Good morning … a couple / few things overnight which are helping shape shift this mornings rates price action, and for that, a check in with 5s (given JPMs focus - below) …

… I spy with my little eye a yield which appears to be overBOUGHT and, while the current (DOWN)trend in yields overriding the 2024 (UP)trend, a bit of a pause that refreshes might very well be in order. Especially as this holiday interrupted trading week of summertime gets underway. Throw in not much in way of data and … here are a couple / few of those ‘things’ to consider since we’ve left off …

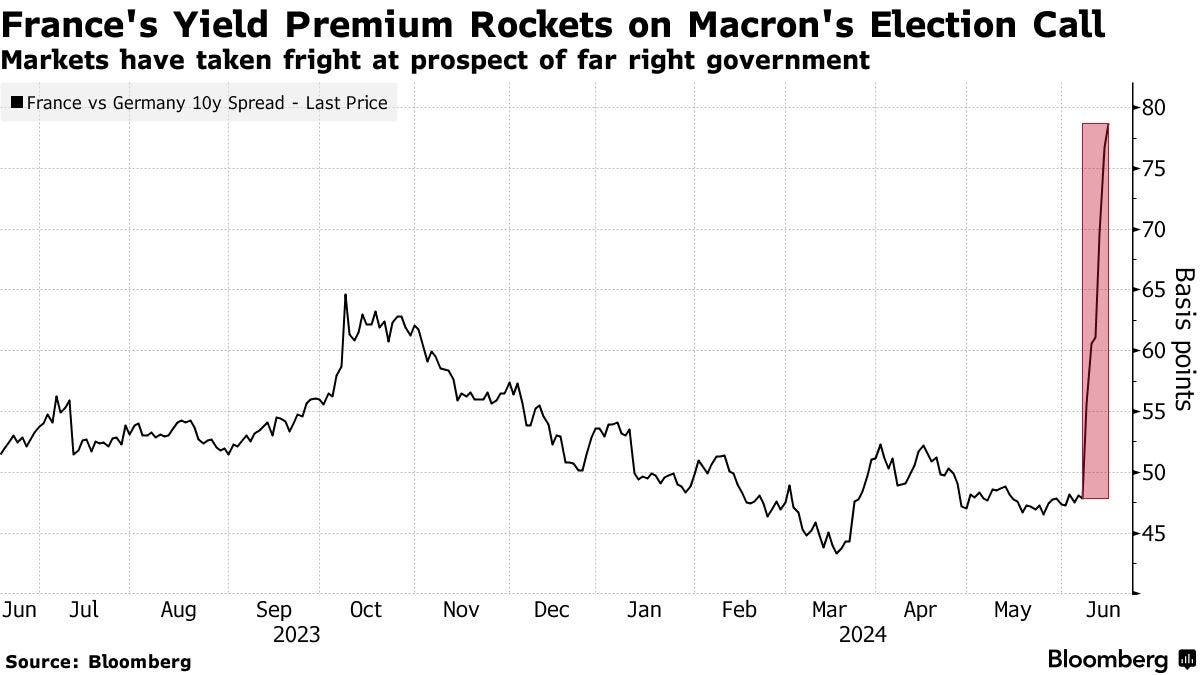

Bloomberg: French Bond Rout Pauses as Traders Assess Le Pen’s Reassurances

Stabilization follows worst week since 1990 for 10-year spread

National Rally leader tells newspaper she’d work with Macron

… The 10-year yield spread over safer German notes widened the most on record last week, according to data compiled by Bloomberg going back to 1990.

Still, the market remains fragile ahead of the first round of voting on June 30. As trading kicked off, the 10-year yield gap over German bonds grew to more than 80 basis points, the widest level since 2012 on a closing basis. While that largely reflected a change in the underlying benchmark bond and not a fresh bout of selling, strategists warned against chasing the move….

… and back onshore where non-voting FOMC member Ka$hkari took TO the weekend press …

Face The Nation: Minneapolis Fed president Neel Kashkari says signs "high-pressure" economy may be "cooling" (while noting REASONABLE to predict DECEMBER CUT -RTRS … but in his own words:)

…drivers as always from near and back to FAR (east) where…

Reuters: China fails to cheer, as France scores own goal

A muted start to the week in Asia with Chinese data too mixed to provide much momentum as political uncertainty in Europe lurks in the background.

