Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP Im gonna just say that if yer NOT confused by now yer NOT paying attention. There was plenty in that jobs report for every single view you might have…

ZH: Inside The Most Ridiculous Jobs Report In Years

… I GET ‘IT’ — desire for focus on revisions, foreign born workers and the general pre - election farce / forces at play which may / may not represent Bidenomics shenanigans at work here — I will not wade into those waters.

ZH has plenty of the details and QUESTIONS which need be answered (how could such a good report come with an increase in the URATE, for example … here’s another for you to ponder — how could the ECB cut rates and INCREASE their inflation f’cast??)

My station in life is not now, and never was, to question the data, but rather to skate to where ever the (rates market)puck is gonna be.

Despite or because of data (and all it’s misgivings).

At the turn of the year, bond jockeys priced 7 cuts.

Now we’re seeing folks reiterate July start to cuts, a faster pace and accelerated end, and / or stick to their calls of only 1 cut but later on AFTER the election.

Team Rate Cut has many allies and frankly, I know many of them, and they are all lovely people. Many have Bloomberg terminals and so, a better ability to review the data and economically workbench it, than I.

Stock jockeys are able to see past news — strong / good data and weak / bad data — and see rate cuts as the answer regardless. At the same time, rate cuts may NOT be the answer and the conclusion always arrived at IS … stocks for the long run. How many rate cuts? Who cares … don’t matter. Until it does.

What I can say is that when it DOES matter, it will be when the economy is faltering and having ‘the flation’ will be an actual desired thing — can you image hoping for ‘the flation’??

That time will come and we’ll be longing for it but for now, well, it doesn’t seem to me to be the case.

The higher income bucket has $$ to invest (NVDA, mmkt mutual funds, GME or whatever else roaring kitten is selling), while the bottom, well, ‘the flation’ is killin’ ‘em.

Rate CUTS don’t seem like the answer and the ECBs action in the week just passed really has ME struggling.

Cutting rates while forecast for HIGHER ‘flation … dunno. Something ELSE at work here and doesn’t feel right. My HOPE and, if asked, my guess would be the Fed is NOT about to cut rates in the week / month ahead. No June / July CUT then elections become more a topic.

Having been fooled back in ‘the day’ by Team Transitory only to realize AFTER the fact how powerful politics are, well … I’m grateful i’m not walkin’ a mile in their (policy makers, investors, traders) shoes.

Lots of moving parts — as always — and the narrative will change again along with the wind blowing now back in favor the GDPNows sails … click the link, check out the chart as GDP hooking back UP …

… Latest estimate: 3.1 percent -- June 07, 2024

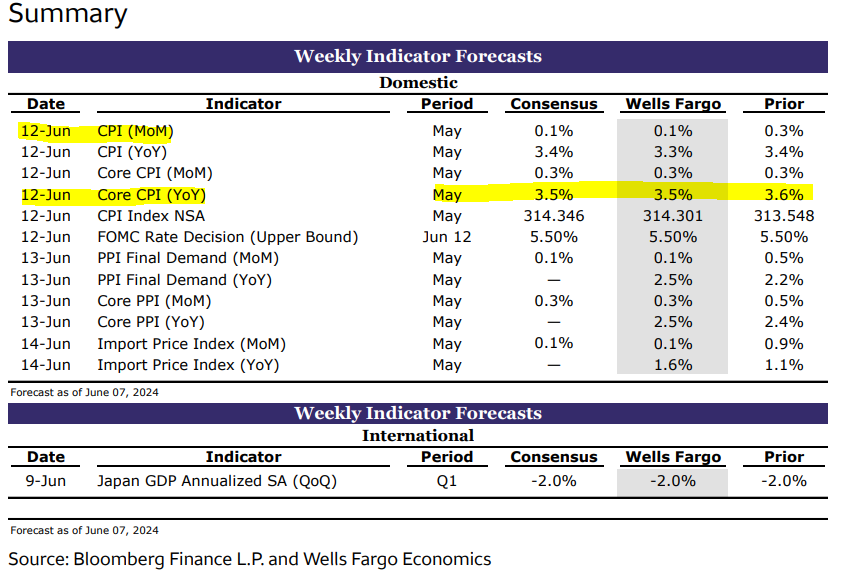

… and bonds, well, the bond market reacted BUT … It has spoken and the Fed and pundits are all listening ahead of the CPI and FOMC (both, conveniently on June 12th!). Reflexing to strong data and in some context … the moves seem tilted still favoring Team Rate CUT.

