weekly observations (06.17.24): some gettin' SHORT 10s others sellin' to get FLAT;'2-year T-Note yield says that the Fed Funds target rate is more than half a point too high.'

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP lets have another go at finding a(nother?)most interesting chart …

20yy — given this coming weeks liquidity event, I spy with my little eye momentum that is leaning towards, but not yet extremely, overBOUGHT on a WEEKLY basis …

… but on a DAILY basis, perhaps more clearly in need of a concession to price this weeks supply unless, of course, you are thinking / more concerned with disinflation and a card carrying member OF Team Rate Cut …

Next up, lets deal with a couple / few items of interest from yesterday helping understand how it is we got ‘here’, a week AFTER a confusing NFP and a week with supportive CPI, FOMC and PPI …

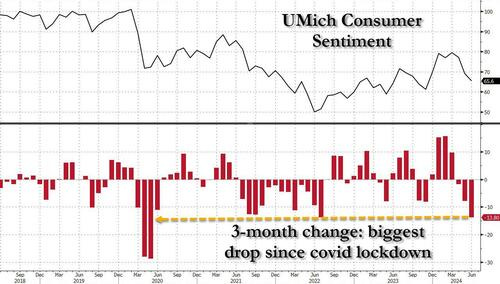

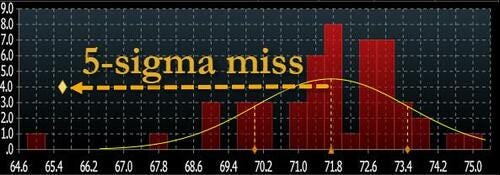

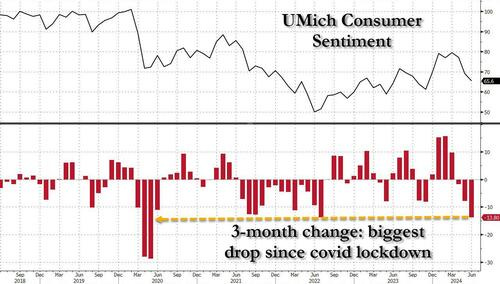

ZH: Bidenomics Implodes: Consumer Sentiment Unexpectedly Slumps To 7 Month Low In 5-Sigma Miss

…One month after the May Consumer Sentiment printed at a record 7-sigma miss to expectations, consumer sentiment once again "unexpectedly" slumped, this time from an upward revised 68.8 to 67.6, the lowest print since last November, and the biggest 3-month drop in sentiment (-13.8 points) going back to the covid lockdowns.

... which was not only a 5-sigma miss to the median estimate (an improvement from last month's 7-sigma)...

... but also the biggest miss of 2024.

The collapse in sentiment was broad based, and hammered both current conditions - which plunged from 69.6 to 62.5, the lowest since 2022 and badly missing estimates of 72.2 - and also expectations, which dropped from 68.8 to 67.6 (and also far below the 72.0 estimate).

… and from near / dear to far away places where lots of strife bubbling underneath surface of markets …

