On June 6, the GDPNow model estimate for real GDP growth in the second quarter of 2024 is 2.6 percent, up from 1.8 percent on June 3.

Ummm … wait, what?

And SO, the passing of time is nearly DONE, with NFP upon us … weekend missive to be filled with NFP recaps and victory laps, for sure … Before we get THERE and on heels of BoC launching easing cycle …

ZH: ECB Cuts Rates For The First Time Since 2019, Does Not "Pre-Commit To A Particular Rate Path"

ZH: Initial Jobless Claims Rise Near 8-Month Highs

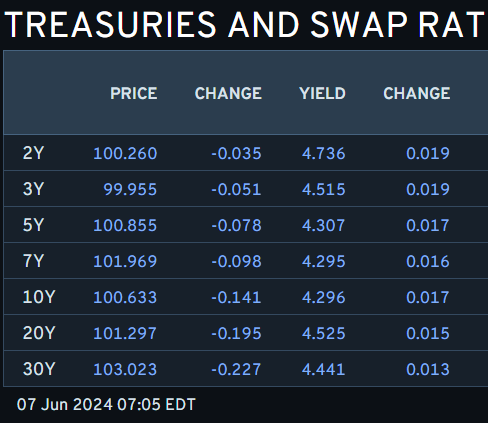

… hmm. Know what? I’m gonna quit while I’m behind as the moment I hit SEND everything set to change and so … here is a snapshot OF USTs as of 705a:

… and while these PRE MARKET prices are of importance, a weekly close will be reviewed over the weekend. For NOW, though, HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are unchanged on the session, mildly outperforming bunds ahead of the much anticipated NFP report. There was a modest drift cheaper overnight on a hit to EGBs post-ECB, which has backtracked in early-London hours. Flows saw some early front-end selling pressure which spread to the 10yr sector with real$ looking to lighten up positions after the sharp rally. Conversely, in the past few hours, our desk has reported scattered demand in the belly, some position-squaring in play. Session volumes are ~70%, with commodities mixed (CL +0.5%, HG -2%, NG +1.3%) after bifurcated risk-performance in APC (NKY -0.1%, KOSPI +1.2%, SENSEX +2.2%, SHCOMP +0.1%). S&P e-minis are showing little change here at 7am, the DAX -0.8%.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: European equities slip, Gold slips as China maintains gold reserves, USD flat ahead of US NFP … USTs trade within a contained range, Bunds are softer post-German data and unreactive to a slew of ECB speakers who mainly stuck to the data-dependent script; EGBs hit on Q1 wages … USTs are marginally in the red, with no real reaction to the morning's data points or extensive ECB speak. Focus entirely on payrolls before CPI and the FOMC next Wednesday; USTs in narrow 110-06 to 110-10 bounds which are entirely contained by Thursday's 110-03 to 110-13 parameters.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use…and I offer these as almost a kind of joke whereby the hours spent (hopefully less now thanks to AI) creating these reports BEFORE NFP boggles the mind. I say that with the latest Atlanta Fed GDPNow (back UP from other days drop … “On June 6, the GDPNow model estimate for real GDP growth in the second quarter of 2024 is 2.6 percent, up from 1.8 percent on June 3.”) in mind as an example of how swiftly things change. In any case, here’s SOME of what Global Wall St is sayin’ …

NFP preview. "We believe the goldilocks range for NFP is +125-175K ... Sub-125K gains in NFP could increase the risk of triggering the Sahm Rule*, reviving recession fears in the market."

The ECB delivered on its soft, well-telegraphed easing of policy in June, cutting all policy rates by 25bp. Communication on the future rate path was non-committal, with little signal on the timing of the next move. The forecasts saw upward revisions to growth and inflation, the latter driven by higher unit labour costs.

BARCAP: US CPI Inflation Preview (May 2024 CPI): Moving sideways (hmm, sideways is NOT, IMO, time to CUT but what the heck, who cares, cuz, you know, BoC and ECB…)

We forecast a 0.12% m/m SA rise in headline CPI, keeping the annual rate at 3.4% y/y. We estimate that core CPI remained broadly unchanged at 0.29% m/m, as some easing in core services prices was offset by less deflation in core goods. We forecast the NSA index to print 314.418.