QUESTION: What happens IF Fed pulls an ECB? Cuts with ‘flation running too hot.

3yy WEEKLY: momentum NOT overSOLD and rates remain below ‘24 uptrend

10yy WEEKLY: same as above … UPTREND broken and a new downtrend …

30yy WEEKLY: watching 4.427 — most interesting level IMO

… In sum total a bit of an intraday(s) concession FOR supply, CPI and FOMC might very well be required especially in light of NFP — right or wrong as there was plaenty for Team Rate Cut to sink their teeth in to … Charts above are offered with a large grain of salt AND on the heels of CitiFX levels noted HERE, yesterday.

Get yer bids in Chicago style (or perhaps Michigan style), EARLY AND OFTEN.

NOW, lets deal with a couple / few things items from yesterdays NFP report where there was clearly something for EVERYONE (and as always, just depends on abilities and tools to dig/shape-shift and economically workbench the data to show it) …

Bonddad: Houston, we have a serious problem: the two job surveys show two completely opposed economies

ZH: May Payrolls Soar 272K, Above Highest Estimate, As Wages Come In Red Hot

ZH: Payrolls Instant Reaction: A Schizophrenic Report (Peter Tchir after his f’cast UPDATE)

… Ok I’ll move on AND right TO some of THE VIEWS you might be able to use. Here a couple / few things which stood out to ME …

ABNAmro: Update on our Fed and ECB views | Insights newsletter

We have made some changes to our Fed and (more modestly) ECB views. In this note, we set out the changes as well as the implications for our rates forecasts. The first Fed cut is now seen in September, with a slower pace of rate cuts initially. We have removed a July ECB rate cut from our base case, but see rate cuts at each meeting after that. Bond yields have been revised higher, but they are still seen dropping, with curves steepening.

Payroll employment increased a strong 272k in May, surpassing expectations, while the unemployment rate ticked higher by 0.1pp to 4.0%, and the participation rate ticked lower. This bolsters our conviction that underlying growth conditions remain resilient, and we retain our baseline call for just one rate cut in 2024.

… US Outlook Resilient resilience The rebound in payroll employment, wage growth and income in this week's employment report suggests that the resilience narrative remains intact despite diminished labor market dynamism. With data downplaying risks to full employment, we expect next week's dot plot to show just one cut in 2024 as the Fed waits out inflation.

