… Bonds are modestly firmer and in proximity to yesterday’s highs

… and with that in mind, BONDS …

… I’ve attempted to highlight momentum — overSOLD — rolling over, crossing in a BULLISH (lower yields) fashion and the last time we did this, long bonds up nearer 5.25% … question then is if the setup the same, wil we rally over a 100bps lower here now?

My guess is NO BUT momentum can be worked off with somewhat lower yields and / or TIME AT A PRICE … Will have a look at longer-term WEEKLY over the weekend before I’d place any chips down on the table BUT … for those who were out last weekend buyin’ 5s, the idea that bonds are holding at / near ‘support’ (4.42% above) IS interesting …

Even more so given the DATA deluge yesterday …

ZH: Initial Jobless Claims Bounce Back To 1-Month-Highs (From Near 54-Year Lows) (GOOD for rate cut ‘istas)

ZH: Q4 GDP Unexpectedly Soars, Driven By Lack Of Destocking And An RV Spending Spree (for somewhat more, see ZH below on the one YUGE PROBLEM)

ZH: 'Need Moar War' - GDP-Driving Capital Goods Shipments Are Down Year-Over-Year

ZH: National Economic Activity Unexpectedly Declined In December; Chicago Fed Index Shows (GOOD for rate cut ‘istas)

… set us up for final installment of US Treasury supply …

ZH: Solid 7Y Auction Sees Jump In Foreign Demand, Sends Yields Lower

… While the headline print was subpar, the rest of the auction was solid, with the bid to cover rising from 2.498 to 2.574, the highest since October.

The internals were even stronger, with Indirects awarded 69.1% of the auction, the highest since October, and above the 68.1% recent average; and with Directs taking down 17.0%, Dealers were left holding 13.94%, the lowest since October.

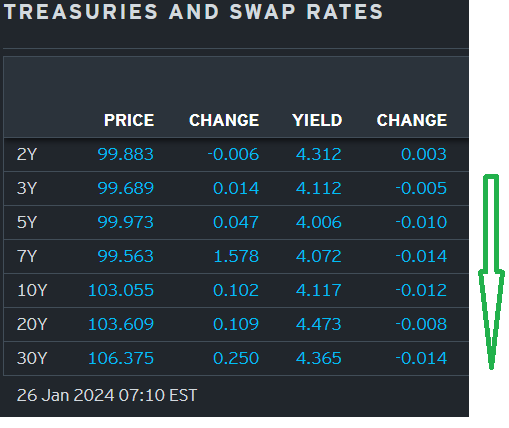

… and now we’re all staring down the final hurdle between US and the weekend I’ll not delay any further. Here is a snapshot OF USTs as of 710a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve pivoting flatter around a little-changed intermediate sector this morning. DXY is lower (-0.3%) while front WTI futures are lower too (-0.7%, see attachments). Asian stocks were generally lower, EU and UK share markets are all higher (SX5E +0.95%) while ES futures are showing -0.2% here at 6:50am. Our overnight US rates flows saw a choppy overnight trade but with a lingering bid with Tsy coupon supply out of the way for the next 11 days. We had light selling of the belly from systematic names alongside steepening interest in 5s10s. Overnight Treasury volume was ~85% of average with standout average turnover seen in 7yrs (136%) after yesterday's auction of the same.

…US 5yrs don't show the same tactical bull vibes that German and UK 5's do right now with daily momentum barely even getting to 'oversold' levels during the recent back-up. Such may be a legacy of the very good dip buying/receiving reported by my colleagues above. We'll spot local support holding up near 4.102% with major range support levels highlighted around that. Bottom line: we're not sure what to make of this 5yr Treasury chart just yet...

… Hmmm okie dokie. I’m SURE those out LAST weekend noting bullish view of 5s are well aware and so I’ll move along … and for some MORE of the news you can use » The Morning Hark - 26 Jan 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … Lots of GDP recaps and victory laps, for sure … with a little bit on ECB …

ABNAmro: ECB sounds more constructive on inflation but we stick to June call

The Governing Council struck a more optimistic tone on inflation following the January monetary policy meeting. While taken in isolation, this would open the door for an early rate cut, given that ECB officials spent the whole of last week guiding the market towards a later rate cut, we are sticking to our June call for the start of the easing cycle.

