while WE slept: USTs 'marginally' weaker on light volumes; "10-Year Treasury Yield is Too High" (Paulsen); 'Long-Term Yields Are About To Spike Again' (Goldilocks)

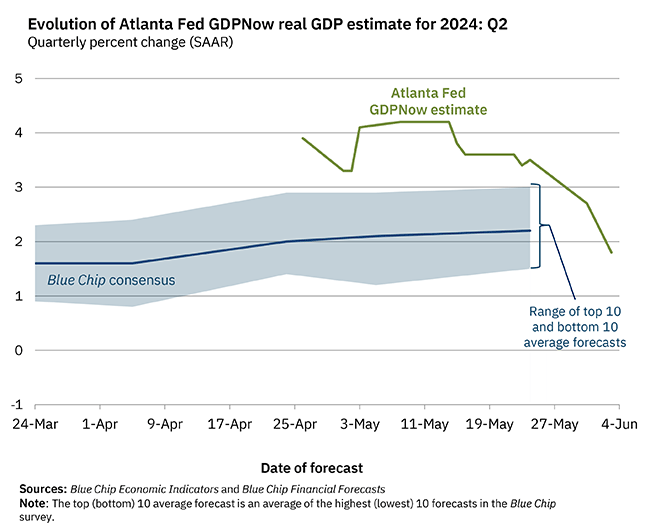

Charts schmarts … trend is yer friend ‘til it bends and the 2024 UPTREND certainly breaking down and why not when just couple weeks ago GDP said to be 4% and recent updates showing that now closer to 1.8% …

… The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2024 is 1.8 percent on June 3, down from 2.7 percent on May 31. After recent releases from the US Census Bureau and the Institute for Supply Management, the nowcasts for annualized second-quarter real personal consumption expenditures growth and real private fixed investment growth declined from 2.6 percent and 3.1 percent, respectively, to 1.8 percent and 1.5 percent.

