Good morning … ALL views are created equally and we KNOW some are more equal than others and SO …

Bloomberg: Powell Signals Rate-Cut Delay After Run of Inflation Surprises

Fed chair said appropriate to give policy further time to work

Central bank can keep rates steady for ‘as long as needed’

WSJ: Powell Dials Back Expectations on Rate Cuts Inflation and hiring have been firmer than expected this year, weakening the case for pre-emptive rate reductions By Nick Timiraos Updated April 16, 2024 4:05 pm ET

… Team Biden and Team Rate CUT not gonna be happy when they learn of these remarks? As for the remarks impact …

… Yesterday's losses gathered pace as the day went on, but a key catalyst were remarks from Fed Vice Chair Jefferson. He said that “if incoming data suggest that inflation is more persistent than I currently expect it to be, it will be appropriate to hold in place the current restrictive stance of policy for longer. I am fully committed to getting inflation back to 2 percent.” So an explicit acknowledgement that further upside inflation surprises would lead to a longer period of restrictive policy. Later in the day, Fed Chair Powell echoed the risks of a greater delay to rate cuts, saying that the “The recent data have clearly not given us greater confidence and instead indicate that is likely to take longer than expected to achieve that confidence” in the path of inflation and noting that the Fed can keep rates steady “as long as needed”.

Those remarks saw investors price increased chances of higher-for-longer rates, with Fed funds futures now pricing only 40bps of cuts by year-end, the lowest this has been so far in this cycle. 2yr Treasury yields briefly passed 5% intra-day around the time of Powell’s comments, before closing +6.6bps higher on the day at 4.99%. And 10yr yields hit their highest level since early November (+6.5bps to 4.67%). Real rates drove the increase, with 10yr real yields up +8.0bps to 2.25%, but there were also rising market concerns about inflation. For instance, the US 2yr inflation swap (+2.2bps) reached a fresh one-year high of 2.68%, its highest level since the SVB turmoil back in March 2023… -DBs Early Morning Reid (April 17, 2024)

… and these words came just ahead of this afternoons ‘liquidity event’ (aka 20yr Treasury auction) and so a bit of a concession given yesterday and being taken away this morning …

20yy: bullish setup ahead of supply …

… and in other ‘Good’ news …

ZH: US Housing Starts Collapsed In March - Biggest Drop Since COVID Lockdowns

… GOOD in the eye of the beholder … AND then there was just some MEH news …

… AND I should have quit while I was behind and so, here is a snapshot OF USTs as of 704a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher this morning as some TSY benchmarks respect local support levels while the tactical short-base builds. We illustrate and discuss this below. DXY is modestly lower (-0.11%) while front WTI futures are lower too (-0.9%). Asian stocks saw gains in China and a mixed performance elsewhere, EU and UK share markets are all higher (SX5E +0.9%) while ES futures are showing +0.45% here at 6:45am. Our overnight US rates flows saw muted flows in Asia with prices spending much of that session around unchanged until they sagged at the crossover after the disappointing UK inflation numbers. During London's AM hours the desk saw more buying interest (3's to 7's) after the UK inflation-inspired dip. Indeed, the desk added: "Most real money accounts remain inclined to put cash to work at these levels despite the hawkish comments from Powell yesterday afternoon." The focus by fast$ has been largely on curve with some interest to flatten 3s5s and 2s10s this morning. Overnight Treasury volume was decent at ~120% of average with 3yrs (147%) and 5yrs (150%) seeing some relatively elevated turnover this morning.

… Our last attachment is way off-topic, but after reading about the emerging stresses/charge-offs in the credit card space... we thought we'd check in with the Fed data on banks' assessed credit card rates. 22.6%!? Sheesh.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities at session highs, Dollar softer & Gilts pare initial post-CPI weakness; Central Bank speak due … USTs incrementally firmer, Gilts gapped lower following hotter-than-expected CPI though have pared to near unchanged … USTs are firmer by a handful of ticks as the benchmark lifts slightly from Tuesday's Fed-induced hawkish action. Currently at a high of 107-25+ from Tuesday's 107-13+ contract low which was spurred by Fed speak.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

CitiFX: US yields: Stretching the resistance bands

US yields are testing key resistance levels. Despite that, momentum indicators show no indications of turning lower, suggesting we could still see even higher yields.