BARCAP: Q4 GDP posts upside surprise on continued inventory investment

The advance estimate shows GDP decelerated from 4.9% to 3.3% q/q saar in Q4, surpassing consensus expectations. The bulk of the upside surprise came from stock building, while consumer spending appears poised to continue into Q1 24. All told, an abrupt turn to below-trend growth seems unlikely.

BloombergBNP US Q4 GDP: Consumer vigor implies momentum spilling into 2024

KEY MESSAGES

A series of solid economic data of late culminated in a Q4 GDP release showing a sizable acceleration in economic growth in H2 2023, as the economy grew at 3.3% saar on the back of a 4.9% pace in Q3, driven by robust consumer spending.

The headline reading was inflated by a positive contribution from exports and inventories, which added 0.5pp to growth, against expectations for a sizable drag. Final sales to domestic purchasers (GDP excluding inventories and trade) growth slowed to 2.7% from 3.5% prior, in line with our projections. The data reflects underlying growth is decelerating but remains robust and implies solid momentum going into the beginning of 2024. Continued buildup in inventories likely suggests companies are restocking in anticipation of continued strength in growth.

Following the advance release of Q4 GDP, confirming our expectations for a strong contribution from personal consumption, we have revised our projections for H1 2024. We now estimate GDP to grow at 1.5% q/q saar in Q1 (previously estimated 0.0%) and entirely revise away the Q2 contraction expectation (we now project growth at 0.7% q/q saar as opposed to -1.3%). The new estimate leaves growth below potential in 2024, and for the year as a whole implies growth in the vicinity of 1.0%.

The scope of any further upgrades to the GDP profile will depend on the trajectory of financial conditions. As we saw in the wake of the Silicon Valley Bank failure, the subsequent easing of financial conditions resulted in a significant upside surprise to GDP data in Q3. This remains a risk scenario for 2024 and could be altered through Fed communication.

Continued declines in the personal savings rate (4.0% versus 4.2% prior) as a percentage of disposable personal income suggest consumers are becoming more optimistic in the outlook as they increasingly rely on credit to finance spending on goods and services.

We expect the FOMC to keep rates unchanged at the January meeting, with communications likely to lean against imminent cuts.

A faint hawkish bias may remain in the statement, though we admit it will be a close call. If not, we expect the committee to introduce language signaling a patient approach before adjusting policy settings.

Recent easing in financial conditions and signs of economic resilience afford the FOMC some time to judge whether inflation is durably converging to the 2% target.

Our base case is for 150bp of rate cuts this year, starting in May. Though we cannot rule out a March move if data warrants (such as a stall in hiring or other activity data), our recent upgrade to economic growth in H1 2024 raises the alternative risk that cuts are delayed or diminished.

We expect Fed officials to devote time at the meeting to discussing QT tapering and for Chair Powell to address the topic in the press conference.