… meanwhile, back at the ranch, a couple NFP pregame recaps of ADP …

CalculatedRISK: ADP: Private Employment Increased 152,000 in May

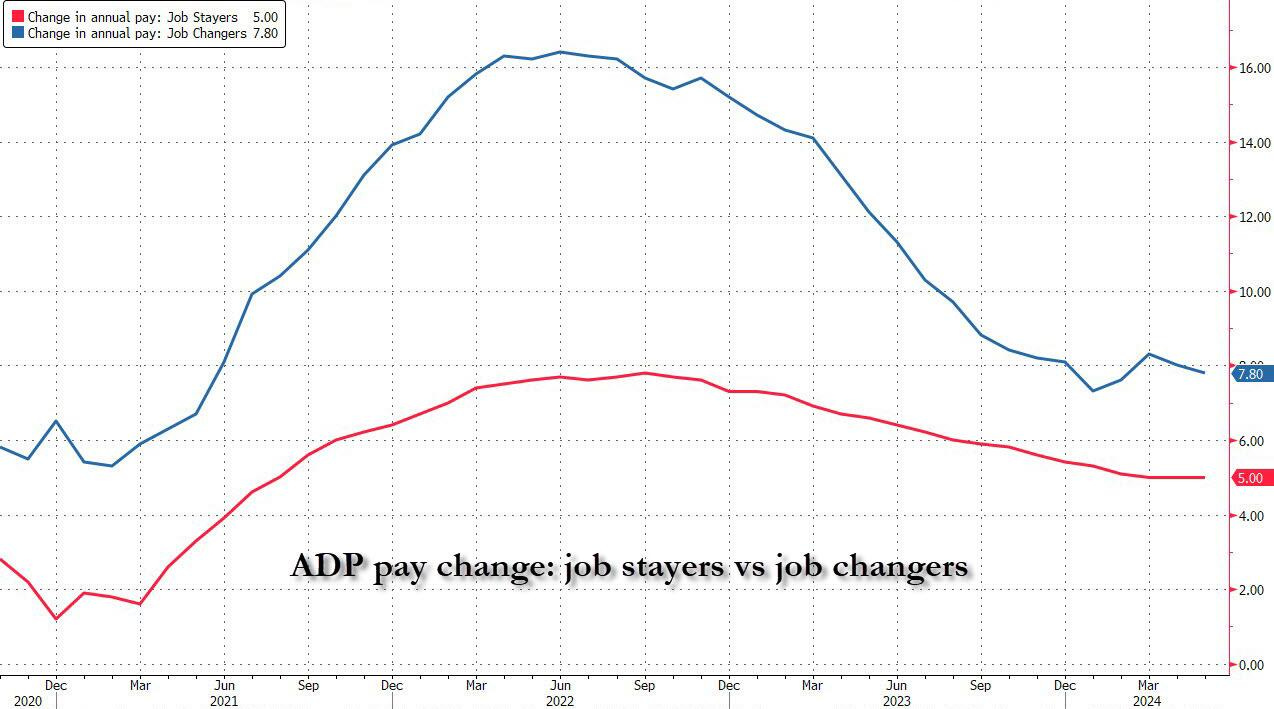

ZH: ADP Payrolls Unexpectedly Tumble To Lowest Since January As Wage Growth Continues Slowing

… Confirming the slowdown, ADP's chief economist Nela Richardson, said that “Job gains and pay growth are slowing going into the second half of the year,” adding that "the labor market is solid, but we're monitoring notable pockets of weakness tied to both producers and consumers.”

Wage growth continue to slow for Job-Changers, who saw a 7.8% increase in pay in May, down from 8.0% in April, while Job-Stayers' wage growth remained unchanged at 5.00% for the 3rd month.

… and as funTERtaining as the ADP really is, can I get an AMEN from Team Rate CUT on this one from the great north…

ZH: Bank of Canada Cuts Rates By 25bps As Expected, First G7 Central Bank To Launch Easing Cycle

… shortly AFTER this launching of a rate CUTTING cycle …

CalculatedRISK: ISM® Services Index Increases to 53.8% in May

ZH: Services ISM Unexpectedly Surges Out Of Contraction, Prints At 53.8, Above All Estimates

… AND surging outta contraction here as Canadians launching rate cutting cycle ‘up there’ … markets and global macro is ripe with all sorts of narratives readily avail to support whatever your P&L says you should support.

Choose your own ending, if you will … growth slowing, inflation hopefully to follow and rates coming down BUT ‘flation sticky and cutting rates will certainly bolster inflation expectations (?) and so, maybe just maybe it will be the year of the … steepening?

Whatever … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are marginally weaker, led by the belly, with bunds ever-so-slightly outperforming as we await the ECB decision (25bp cut assured). Flows in early-London have been 2-way, but major conviction still lacking, according to the desk. Some interest in initiating steepeners has been seen as well as x-market selling out the curve from real$. Short-covering concerns on the part of fast$ and CTAs remain thematic, as evidenced by performance across the futures complex. Volumes are running below recent averages at ~70%. Crude Oil (+0.5%) and Copper (+0.7%) rebounded overnight, with stocks in Japan (NKY +0.6%) and India (+0.9%) higher as well. The DAX is outperforming pre-ECB (+0.7%), while S&P futures are showing +0.75pts here at 7:15am.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures are mixed & EUR slightly higher ahead of the ECB policy announcement … Bonds are slightly softer, giving back some of this week’s advances … USTs are consolidating between five and ten ticks from Wednesday's 110-12+ WTD peak. Specifics light thus far with the macro focus firmly on the ECB, with US Challenger Layoffs and Initial Jobless Claims also on the docket.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

ABNAmro: Global industry shaking off disturbances | Insights newsletter

Global manufacturing PMI rises to highest level in almost two years. EM outperformance continues, but picture improves for DMs as well. Our global supply bottlenecks index still in excess supply territory.

Asset Allocation Model Slightly Favors Bonds Our stock/bond asset-allocation model, which we call the Stock Bond Barometer, is indicating that bonds are the asset class offering the most value at the current market juncture. But not by much. Our model takes into account levels and forecasts of short-term and long-term government and corporate fixed-income yields, inflation, stock prices, GDP, and corporate earnings, among other factors. The output is expressed in terms of standard deviations to the mean, or sigma. The mean reading from the model, going back to 1960, is a modest premium for stocks of 0.16 sigma, with a standard deviation of 0.97. In other words, stocks normally sell for a premium valuation. The current valuation level is a 0.34 sigma premium for stocks, just above the historical average but within the normal range. Other measures also show reasonable multiples for stocks. The forward P/E ratio for the S&P 500 is 19, within the normal range of 13-24. The current S&P 500 dividend yield of 1.3% is below the historical average of 2.9%, but also 29% of the 10-year Treasury bond yield, compared to the long-run average of 39% and the all-time low of 18%. Further, the gap between the S&P 500 earnings yield and the benchmark 10-year government bond yield is about 340 basis points, compared to the historical average of 400 and nosebleed valuation levels of 200 basis points. We expect results from our stock-bond valuation model to favor stocks, as interest rates head lower and EPS growth picks up. Based in part on the output from our Stock Bond Barometer, our recommended asset-allocation for moderate accounts is 70% growth assets and 30% fixed income.

