with …tripling of steel and aluminum tariffs, which are said to NOT be inflationary …

CNBC: Biden wants to triple China tariffs on steel, aluminum imports

… Tariffs can also have unintended economic ripple effects by raising U.S. manufacturing costs that may ultimately translate to higher consumer prices. That would be an unwelcome result during a time when Biden is already in the middle of a yearslong battle to bring down stubborn inflation and prove to voters that his economic agenda is working.

A senior administration official on Tuesday rejected the notion that tariff hikes would lead to higher inflation.

“If taken these actions will not increase inflation, but they will protect American jobs and steel industry,” the official said on a call with reporters. “Residual inflation is not coming from goods, these actions will not change that.” …

… I’m speechless (cuz, you know, if you-know-who said this, he’d be ridden like Smarty Jones) and so I’ll just move right along …

How ‘bout some GREAT news …

ZH: Stellar 20Y Auction Sends Yields Sliding To Session Lows

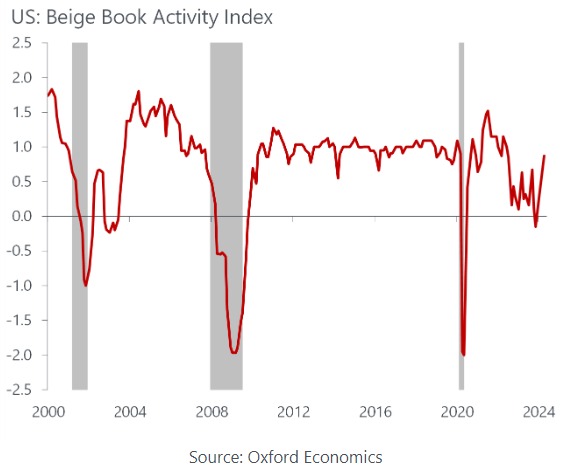

…. which then was followed by / accompanied with latest from Beige Book:

CalculatedRISK: Fed's Beige Book: "Economic activity expanded slightly" ZH: Beige Book Reveals Economy In Far Worse Shape Than White House Claims

… and I am done. Shoulda quit while I’m behind still making sense of it all … good news on EARL front, as far as yields go BUT running into what looks to be decent ‘support’ (Earl) and so, resistance (bonds). So … here is a snapshot OF USTs as of 703a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher with Gilts leading the way this morning. DXY is little changed while front WTI futures (see attachments) are -1% lower. Asian stock were mostly higher, EU and UK share markets are modestly higher (DAX UNCHD but SX5E +0.4%) while ES futures are showing +0.25% here at 6:45am. Our overnight US rates flows saw heavy block futures activity with volumes elevated in the 20yr cash sector too (better selling in 20's seen, on balance). Further in, we saw better real$ buying in intermediates, balancing the back-end selling. During London's AM hours saw more real$ demand for 3yr-7yr paper alongside fast$ interest to get long the 3y point in various 'fly structures. Overnight Treasury volume was decent at ~115% of average with 7yrs (174%) and 20yrs (245%) seeing some relatively high average turnover among the benchmarks.

…The 30yr Treasury chart looks predictably similar in set-up but with one teachable aspect to it: the apparently false breakout above the channel top this week. We said a few days ago(?) that we don't think that investors should follow topside breakouts like that; channel-reverting as they often can be. This is a good example of that risk... You want to see another picture like that? Well, have a look at the well-correlated (to 30yrs) chart of front WTI futures (CL1) and its recently failed breakout above its channel. Daily momentum is solidly bearish for CL1, as you can see in the lower panel, while medium-term (weekly) momentum is trying to flip bearishly here from a deep 'oversold' reading too (not shown). So the rally in CL1 that began in mid-December, and that may have helped to drag yields and breaks higher, appears to be reversing (or at least there's an imminent threat of such).

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Contained trade in equities & FX, TSMC earnings strong and Crude at lows … Bonds bid, continuing the upside seen following Wednesday’s auction … USTs are bid, but only modestly so with newsflow somewhat limited thus far ahead of IJC & Fed speak. Positive undertones continue from the strong 20yr sale on Wednesday; USTs around their 108-10+ peak, surpassing Tuesday's 108-08 best.

The plunge in oil prices on Wednesday has interesting implications for techs. We are on the verge of posting bearish indications and formations, which could suggest another 3% move lower in oil prices in the short term.