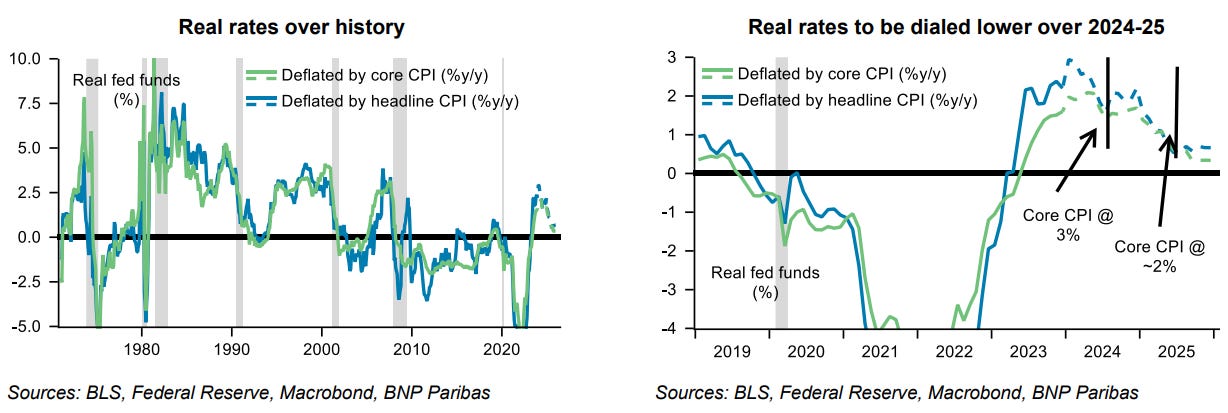

… Normalization in nominal rates as inflation subsides: We expect this cutting cycle to be different from most. Instead of cutting quickly in response to a shock, 2024 should be the year the Fed starts to dial back policy restriction in response to inflation converging toward target. The charts below show the funds rate adjusted for CPI inflation, one proxy for relative restriction over time.

Our view is yearend fed funds of 4.0% and 2.75% in 2024 and 2025, respectively…

DB: To AIT or not to AIT (this one needs further review…)

To AIT. Into covid, the Fed developed the concept of Average Inflation Targeting (AIT) as its new policy framework. In that framework, the Fed would wait for long-term average inflation (e.g. 3y or 5y average) to exceed target before tightening monetary policy. While 3m/3m and 6m/6m core PCE inflation was well above target in January 2021 and real policy rates were deeply negative and well below any reasonable estimate of neutral, the Fed did follow AIT and wait for the long-term averages to be comfortably above 2% to start hiking in March 2022.

Or not to AIT? Today, the 3y and 5y average core PCE are both comfortably above target and are expected to remain so for at least a year. Thus, in an AIT framework, the Fed should not consider easing policy this year. Still, recent Fedspeak, the SEP and market pricing suggest that the Fed is likely to initiate its rate cut cycle by mid-year. The easing cycle is justified by the fact that 3m/3m and 6m/6m core PCE inflation fell below target and the desire to avoid real policy rates which are already in restrictive territory to rise further.

Bottom line: If you want a framework to survive the test of time, keep it sophisticatedly simple

Goldilocks: Q4 GDP Growth Remains Strong at +3.3%; Core Capex Orders Rise; Jobless Claims Rebound; Goods Trade Deficit Narrows

BOTTOM LINE: Real GDP rose 3.3% annualized in the fourth quarter, well above consensus. The composition was not quite as strong, as inventories contributed 0.07pp to GDP growth and we assume will weigh on the Q1 pace. Nonetheless, demand growth proceeded at a strong clip, with domestic final sales rising 2.7% annualized once again led by consumer and government spending. Following this morning’s data, we left our December core PCE estimate unchanged at +0.18% (mom), now corresponding to a year-over-year rate of +2.93%. We will launch Q1 GDP tracking following tomorrow’s personal income and spending details. The goods trade deficit narrowed in December, driven by an increase in exports. Durable goods orders were unchanged in December, below expectations for a moderate increase, while core capital goods orders grew by slightly more than expected. Initial claims rebounded by more than expected.

JEFF: Q4 GDP Up 3.3%... A Strong Follow-Up to an Impressive Q3

■ Q4 GDP rose 3.3%, stronger than the consensus forecast of +2.0%. ■ Overall, the numbers are pretty surprising. The bulk of growth was driven by strong consumer spending as PCE rose 2.8% q/q and contributed 1.9 ppts to top-line growth. This was modestly above expectations, but inventories and government investment were quite a bit stronger than we were expecting. Conversely, investment in both residential and nonresidential structures was softer than what was implied by the monthly data. ■ The Q3 and Q4 growth data have been extremely impressive, but they set a very high bar for Q1. ■ Bottom line, the consumer went nuts in Q3, spending tons of money on vacation, entertainment, and recreation experiences. Whether fueled by credit or by wealth effects among higher-end consumers, they maintained this strong momentum into Q4. ■ Despite the consumer strength, we are not altering our long-term view. Components of GDP that tend to be meanreverting have been making outsize contributions to growth, and we expect a pullback in Q1. Cooling growth along with continued disinflation should keep the Fed on track for a 25 bp rate cut in March.