The ISM services composite jumped back into solid expansionary territory in May following April's dip, led by upswings in business activity and new orders. Although this likely exaggerates underlying growth, the resilience theme is alive and well. With pipeline pressures persisting, this may not bode well for the supercore.

DB: Early Morning Reid (good news is bad but bad news within the good was great or terrible but awesome … depending on your P&L and views … happy ECB cut day?)

… The ribbon was also cut for a brand new all time high in the S&P 500 (+1.18%) last night, the 25th so far this year. The last week has seen the index at the bottom and now the top of the (relatively narrow) one-month range. The advance yesterday came as good economic news was seen as good news for markets again, while renewed tech optimism saw Nvidia (+5.16%) become the third company to reach a $3trn market cap. So normal service for 2024 has returned.

Yesterday’s advance was initially supported by the US ISM services for May, which surprised on the upside at 53.8 (vs 51.0 expected). That was significant as the previous month had seen the index fall to a contractionary 49.4, so the bounceback suggests that was just a blip rather than the start of a more concerning trend. This reading was also the index’s highest level since last August, and the largest monthly increase since January 2023. That said, a few of the details weren’t quite as strong. For example, the employment component was still in contractionary territory at 47.1 in May (vs 47.2 expected), and therefore in line with the wider narrative of a slackening labour market. The prices paid index fell back from 59.2 to 58.1 (vs 59.0 expected), as inflationary pressures came off a tad. Supporting the employment story, the ADP payroll numbers for May also undershot expectations, rising +152k (vs +175k expected), which is its slowest pace since the start of the year.

These softer elements meant investors priced in more rate cuts for a sixth day in a row. For instance, the amount priced in by the Fed’s December meeting was up +4.7bps to 50bps. In turn, 2yr yields ended the day down -4.8bps to 4.72%, whilst 10yr Treasury yields saw their fifth decline in a row, down -5.1bps to 4.28%, their lowest since March. That move has stabilized overnight however, with 10yr yields (+1.9bps) back up to 4.29% as we go to print…

Slow inflation progress this year keeps the Fed on hold for longer. Chair Powell should emphasize patience. We still see a first cut in September. Our strategists maintain long 3m10y receivers.

Key expectations

The FOMC remains on hold at 5.375%. The FOMC statement describes progress on inflation as slowed rather than stalled. The Summary of Economic Projections will likely show a shift to two cuts this year instead of three, marking to market for stronger inflation data in 1Q.

In the press conference, we expect Chair Powell to emphasize patience as the Fed awaits more convincing data and to maintain a cutting bias. We continue to look for three cuts this year starting in September.

Our rates strategists do not expect markets to get much excitement from the dot-plot, but see an asymmetric risk toward lower yields emanating from the FOMC press conference, as well as the CPI print that precedes it. They continue to suggest holding 3m10y receivers.

Given recent shifts in market pricing, our economists’ expectation that the FOMC would only change its forecasts slightly would probably not surprise investors and would drive little USD reaction.

On the agency MBS side, our strategists remain long mortgage basis.

There is a strong consensus about today’s ECB policy rate decision. A total of 53 out of 55 surveyed economists expect a 0.25% rate cut, and ECB Chief Economist Lane has practically promised an easing (chief economists are, of course, never wrong). The idea this year has been that most major central banks would follow inflation lower. Eurozone inflation is lower. Rate cuts are not stimulatory, but stabilizing (keeping the real interest rate steady).

The uncertainty is not today’s move, but what happens next. Ideally the signal would be a steady rhythm of rate reductions—a quarter point a quarter, reflecting ongoing disinflation (as evidenced in yesterday’s producer price data). The risk is that ECB President Lagarde introduces deliberate uncertainty. Investors will focus on the press conference, and the subsequent “clarifying” statements from other ECB members.

US April trade data is not normally a market moving number, but it has some relevance. For one thing, trade has become a political football, with US companies and consumers being taxed for daring to buy things made overseas. It also hints at domestic demand patterns…

Summary The ISM services index leaped by the most in 16 months, revealing the April contraction was a blip and activity remains steady. While new orders suggest continued demand, the selected industry comments and continued employment contraction reveal a touch of caution among service-providers.