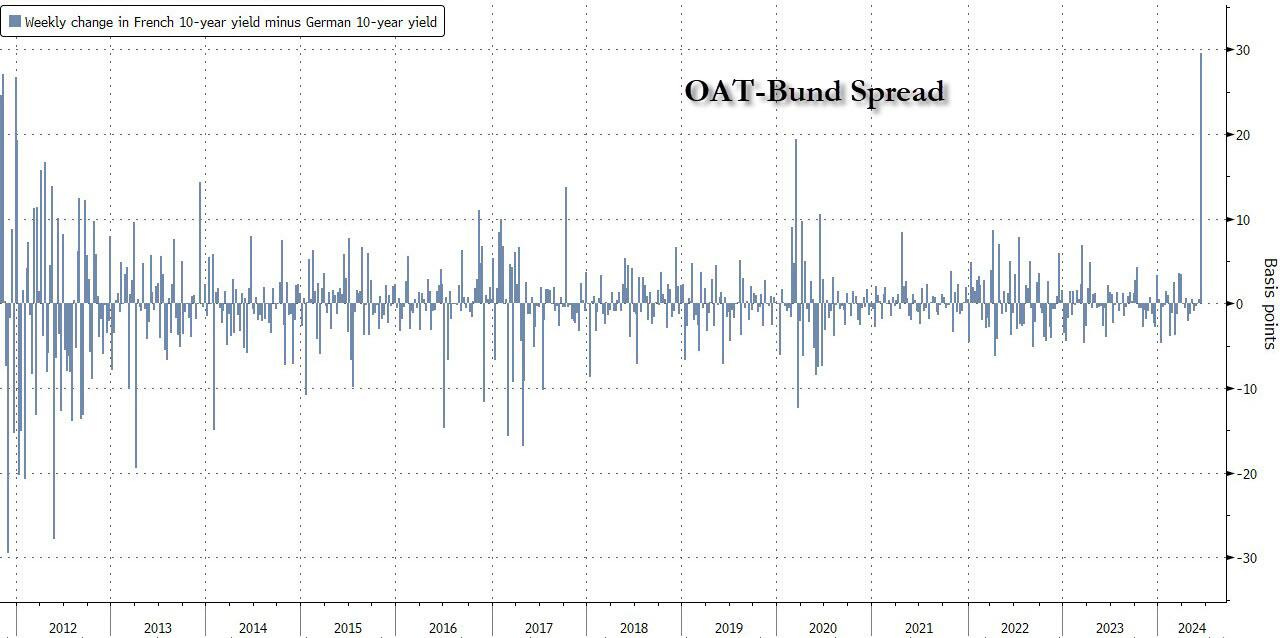

ZH: French-Bund Spread Blows Out Most On Record As Market Braces For Return Of European Debt Crisis

… But if stocks were hit, the bond market was absolutely crushed: French 10-year bond yields (OATs) over their German Bund counterparts, just jumped by a record this week as the two bonds diverged with a thud.

According to Bloomberg data, the OAT-bund spread widened 29bps this week to 77bps, the highest since 2017!

The prospect of the far-left getting a sway over policy has rattled investors in the past. When polls in 2017 showed the presidential election could end up as a head-to-head between Le Pen and Melenchon, French debt sold off sharply, quadrupling its premium over safer German peers in a matter of months. This time is even worse, with S&P downgrading the French credit rating from AA to AA- citing larger-than-expected deficits and political fragmentation as reasons for the downgrade…

… Ok SO some data that will not deter any / either view and some inputs from near as well as far. Lots to consider into the days and weeks ahead with a couple holiday shortened weeks to look forward to, I’ll move on AND right TO some WEEKLY NARRATIVES … a handful of some of THE VIEWS you might be able to use.

BARCAP Global Rates Weekly: Data speak louder than words

In the US, while inflation progress may allow for a cut, the totality of data argues against the meaningful cumulative easing that is priced in. We recommend shorting 10y USTs. In Europe, French political uncertainty is weighing on OATs. In Japan, initial focus is on the MPM and if the BoJ sets the stage for a July hike.

United States: Interest Rates Data speak louder than words We recommend shorting 10y US Treasuries. While inflation progress may allow the Fed to cut, the totality of data argues against the meaningful cumulative easing that is priced in. Incoming data are likely to show a rebound in activity, rather than a slowing as the consensus expects. We take profit on 5s30s curve steepeners.

… Market Implications: Short 10y USTs; take profit on 5s30s steepeners

… First, as noted above, we believe economic activity is likely to rebound, surprising the consensus to the upside and leading to higher rates. The consensus has consistently been too negative on the economy, expecting a slowdown that has failed to materialize ( Figure 17). Data surprises have been negative over the past month, but some of the soft data are turning (eg, NFIB survey) ( Figure 18). We expect the next week's retail sales report to show a pickup in consumer spending based on real-time transaction data. In a similar vein, inflation markets have already taken a strong signal from the recent data, with y/y CPI inflation priced to fall to 2.3% over the next year and rebound only slightly to 2.4% over the subsequent year. Overall, we see risks as skewed towards upside surprises.

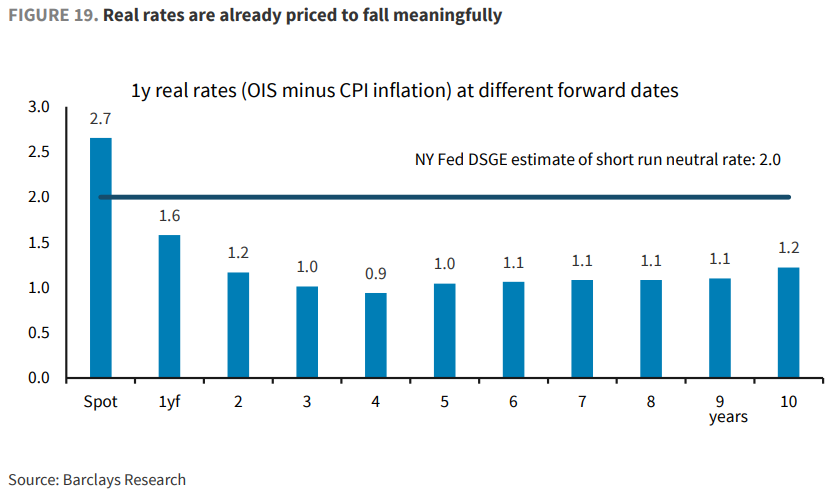

… Second, markets have already priced in a meaningful decline in the real policy rate to well below the current estimates of the short-run real neutral rate. In Figure 19, we show 1y real rates at different forward dates (estimated as 1y OIS minus 1y CPI swap rates)…

