Good morning … This morning, everyone talkin’ about Chris Waller last night at The Economic Club of NY and if yer sick of hearin’ readin’ seein’ pointification about pontification then simply move along, delete, unsubscribe, improve yer spam filter or whatever.

Disclaimer in mind, this mornings edition brought to you largely BY …

… No, NOT Disney … Chris Waller spoke at The Economic Club of New York and while as we all know, all opinions are created equally, and it remains that SOME (#FOMC101 HERE) are MORE EQUAL than other and so … a link and a few quotes …

For release on delivery 6:00 p.m. EDT March 27, 2024

… In trying to judge what the underlying trend is for inflation, I tend to look at annualized core measures over 3 or 6 months. For most of a year, I watched these numbers come down more quickly than 12-month readings, telling me that we were making substantial progress. But, more recently, the 3-month core CPI, which was running at a 3.3 percent rate in December, rose to 4.2 percent in February. Six-month core CPI, which was also 3.3 percent in December, was up to 3.9 percent last month. These shorter-term inflation measures are now telling me that progress has slowed and may have stalled. But we will need more data to know that…

… It is appropriate to point out that a month or two of data does not necessarily indicate a trend, and there are good reasons to think that progress on inflation will be uneven but likely to continue down toward 2 percent. At the same time, monetary policy is data driven, and I do want to take it into account when formulating my economic outlook. While I don’t want to over-react to two months of data, I do think it is appropriate to react to it…

… In my view, it is appropriate to reduce the overall number of rate cuts or push them further into the future in response to the recent data. This reflects the reality of managing an outlook in real time as data comes in. Subsequent data may well alter this outlook again, but we shall see. Based on what we know now, there is no urgency in taking that step.

So where do I see things standing? I see economic output and the labor market showing continued strength, while progress in reducing inflation has slowed. Because of these signs, I see no rush in taking the step of beginning to ease monetary policy. The target range for the federal funds rate has been 5¼ to 5½ percent since last July, and I believe that this restrictive level is helping to reduce imbalances in the economy and continuing to put downward pressure on inflation. All indications are that the economy continues to grow at a healthy pace. While retail sales and some other indicators suggest a softening in demand this quarter from the second half of last year, when growth accelerated, the evidence for a significant slowdown is sparse. Meanwhile, as the labor market continues to add jobs at a rapid pace, some signs point to improvement in the imbalance between supply and demand, but others indicate continued tightness…

… As a result, in the absence of an unexpected and material deterioration in the economy, I am going to need to see at least a couple months of better inflation data before I have enough confidence that beginning to cut rates will keep the economy on a path to 2 percent inflation. Fortunately, we can wait to see how the data come in before deciding the appropriate time to start lowering the policy rate …

… umm … #FOMC101 HEREfor those who are — like me — trying to follow along at home.

Meanwhile, back at the ranch, it would appear that ‘thin markets’ and mysterious moves in markets helped bonds yesterday. Likely not all that mysterious given week, month, QTR (and Japanese FY)end at the close of biz today (bullish FI impulse noted HERE) …

#Got7s? Maybe NOT so mysterious a bid, then, for bonds yesterday …

ZH: Stellar 7Y Auction Sends Treasury Yields To Session Lows

After two solid, record-sized coupon auctions, moments ago the Treasury concluded the week's scheduled issuance when it sold $43 billion in 7Y notes (which unlike the 2s and 5s previously, was not a record-large auction and has a ways to go to catch up to the $61BN 7Y auctions during the depths of the post-covid crisis).

The auction priced at a high yield of 4.185%, which was notably below last month's4.327% and also stopped through the 4.193% When Issued by 0.8bps, the second consecutive stopping auction following three "tails."

The bid to cover of 2.614 was above last month's 2.577 and was the highest since October, naturally well above the six-auction average of 2.54.

The internals were also impressive, with Indirects awarded 69.7% which was also the highest since last October. And with Directs taking down 17.4%, up from 14.8% last month, Dealers were left holding on to 12.9%, the lowest since - you guessed it - October 23.

… Overall, this was an impressive, "A+" rated auction, as the market reaction agreed by sending Treasury yields to session lows...