At least Chinese retail sales topped forecasts with a rise of 3.7% on the year, likely boosted by the May holidays, but industrial output and fixed-asset investment both underwhelmed…

… here is a snapshot OF USTs as of 730a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are cheaper and steeper on 105% 30d volumes, flows more balanced amid some relative stability in French assets, better duration selling seen from real$. Bund gamma is still a bit better bid (opened +4nv), while France-Gmy is 3.5bp wider in 10y, and EUR itraxx is a tad wider as well. Risk-off was seen in APAC bourses too (NKY -2%, -0.5% KOSPI, SHCOMP -0.6%). Commodities are a tad weak: CL -0.1%, HG -1.6%, XAG -1%. FX majors are largely flat, while Eurostoxx futures are +0.4% and S&P E-minis are -3pts here at 7:15am.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures tentative, Dollar flat & Antipodeans lag after mixed Chinese data … Bonds are subdued paring recent EU political-induced upside on Friday, as participants digest ECB sources which suggest that the Bank is in no rush to discuss a French bond rescue … USTs are incrementally softer, paring some of the pronounced gains seen on Friday. Today's focus will be on Fed's Williams, Harker & Cook, where remarks will be scrutinised to see where they place their dots and how much sway, if at all, May's CPI had on them. In narrow 6 tick parameters; yields bid across the curve which is ever so slightly flatter thus far.

We do not think the recovery in retail sales will be sustained, given fading one-off boosts, a deteriorating labour market, and financially constrained households. We think the housing sector is yet to bottom, remaining the largest drag on growth. Infrastructure investment is also slowing amid rising risk scrutiny.

BNP: Sunday Tea with BNPP: Politics remains centre stage

KEY MESSAGES

The surprise announcement of a snap parliamentary election in France has introduced uncertainty into European asset prices with the risk premium now in line with previous presidential elections. We have gone short EURJPY and re-entered a 10y cross-Atlantic spread.

Last week, lower US inflation was welcome news for the FOMC but the hawkish surprise on the committee’s 2024 dot plot supports our view that the Fed will wait until December before commencing its rate-cut cycle.

… We continue to expect the Fed’s first rate cut of this cycle to be seen in December. The Fed’s forecast implies an average monthly pace of inflation for the rest of the year of just under 0.2% m/m – in line with our own forecast for inflation. As a result, absent a more significant deterioration of the labour market, we think the Fed will opt to cut once in 2024, most likely at the last meeting of the year.

In terms of US yields, we think the environment is now more favourable to buying the dips in the US 10y, towards the high-end of our 4.20% to 4.60% fair value range.

We think the Swiss National Bank and Bank of England will keep their respective policy rates on hold this week.

China's economic activity softened in May. Underperformance came mainly from a 1.1ppt drop in industrial output growth to 5.6%, as well as a further slowdown in fixed asset investment to 4% ytd YoY. Property sales, prices and housing new starts all dropped further despite the government's renewed policy support since mid-May. Meanwhile, consumer demand have improved modestly with retail sales and services output growth both rebounding from their April lows, but their improvements were not sufficient to offset the deceleration from other sectors. At the aggregate level, we estimate output growth slowed to 4.7% YoY in May from 5.1% in April and 5.3% in Q1. We see downside risks to our Q2 (5.5%) and 2024 full year (5.2%) GDP growth forecasts.

Today's FICOTD looks at two different metrics to gauge the extent of contagion stemming from the widening in OAT spreads…

… The second is the ECB’s systemic risk indicator, which is calculated across rates/ equity/money market/fx. It is a day lagged - a significant negative when conditions are rapidly changing - but again would still send the same signal. It is unlikely that Friday's price action has moved the needle enough to change the message. If anything, some of the widening has unwound at the time of writing.