…WTI A similar chart to Brent. Price broke below 83.60-83.85 (November 3 and March 19 highs) after coming close to testing the 76.4% Fibonacci retracement. On the weekly chart, we are also looking at a potential evening star formation, with weekly slow stochastics also looking likely to cross lower from overbought territory.

What it means: IF we see the weekly developments, it would also indicate further downside for WTI. Next support is at 80.16-80.85 (55d MA, March 21 low, March 1 high).

OTHER TECHNICAL DEVELOPMENTS WORTH NOTING … US Rates: in both 2y yields and 10y yields, we have seen a retreat from resistance levels. However, the prior developments mean that we retain our view of being slightly biased towards higher yields. We keep a close eye on slow stochastic (momentum) indicators for any turn lower, given the attractiveness of these levels to dip buyers. Check out the details in our note CitiFX Techs - US yields: Stretching the resistance bands

DataTrek: Why The Fed Would Hike, Fund Flows

Topic #1: What would it take for the Fed to raise rates (not cut or simply leave them unchanged) over the next 12 months? This question is starting to get some traction, even though markets are thus far shrugging it off:

Futures give 71 percent odds that Fed Funds will be lower than today after the September FOMC meeting.

This market also puts 57 pct odds on 2 or more rate cuts by year end 2024.

Two-year Treasuries yield 4.9 percent, less than the current Fed Funds rate of 5.25 – 5.50 pct. Note: since real rates are positive, this market is expecting more than just 1 rate cut over the next 2 years.

An about-face on rate policy would therefore be a genuine shock and, despite seemingly zero odds of occurring, one at least worth considering. Not only would it reignite worries about Fed policy shoving the US into recession, but it would also signal that the long run neutral rate of interest is higher than previously thought. This would push long term rates higher, raising the cost of capital for individuals and companies.

The following chart of Fed Funds (black line) and annual Consumer Price Index inflation (red line) from 1960 to the present tells the story of how these 2 variables interrelate across time:

The three periods highlighted in the graph tell very different stories about the intersection of Fed rate policy and inflation:

From 1960 to 1980, rates and inflation tracked very closely. Fed Funds rose when inflation increased and fell when it decreased. While the Fed of the 1970s is often criticized for not doing enough to tame inflation, it was not entirely asleep at the switch. When inflation increased, the FOMC pushed rates higher. The trouble was that, when inflation fell, they were too quick to lower rates. That is how we ended up with +15 percent inflation in the early 1980s.

From 1981 to 2001, Fed Funds were consistently above CPI inflation. The 1981 – 1982 “Volcker Recession” squashed inflation because rates were far above CPI. The FOMC under Alan Greenspan then continued this pattern, which had the desired effect of keeping inflation under control.

From 2002 to the present, rates have generally been below CPI inflation. This was especially true in the slow-growth 2010s. The only exceptions were in 2007 and the last 12 months.

Takeaway (1): Should inflation start to reaccelerate, Chair Powell and the FOMC will have no choice but to increase rates – possibly dramatically – or risk a repeat of the 1970s. Paul Volcker was successful because he proved to markets, businesses, consumers, and investors that the Fed was OK with causing a deep recession in pursuit of its goal to tame inflation. Thus far, Powell’s Fed has been able to avoid that outcome. If inflation does start to move higher, however, they may have to bite the bullet and accept harsher economic medicine is needed to achieve its goal.

Takeaway (2): As we have been discussing recently in these notes, oil/gasoline prices are the fulcrum issue for inflation just now. If they rise dramatically due to the situation in the Middle East, the Fed will have a tough decision to make. When Russia invaded Ukraine in 2022, oil prices surged but did not cause recession or even weaken the US economy enough to get inflation tracking more quickly to 2 percent. Whether a longer-lasting oil shock has a larger impact remains to be seen, and the Fed’s strategy of being data dependent may leave it behind the curve either in raising or lowering rates.

Takeaway (3): Equity markets understand this tension but have the luxury of time before deciding whether to discount the risk of higher Fed Funds. Mideast tensions may wane. Corporate earnings are still strong. Interest rates are higher, but not yet breaking out to the upside. We often say that equities are an optimist’s game, but they also favor the patient…

GoldilocksUS Daily: Do the Official Statistics Fully Capture the Recent Surge in Immigration?

