while WE slept: USTs marginally lower in QUIET pre ADP trading (volumes ~70% avg); "are we all just tradin' energy?"; "Is the Fed Put Back?" (Yardeni chart); today vs 1950s (DB)

ZH: Job Openings Tumble With Hiring Stuck At 2018Levels (a healthy and snarky run thru data point which was just another in recent string of weakness and so, music to Team Rate Cuts ears…bring back more pricing … see below, DB and Yardeni, for example)

… and with that, bonds continued along their merry way with relentless BID and as best I reckon, there was some selling down against ‘resistance’

10yy: down about 30bps since … this past Thursday and interesting where they’ve paused …4.34 seems to be an inflection point of sorts …

… Oversold conditions can work themselves off in a couple ways … rates move HIGHER (from what looks to be resistance (4.427%) dating back to October of 2023 OR simply time at a price (which might also provide needed cover — DATA — ADP today, NFP Friday — which might move rates lower … remains to be seen … but a large move in a short period of time should be ‘nuff reason to pause.

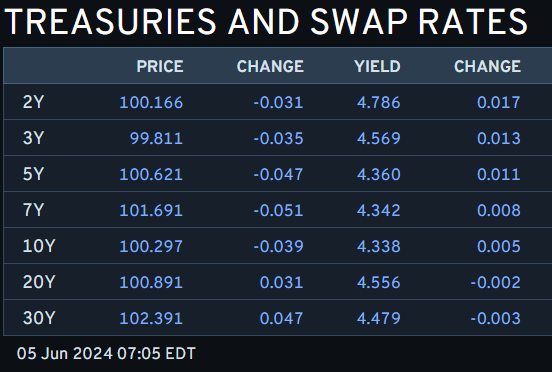

That said, we’ll move right along TO ADP and a relative calm / quiet period (Thursday) awaiting more definitive report in the form of NFP but for now … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are marginally lower across the belly (2s5s10s +0.6bps) in relatively quiet conditions as we await ADP, the S&P Service PMI, and ISM services. UST volumes are running ~70% the 30d average, with light selling activity going through the front-end in Tokyo hours. Flows into the London crossover included profit taking from real money on the recent strength and paying interest in the front-end. The 20y sector is slightly richening (10s20s30s -0.7bps) ahead of the 20yr buyback op ($2bn). APAC equity performance was mixed (SHCOMP -0.8% vs SENSEX +3.2% and NKY -0.9%). Industrial commodities are roughly unch’d with Crude and Copper flat, while Gold is 0.3% higher. The DXY is slightly stronger, with USDJPY +0.8% and USDMXN -1%. S&P futures are showing +9pts here at 7am, with the DAX +0.8% as well…

… Are we all just trading energy?: a comparison of US 5y yields and Crude Oil really puts things in perspective given the symmetry to the yield moves in Q4 2023.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities on a firmer footing, DXY gains & USD/JPY back to 156; US ISM Services due … Bonds are incrementally softer and unreactive to EZ Final PMIs … USTs are slightly softer in a breather from this week's upside ahead of US ISM Services and ADP National Employment. Treasuries are currently holding around the low of 109-26+ with no follow-through from the morning's European/UK data points.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: April JOLTS: The waiting is the hardest part

April JOLTS estimates place the job openings-to-unemployment ratio back at its prepandemic level, in line with the FOMC's soft landing plan, joining other indicators of labor market dynamism such as the hiring rate and separations rate. Upcoming prints for inflation and wages should help show whether its plan is sufficient.

The last week has proved to be a real challenge for markets to work out whether weaker US data is good or bad news for equities. This marks a bit of a change as in recent months both good and bad data were used as a justification for a rally. It does seem we've moved to a more nuanced debate. However before we get too excited about a possible change in emphasis, the S&P 500 is only down -0.25% since returning to trading after Memorial Day last Monday and keeps on bouncing off the weaker data inspired intra-day lows of the last week.