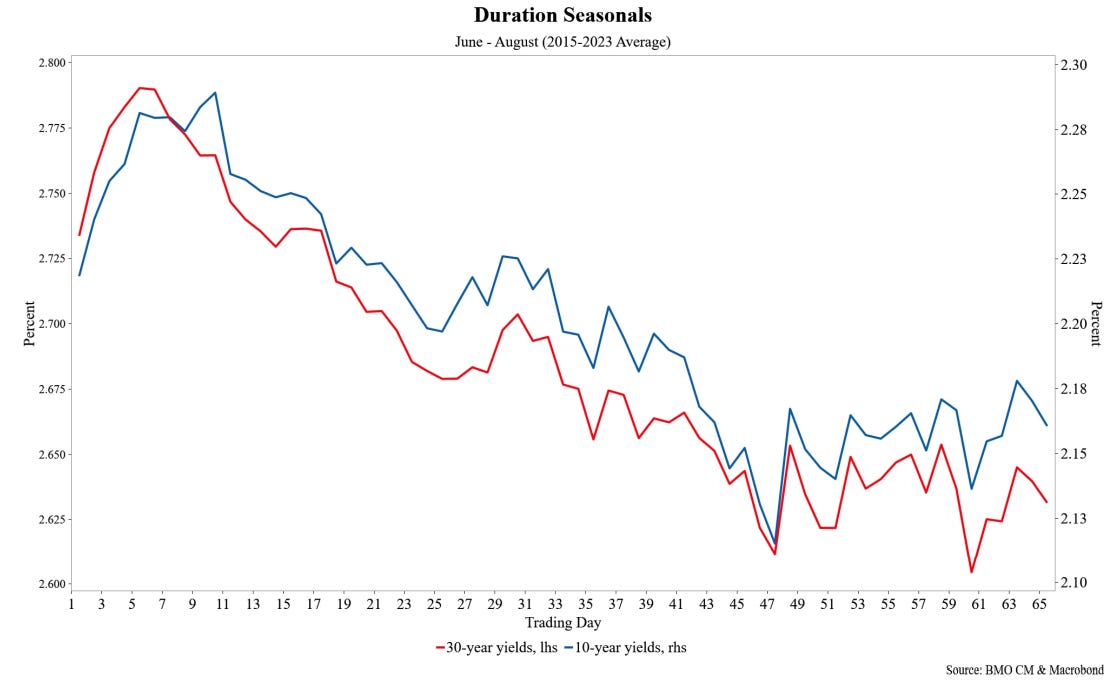

BMO: Sizing up the Seasonals (best in biz here … some NFP thoughts and … SEASONALS .. also note - booked SOME profits on LONG 10s at 200dMA - 4.348 - looking to 4.25% to sell rest … will look to CPI to get into 2s10s flattener IF kneejerk steepening provides opportunity … )

…The setup in the Treasury market for the employment report left ample room for a selloff that didn’t do any damage to the technicals. 10-year yields remain comfortably below 4.50% and the 2s/10s curve is in the -40 bp to -50 bp range. While the implied probability of a September cut slipped to ~50/50, the September 18th meeting remains far enough away on the horizon to be in play unless and until there is greater confidence that inflation has finally convinced the FOMC to begin lowering rates. The biggest takeaway from NFP was that the odds just dropped that the employment half of the Fed’s dual mandate will be what eventually drives the FOMC into rate cutting mode. In short, the onus is squarely on Wednesday’s inflation data to either justify or materially challenge the potential for a third quarter rate reduction…

… Charts of the Week In pondering the direction of yields over the summer months, the relevance of seasonal factors comes increasingly into focus despite the fact that the implications of supply, monetary policy, and global growth and inflation expectations will remain far more impactful drivers of the direction of rates. While the impact of summer trading conditions may be lessened in the current stage of the rates cycle, we would be remiss to entirely overlook what historical trends imply about the direction of yields over the coming months. In light of this, our charts of the week offer a simplified look at what recent years imply about the path of rates between now and Labor Day…

… Our second chart shows summer month seasonality for 10- and 30-year yields from 2015 to 2023. There is a clear bias toward lower rates from the beginning of June to the end of August – although it's notable the downward trajectory begins to stall as Labor Day approaches during the final weeks of August.

Significantly stronger-than-expected payrolls in May coupled with an increase in the jobless rate is consistent with continued rebalancing in the US labor market, not deterioration.

The report will reassure Fed officials that they can remain patient in waiting to see sufficient progress on inflation, in our view.

Despite the unemployment rate rising, the speed of increases in the jobless rate is insufficient to trigger the Sahm rule.

We expect US core CPI to rise by 0.3% m/m for the second straight month in May, providing further signal that inflation is coming off its Q1 hot streak.

After downshifting over the past several months, we think housing inflation likely remained at April’s run-rate in May, with the next leg lower coming in Q3.

We see risks as largely balanced, with projected flat used vehicle prices leading to higher core goods inflation than in April versus a potential cooling in monthly inflation in several service categories.

The Fed will likely welcome the May pace of inflation as it did the April data. However, we think the Fed will want to see multiple more months of similar data before seriously entertaining a rate cut.

Though May headline (272k) and private (229k) payroll gains meaningfully outperformed consensus estimates, they were moderately above their six-month averages of 255k and 202k, respectively. Adding to the strength of the report was a 0.4% gain in average hourly earnings while hours worked (34.3 vs. 34.3) remained steady, leaving the year-over-year growth rate of our payroll proxy for nominal compensation at 5.5% – roughly in line with what our forecasts had anticipated and down roughly 20bps from April. With respect to the underlying details of the establishment survey, the three sectors that have driven nearly 75% of job gains over the past 12 months once again were the drivers in May – namely, private education/ health services (+86k), leisure/hospitality (+42k) and government (+43k). In addition, we saw strong rebounds in construction (+21k), as well as professional and business services (+33k). In short, the May establishment survey showed a resumption of the hiring trends that have been in place for the past year and should alleviate fears of a more concerning slowdown in the labor market.