… Nonfarm payrolls are less directly affected by underestimates of immigration in the Census, as they are tied to establishments that can report employees regardless of their immigration status. This means that the surge in unauthorized immigration in 2023 likely contributed to the widening of the employment gap between the establishment survey and the household survey. Using state-month level panel regressions, we estimate that nonfarm payrolls likely capture 0.6-0.9 million workers missed by the household survey. This suggests that nonfarm payrolls undercount unauthorized immigrant employment by roughly 0.1-0.4 million.

An undercounting of unauthorized immigration has likely contributed modestly to the sharp increase in the gap between gross domestic product (GDP) and gross domestic income (GDI) over the last year. We suspect that GDP, which is an expenditure-based measure of economic activity and is constructed using sales and production data, may have captured the consumption boost from recent immigration surge, while GDI, which is an income-based measure of economic activity, may have underestimated the total employment and compensation paid to undocumented workers. Incorporating recent immigrant workers into the wages and salaries component of GDI reduces the GDP-GDI gap by about 0.1-0.2pp.

Strategas: SHORT-TERM INDICATORS STARTING TO LOOK RINSED …

… MACRO LESS SUPPORTIVE AS RATES CONTINUE TO PRESS HIGHER

UBS (Donovan): The destructive power of economic nationalism

US President Biden called China “xenophobic” in comments highlighting China’s structural economic challenges. Biden also pledged higher taxes on US consumers of China’s steel and aluminum. US Congress lives in terror that China will learn the “Texas hold‘em” TikTok dance before Speaker Johnson has mastered the moves, and is proposing to tie a TikTok ban to aid measures for Ukraine and Israel.

The world is undergoing significant structural change. Fear of change, with loss of income and social status, encourages people to look for scapegoats. The political response to this is often prejudice politics, and (when foreigners are the scapegoats) economic nationalism. This is a global trend, and economically destructive. Success in the coming decades depends on having the right person in the right job at the right time. Prejudice and economic nationalism stand in the way of that…

Wells Fargo: Worst of Both Worlds: Are the Risks of Stagflation Elevated?

Part I: A Framework to Characterize Episodes of Stagflation Summary

In this first report of a three-part series, we present a framework to characterize historical episodes of stagflation into mild, moderate or severe episodes.

Iain Macleod coined the term "stagflation" during an address to the House of Commons in 1965: “We now have the worst of both worlds—not just inflation on the one side or stagnation on the other, but both of them together.”

Stagflation can impose significant stress on the economy and can be a difficult situation to escape. Elevated inflation erodes consumer purchasing power, while weaker demand leads to a deterioration in the labor market, thereby limiting the opportunity for real wage gains.

Conventional monetary or fiscal policy actions are remedies that often improve stagnation or inflation, but not both.

The most salient episode of stagflation in modern U.S. history occurred in the 1970s. A perfect storm of energy price shocks, robust labor cost growth and elevated government spending led inflation to spiral, while economic output faltered and unemployment rose.

While we could debate on the fairness of that comparison, the exercise of comparing bouts of stagflation led us to develop a simple framework to organize historical episodes on a severity scale.

In data that span 1950 to present, we identified 13 instances of stagflation. Five episodes are mild, four are moderate and four are severe. The shortest episodes lasted two quarters, occurring in 1977-1978 and 1995, and the longest episode occurred in 1979-1982 (16 quarters).

In the next installment of this series, we summarize past episodes of stagflation and their accompanying monetary policy decisions.

… To the best of our knowledge, Iain Macleod coined the term during an address to the House of Commons in 1965. He said, “We now have the worst of both worlds—not just inflation on the one side or stagnation on the other, but both of them together. We have a sort of ‘stagflation’ situation. And history, in modern terms, is indeed being made.”

Macleod believed history was being made because the economic literature at the time doubted the existence of stagflation. Stagnation and inflation often move in opposite directions. The Phillips Curve is predicated on a similar principle. That is, a rising unemployment rate, which typically correlates with falling output, will bring down inflation; a falling unemployment rate, which typically correlates with rising output, will push inflation higher. The occurrence of stagflation ran in opposition to the logic behind the Phillips Curve, as elevated price growth persisted amid rising unemployment and weak economic growth.

Stagflation can impose significant stress on the economy and can be a difficult situation to escape. Elevated inflation erodes consumer purchasing power, while weaker demand leads to a deterioration in the labor market, thereby limiting the opportunity for real wage gains. Conventional monetary or fiscal policy actions are remedies that often improve stagnation or inflation, but not both. For example, enacting an expansionary policy, such as a fiscal stimulus package for consumers, can promote economic activity during a downturn, but it can also cause inflation to rise, all else equal. On the flip side, enacting a contractionary policy, such as raising short-term interest rates, can help to rein in inflation, but higher rates also dampen economic growth prospects.