This trend continued yesterday following the April JOLTS report which encouraged another notable fixed income rally with 10yr Treasury yields (-6.3bps) falling for a fourth consecutive session. The combined -28.6bp drop over that time period is the largest such fall in yields since Mid-December. Until the last 100 minutes of US trading equities were lower but another late rally helped edge the S&P 500 (+0.15 %) higher…

The April PCE inflation reading came in line with the expectations and appeared to slowly resume its downward trend. Year-over-year headline PCE inflation fell 4bps to 2.66% while core PCE inflation fell 6bps to 2.75%. Updating our suite of statistical models, we find that our monthly mean estimates for trend inflation declined by only 2bps to 2.9%, while the median estimate dropped by 10bps to 2.9%, the first time both metrics have fallen below 3.0%. While the disinflation trend is likely reasserting itself, our underlying inflation gauge remains elevated.

Indeed, Fed officials mostly maintained their near-term policy outlook that it will take longer to regain the confidence in the disinflation process. Most officials repeated that they will need to see several more months of positive inflation data to affirm that inflation remains on the right track, suggesting that the first rate cut is likely to happen later this year, with September being the earliest timing on inflation grounds alone (See Fed Watcher: More confidence needed until further notice). We continue to expect one rate cut this year in December followed by the completion of a mid-cycle adjustment by mid-2025 (See US outlook update: Trying to reason with election season).

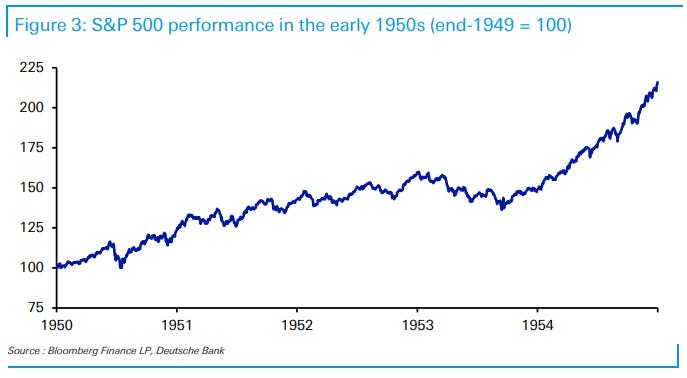

There’s been a lot of discussion over the last couple of years about which period of history our current era is like. The most common comparison has been with the 1970s, due to high inflation and a spike in energy prices. The late-1990s is another where there are parallels, as excitement about tech stocks led to a major equity rally. We’ve also pointed to the late-1960s, when growing quantities of stimulus helped to push up inflation in an environment when unemployment was already very low.

But in recent weeks, we’ve started to see increasing comparisons with the early 1950s and today. Both periods have seen unemployment at historically low levels. Both saw a strong performance for risk assets. Both saw an initial burst of inflation that mostly subsided. And similar to today, the early 1950s was an era of heightened geopolitical risk during the early phase of the Cold War.

This week could well see another parallel. On Friday, if the US unemployment rate remains beneath 4% in the May jobs report, it would mark 28 consecutive months of sub-4% unemployment. That would exceed the 27-month run in the late-1960s, and would therefore mark the longest stretch of sub-4% unemployment since the early 1950s.

Time will tell if the early-1950s offer a good parallel, but if these similarities do hold, there could be a lot of scope for optimism. In particular, low unemployment has often been a spur to productivity growth, as firms find it more difficult to hire workers and become more focused on helping their existing staff to be more productive. Given the growth of AI in our own time, this suggests there could well be some upside risk to economic growth over the years ahead.

Let’s run through some of these parallels:

1. Unemployment is at historically low levels

2. Risk assets are performing very strongly

3. Both periods saw an initial burst of inflation which mostly subsided.

4. Both eras were periods of heightened geopolitical risk.

Summary April marked a step forward in getting inflation back on a downward path after price growth picked up in Q1. Yet the FOMC will need to see inflation downshift further in order to gain the "greater confidence" needed to eventually reduce the fed funds rate. May's CPI report is unlikely to suggest inflation is rapidly approaching the Fed's target, but it should at least offer more evidence that the first quarter's flare-up has subsided.