... and where every aspect of the sale came "above and beyond" and did not even hint at a possibility of demand drop at a time when US debt is growing by $1 trillion every 100 days. Then again, it's only a matter of time before that does happen so for all those who bought paper today, enjoy it while you can.

… ultimately it boils down to week, month and QUARTER END (bullish FI impulse noted HERE) …

ZH: Trump'n'Pump Continues As Massive Squeeze Lifts Small Caps Into Month-End; Gold Closes At Record High

Stocks up large (and non-stop in Q1) while bond (prices) drifted lower (yields higher)...

Source: Bloomberg

Which may explain why bonds were bid today (given the absence of macro data), with 10Y Yields back at their lowest in two weeks...

… Once again … Maybe then it’s NOT so mysterious a bid, then, for bonds yesterday … Moving on then to NOT SO mysterious market machinations (although, I’ll readily admit to a bit of surprise when waking up this morning at O’Dark Thirty and noticing a bit of a selloff in rates but then … not so much surprise when one considers the CURVE (and it’s bearish flattening) reflexing TO … Wall-E.

Here are couple visuals to consider …

2yy: 4.57% on DAILY chart looks like a level of interest to ME

30yy: triangulating range NOT yet being tested … watching 4.45% - 4.25%

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with the curve flatter after Fed Governor Waller repeated his 'What's the rush?' mantra as he waits for 'at least' a few months of friendly inflation data before supporting a rate cut. Despite today's early close, we do get a decent brace of data before month and quarter-end activity kicks off near mid-day... DXY is higher (+0.25%) while front WTI futures are higher too (+0.95%). Asian stocks saw weakness in Japan (NKY -1.46%) and mixed results elsewhere, EU and UK share markets are mostly higher (SX5E +0.37%) while ES futures are little changed here at 6:50am. Our overnight US rates flows saw post-Waller unwinds of curve steepeners as a main theme this morning. During London's AM session we also saw fast$ selling in the belly with some fast$ names adding back steepeners after 2s30s had flattened as much as -6bp earlier this morning. Overnight Treasury volume was decent at ~125% of average overall.

… Our first two attachments look at Treasury 30yrs and German 5yrs to show how each benchmark remains in a bear channel in place since late last year. Bonds still show local support near 4.47% within that bear channel just as German 5's have recently found decent support near 2.47% within theirs …

… Well, our next attachment shows this morning's gap flatter in the Treasury 2s10s curve, taking out a modest steepening trend (drawn in) in place for the past few weeks. We look at this morning's breakdown and think back to our Conference Board (CB) sentiment (expectations - present situation) and 2s10s curve overlay update earlier this week and how the most recent CB readings were notably flattener-friendly (strong current conditions, weaker expectations). So maybe Waller spurred a bit of a catch-up flattening in 2s10s overnight?

… and for some MORE of the news you might be able to use…

The Morning Hark - 28 Mar 2024: Today’s focus...JPY still on tenterhooks. Waller cautions on inflation and rates. SBF’s Big Day Out.

NEWSQUAWK: Stateside futures softer, Dollar bid post-Waller though Crude/XAU remains resilient; US IJC due … Bonds are lower in a continuation of post-Waller price action

… There has also been a trend through earnings seasons of the market performing best one to two weeks ahead of earnings, rather than during reporting season itself (Fig. 1). With US equities trading just below all-time highs and volatility at lows, we suggest considering delta replacement strategies and owning short dated, low premium upside calls. Either SPX 11 April to play a pre-earnings rally, or SPX Jun24 to capture earnings including NVDA.

… As trading floors resemble ghost towns tomorrow, we'll see the US core PCE print. DB expects +0.27% vs. 0.42% last month. In Powell's press conference, he remarked that the month-over-month print for core PCE could be "well below 30bps" at the end of the month. Taking him at his word does offer downside risk to our economists' forecast. They believe upward revisions to the January healthcare services prices could square these two numbers. We'll also see French and Italian inflation tomorrow so a busy day for a holiday!

The latest guess at UK GDP in the fourth quarter left headline numbers unchanged, while the details shifted. Strike action undermined fourth quarter activity. The data will be revised for years to come, and history suggests it will be revised stronger. Things like productivity gains from flexible working and additional income streams from side hustles are harder to capture in early GDP guesses.