RBC: U.S. GDP strong in Q4 alongside moderate price growth (so, strong is GOOD for rate cuts?? askin’ for a friend)

… Bottom line: The U.S. economy remained resilient through the end of 2023, with output growth for the full year accelerating from 2022’s gain despite sharply higher interest rates. There are still signs that economic momentum is slowing – the household saving rate continues to run below pre-pandemic levels and declining job openings are flagging a softening in the labour market. But inflation has also slowed without the amount of economic pain that was feared when the Federal Reserve started aggressively hiking interest rates to cool an overheating economy and price growth. We continue to look for U.S. GDP growth to slow in the first half of 2024 and for the unemployment rate to drift higher. But a softer economy and slower price growth are expected to allow the Fed to begin to ease off the monetary policy brakes by pivoting to moderate interest rate cuts by mid-year.

GDP exhibits surprising strength in inventories Real GDP growth in Q4 topped our (1.6%) and consensus (2.0%) estimates, rising 3.3% (saar). Surprisingly, the steep drop in the contribution of inventory investment we expected (we thought a drag of 0.6 pp) instead was reported to be a 0.1 pp positive contribution. That comes on top of the 1.3 pp inventory stocking added to Q3. Net exports also added 0.4 pp to growth in Q4, and which was expected to weigh on GDP in Q4, but the reported narrowing of the trade balance in the quarter was better than previously expected and services exports posted strong growth in the quarter…

… The implications of the big miss in inventories is negative going forward. If the BEA assesses that the change in private inventories continued to build in Q4 upon the large build in Q3, that implies more weakness going forward, all else equal. The information on private domestic demand in the report arrived roughly in line with expectations. Government spending was a little better than expected (3.3%), but most components slowed from Q3. The guts of the report this morning were not really news, while the inventory…

… Inflation implications: monthly PCE prices update Using today’s data to back out the implied December increase in core PCE prices suggests a 0.16% increase (both if there were no revision to either October or November, and if November and October show the small revisions that we expect them to). This is about 1 bp higher than the 15 bp rise that we have been projecting since last week’s import prices for December were released. The extra bp would still suggest the 12-month change in core PCE prices falls to 2.9%.

In today's Q4 GDP release, headline PCE prices increased 1.66% at an annual rate, in line with our expectations for a 1.65% increase, while core PCE prices increased 1.99%, also in line with our expectations for a 1.98% increase. For the four quarters of 2023 headline PCE inflation was 2.72% and core PCE inflation was 3.154% --- headline PCE inflation was a little below the FOMC’s December SEP for a 2.8% increase while core PCE inflation was just barely in line with the SEP projection of 3.2%.

Wells Fargo: Fourth Quarter GDP: Strong Growth With Low Inflation (so, rate cuts? YES — 25bps in May …)

Summary

Real GDP grew at an annualized rate of 3.3% on a sequential basis in the fourth quarter, which was significantly stronger than the 2.0% rate that the consensus forecast had anticipated.

GDP growth was more or less well-balanced in the fourth quarter. Real consumer spending grew at a solid rate, real investment spending eked out a modest gain and real government spending also rose.

The surprise in the overall GDP growth rate came from real net exports, which added 0.4 percentage points to GDP growth. The quarterly data imply that real exports grew at a robust rate at the end of the year.

Real GDP grew 3.1% between Q4-2022 and Q4-2023. Despite 525 bps of Fed rate hikes since March 2022, the U.S. economy continues to power ahead.

The core PCE deflator, which Fed officials view as the best measure of the underlying pace of consumer price inflation, rose at an annualized rate of only 2.0% on a sequential basis in Q4, the second consecutive quarter in which prices have risen at the FOMC's target of 2%.

