With the geopolitical turn of events over the weekend (increasing tensions, higher oil prices DO pose a problem for the Fed and rate CUTS **IF** they are sustained) along with some financial chicanery in Chinese markets (stopping short of ‘official’ ban of short-selling BUT … see below for more) combined with this weeks domestic event risks (ADP, Treasury reFUNding, NFP) and my limited capacity to help, I’ll quit while I’m behind and try to keep MY thoughts real brief.

AND with all the aforementioned pushing and pulling it’s worth noting that USTs are … down couple basis points. With a couple of looks at long bonds (here and here), today I’ll have a quick peek at 2yy — a rate cut and F2Q (in years past) proxy — with weekly momentum more overBOUGHT (so, ripe for correction HIGHER in yields) to the DAILY showing the opposite …

… meanwhile yields (4.33) are a touch below middle of larger ranger at play here (5.25-3.60) and with weekly overBOUGHT whereas daily is overSOLD, it really comes back to your own view and timeframe…

MLets move on TO a snapshot OF USTs as of 734a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher with the curve modestly flatter (see attachments and discussion) with Gilts and Bunds outperforming amid FTQ conditions (US soldiers killed by drone in Jordan). DXY is higher (+0.17%) while front WTI futures are little changed. Asian stocks were generally higher, EU and UK share markets are mixed while ES futures are showing +0.1% here at 7:10am. Our overnight US rates flows saw a lackluster Asian session with some real$ selling in intermediates (fast$ interest to flatten too) seen after the FTQ open higher. During London's AM hours we saw better buying from central banks and real$ in the 5y-7y sector. Overnight Treasury volume was ~70% of average.

… Today's attachments sketch these 'risks' out pretty well. Our first attachment looks at the set-up in Treasury 2-years in a daily chart with its associated momentum study in the lower panel. The oscillator lines have merged (little recent thrust in yields save for sideways) and the level(s) is nowhere near the extremes that might warn of a potential trend phase shift. Simply, 2's look stuck and there's little indication that they're about to up-stakes and head somewhere else.

At the other end of the curve, 30yr Treasuries appear to be reversing their ~month-long bear trend with daily momentum (lower panel, circled) flipping bullishly from a still deeply 'oversold' reading. Bonds look tactically great here while there's little in the shorter-term 2yr yield chart that resonates with us... Bottom line: there's a strong whiff of emerging bull-flattening risks to start this week in US rates.

What then of the year of the STEEPENING?? Nevermind … and for some MORE of the news you can use » The Morning Hark - 24 Jan 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in addition TO what was compiled and sent Saturday) …

We think the stage is set for the ECB to cut in April, even if it didn’t offer any definitive signal at its meeting last week. Risk/reward continues to favor receiving April meeting OIS, while the EUR remains an appealing funder for higher yielding EM currencies.

US inflation looks supportive of rate cuts, but above trend growth may inject a measure of caution into Fed messaging. We maintain our curve steepener and short USD biases but are attentive to growth momentum ahead of another potentially firm jobs report.

Treasury issuance announcements and any information around the Fed’s QT will be the other key focus. We remain positioned for pressure to build on front-end spreads and funding costs.

… Details incoming on the Treasury supply/demand picture: Away from the policy rate and data side of the coin in the US, the coming week will also be key in terms of the supply/demand landscape for Treasuries. Prior to the Fed decision, Treasury will announce its borrowing estimates for Q1 and Q2 2024 on Monday, followed by the broader refunding decision on Wednesday morning, where we’ll get details on auction sizes. While the Monday information is a bit more niche in the broader scheme of things, a higher-than-expected estimate at the end of July precipitated the first leg of the supply-driven sell-off in US rates. Having revisited our estimates for deficit seasonals, we now expect Q1 marketable borrowing of USD809bn (near Treasury’s estimate from November) and USD284bn in Q2, which we see as setting the stage for a third and final round of coupon size increases to be announced on Wednesday. Our baseline would see quarterly duration supply rise to about USD700bn 10y equivalents, up nearly 30% from when auction size increases began (Figure 3).

Goldilocks: Higher Costs Due to Red Sea Shipping Disruptions Imply Modest Upside to Global Inflation (but … but I thought it was no big deal…reading on, THE view is it really isn’t even a rounding error … ?)

Sea freight costs have risen sharply due to Red Sea shipping disruptions, with shipping costs from Asia to Europe rising by 350% and by 100% from Asia to the US. Some commentators and investors worry that these cost increases could meaningfully raise global goods inflation, especially since inflation pressures from post-pandemic supply disruptions remain relatively fresh on their minds.