Wells Fargo: School Me Once: Student Loan Cancellation Revisited

Summary New proposals from the Biden administration have brought student loan relief and its implications back into the macro discussion. In this report we (I) offer some context for student loans in the overarching category of household debt, (II) recap some of the high-level developments that have impacted the category in recent years and (III) offer a rough assessment of the latest proposals and weigh the impact on the consumer. In a nutshell: student loans are a fast-growing category of household debt, there has been a lot of tinkering with repayment in recent years and the latest developments will not make or break aggregate consumer spending even if the proposal overcomes the expected political and legal challenges.

Wells Fargo: Bank of England Set To Join The 'Higher For Longer' Club

Summary

The U.K. economy has continued along its disinflation path in early 2024, but at a more gradual pace than previously, as this week's wages and price data both surprised to the upside. At the same time, there are nascent signs of U.K. economic recovery. Sentiment surveys have been on an overall improving trend for the past several months, while January and February GDP outcomes point to a return to positive growth after the U.K. economy contracted during the second half of 2023.

A slower pace of disinflation could make Bank of England (BoE) policymakers cautious about lowering interest rates prematurely, while signs of economic recovery arguably reduce the urgency for monetary easing. Against this backdrop, we now forecast later easing than previously from the BoE. We forecast an initial policy rate cut to 5.00% at the August monetary policy meeting, followed by 25 bps rate cuts in November and December, for a cumulative 75 bps of rate cuts this year, which would see the policy interest rate end 2024 at 4.50%. We see a further cumulative 125 bps of BoE policy rate cuts in 2025, which would see the central bank's policy rate end next year at 3.25%.

Overall we expect the BoE to deliver modestly more easing than anticipated by market participants this year, and forecast noticeably more easing than expected by market participants next year. Over the medium-term, that could contribute to downward pressure on shorter-term U.K. bond yields, and see the pound underperform relative to many other G10 currencies over time.

… And from Global Wall Street inbox TO the WWW,

Bloomberg (via ZH): "No Clear Trend What Happens Next": Stocks Are Displaying Bearish Features Last Seen In 2022

… A lot will depend on corporate America’s showing this earnings season and where Treasury yields go from here. Tech giants like Microsoft, Meta Platforms and Amazon — among those projected to lead profit growth in the S&P 500 — are due to report next week and may offer a helping hand to stocks.

Fed chair ignited rally by signaling rate cuts in December

Housing, insurance, commodity prices among contributors

… Price gains have proven much stickier than anticipated a few months into 2024 amid a resilient economy and labor market. On Tuesday, Fed Chair Jerome Powell said persistent inflation means borrowing costs will stay elevated for longer than previously thought, a shift in tone with ramifications for policy around the world.

A persistent shortage of housing is partly to blame, as are rising commodity prices and car insurance premiums. But some also point to Powell himself for prematurely telegraphing interest-rate cuts, which ignited optimism in financial markets and fueled economic activity.

“They just got the inflation picture wrong,” said Stephen Stanley, chief US economist at Santander US Capital Markets LLC. “The mistake they made was they got really enamored with the combination of really strong growth and benign inflation that we saw in the second half of last year.”..

Bloomberg: Investors are on a sentimental journey — to where? (Authers’ OpED with couple snazzy BEIGE visuals)

… It may also have succeeded, if that’s the word, in stimulating the economy just in time to thwart inflation from returning to its 2% target. That comes through from the latest edition of the Fed’s Beige Book, a compendium of the conversations that its regional branches have been having with local bankers and business executives. It found that the economy had “expanded slightly,” and that pressure on wages was moderating. As the name implies, the hope is that a more impressionistic or subjective approach will lend itself to subtlety and muted colors. However, it’s possible to sift through the words to come up with harder measures of activity. This one, produced by Oxford Economics, reveals a considerable pickup in activity since the pivot:

Even the Fed itself now uses natural-language processing to drill deep into its Beige Books, and has found out that they mean something. A study by the Cleveland Fed shows that the compendium of anecdotes really does help to predict recessions. It also reveals, fascinatingly, that if the US avoids a recession, last year’s rise in negative sentiment will prove to be the worst on record that didn’t end in a downturn:

That helps justify last year’s pivot. It also suggests that it may genuinely have averted one possible negative outcome, and raised the risk of another. Improving sentiment had tangible results …