The favorable news on inflation gives the FOMC leeway to begin an easing cycle in coming months. We look for the Committee to cut rates by 25 bps at its May 1 meeting, although today's inflation data will keep market hopes for a rate cut at the March 20 meeting alive.

Wells Fargo: Despite Flat Headline, Durables Report Signals Brighter Days Ahead (bright days ahead even brighter if Fed cuts rate, amIright?)

Summary Durable goods orders may have been virtually unchanged in December, held back by diminished demand for aircraft, but the underlying details point to a much-needed turnaround for long-lasting manufactured goods.

… And from Global Wall Street inbox TO the WWW,

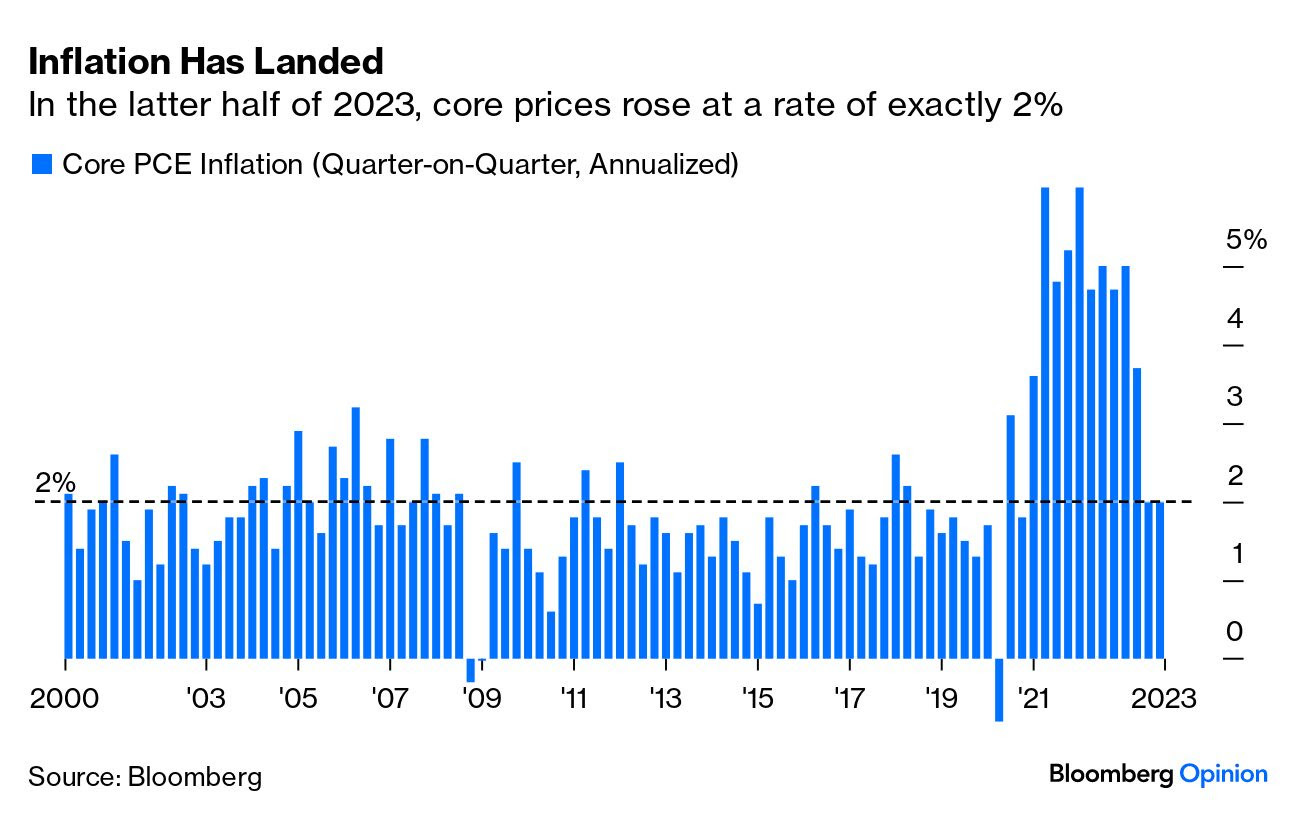

Bloomberg: Fed fears being sucked under a Trump riptide (Authers’ OpED — aside from political angle, “…inflation has been beaten…”)

Uber-caution learned from the 1970s and distrust of a Trump backlash are weighing against early rate cuts despite the turn in inflation.