There will be a further guess at US GDP in the fourth quarter. The expectation is for little change. Of course, revising GDP matters little to equities or politics. Earnings growth reflects actual activity—over time, the (relatively minor) part of GDP measuring listed corporate activity should converge with earnings. Politically, spin matters more than substance—what voters feel about the economy matters more than what is actually happening.

German retail sales were weaker than expected in terms of the monthly change, but of course the previous data was revised stronger (as German data nearly always is), helping to boost the yearly growth figure.

Assorted inflation figures are due tomorrow—consumer prices from France and Italy, and the US personal consumer expenditure deflator. Most inflation figures are now within an acceptable range (for a 2% target, anything between 1% and 3% is on target, practically speaking).

So said Federal Reserve Governor Christopher Waller this evening at the Economic Club of New York in a speech titled “There’s Still No Rush.” He noted that the latest inflation figures were "disappointing" and that the economy and labor market remain strong. So, in his opinion, "it is appropriate to reduce the overall number of rate cuts or push them further into the future in response to the recent data." The Summary of Economic Projections released last week by the FOMC showed that nine of the 19 participants projected two cuts or fewer this year. Nevertheless, Fed Chair Jerome Powell sounded more dovish in his presser last week and dismissed the inflation news as "bumps."

… Is there anything to worry about? We continue to monitor the price of a barrel of Brent crude oil (chart). The price is up 16% since it recently bottomed on December 12 last year. We think that reflects a rising geopolitical risk premium. Alternatively, it may signal that the global economy is picking up, though we doubt that. Either way, overweighting the S&P 500 Energy sector makes sense to us.

For now, we have nothing to fear, but nothing to fear. The Investor Intelligence Bull/Bear Ratio has been hovering around 4.00 for the past three weeks. (chart).

During March, only 25.5% of respondents in the Consumer Confidence Index survey are expecting lower stock prices over the next 12 months (chart). The bears are the contrarians.

… And from Global Wall Street inbox TO the WWW,

Apollo: HY Default Rates and Financial Conditions

Higher costs of capital have pushed up default rates in high yield corporate credit since the Fed started raising rates in March 2022.

But since the Fed turned dovish five months ago, credit spreads have tightened and stock prices have rallied, which has reopened capital markets with more M&A activity and IPO activity.

As a result, the high yield default rate is now beginning to flatten out, see chart below.

In short, the negative effect of Fed hikes is being offset by the Fed pivot and the associated easing in financial conditions.

Bloomberg: Why Stock Market Bears Have Thrown in the Towel (Authers’ OpED)

Belief in a hard landing in the US is over. Doubters may now predict a soft one, but markets are positioned for no landing at all.