US 2y yields: Markets are testing key resistance at the ~5.0% handle (76.4% Fibonacci, November 27 high, psychological level). This is especially so, considering we saw a market indecision doji last Thursday.

Base case: While the resistance is strong, there are no indications at the moment that the move higher in yields will be contained - daily slow stochastics (momentum) remain firmly in overbought territory and we are not close to seeing a crossover back below.

Hence, we are slightly biased towards higher yields with subsequent resistance at 5.08% (November 2023 highs). However, we think it is unlikely we break above that considering attractiveness to Treasury dip buyers.

Case for lower yields: We are closely watching daily slow stochastics on whether we see a cross back lower from overbought territory. This has been an important indicator, averaging ~20bps retracement in the last 3 times we have seen it this year.

Source: Citi, Bloomberg (Click image to enlarge)

US 10y yields: Yields are testing 4.70-4.73% (November 13 high, 76.4% Fibonacci retracement), which we think will hold in the short term. However, the key point here is a potential weekly close above.

Why this is important: The 4.70-4.73% resistance band is strong, and we expect short term resistance at this level. However, IF we see a weekly close above, there would be no further strong levels till 5.02% (2023 highs).

DB: An un-happy meal - Food inflation and what it means for the US election

For the US consumer today, the exact same grocery basket is 21% more expensive relative to the start of the Biden administration in January 2021. To put this into perspective, under the Trump administration, the cost of the same basket of groceries increased less than 7%.

US government estimates have shown that food inflation is set to decelerate throughout 2024, but the cumulative effects of previous price gains means any further increases in food prices will be especially painful for already hard-pressed consumers, particularly for those in lower income groups. According to our proprietary dbDIG survey of US consumers, 61% of respondents are more than ‘fairly worried’ that the increasing cost of household groceries in the next three to six months would mean they will have to purchase less food for their household.

Food represents a material proportion of the day-to-day expenses of consumers, and therefore their perception of the ‘health’ of the economy. Despite the efforts made by the current administration in tackling the pandemic-induced inflation, food inflation remains significantly high relative to January 2021. Critically, the impact of this cumulative food inflation as well as an erosion in purchasing power may affect US voting decisions to the detriment of the current administration in the November 2024 US election.

… What makes this even more uncomfortable for US consumers is that up until 2022, the percentage of income spent on food in the US had been trending downwards since the 1960s due to falling prices for food consumed at home. But this trend was bucked in 2022 as consumers increased the average proportion of their disposable income spent on food by 13%, the sharpest annual increase on record. In fact, in 2022, US consumers spent an average of 11.3% of disposable income on food, the highest percentage since 1991. And according to our proprietary dbDIG consumer survey, the median spend on all food has again increased from 12% to 13% of income from 2022 to the first quarter of 2024.

Goldilocks: Industrial Production Increases on Stronger-than-Expected Manufacturing

BOTTOM LINE: Industrial production increased by 0.4% in March, in line with consensus expectations, and manufacturing production increased by 0.5% and was revised higher in February. Following today’s mixed data, we left our Q1 GDP forecast unchanged on net at +3.1% (qoq ar). We lowered our domestic final sales forecast by 0.2pp to +3.1% (qoq ar).