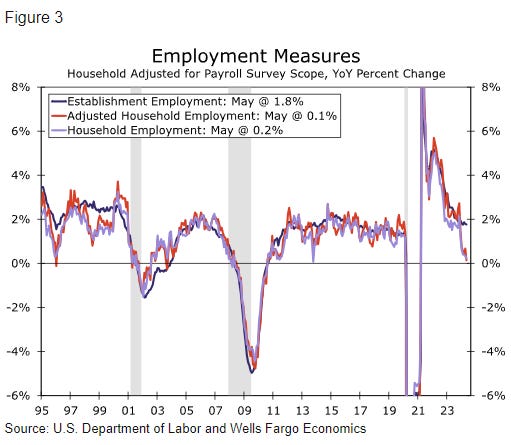

To be sure, the household survey data were less positive as a 408k decline in employment, coupled with a 157k increase in unemployment, resulted in a tenth increase in the unemployment rate to 4.0% -- the highest since November 2021 (4.1%). While the monthly changes in household employment and unemployment are historically volatile, the annual growth rate of household employment continues to notably underperform that of both the establishment survey, as well as ADP private employment. That said, the majority of the weakness in household employment over the past year has been due to the 20- to 24-year old cohort where employment is down nearly 6% over the last 12 months. Employment of those 25 and over is up a more healthy 0.7%. While this doesn’t explain all of the gap between the aforementioned growth rates, arguably, the establishment survey should better capture the labor supply contribution from immigration relative to the household survey (see “How large was the inflation mitigation from immigration?”). In addition, we would note that historically such gaps are not entirely unusual.

As we detail in our latest chartbook, the strength in payroll gains remains partly a function of the lack of layoffs as the latest JOLTS survey data showed no change in the private layoffs and discharges rate (1.1%) or the private hiring rate (3.9%) – the former being lower than any period prior to covid and the latter being the lowest since 2014. As we noted recently (see “ Let it churn (or not): Fading dynamism of the US labor market”), such a lower level of labor market churn typically would be associated with a significantly higher unemployment rate. That being said, the overall labor market picture remains broadly healthy and from the Fed’s perspective, does not warrant any urgency to ease the policy rate – particularly, given stubbornly elevated inflation. In summary, we view today’s data as consistent with our view that the Fed will remain on the sidelines ahead of the election, with an initial rate cut coming at the December meeting (see "June FOMC preview: Time is on their side, yes it is”).

The May nonfarm payroll gain of 272k was moderately above the 6-month average of 255k

…Revisions to nonfarm payrolls have been broadly negative

Payrolls gains of 272k showed continued resilient in the labor market, enable by growth in labor supply. More weakness in the household survey pushed the unemployment rate higher. Earnings were firm. The labor market is coming into better balance and we expect three cuts this year starting in Sep.

… Our forecast remains forthree 25bp cuts this year starting in September, as the return of disinflation restores confidence among the FOMC that inflation is moving sustainably back towards 2%…

MS: The Eyes of the Beholders | Global Macro Strategist

More central banks hopped on the easing train this week, but investors don't expect the Fed to join the passenger manifest for some time. US economic data continue to confuse, instead of clarify, leaving the FOMC's perspective – or Chair Powell's – most important to the direction of macro markets.

…Interest Rate Strategy United States Yield reversal amid a Rorschach test: We think the latest payrolls data justify some reversal of bearish expectations that had been priced coming in (a "whisper number" of 140k headline payrolls), but we do not see them driving continued momentum to higher yields given the mixed read of parts of the payrolls report – a Rorschach test for markets.

Markets overly focused on headline payrolls – the odd one out: The upside surprise in the latest payrolls is not the same in our view as the upside surprises in the past because other indicators are weakening alongside it. Relative to the Kansas City Fed's Labor Market Conditions Index (LMCI), which extracts the overall labor market trend, the household survey matches overall trends better than headline surveys. And the market has largely priced the headline payrolls surprise, ignoring other weaker parts of the report.

… Given our understanding that the Treasury market may be incorrectly pricing just the headline surprises, ahead of the CPI print (where our economists expect continued descent) and the FOMC meeting next week (see our preview below), we stay with our long duration bias – and maintain long 3m10y receivers…

June FOMC preview: We do not expect markets to get much excitement from the dot-plot, where our economists see two cuts for 2024, but see an asymmetric risk toward lower yields emanating from the FOMC press conference, as well as the CPI print that precedes it. We continue to suggest holding 3m10y receivers.