…Third, the term premium has room to move higher, and the CBO's update to its deficit outlook next week should provide a catalyst. Before the GFC, there was a meaningful slope at the back end of the SOFR curve that is currently missing ( Figure 20). In Figure 21, we provide a scenario analysis for back-end SOFR rates using various assumptions about the long-term neutral rate and term premium…

… We believe a material worsening in deficits is likely to put into question the time line and the magnitude of the eventual increases in auction sizes that is required…

…Finally, leveraged positioning has exacerbated the rally, and while it is still short-duration, in our assessment, it is less so than earlier. In Figure 22, we show an empirical estimate of the duration of macro hedge funds/CTA investors (proxied using the HFRXM Index) by regressing daily returns on yield changes and risk asset returns. The exponential weighted index puts more weight on recent data points in the regression. As can be seen, short positioning has been pared back quite a bit, which suggests short covering has played a role in this rally. Negative data surprises still have the potential to be exaggerated, but less so than earlier.

… Treasury liquidity: It's not what it looks like Discussions have surfaced around Bloomberg's index that shows liquidity conditions in the Treasury market have weakened to around GFC levels. However, Barclays' equivalent metric does not show a similar increase. We believe liquidity conditions are not as bad as implied by the Bloomberg index .

… Resilience means FOMC can wait Inflation was surprisingly soft in May, keeping the possibility of Fed cuts on the table for later this year. With the latest activity data reiterating the economy's resilience, the FOMC seems inclined to err on the side of caution, signaling only one cut this year. Indicators point to strengthened data next week…

BMO rates weekly, “What Happens in Paris...” (interesting to see EZ geopolitical scene rise in importance from best in the biz…who, by the way, booked prof on remaining long 10s, entered tactical 2s10s flattener and booked THOSE profits, too … this week again looking at 2s10s flattener as well as looking to get short 5yr BREAKS)

… At a minimum, we suspect that concerns regarding a wholesale deleveraging into the end of the quarter will persist into the week ahead, which contains remarkably little other incoming information from which to derive a trading bias. The adage ‘never short a quiet market’ remains all the more apt when the primary source of tradable headlines will come in the form of the debate between the French far-right and far-left. We’re reminded that financial markets have a strong tendency to see fire when it’s actually just fog... not smoke. This nonetheless will detract from the skittishness of the US rates market that also has the backing of an unexpected jump in initial jobless claims, a softer inflation profile, and a Fed that has made it clear that cuts are coming, even if the first move is delayed until the December meeting. We still see a reasonable path to a September cut on the inflation data alone, to say nothing of a downshift in the employment market or further contagion from the discord in Europe.

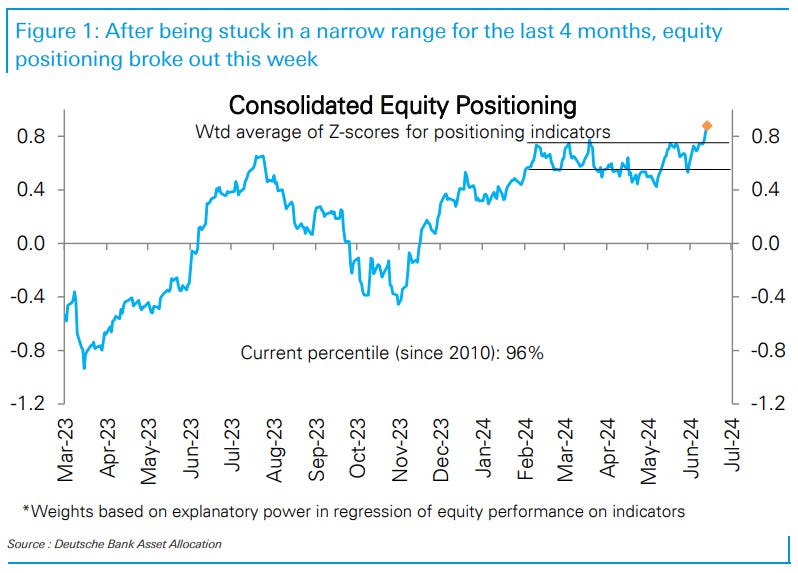

DB: Investor Positioning and Flows - Ratcheted Higher

After four months of being stuck in a narrow range, our measure of aggregate equity positioning broke above it this week, jumping into the top decile. It is now at its highest since November 2021, albeit still below and within its long-run band (z score 0.88, 96th percentile). Discretionary positioning drove the jump this week (z score 1.03, 96th percentile) while systematic strategies positioning was largely flat (z score 0.75, 85th percentile). Nearly all the underlying components of our aggregate measure are now above average. Across sectors, positioning in MCG & Tech rose sharply, as did that for the rate sensitive Utilities, Staples and Real Estate sectors, while the rest saw declines…