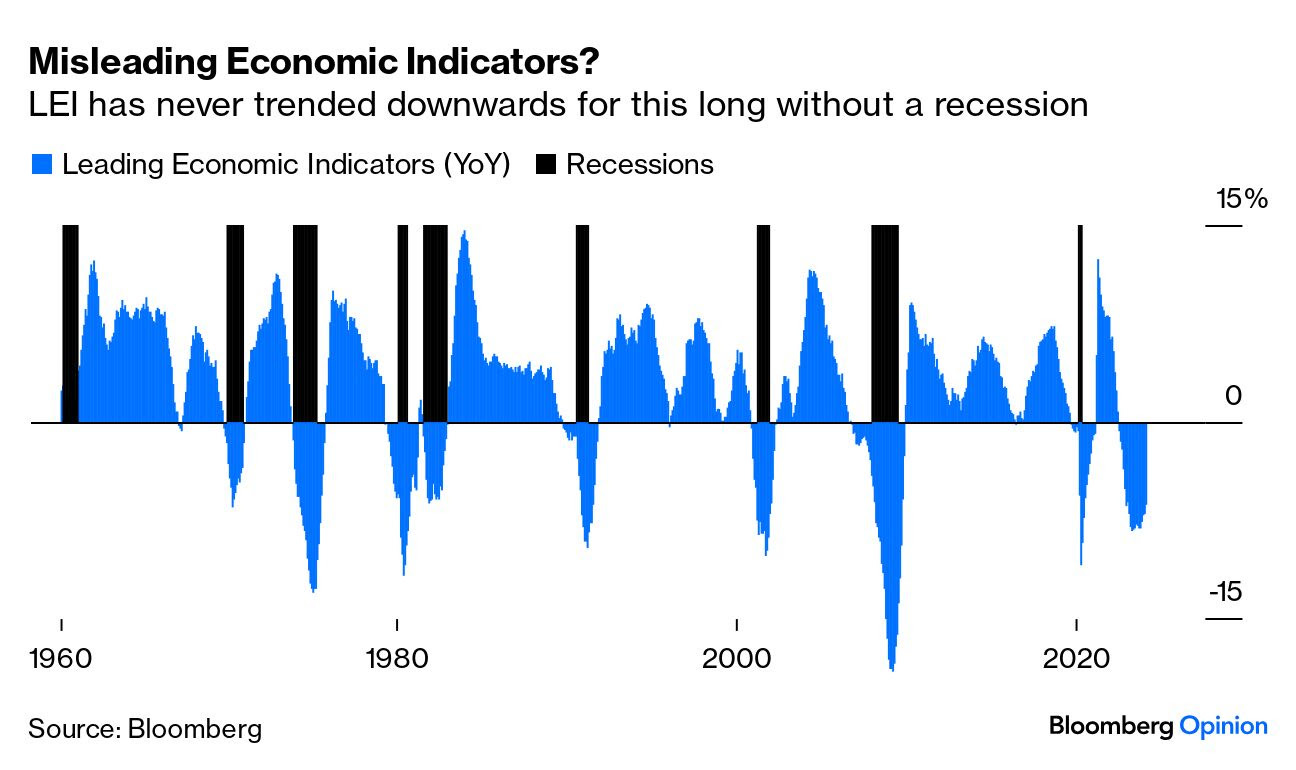

… To be clear, if we really are out of the economic woods, and the US can get through this cycle without a recession — that’s amazing. There is a reason why money managers, economists and bond dealers were convinced a slowdown was coming. One of the clearest ways to demonstrate this is with the Conference Board’s leading economic indicators. Generally, when the LEI go negative year-on-year, and stay that way for any length of time, there will be a recession. Like the yield curve, this was a trusty recession indicator and suggested that one was inevitable:

So the newfound confidence looks a tad overdone. More evidence for this comes in a fascinating paper from the hedge fund group DE Shaw, which compares estimates for growth and inflation reported by economists for the New York Fed’s regular survey known as the SMP (Survey of Market Participants). The latest growth projections are shown in the orange bars; the total spread of outcomes over the postwar period is in blue. Experience suggests outliers are more likely than economists now think:

Over the entire period, there has been a spread of 6.4 percentage points in outcomes. This has reduced to 3.2 percentage points during the “extreme moderation” since the Global Financial Crisis. The latest projections are narrower still, and suggest much less possibility for an upside surprise than history might prepare us:

DE Shaw suggests that “no landing” — a much stronger growth than now assumed — is more likely than economists think:

In our view, it strains credulity that the range of plausible outcomes for the coming year is substantially narrower than the distribution of realized outcomes during the Extreme Moderation, arguably the most stable period known to US economic history. This is especially true given the tendency for macroeconomic volatility to “cluster” over time.

As it is, the asset allocators have enough conviction to bet that equities will beat bonds over the next 12 months. That’s a turnaround after five consecutive quarters when bonds were (incorrectly) expected to outperform. Rate cuts to combat a slowdown would generally ensure a good performance for bonds while equities suffered; so this would be consistent with a belief in “higher for longer” thanks to economic strength:

Against that, the asset allocators also now think that high-yield, riskier credit should beat investment-grade over the next 12 months…

… THAT is all for now. Something over the weekend but for now … Off to the day job…

{kind=link}

Fascinating edition.

Waller and Powell's "good cop/bad cop"

routine is working like a charm.

Goldilocks has arrived, with one

Big Caveat....the Fed MUST finish the

job on Inflation.

Because higher Inflation and higher

Interest Rates will spoil the Party.

Very interesting piece by D E Shaw.

Thank you for your work.