We are less concerned that higher costs will significantly raise inflation for two reasons. First, the current increase in shipping costs does not coincide with the widespread factory shutdowns and transfer-driven demand surges that helped send goods inflation soaring in the aftermath of the pandemic, suggesting less scope for amplification of cost pressures today.

Second, international transport costs account for a small share of the price of final consumption goods (around 1.5% on average), with sea freight accounting for an even smaller share (around 0.7%). Under reasonable pass-through assumptions, a 100% increase in the cost of sea freight therefore only raises core goods inflation by around 0.4pp and overall core inflation by around 0.1pp.

Combining our estimated rules of thumb with the observed increases in sea freight rates, we estimate higher shipping costs will raise global core inflation by roughly 0.1pp in 2024, with somewhat larger effects in Europe and somewhat smaller effects in the US. We therefore see only modest upside inflation pressure from Red Sea shipping disruptions barring a more significant increase in transport costs going forward.

Goldilocks: January FOMC Preview: Keeping a March Cut on the Table

Heading into the January FOMC meeting, the market is priced for a close to 50% chance of a rate cut at the next meeting in March. The FOMC will likely aim to keep a March cut on the table without sending a decisive signal by removing the outdated hiking bias from its statement and noting that future policy changes will depend on upcoming inflation and other data.

Specifically, the FOMC could revise its statement by borrowing language from the December minutes to note that it expects that it will “be appropriate for policy to remain at a restrictive stance until inflation is clearly moving down sustainably toward the Committee’s objective,” dropping the minutes’ “for some time” qualifier to make it clear that a March cut is possible. Chair Powell could then respond to questions about a March cut by simply pointing out that there are still two rounds of inflation data and annual revisions to the CPI yet to come.

We continue to expect the FOMC to deliver a first cut in March and 5 cuts in total in 2024. The main reason is that progress on inflation has already surpassed the threshold the FOMC has given. While we continue to see cuts as optional and suspect that Fed officials will become a bit less concerned about risks to the economy from keeping rates high after the Q4 GDP print, this is only a secondary reason for cutting, and there are some modest downside risks to inflation and the labor market that could still provide additional reasons for the FOMC to cut sooner rather than later.

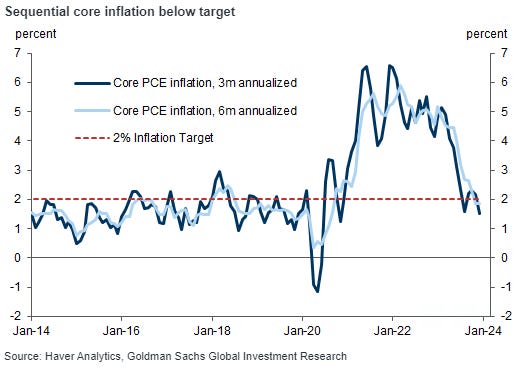

Soft landing on track. The broad data still points firmly in the direction of easing inflation pressure and resilient growth, especially in the US. Core PCE inflation is below the 2% target over 6 months (1.9% annualized) and even more so on a 3-month basis (1.5% annualized), alongside solid US growth data. While disinflationary pressures are global, US activity still looks more resilient than in other major regions, and manufacturing looks soft, so the US consumer remains the brightest part of the global demand picture. Because markets are already priced for good outcomes, we expect periodic wobbles around this benign path. But we still think it makes sense to fade those pullbacks and expect US equities and credit to make new highs, as they have been. Our central macro forecast generally supports low volatility and high valuations, even if that makes it uncomfortable to be long. Interest rate and FX markets have modestly reduced their expectations for Fed cuts lately, and longer-dated yields have drifted higher since the start of the year. But the risks around the rate path now look more balanced. If inflation trends continue to move lower and reduced easing expectations are largely driven by better growth, we expect risk markets to remain on an upward trend.

MS Sunday Start: What's Next in Global Macro: QT Will End...but Not All That Soon

Neither we nor markets expect a policy move at this week’s Fed meeting, but no doubt we will all be looking for hints on QT. Nothing explicit is likely in the policy statement, but Chair Powell may well be asked about it. Our outlook is that while the FOMC may start the discussions around tapering QT as soon as at this meeting, tapering itself is still a ways off, and the actual end of QT will come early next year…

…So, the next step is for the Fed to shift from “talking about talking about tapering QT” to actually talking about tapering QT. Only after that step will we start to look for the end of QT, which the Fed will determine with an eye on money market conditions. In particular, the Fed is looking at whether SOFR is trading below the rate the Fed pays on reserves, in which case it will likely judge conditions to be accommodative, or above the rate the Fed pays on reserves, in which case the Fed’s calculus will change and the discussions about the end of QT will pick up steam.