Following the higher-than-expected March CPI, we have pushed back our call for quarterly Fed cuts starting to July 31, with risks tilted to the later side. But we still feel comfortable with the disinflation narrative because of special factors in the recent inflation numbers, well-anchored inflation expectations, and continued labor market rebalancing. Elsewhere in G10, we expect the ECB, BoE, and BoC to start easing in June, with three consecutive cuts up front and a shift to quarterly cuts in Q4. Our monetary policy forecasts are even further below market pricing in EM. In China, we expect growth of 5.0% in 2024, slightly above consensus, followed by a gradual slowdown in subsequent years. Our baseline economic forecasts should be friendly for risk asset markets, but the combination of delayed monetary easing, high valuations, geopolitical turmoil (including ongoing escalation between Israel and Iran), and the impending US presidential election could keep the investing environment choppy…

UBS (Donovan): The problems with Powell (seems like he’s lobbying to be Fed chair? whatever the case, i’d say for better or worse, TODAY I happen to whole-heartedly agree with Donovan’s unfortunate message here …)

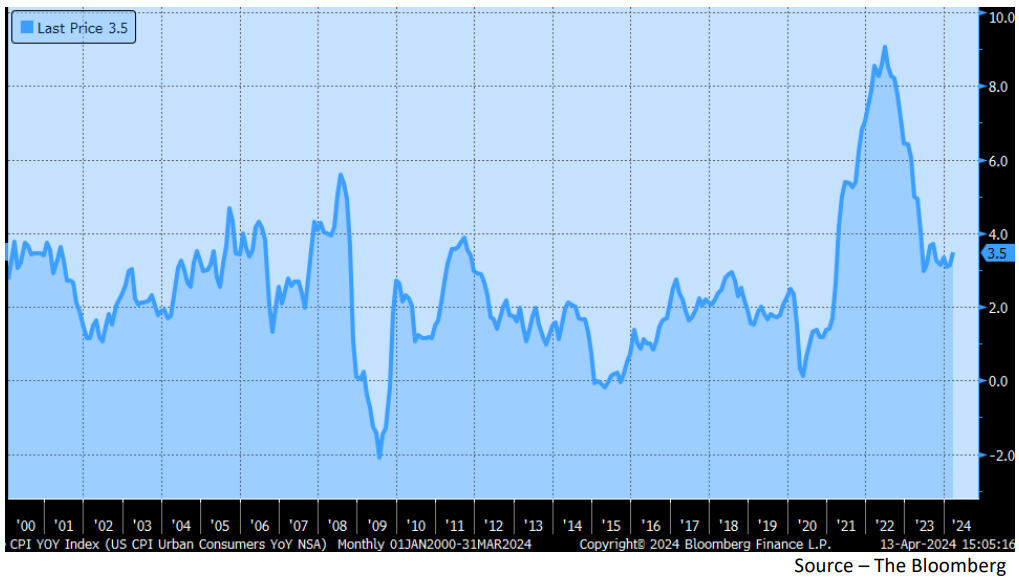

Federal Reserve Chair Powell is not an economist. Not everyone can be an economist, but central bank heads probably should be economists. Yesterday, Powell stated reaching 2% inflation was taking longer than expected. The US PCE deflator is 2.5% y/y, the core PCE deflator is 2.8% y/y, and harmonized inflation is 2.4% y/y. Imprecise data means most economists regard a 2% inflation target as meaning a 1%-to-3% range. The fictional owners’ equivalent rent may be taking longer than expected to reach 2%, but that is not the same thing as inflation.

Powell has never articulated a medium-term policy framework beyond “data dependency”. Keeping interest rates higher for longer will do nothing to reduce owners’ equivalent rent (it might increase it). Higher for longer might make durable goods deflation worse. There is a risk that Powell might be more concerned with political presentation than good economics…

Wells Fargo: Picking Up Off the Mat: Manufacturing Output Sees Second Month of Gains

After spending the better part of the past year in the doldrums, the factory sector is showing signs of life. Industrial production rose 0.4% in March, coming on the heels of an upward revision to February. The outturn marks two consecutive months of increases for the first time since early 2023.

It's official: Fed Chair Jerome Powell confirmed today that he and his colleagues aren't convinced that inflation is coming down fast enough to consider cutting the federal funds rate (FFR) any time soon: "The recent data have clearly not given us greater confidence and instead indicate that it is likely to take longer than expected to achieve that confidence," Powell said at a moderated question-and-answer session in Washington.