The S&P 500 rose to yet another record high today, once again led by semiconductor stocks, in particular, by Nvidia (chart). The chipmaker just joined the $3 trillion dollar market-cap club along with Microsoft and Apple. The long line to buy the company's GPU chips keeps getting longer. It will have a 10-for-1 stock split on Friday.

Perversely, the bulls are also charged up by the latest batch of relatively weak economic indicators, including May’s M-PMI and ADP payrolls reports. They figure this increases the odds of the Fed cutting the federal funds rate (FFR) this year.

In our opinion, the latest data suggest that the economy is slowing rather than heading for a hard landing that would force Fed officials to cut the FFR in the coming months. If they do act prematurely--before inflation is convincingly back down to their 2.0% target--they risk fueling a meltup in the stock market, one that may already be underway.

Consider the following:

(1) NM-PMI vs M-PMI. The ISM nonmanufacturing purchasing managers index jumped in May to 53.8, retracing a brief dip below 50.0 (chart). The production component soared to 61.2 from 50.9 and the prices-paid index declined to 58.1 (from 59.2). May's data reversed the stagflationary blip in April.

The M-PMI was less hot, as the goods sector remains in a growth recession. This confirms our view that the US economy is transitioning from an industrial one to a digital one, dominated by services and technology providers. Fewer US companies produce goods and fewer workers are employed by them. This helps to explain why manufacturing-related indicators (such as the M-PMI and LEI) erroneously signaled a recession over the past couple of years.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: The Goldilocks Market Is Ignoring Slowdown Signs

… The reality is that there are significant weaknesses in how far and wide prosperity has been delivered, a fact which macro data masked for a long time. Significant swathes of the US economy, especially smaller businesses and lower-income households, have been struggling. And the weakness at the macro level now reveals that the pain has started to grow. A booming stock market and greater interest income can only goose the economy so far. Eventually the anti-stimulative effects of the Fed’s rate hikes had to take over. And they have.

I think that means rate cuts are on the cards for the end of the year. But unless the weaknesses grow from here, you’ll still probably want to avoid getting too exposed to long-term bonds, which have been pricing in slowdown risk for a while, holding their yields sharply below short-term ones. Even so, bonds do offer a compelling value overall given how the yield curve sits. On the other hand equities, which are also richly priced, need a Goldilocks scenario to eke out more gains.

Where we are now on equity market pricing

Before we get into the data and what it means for the market, let’s look at where we are in terms of the two big yardsticks — the S&P 500 price/earnings ratio and the Treasury curve’s inversion.

When you look at how much we pay for each individual dollar of earnings in the S&P 500 over time, two things become clear. One is that interest rates matter a lot. You can see that due to the secular rise in price to earnings from 1982 to 2000 as interest rates dropped. There were peaks and valleys during that 18 year period, but the clear trend is up due to the much greater value of future earnings due to the lower opportunity cost from lower interest rates. That interest rate factor dominates all others.

Yet you can also discern a cyclicality to P/E ratios, with the ratio peaking with Fed rate-hiking cycles in 1989, 1994 and 2000. Some of the subsequent peaks are more about the low earnings due to recession than price. But even after the 2000 Internet bubble was popped, you can see a clear secular trend that began after the financial crisis through today, where the price of the S&P 500 is far richer today than it was 15 or 16 years ago.

The upshot: Right now, we’re at P/E levels near the top of the range except for by the Internet Boom’s glory days and the recent 2021 lockdown trading bonanza. We passed the dampening phase of Fed rate hikes in 2022 and are still in the up-cycle of P/Es due to the current expansion. That makes share prices vulnerable to a recession, even if it is accompanied by interest rate declines.

The yield curve is still predicting recession

On the interest rate side, you’d have to go back to Volcker’s economy-crushing rate hikes to see the curve this inverted. Looking just at the difference between 3-month and 10-year Treasuries over the last three decades, we haven’t seen the curve this inverted.

The yield curve being inverted tells you that people are willing to buy long-term bonds and receive less compensation than short-term paper because they believe yields are going to decline over time. Historically, because the Fed hasn’t been able to stick a soft landing that often, that ‘predicts’ a recession. So given we have the most inverted yield curve in ages, either the belief in the Fed’s abilities to manage the business cycle have increased or recession will eventually come.