MS The Weekly Worldview: How bearish should we be on China? (not directly related TO Evergrande but…)

China's economic data remains soft. The recent policy intervention in China will not be enough to combat low growth and debt-deflation risks.

Recent stimulus has come on the heels of yet more weakness in economic data. The GDP deflator for China has been in outright deflation, and we are now tracking a mere 0.1% for 2024 as a whole. In the current circumstances, the GDP deflator is better measure than consumer prices because consumption is a smaller share of GDP in China than most other economies, and this deflator is more closely tied to corporate earnings at all stages of production. More broadly, the soft start to 2024 is also visible in leading indicators, including but not limited to housing sales and construction activity.

… And from Global Wall Street inbox TO the WWW,

AcademySecurities (via ZH): This Week Will Be Determined By What Powell Says Between 2:30pm And 3:00pm ET on Wednesday

Apollo: Supply Chain Issues Coming Back for Container and Air

The price of transporting a container is rising and air freight rates are increasing, but the ongoing supply chain problems are not broad based like the way they were during the pandemic, see our chart book available here.

Bloomberg: While Fed studies nuance, Americans see a canyon (Authers OpED)

… Definitional issues now raise their ugly head. At the committee’s meeting last May, Chair Jerome Powell introduced his preferred definition, which subtracts the one-year bond market breakeven rate of inflation from the effective fed funds rates. At the time, that made real rates look far higher than they did using most other logical alternative measures, so it looked as though he might be establishing a rationale for cuts. That is even more the case now. Subtract current core CPI inflation from fed funds, or take the yield on 10-year Treasury Inflation-Protected Securities (TIPS), and real rates look considerably less alarming:

In this context, it’s interesting that the WSJ chose to graph real rates using the Powell definition. Is it as concerning a measure as it looks? Arguably not. Taking the broad measures of financial conditions published by Goldman Sachs and by Bloomberg ourselves, which include risk appetite from the stock market, bonds, and commodities, we find they are in agreement that life in the financial space at present is distinctly easy.

Bloomberg: China Tightens Securities Lending Rule to Support Stock Market

Sam Ro from TKer: Whether or not the Fed cuts rates is not the right question

… I’m no monetary policy economist. But as I discussed on the Investopedia Express podcast earlier this month, I think concerns about the Fed’s next move on interest rates are a bit overblown.

First of all, we’re talking about a potential 25-basis-point cut from a range of 5.25% to 5.5%. Sure, that’s not insignificant. But that’s nowhere near as big a deal as it was when we were talking about 25-, 50-, and 75-basis-point rate hikes from near 0%.

In other words, the stakes for the upcoming Fed policy meetings aren’t nearly as high as they were in 2022 and 2023.

Third, we have to keep in mind that rate cuts and rate hikes — in and of themselves — aren’t the real issue. Rather, they represent reactions to real issues…

…The bottom line I think we’ll probably continue to hear pundits warn that rate-cut odds are coming down and argue this is bearish for stocks.

But before buying into that argument, we have to understand the economic circumstances that would cause the Fed to put off rate cuts.

If it’s because the economy is proving to be stronger than expected, then it’s no sure thing that keeping monetary policy tight is necessarily bad news — as we learned all of last year. By the way, it is the case that the economy has been proving stronger than expected as inflation rates continue to cool. And even as the odds of a rate cut have declined, the S&P 500 has been hitting fresh record highs.

And amid all this, the debate is over a relatively small move in the Fed’s benchmark interest rate. That is to say maybe the Fed's next move just isn't that big of a deal.

As always, context matters — especially when we’re thinking about developments that appear bullish or bearish for stocks.

*One more quick thought While we’re on the subject, we should also consider the possible scenario the Fed begins cutting rates because the economy takes a significant turn for the worse. As Carson Group’s Ryan Detrick observed, rate cuts that were intended to stimulate the economy amid a recession came with the S&P 500 falling an average of 11.6% in the year that followed.

This is a scenario where the rising odds of a rate cut is not necessarily a bullish signal. Another reminder that context matters…

Could be my anti-49er bias (h/t Kapernick), but I (and the Pros) say Race to Place your bets on the Chiefs. I'm thinking of making the drive to State Line of Nevada to place bets myself. Appears Mahomes and Reid only lose to Brady in the playoffs/SB....

Could be my anti-49er bias (h/t Kapernick), but I (and the Pros) say Race to Place your bets on the Chiefs. I'm thinking of making the drive to State Line of Nevada to place bets myself. Appears Mahomes and Reid only lose to Brady in the playoffs/SB....