We estimate headline CPI rose 0.1% in May, which would mark the smallest monthly gain since last October thanks in part to an unusual drop in gasoline prices for this time of year. Excluding food and energy, the CPI likely advanced 0.3% again in May, with the drivers little different from April. Core goods prices likely fell another tenth or two amid the ongoing slide in vehicle prices and a modest decline in other core goods. Prices for core services look to have increased 0.4% for a second straight month amid the slow moderation in housing and other services inflation.

Another 0.3% monthly increase in core CPI would nudge the year-over-year rate down to a three-year low of 3.5% and point to core PCE inflation edging down to 2.7% in May. Inflation as measured on a year-ago basis likely will hold at these rates through year-end amid unfavorable base effects. That said, we continue to look for monthly readings to gradually trend lower as inflation pressures subside. The slow pace of improvement may not be enough to convince some Fed officials over the next few months that inflation is headed back to target on a sustained basis.

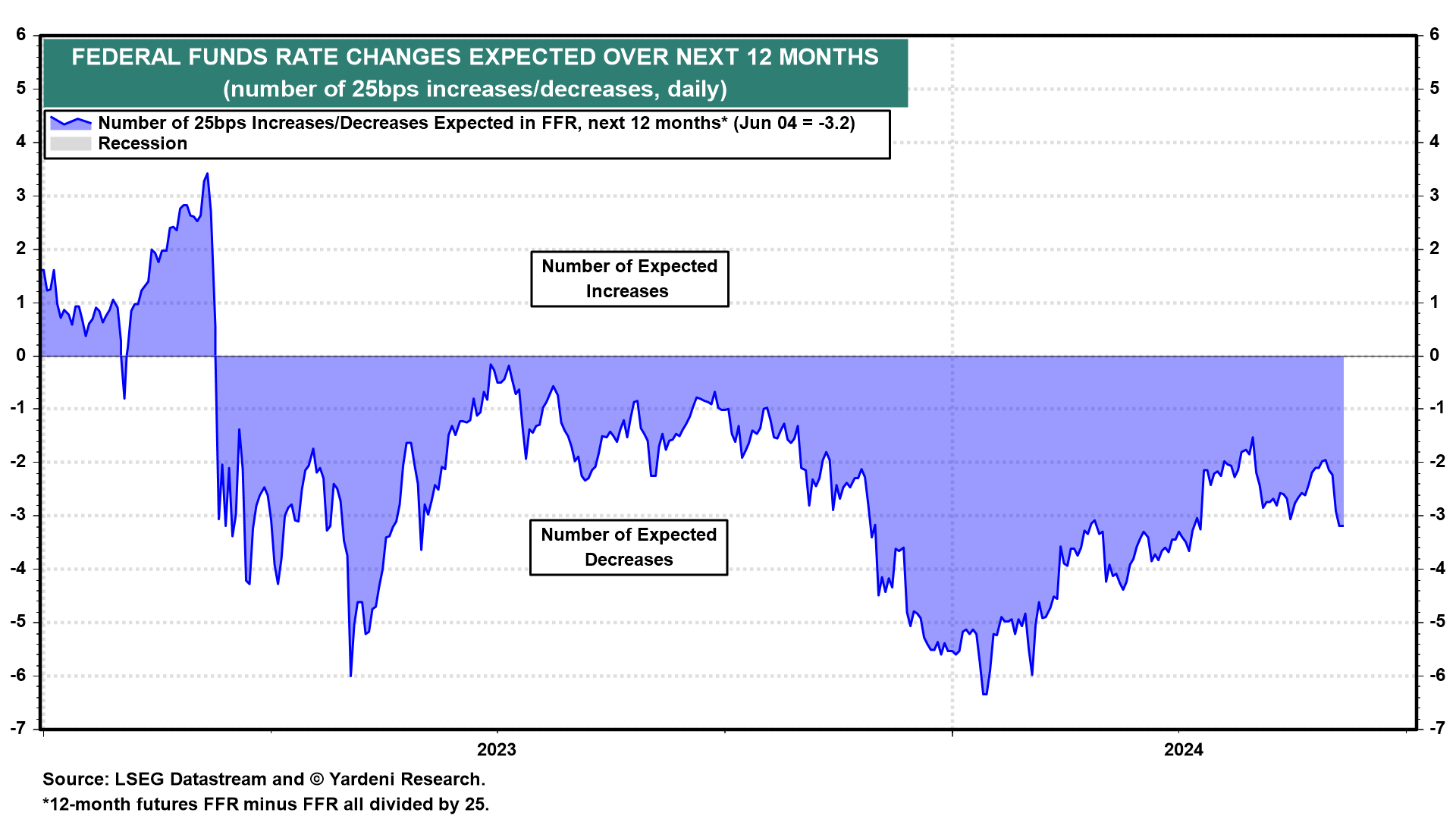

Yardeni: Is the Fed Put Back? (great chart … here we go again?)