At the start of the year, market participants expected several cuts in the FFR this year based on the observation that once the Fed has stopped raising it, the rate was cut quickly or after a short pause in the past (chart). We've observed that in the past, the Fed cut rates in response to major financial crises, which haven't occurred so far.

Today, the 2-year Treasury note yield closed at 4.97%, while the 10-year yield rose to 4.67%..

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: Bond Crash Impacting A Portfolio Near You

… And if you’re looking for a catalyst, the Bond Market crashing is certainly one of them.

Long-term bonds went out at new 5-month lows yesterday, as this 4-year long crash continues.

Interest rates have been going higher.

I don’t know why people keep telling me that they’re going lower.

It’s weird, because it’s the exact opposite.

And you’re seeing that impact stocks on an individual basis as well. Small-cap Technology has been selling off all of 2024, already down 10% Year-to-date…

Bloomberg: What If The Fed's Hikes Are Actually Sparking US Economic Boom?

Bloomberg: Higher-for-longer is pushing Dollar Power to limit (Authers’ OpED)

Powell makes clear that the Fed won’t cut soon. The dollar is turning the screws, and markets and other central banks can’t keep up.

… His comments were definitely in a hawkish direction, and therefore stocks did close a little down for the day, while bond yields rose yet further. However, over the course of the day, the effect of his words (the point when his remarks went public is indicated by the red line in the chart) was muted. US markets already knew that inflation wasn’t low enough for the Fed to start cutting, so the latest Powellspeak didn’t make that much difference:

Convexity Maven - "Bedtime for Bonds" (basically vol DEAD buy new issue MBS thru his ETF)

NOTE: This Commentary has no math or formulas]

While never totally transparent, the medium-term path forward for interest rates is well lit.

Via a combination of Politics, the Data, the Calendar, and Hubris (human ego) the FED is boxed-in, and the most likely scenario is “one and done” until the election.

Today I offer a bedtime story of why selling interest rate Convexity via newly-issued MBS offers a better risk::return profile than taking Duration or Credit risk…

… This notwithstanding, at the time the FED had good reason to anticipate inflation stability near their professed target of 2.0%. This confidence was not pulled from their nether regions since their preferred inflation measure of -olajbogyo line- Core Personal Consumption Expenditures (PCE) had been bouncing around that level for the better part of two decades. [The “core” rate excludes the more volatile “food and energy” components are discarded.]

… Mr. Powell first discussed the concept of “transitory” in his June 22, 2021, testimony to a Congressional Oversight panel. Here, he was responding to the recently reported 5.0% year-over-year (YOY) increase in -felho line- Consumer Price Inflation (CPI).

While this may have been a sincere belief after the Covid tumult, I suspect it was also shaded by his desire to be nominated for another term as Chairman…

The TINY (#thereisnoyeild) market means that you can now get almost 4x the yield in Treasury Bills rather than US Large Cap stocks...in the last 100 years has only ever been the case in the Tech Bubble years

Anyone else notice Powell doesn't mention VOLKER near as often lately? I generally like Powell and am rooting for him, which makes this latest flip-flop-flip most unfortunate. Have learned there's lots behind the scenes going on for the important & powerful that we're ignorant of, I don't envy Powell's pressure from the likes of Brandon, Bernie, Warren, MIC, EU/NATO/Israel/OPEC+ etc.

Anyone else notice Powell doesn't mention VOLKER near as often lately? I generally like Powell and am rooting for him, which makes this latest flip-flop-flip most unfortunate. Have learned there's lots behind the scenes going on for the important & powerful that we're ignorant of, I don't envy Powell's pressure from the likes of Brandon, Bernie, Warren, MIC, EU/NATO/Israel/OPEC+ etc.

On the FoodFlation topic, told the cashier last wk that I like Cheap Food & never imagined eating Swansons TV dinners again....