The upshot: bonds may actually be well-positioned for gains. In the early 1990s, and after the Internet Bubble and the Great Financial Crisis, the yield curve eventually ‘uninverted’ to the tune of 400 basis points. If something similar happened today, gains in (treasury and non-defaulting corporate) bonds would be astronomical…

FRBNY: A Season of Change for the U.S. Treasury Market

Thank you all for having me.1 I want to especially thank Scott O’Malia and the ISDA team for the invitation to speak here at such an important time in the U.S. Treasury market. As already introduced by Scott and Gary and subject to much further discussion at today’s forum, the Treasury market is undergoing significant and transformative structural changes. The expansion of central clearing in the Treasury market that will occur as a result of the SEC’s central clearing rule is probably the single greatest change to Treasury market structure since the advent of electronic trading of Treasuries over central limit order books in the early 2000s, which paved the way for the high-frequency trading of Treasuries that is prevalent today. This change is occurring during a critical period of growth for the Treasury market—the Congressional Budget Office forecasts Treasury supply to increase by more than $20 trillion over the next 10 years.2

As the market navigates the legal and operational work related to the expansion of central clearing, many questions will need to be answered with regard to how clearing will evolve and what effects it will have on the Treasury market more broadly. As the SEC’s central clearing rule is implemented, it will be crucial to carefully monitor market dynamics and track Treasury market liquidity and functioning. Recent progress on the data and transparency front will help in this regard. Additionally, as Treasury market structure undergoes this transition, market participants should remain cognizant of, and follow, best practice recommendations, which support the integrity and efficiency of this critical market. Today’s forum will cover many of these issues in detail, and I am excited to hear views about progress on these topics.

Before I go any further, let me share the standard Fed disclaimer: the views I express today are my own and do not necessarily represent the views of the Federal Reserve Bank of New York or the Federal Reserve System…

… Best Practices: Important Touchstones during Transitional Times Finally, I will turn to the importance of market best practices during times of change like today. The TMPG best practice recommendations provide an important reference for market participants to support the integrity and efficiency of the U.S. Treasury market, along with markets for agency debt and agency MBS.16 The sound functioning of the U.S. Treasury market is critical given the key roles Treasury securities play in the financial system—as global risk-free benchmarks for other financial instruments, as the primary means of financing the U.S. government, and as the instruments used to implement Federal Reserve monetary policy.

Especially during this time of significant market structure change, it is important to continuously engage with the TMPG best practices to ensure these changes are implemented in a way that promotes market integrity and efficiency. TMPG best practices evolve over time and are updated and amended as needed to support the resiliency of the covered markets. In fact, this February, the TMPG updated its best practice recommendations to promote greater repo market price transparency around early morning transactions over interdealer voice brokers, encouraging publication of all voice trades to electronic trading screens when the trades are agreed to.17 I urge you all to review the updated best practices and familiarize yourselves and your firms with the recommendations.

Thinking about this time of change in the Treasury market reminds me of the song “Turn! Turn! Turn!”—written by Pete Seeger and popularized by The Byrds—which chronicles the seasons of life. In particular, the lyrics “a time to plant, a time to reap” are relevant to where we find the Treasury market today. As we enter upon this season of change for the Treasury market, now is the time to plant the seeds of sound market structure so we can reap the benefits of a more robust and more resilient Treasury market in the future. The work of promoting U.S. Treasury market resilience is ongoing and requires all hands on deck. The official sector, private sector, and academia all need to work together to preserve the continued smooth functioning and safety of this most important market.

FirstTRUST: The ISM Non-Manufacturing Index Rose to 53.8 in May

The ISM Non-Manufacturing index rose to 53.8 in May, well above the consensus expected 51.0. (Levels above 50 signal expansion; levels below signal contraction.)

The major measures of activity were all higher in May. The business activity index rose to 61.2 from 50.9, while the new orders index increased to 54.1 from 52.2. The employment index rose to 47.1 from 45.9, while the supplier deliveries index increased to 52.7 from 48.5.

The prices paid index declined to 58.1 in May from 59.2 in April.

… In other news this morning, ADP’s measure of private payrolls increased 152,000 in May versus a consensus expected 175,000. We expect Friday’s payroll report to show a nonfarm payroll gain of 196,000. In other recent news, cars and light trucks were sold at a 15.9 million annual rate in May, up 0.8% from April and up 2.5% from a year ago.