The ECB’s well-telegraphed 25bp rate cut at its June meeting was accompanied by a distinct lack of guidance on the future path of rates, suggesting a return to more genuine ‘data dependence’.

The emphasis on accumulating data and the ECB’s updated forecasts support our expectation of a quarterly pace of rate cuts. That said, comments suggested a lack of conviction which, coupled with higher inflation forecasts, was marginally hawkish.

We continue to see the next rate cut coming in September and expect three (including today’s) rate cuts in total this year. However, we were left with the impression that risks are skewed towards fewer, not more, cuts than is our central case.

Rates: Following the ECB meeting, we see US data ‒ particularly the NFP data on Friday ‒ as the main driver of EGB yields near term.

FX: Despite today’s marginally more hawkish ECB meeting, we continue to view risks to EURUSD as skewed to the downside given other factors that could weigh on the EUR. We remain short the EUR versus the CHF, GBP, MYR and PLN.

The FOMC will keep rates unchanged at the June policy meeting and signal no rush to engage in a first cut, we think.

We expect a median of two cuts in the updated 2024 dot plot (from three currently), with the risk in the direction of just one. While a close call, two cuts maintains optionality if labor data weakens more than expected.

We continue to see the first cut in December, with resilient inflation and election uncertainty forestalling an earlier move.

We entered into a long 10y US versus short EUR rate trade on 15 May. We argued at the time that eurozone data had reinforced our non-consensus bullish view on the European economy, while at the same time the bar for further upside surprises in the US had reset higher after a series of strong reports in Q1 2024.

We entered the trade ahead of the April US CPI report, arguing that even an in-line print would nourish the perception US data were softening, thereby giving the nod to investors to increase duration. We noted that given the directionality of the spread to US rates, a US rates rally would likely be met with an outperformance of US rates versus Europe…

… Trade: Keep long 10y US SOFR versus short EUR 10y ESTR. Move stop to 135.2bp. Keep target at 100bp.

CitiFX Techs: USD & US rates: Levels into NFP (entire note worth a click I’ll offer some of their most excellent WEEKLY charts to watch ahead of NFP, as these are most likely best to watch ahead of weeks close…)

We highlight some levels to watch into NFP for the Dollar and US rates:

2y yields: Testing support at 4.70-4.76%. Subsequent support at 4.40%. Resistance at 4.98-5.04%

5y yields: Near support at 4.29%. Subsequent support at 4.0%. Resistance at 4.65%

10y yields: Near support at 4.23%. Resistance at 4.64%.

30y yields: Watch if we sustain a weekly close below ~4.50%. Subsequent support at 4.33-4.37%.

DB: Trading the US Employment report (Ruskin writes, we lean in and listen)

The market has been 'leaning into' thoughts of a softening US economy. Weakerthan-expected labor market data would reinforce the recent softening in bond market yields, and solidify the 10y yields levels below the 4.3 - 4.34% pivot area. Stronger-than-expected data, would, however, fly in the face of recent negative data surprises, and not for the first time confound thoughts of a material slowing in the US economy. After all, NFP has exceeded expectations in 9 of the last 12 monthly releases and was above expectations in 11 of 12 releases in the 12 months before this (see Figure 4). In short, the market will embrace softer data as providing an accurate rendition of economic deceleration, but it will have even more shock value if the data is strong. With this in mind, there could be a sharp-ish response to either an upside or downside surprise, and the impact could be quite symmetrical and sizable, albeit for very different reasons.