Treasury yields retraced to their lowest levels since March, supported by benign inflation data, renewed political risk in Europe, and a dovish BoJ

We think Treasury yields are likely to remain rangebound through the summer. On one hand, this week’s data should allay fears that inflation is reaccelerating, and leaves the door firmly open to lower rates later this year. However, the Fed is in no rush to ease, and if the first cut is indeed months away, it will be challenging for yields to decline further over the near term

Though the environment supports carry trading, risk adjusted-carry is pretty low and the 5-year sector is trading near the richest levels on the fly YTD: take profits on 3s/5s/7s belly-richening butterflies

With yields at multi-month lows, OAT/bund spreads priced for a more negative outcome, and next week’s retail sales likely to show a healthy bounce, we turn tactically bearish in the 5-year sector …

… Sell 100% risk, or $50mn notional of T 4.5% May-29s (yield: 4.227%; bpv: $446/ mn) - Yield is 4.227%. One-month weighted carry is 2.1bp and roll is 0bp …

MS: Sunday Start | What's Next in Global Macro: AI and the Credit Markets

… The bottom line: As AI-driven technology diffusion takes center stage, credit markets, broadly defined, will likely play a growing role. As always, there will be winners and losers, but AI as a theme for credit investors is here to stay.

With the Fed and ECB's June meetings behind us, we discuss why the ECB cut ahead of the Fed, and the paths forward.

… How could we be wrong on our outlook for these two central banks? Inflation is the clearest path. Both economies had some upside inflation surprises this year that caused the market to reconsider the path. Noisiness in the data helps to explain both the delay in the Fed’s cutting cycle and our view that the ECB will only cut at projection meetings—both central banks are data dependent these days. For the ECB, we could also be wrong if the growth data continue to surprise to the upside. The ECB revised up its growth forecast for this year, and sees growth next year slightly above potential. But it continues to see inflation at the end of 2025 at target, and for 2026, even a touch below. Typically, inflation projections reflect growth expectations from a year earlier, so if incoming data push the forecast for next year’s growth notably above potential, then the inflation path would likely also be revised higher, and the prospects for cuts would come under more scrutiny.

Consumer price disinflation is raising expectations for a Fed rate cut, which is fueling a meltup in stock prices. This morning on CBS' "Face the Nation," Minneapolis Fed President Neel Kashkari said that a rate cut by year-end is a “reasonable prediction.” On Friday, the 10-year Treasury bond yield fell below 4.25% to 4.20%. The technical picture is signaling that it might continue to fall down to 4.00% in coming days (chart).

The prospect of lower interest rates is fueling momentum investing (chart). Leading the momentum meltup are technology companies that are associated with artificial intelligence…

The Fed’s pivot from hawkish to dovish and associated easing in financial conditions have boosted expectations for US consumer spending, see chart below.

Bloomberg: For Bond Traders, Data Matter More Than What the Fed Is Saying

Treasuries rally as soft inflation data bolsters rate-cut bets

Fed expectations downplayed as economy keeps defying forecasts

The US bond market is driving home a lesson about the new world investors are living in: The data matter far more than anything the Federal Reserve might say.

That was on stark display Wednesday, when a softer-than-expected rise in the consumer price index that morning set off one of the biggest Treasury rallies of the year.

Less than six hours later, after the Fed’s latest economic projections penciled in just one rate cut this year, the rally faded a little. But it revived Thursday as an unexpected drop in producer prices and a rise in jobless claims suggested inflation pressures are continuing to ease. The 10-year yield ended Friday near 4.2%, down 21 basis points in the biggest weekly drop since mid-December.

In short, the dovish inflation data drowned out any hawkish sounds from the Fed.

The movements underscore the diminished significance of the Fed’s guidance at a time when the economy keeps surprising virtually everyone, including central bank policymakers themselves. Fed Chair Jerome Powell at last week’s post-meeting press conference acknowledged as much, saying that the Fed is mindful of going where the data leads.

That means the bond market is likely to continue on a rather bumpy path as the interest-rate outlook is reassessed whenever key data arrive.

Policymakers “are going to talk, but the market needs to discount more than usually what they say in this environment,” said Jean Boivin, head of the BlackRock Investment Institute. “This environment is one where there is excessive response to incoming macro data.” …

Sam Ro fro TKer: 6 charts that help explain why stocks keep going up

Looking Back to 1968 and Forward to What Might Lie Ahead

Jeffery Gundlach

I was 8-9 years old......I do remember the turmoil and anxiety, that was in the air......

https://youtu.be/Gg0qF2r9T1c?si=qYBi85R_dhsXHcY8