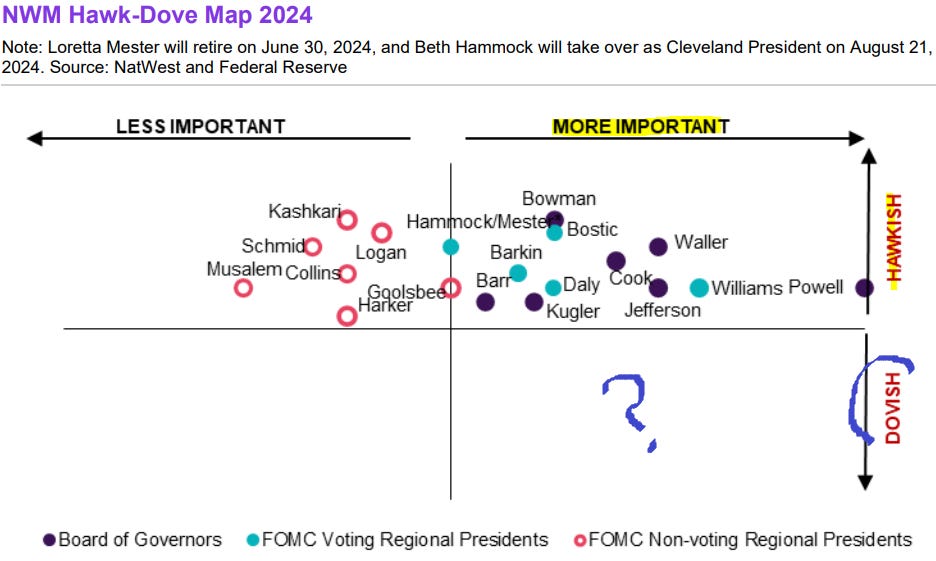

NatWest: US Weekly Economic and Strategy Brief (linking for the updated dove / HAWK CHART into the CPI, FOMC week ahead … am wondering if this chart like the boy who cried wolf…?)

Summary Nonfarm payroll growth bounced back strongly in May, rising 272K in the month relative to the 165K pace that was registered in April. Job growth over the past year has been concentrated in industries that are less cyclically sensitive, and this was once again true in May with employment growth led by health care (+84K), government (+43K) and leisure & hospitality (+42K). Average hourly earnings also topped expectations, rising 0.4% in the month and 4.1% over the past year.

However, the separate household survey was more underwhelming. A 408K decline in employment as measured by the household survey, when paired with a 250K drop in the labor force, pushed the unemployment rate up to 4.0%, its highest reading since January 2022.

On balance, we suspect the truth lies somewhere in between the robust establishment survey and the faltering household survey. We think employment growth is continuing at a solid pace, but there are ample signs that the heat in the labor market over the past few years largely has been removed. Declining job openings, a falling quit rate, narrowing employment growth and decelerating wages all point to a labor market that is coming into better balance. Policymakers will need to see a few slower inflation reports over the summer in order to start cutting rates by the fall, and all eyes now turn to next week's CPI report, to be released on the same day as the conclusion of the FOMC meeting. Our preview of next week's CPI report can be found here.

… The separate household survey was not nearly as impressive as the nonfarm payroll numbers. Household employment declined by 408K in May and continues to badly lag job growth as measured in the establishment survey, the latter being the survey from which nonfarm payrolls are derived (Figure 3). The split between full-time work (-625K) and part-time employment growth (+286K) was equally underwhelming. A 250K decline in the labor force pushed the labor force participation rate down two ticks to 62.5%.

United States: July Cut Bites the Dust; September Hanging on Edge of Its Seat

The strong job gain and rebound in average hourly earnings in May reaffirm our expectation that a rate cut remains some time away and is increasingly dependent on a few slower inflation reports. Next week's CPI report and the FOMC's Summary of Economic Projections are now in focus.

Interest Rate Watch: Dots Headed Higher

The FOMC will release an updated Summary of Economic Projections (SEP) coinciding with its policy meeting next week. Price pressures have held relatively firm in the months following the last SEP, leading us to anticipate an upshift in the median dot. We also expect longer-term interest rate expectations to edge higher, reflecting the possibility of greater underlying economic potential.

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Against All Odds Research

@JasonP138

Long bonds have not made a new 52 week high since 2020.