As we have noted in the past, strong labor market data gives the Fed 'optionality' to wait out the slowing in inflation, when there is limited immediate social cost to maintaining a tight interest rate stance. If, however, the data is softer, it will start to create a more active debate about how patient the Fed can be, although even here, we will need more than one soft employment data point to put the Fed on notice.That the market already has over an 80% probability that the Fed will cut by 25bp through September, on balance, tilts the risk-reward to playing against a preelection cut, not least because a soft payroll number is not a sufficient condition for an easing, given the other side of the dual mandate is 'non-compliant' and inflation needs to soften, too. At the front-end (Sept fed funds futures), there is, if anything, some asymmetry favoring paying rates, if only to trim pre-election easing expectations…

The ECB had prepared the ground for a rate cut today and it delivered against those expectations, cutting the deposit rate 25bp to 3.75%. The cut was supported by all but one of the Governing Council. However, garnering the support of most hawks came at the cost of a clear signal that this is the start of an easing cycle and made today’s policy move feel like a “hawkish cut”.

The ECB offered no guidance on the next steps in the monetary policy cycle. Maximum policy optionality is being retained. The ECB is purposefully not presenting today as the first cut in a series. The data do not give the ECB the collective confidence to present it as such.

Nevertheless, with policy rates still restrictive and underlying confidence in the wages and general disinflation narrative growing, President Lagarde was at least implicitly confirming the direction of travel is further rate cuts. When exactly they happen will be determined by the data.

Our baseline is three cuts in total in 2024: June, September and December. We recently changed the balance of risks around this baseline from 4 cuts to 2 cuts. That change feels even more appropriate after today’s meeting. A September cut is not a done deal.

We see a terminal rate of 2.00-2.50% at end-2025/early-2026. Neutral is somewhere in this range. We expect wage growth to slow and core inflation to be back to target by end-2025. We expect a net tightening of the fiscal stance. We also expect higher uncertainty (global trade, geopolitics, etc) to be a growth headwind. We expect further cuts in 2025 and continue to think market pricing is too hawkish.

UBS: The ECB creaks toward a cutting cycle (NFP > ECB IMO and so, some thoughts on topic…)

… It is US employment report Friday. There are quite serious questions about the quality of this data—poor survey responses, poor assumptions about business creation, and a meaningful difference between the establishment and household surveys. Markets will react because that is the tradition.

The expectation is for a boring report, with the key numbers essentially the same as last month. The range of forecasts is unusually tightly clustered, with only a couple of economists breaking away from the pack. Revisions are important, given the data quality problems.