…What does elevated positioning mean for equity returns? Equity positioning is clearly quite elevated. However, it has not risen in a vacuum and largely reflects earnings growth which accelerated into the low double digits in Q1. At these levels positioning has historically still been commensurate with continued upside for equities. However, a further increase will take it to more than 1sd above average, a level that has previously been associated with a significantly wider band of forward returns, i.e., equity positioning and equities would become far more vulnerable to negative shocks (Positioning And Forward Returns, Jun 2020)…

MS: Friday Finish – US Economics: With Inflation Falling, So Should Rates

Inflation is falling, and the economy is slowing. To balance the risk of holding the policy rate too high for too long against the risk of cutting too early, the FOMC should act sooner than later. Chair Powell can dart nimbly around the incoming data should financial conditions ease too much.

MS: From the Grind to the Unwind | Global Macro Strategist

Recent political events led to price action, suggesting unwinds of popular carry trades in Mexico and France. While the domino effect may be contained for now, we caution against adding to popular trades like US yield curve steepeners, which could be at risk if economic activity data disappoint.

Global Macro Strategy We discuss worrisome signs involving politics and fiscal deficits and how these coincide with an increasingly downbeat US consumer, a smaller US cash flow deficit relative to last year, and no additional banking system liquidity – leaving us cautious on risk. We also discuss how the US election may affect US rates, and how the French and US elections skew the risks toward a lower EUR/USD exchange rate.

Interest Rate Strategy In the US, we exit long 3m10y receivers and receive July FOMC OIS swap at 5.31%. In the euro area, we maintain our structural receive EUR 1y1y and maintain our long ERZ4 97.125 call. In cash, we maintain our 2s10s BTPs steepeners vs. Bunds. In the UK, we maintain SFIU4/U5 flatteners, and keep our pay 5s10s30s SONIA fly and short 15y ASW positions. In Japan, we shift from long 10y JGB ASW outright to 5s10s ASW box flattener. We also shift from long 20y JGBs on 10s20s30s fly to 5s20s30s fly. We maintain pay 10y on 2s10s20s fly…

…United States …Four reasons to stay tactically neutral on duration:1) Retail sales could look healthy, 2) Yields are at the low end of their recent range, 3) Summer seasonality/carry can lift yields higher, especially because the Fed is in wait-and-watch mode, and carry for being short has increased, and 4) With the first 2024 Presidential debate 2 weeks away, term premium expansion might be on the market's mind. We closed our long 3m10y receivers after the June FOMC meeting, and suggest receiving July FOMC OIS as an attractive risk-reward (3bp spent for 22bp payout).

We have held TIPS as a most preferred allocation for close to a year. At the end of August 2023, there was a material differentiation between what the market was pricing for current and for future inflation expectations.

In April, we extended our interest rate exposure in TIPS from the 5Y area of the curve to the 10Y area.

With nominal and real interest rates moving lower since our extension, we are taking the gain and closing the allocation. We continue to anticipate that the recent downward trend in inflation will continue. • While we believe real yields are in restrictive territory and that they will decline into the end of the year and into 2025, they are less attractive today versus their nominal counterparts.

Wells Fargo: Still in a Slump: June Marks Third Straight Slip in Consumer Sentiment

Summary Today's softer-than-expected reading puts consumer sentiment at roughly the midpoint of where it has been over the past two years. The growth in prices may be coming down, but prices are not and that is weighing on households, particularly those in the middle most apt to feel the squeeze.

… AND moving along TO a few other things widely available and maybe as useful from the WWW

AllStarCharts (June 7th) Investors Ice the Bond Market Rally (reprise just cuz it was but a week ago the group of so called all stars noted clear disdain for buyin … which, in hindsight, would have been not a good, a GREAT trade … )

… T-bonds also broke above a key polarity zone, triggering our buy signals from last month:

I’ve made clear my disdain for buying treasuries, so the long bond trade will likely be a winner. After all, the best trades are often the hardest to take…

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

AT JayKaeppel

I am NOT a “bond bull.” I am just a speculator considering a reasonably sized (i.e., small) position in TLT call options. Could bonds tank? Absolutely. Hence small speculation, not "loading up." Not advice, just one point of view from a market-addled mind.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

THAT is all for now. Enjoy whatever is left of YOUR weekend and a very happy fathers day to one and all, especially Mine (talk with you tomorrow, Poppy) …