G7 central banks are cutting rates – first Canada and now the European Union.

Will the Federal Reserve follow suit in the coming months?

Investors seem to think so…

US 30-year T-bond futures have posted positive returns six days in a row – their longest winning streak since April last year.

T-bonds also broke above a key polarity zone, triggering our buy signals from last month:

I’ve made clear my disdain for buying treasuries, so the long bond trade will likely be a winner. After all, the best trades are often the hardest to take.

But price is sliding back below our risk level following the May nonfarm payroll data. And a yearlong downtrend line continues to act as resistance. Until T-bond futures break through resistance, the downtrend remains intact, regardless of our buy signal…

Apollo: CRE in Trouble (…Team Rate Cut leanin’ back in…)

There are a lot of commercial real estate investments that need to be refinanced in 2024, see chart below. And rates higher for longer continue to have a negative impact across CRE.

CalculatedRISK: Fed's Flow of Funds: Household Net Worth Increased $5.1 Trillion in Q1

EPB Macro: The Resilience Of The Labor Market (Chart Of The Week)

… The EPB Coincident Employment Index was updated after the May Employment Situation report and showed a slight decline month over month. However, the EPB Coincident Employment Index has increased a total of 1.1% in the 18 months since the yield curve inverted compared to an average performance of -2.0%.

Currently, this is the strongest labor market performance post yield curve inversion on record, dating back to the early 1970s.

It is important to note, however, that the current data is unrevised, while the historical bands are revised data…

Hedgopia: CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (looks like specs had INCREASED SHORTS 10s and flipped from LONG TO SHORT 30s into NFP…interesting)

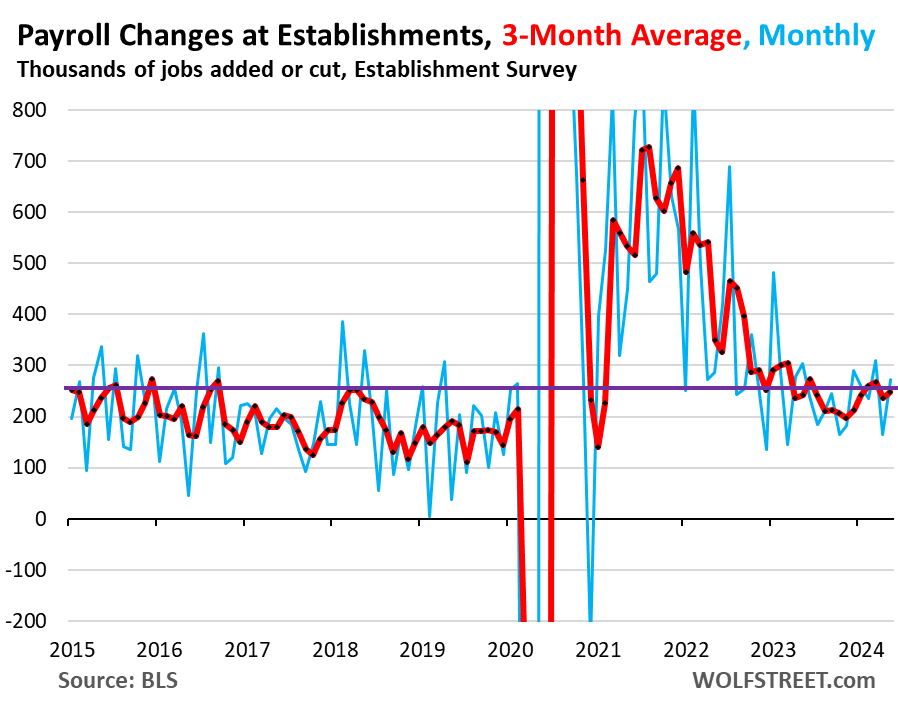

WolfST: A Jobs Report You’d Expect from an Economy Humming along in an Inflationary Environment

Three-month averages have been steadfast: higher-than-normal job creation and wage increases.

ZH: Shock Decline In Credit Card Debt Is First Since Covid Crash, As Card APRs Hit New All Time High

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Danielle DiMartino Booth

Friday's Jobs Report:

https://youtu.be/ILEfy1z99_g?si=AmdZfKbiM3I7o52z

Barchart: An All-Time High $9.3 trillion in U.S. Debt is set to mature within the next 12 months

https://t.co/O8D8SU45tG