… And from Global Wall Street inbox TO the WWW,

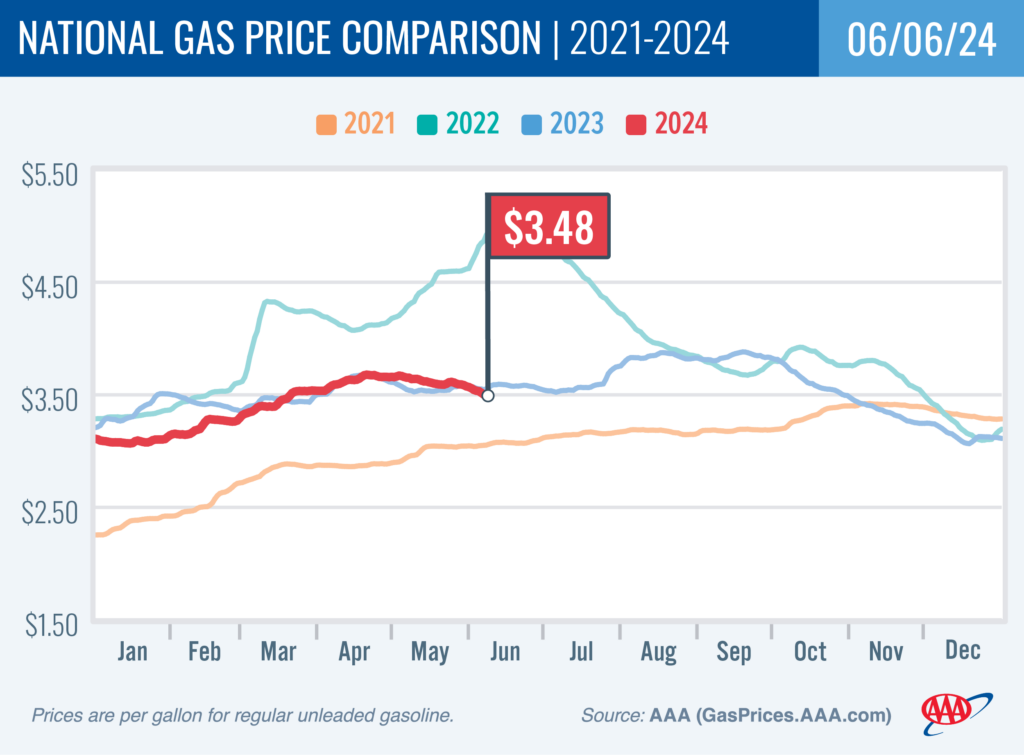

AAA: Drop in Pump Prices Accelerates as Summer Approaches (hey now, good news and esp for those who are ‘energy traders’ — ie all bond jockeys — Team Rate CUT certainly taking note here!!)

WASHINGTON, D.C. (June 6, 2024)—Gasoline prices took another trip south this week, falling eight cents since last Thursday to $3.48. It marks the largest weekly drop of the year. “This drop in pump prices appears to have some sticking power for now,” said Andrew Gross, AAA spokesperson. “More states should see their averages dip below $3 a gallon in the …

Apollo: Global Economic Outlook Improving (time for cuts and a launching of a cycle?)

The consensus probability of a recession has declined significantly in recent months and now stands at 30% for the US, Europe, and UK, see chart below.

ING Rates Spark: US payrolls more exciting than first ECB cut

The ECB announced the first rate cut, with euro rates only up a few basis points. With little concrete forward guidance from the press conference, euro rates will also be watching US data for signals justifying one or two more cuts this year. US payrolls today will grab the spotlight and in our view a consensus reading could bring UST yields higher

… Rate markets set for US payrolls disappointment US payroll figures will likely cause more excitement than the ECB cut. With US rates down significantly since last week, markets seem to be prepositioned for an economic disappointment. Consensus sees numbers coming in at 185k for the nonfarm payrolls for May, a touch above the 175k last month.

Any reading close to consensus, however, would in our view actually be a catalyst for higher yields. The number would be well below this year’s average, but it would not reflect worrisome economic weakness. And with inflation still not where the Fed needs it to be, we think the 10y UST should see higher yields in that case.

As expect yesterday's ECB rate cut to have little impact when the FOMC meets next week where we see fewer rate cuts in their forecast.

… With a multitude of economic data being published every month, there is always room to cherry-pick and find a weak print among the overwhelming mass of strong data. Looking at the more broad data series from various sectors we observe that

Job openings are moderating, but is still higher that at any time before the pandemic. This suggest that companies are very keen on hiring new workers.

Jobless claims are still near historical lows, which would be odd if we were heading into a recession.

Company earnings are at very high levels and have been rising over the last year leaving little incentive to cut back on investments or hiring.

Corporate bankruptcies are low and falling, further showing good overall health among businesses.

Household wealth is still increasing at a break-neck pace. This clearly supports consumption.

Real personal consumption has been growing faster since inflation peaked in 2022, and is currently rising at more 2% yoy. So consumers are spending the increase in real wages rather than save more.

Summing it up, we see the risks of a sharp slowdown in the labour market as very small. We thus believe the Fed will lean on the inflation side of the reaction function when they eventually decide to lower rates. Most likely this will not happen before December and possibly not before 2025. Read more here: https://corporate.nordea.com/article/93011/major-forecasts-divergence

Jobless claims usually rise well before the recession starts, unless it starts with a black swan

US Corporate bankrupcies have been falling over the last year, implying solid economics in the business sector

ZH: Why The Fed Will Pull The First Cut To July From September (Tchir of Academy … an interesting take)

Revisiting Our Rate Outlook As the 10-year Treasury trades near the low end of our current range of 4.3% to 4.5% and we digest jobs data and prepare for the Fed, it seems like a good time to revisit and restate our outlook for rates.

Political Reaction to First Fed Cut

Before going further, it makes sense to take a look at the likely political reaction to the first Fed cut. Why? Because, I for one, believe that it will influence the timing of their cuts this year.