… Ostensibly, the download of the government’s first estimate of gross domestic product in the final quarter of last year should support those who think inflation has been beaten. For the second quarter in succession, core prices rose at an annualized rate of exactly 2%, which happens to be the Federal Reserve’s target:

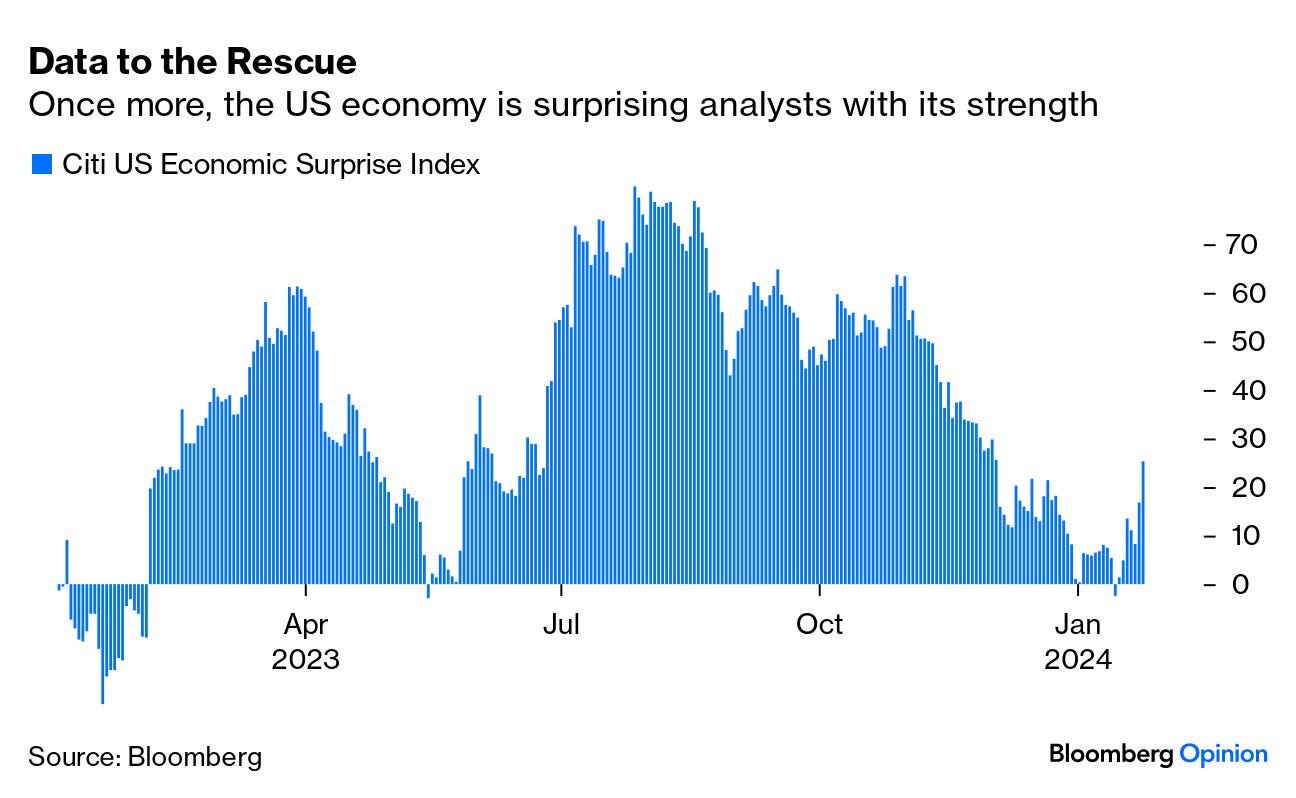

The problem, if it can be called that, is that the economy appears to be in rude health. The figures are often revised, but an annualized growth rate of 3.3%, at a time when many were braced for a recession to be well underway, makes clear that growth is surprisingly good. If we look at Citigroup’s Economic Surprise Index, a gauge of how incoming data compares to prior expectations, we find that it’s jumped back into positive territory this month, after very briefly turningslightly negative:

Rate cuts are generally a measure to be used when things are going wrong. These are not the numbers that would be produced by an economy desperately in need of a rate cut. So while the data begin to look as though it would be safe for the Fed to start cutting soon, they also suggest zero urgency. Barring major data surprises in either direction, this is likely still to be true when the Federal Open Markets Committee meets in March. Expect the next few weeks to be consumed by debate over how the Fed should approach this decision — more scared of cutting too soon, or cutting too late? And how can or should politics affect their call?

FRED: How common is “moonlighting”? (too common and so, good for rate cut ‘istas?)

Moonlighting—simultaneously holding multiple jobs—is fascinating from a macro labor economics perspective: It adds jobs to the economy without increasing the actual level of employment. Fortunately, FRED provides data to help us understand how prevalent this group of workers is in the US economy.

The blue line in the FRED graph above plots the fraction of employed individuals simultaneously holding more than one job for each month. It shows that moonlighters make up a sizable fraction of the employed. From 1995 to the present, about 5-6% of employed persons have held multiple jobs in any given month. The proportion of moonlighters tends to drop at the onset of recessions and recovers afterward, with the starkest decrease occurring during the COVID-19 recession.

How common is moonlighting among men vs. women? The proportion of employed women who hold multiple jobs (green line) is now noticeably higher than the proportion of employed men who do (red line). This divergence became particularly clear after the 2001 recession, with differences of up to 1 percentage point. Since the COVID-19 recession, the proportion of women holding multiple jobs has exceeded its pre-pandemic level, while the proportion of men holding multiple jobs is similar to its pre-pandemic level.

ING: US GDP confounds slowdown fears, but 'job done' on inflation

Fourth-quarter 2023 GDP growth beat all expectations thanks to strong consumer and government spending plus a positive contribution from net trade. First-quarter GDP growth is expected to be weaker based on business surveys, but the Fed is close to declaring victory on inflation with the second consecutive 2% quarterly core inflation reading.

WolfST: The Year of the Recession that Didn’t Come: Our Drunken Sailors Partied & Spent, GDP Jumped

ZH: The GDP Number Was Great... There Is Just One Huge Problem

… So the next time you read something like this from the imposter in the White House...

... respond that today we also learned that our debt grew by $2.581 trillion last year. This means that every dollar in GDP growth cost $1.69 in new debt, and also means that every new job cost futures generations of Americans $957,100.48.

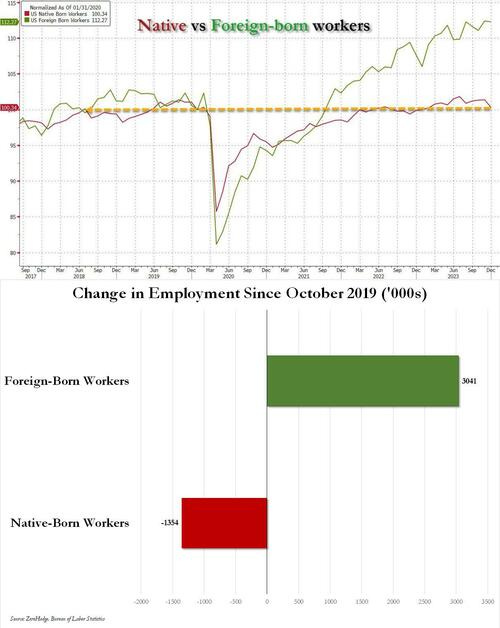

Oh, and before we forget, a reminder that all US jobs created since 2019... have gone to foreign born workers.

MORE over the weekend but … THAT is all for now. Off to the day job…