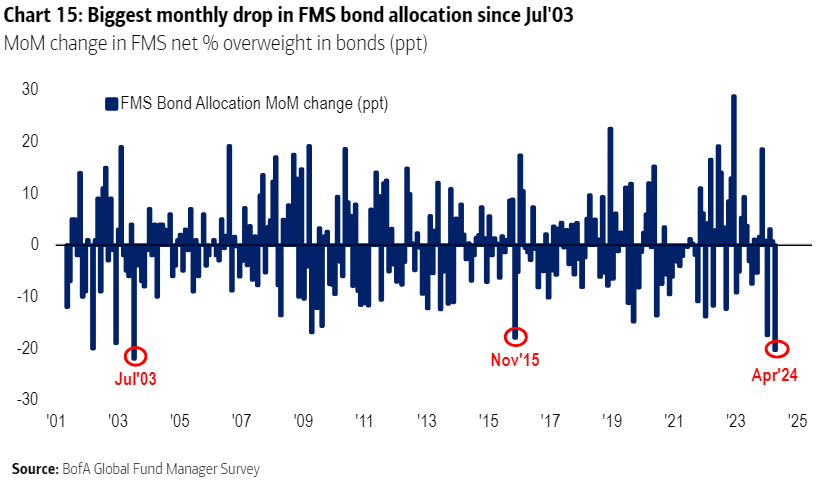

… Higher inflation is generally a good reason to get out of bonds, as the income they pay isn’t protected against price rises. The way investors have moved to exit bonds in the past month is startling. The last move of this magnitude to sell bonds was 21 years ago, in July 2003, as investors breathed a sigh of relief that the Iraq war was over and left their safe havens:

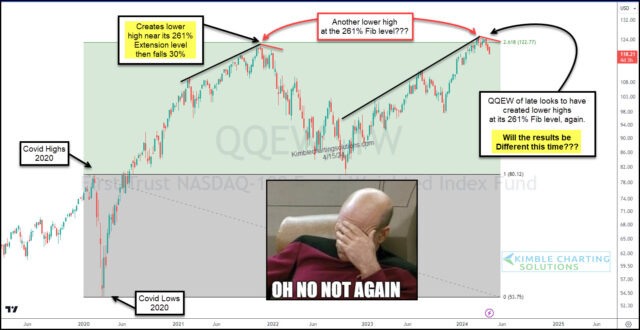

Kimble: Tech Stocks Struggling At Double Top Fibonacci Resistance!

… Finally, in the be careful what you wish for cuz you might just get it (-Everyone’s MOM) category, it’s absolutely devastating to see images from Dubai and the floods, is it NOT the very least bit ironic they ‘seed’ the clouds as they needs the rain and yet, no matter how much money and resources — AI and otherwise — in the region — still could not have seen this coming and were / remain woefully unprepared …

BizInsider: Photos show Dubai overwhelmed by torrential rain — and may expose the downsides of trying to control the weather CNBC: UAE government unit denies cloud seeding took place before Dubai floods Wikipedia: Cloud seeding in the United Arab Emirates

… You get the point unless, of course, you are thinking this was not a flaw but a feature? Anyways, do your own tinfoil hat research and come to yer very own conclusions but I cannot stress enough how very terrible it is. I get that. Have some friends that moved there chasing dreams (really following the money, uprooting entire family but hey, for the right price, apparently) and how it is said there are brightest bulbs, biggest thinkers and resources beyond imagination … and YET … this?

I think Dubia sent up like 4K drones into the heavens a yr ago to electrocute a Thunderstorm....I'd agree that our human urge to play GOD reaps unintended & undesired rewards...but never mind Cloud Seeding, how about them ChemTrails, I see them spraying all the time ESPECIALLY while skiing....oh yeah our dear Air Force went from steadfast DENAILS to in 2018 claiming they're ICE Crystals....in the SUMMER, problem solved....it's just like Economics....extend pretend and FABRICATE!

{kind=link}

I think Dubia sent up like 4K drones into the heavens a yr ago to electrocute a Thunderstorm....I'd agree that our human urge to play GOD reaps unintended & undesired rewards...but never mind Cloud Seeding, how about them ChemTrails, I see them spraying all the time ESPECIALLY while skiing....oh yeah our dear Air Force went from steadfast DENAILS to in 2018 claiming they're ICE Crystals....in the SUMMER, problem solved....it's just like Economics....extend pretend and FABRICATE!