Former President, and presumptive Republican nominee, Donald Trump, is likely to use social media and the campaign trail to claim that the Fed is handing the election to the Democrats. In addition, the cut is politically motivated to help the current president, despite a failure to get inflation under control.

Current President, and presumptive Democratic nominee, Joe Biden, is likely to claim that Bidenomics is working, the country is in great shape, and the Fed cut is confirmation (if not affirmation) that his policies are working.

Some percentage of the population will believe each narrative, and that is important.

Maybe the Fed won’t take this into account, but for me, I would not make the first cut in September.

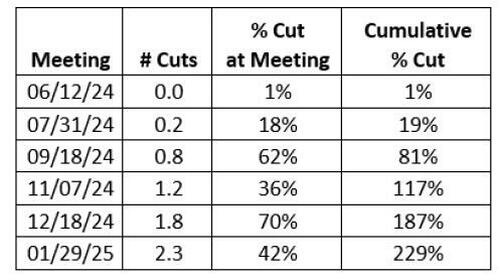

Fed Probabilities

Using the WIRP function in Bloomberg, we can examine what the market is pricing in, as of Tuesday June 2nd.

The market clearly disagrees with me, as the market has September as the largest probability of a cut before December. Cumulatively the market is pricing in an 80% chance of a cut before the election.

I believe the Fed wants to cut once, as it would be a confirmation that their policies have worked. That they tightened appropriately, and slowed inflation down to the point that they can start going the other direction. They did all of that without tipping the economy into recession.

Given the long lag effects and the desire to demonstrate their successful policies, the Fed will give us a cut this year, almost regardless of what the data signals. If the data is too strong, they might not cut, but it has been equivocal at best.

So, I like a cut at the July meeting. 25 bps is my base case, with a possibility of 50 bps if the data is weak enough (which I suspect it will be on the jobs front).

I lean towards July rather than September because, while the Fed will see the same political discourse about their cut, it will be far enough away from the election to mitigate the political noise, and it is peak holiday season, making it less likely that the noise will be heard.

From there I expect another 1 to 2 cuts this year, presumably November and December.

I am basically in the 75 bps camp for this year (with either 2 or 3 cuts), starting sooner than is currently priced in.

We will get an updated Summary of Economic Projections at the June meeting.

On the dot plot front, I am looking for the median to move to 2 cuts, and to be in line with the mean that dropped in the prior release. So, I’m likely going to be fighting the dots.

Look for Powell to put July firmly on the table, which would also be fighting the dots (but he often does that).

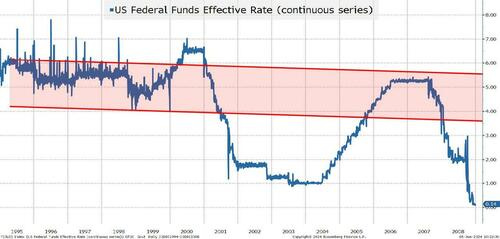

Look for 2026 and the “longer run” (presumably the terminal rate) to inch higher. There has been enough discussion about R* in recent weeks for the Fed not to question what the appropriate level of longer-term yields should be. Similarly, there is enough debate about whether current yields are restrictive at all (not just restrictive enough) that there is likely to be an incremental move to Normal for Longer.

While we have lurched from financial crisis to financial crisis in the past 15 years, maybe we have lost sight of what used to be “normal”? Maybe something well above 3% is “normal”? Will the AI productivity boom not allow for growth with higher rates?

It is probably a touch early to be fixated on the terminal rate, but I think that will become a more captivating topic once the Fed makes the first cut.

I suspect as that happens, that terminal rate projections will increase AND we may finally see some “normalization” of the yield curve…

Seems the Fed wants to mold Reality vs responding to Reality. So very central planner like! I find this concerning. So very often reality BITES! And BTW that was Oodles of fun!

Seems the Fed wants to mold Reality vs responding to Reality. So very central planner like! I find this concerning. So very often reality BITES! And BTW that was Oodles of fun!