ING: Rebound in US service sector may overstate the story

The jump in May services activity follows a steep plunge into contraction territory in April. So, we prefer to look at a two-month average and that paints a pictore of solid, but slowing service sector growth. With employment in contraction territory for a fourth consecutive month, businesses appear wary about the future …

… What follows is a pictorial of various metrics which have been closely aligned with the 10-year yield for the last 15 years, but which are currently disjoined suggesting bond yields should be lower.

1. Commodity Prices

2. High Yield Equity Alternatives

3. Nominal GDP Growth

4. CPI Inflation

5. Interest Rate Expectations

6. Bond Market Volatility

7. Leading Economic Index

8. Copper/Gold Ratio

9. Inflation Expectations

… Final Comments

Bond yields seem to be defying gravity. I do not understand why? Many voices including commodity prices, high yield equity alternatives, nominal GDP growth, the CPI inflation rate, interest rate expectations, bond market volatility, the leading economic index, Dr. Copper, and inflation expectations all argue bond yield levitation should soon come to an end. Sometimes when the weight of the evidence seems pretty one-sided, its best to go with the evidence. After all, gravity has a pretty good track record!

ZH: Goldman On Why Long-Term Yields Are About To Spike Again

… However, as Goldman Sachs Rikin Shah suggested in a note to clients this weekend, the supply-demand imbalance keeps pressure (to the upside) on long-end rates.

DISSECTING THE USD CURVE... LONG END CORRECTION...

We continue to like a short bias in long end US rates for a multitude of reasons – we attribute a few reasons for this.

Buying US duration is a negative carry trade... absent any clarity of an imminent Fed cut, incremental dovish news is needed to justify holding a long position.

Any mention from the Fed (or any CB for that matter) to be in a “wait and see” and “patient” mode is not good for fixed income.

The YoY core PCE path is tricky in H2 this year due to base effects as we have mentioned in the past, and so the path to a near-term Fed cut is more likely to come via a deterioration of the US labour market rather than from the inflation side of the mandate.

Whilst there has been focus around the drop in hiring rates, this largely reflects a decline in quit rates rather than weakness in net labour demand. A situation where turnover is low because workers are content with their jobs and employers content with their employees is not necessarily a major problem.

Unless the labour market picture deteriorates more broadly, we are not overly worried.

Additionally, US fiscal deficit risks are largely skewed one way and will only gain more focus as we approach the elections.

With this context, we would not be surprised to see further UST supply concessions and indigestion..

net US Dv01 supply for 2024 we expect to realise at $1034mm/bp, compared to $701mm/bp in 2023, which is the highest annual net duration supply on record.

June in particular is expected to see $115m/bp of net supply, much higher than May mainly because of lower reinvestment demand coming from index trackers and coupon reinvestments.

The risk/reward is for higher long end US rates from a monetary policy, fiscal policy, supply/demand and term premium perspective.

The market is slow at adjusting long term R* expectations, but the resilience of the US economy at higher rate levels continues to tell us that R* is on the rise.

2 other points to highlight on this front:

1/ The second half of May has seen a 20bp tightening in FCI (largely from rates and equities).. is more tightening likely needed? &

2/ USDJPY FX continues to grind higher.. should this encourage repatriation flows back into Japan (and further selling/unwinds in UST?).

This only changes if we get a sudden weakening in the US labour market (or disinflation impulse) – neither of which we expect for now (even though JOLTS just tumbled, but leaves all eyes on Friday's payrolls).

ZH: Wall Street Admits The Biggest Economic Shocker: All Jobs In The Past Year Have Gone To Illegal Aliens (I suppose this might be somewhat of an offset to the above foreshadowing of spike in yields … cuz, you know … JOBS not so good means bad is GREAT and rates are to be CUT?)

WolfST: Bank of Canada Cuts by 25 basis points, to 4.75% as Economy and Inflation Slowed. QT Continues

Me thinks Paulsen's talking his BOOK. 3 little ideas for him: Debts and Deficits and Issuance

Seems like only yesterday Trump was touting the Trillion Dollar Cap Club: Microsoft Apple Google Amazon. Actually it was 2-11-20. Barely 3 yrs later we have 3T market caps. Nothing flationary THERE :)

Me thinks Paulsen's talking his BOOK. 3 little ideas for him: Debts and Deficits and Issuance

Seems like only yesterday Trump was touting the Trillion Dollar Cap Club: Microsoft Apple Google Amazon. Actually it was 2-11-20. Barely 3 yrs later we have 3T market caps. Nothing flationary THERE :)