The financial markets seem to believe that the Fed Put is back. The recent batch of weaker-than-expected economic indicators raised the number of expected 25bps cuts in the federal funds rate (FFR) from 2 to 3 over the next 12 months (chart). That's according to the basis-point spread between the 12-month FFR futures and the actual FFR divided by 25bps. Investors must be confident that inflation is getting close enough to the Fed's 2.0% target so that it will respond quickly if the economy is (finally) about to fall into a recession. If so, then it won't fall into a recession! That explains why the stock market keeps bouncing back on the initial negative reaction to bad news, which is good news if it means the Fed Put is back!

There are two assumptions being made that might be wrong. First: Inflation might not be close enough to the Fed's target to warrant easing even if the economy continues to weaken. Second: The latest batch of weak economic indicators doesn't mean the economy is falling into a recession. More likely, it might finally be experiencing a soft landing rather than going into a hard landing. The Citigroup Economic Surprise Index is negative currently, but not signaling a recession (chart). Furthermore, it usually swings back into positive territory as long as there's no recession out there.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Pimco Says ‘Generational Reset’ on Yields to Spur a Bond Revival (For details on our outlook for the global economy and investment implications, read the full Secular Outlook, “Yield Advantage.”)

Sees receding inflation to affirm US neutral rate at 2% to 3%

Says markets ignoring recession risk makes bonds a cheap hedge

… “Active fixed income is positioned to perform well if there are no recessions over our secular horizon and to perform even better if there are,” Pimco’s Richard Clarida, Andrew Balls and Daniel Ivascyn wrote in an outlook released Tuesday. As prices climb and inflation recedes, they expect bonds will be even more attractive than cash…

… This time is different as high quality bond benchmarks — including the Bloomberg US Aggregate and the Global Aggregate — are providing 5% or higher yields. “Starting yields are highly predictive of bond returns over a multiyear horizon,” they said.

“Markets don’t appear to price significant recession risk, meaning bonds may be an inexpensive means to hedge that risk,” they added…

Bloomberg: Bond Traders Pile Into Fresh Bets on Faster Pace of Fed Cuts

Dovish options targeted while short covering seen in futures

Fed swaps shift full rate cut to November from December

Bloomberg: Stocks Love ISM, But Payrolls Is Now Bad For Bonds

In a NYT column today Krugman argued that the Fed is fighting the wrong war—“’Goodbye Inflation, Hello Recession?” This isn’t the first time he has argued the war on inflation is won. However, it is striking that he makes this argument following four strong CPI and PCE reports in a row. Where does this optimism come from?

He starts by noting that given all the data available “you can always find a way to justify either optimism or pessimism.” Instead, he argues, focus on the “story.”

… I agree with Krugman that there is some risk of a recession. However, unless the war on inflation is truly won, the Fed should be taking some risk of a mild recession. Moreover, the “R” word sounds ominous, but what kind of a recession are we talking about? Only the most pessimistic forecasters expect the unemployment rate to rise above 5%. A peak of 5% would be a great outcome by historic standards. So yes, I think the Fed should not be cutting any time soon.

US yields have been falling for four days straight on growth pessimism. Bund yields have been dragged lower too, but have less room to fall much further from here. Friday's US payrolls will be an important data point to watch, but with yields already down significantly markets are already positioned for a disappointment

{kind=link}

No this isn't Zimbabwe......

U.S. Interest Expense since 1970 - is this sustainable?

https://t.co/3VUeYpZjcd

Lab-grown diamonds, WTF? New 1 on me....is it here? The Summer Doldrums that is?