while WE slept: USTs a 'hair' higher, flatter on avg volumes; "US 10y yields trading slightly too low"; a longer-term technical framework from a friend #StewTaylor

Good morning … being a bond guy (once or twice removed now), I’ll start my day with a look at yesterday’s 3yr auction as it may / may not offer a proxy of views of value on the front-end of the yield curve as it relates TO CPI up in a short while …

ZH: Stellar 3Y Auction Sees Biggest Stop Through Since August On Surge In Foreign Demand

… The internals were more solid, with Indirects awarded 70.0% of the auction allocation (up from 66.0% last month and well above the recent average of 60.3%, and with Directs taking down 15.6%, the lowest since May 2023, Dealers were left holding just 14.40%, which was the lowest since August 2023…

… Ok GREAT so there was demand and folks are thinking more about a benign CPI and friendly Fed, right? Well … what was weird was that when you think about such a good auction ahead of an important CPI print and yet, on the day, the front end was … SOLD? Yep …

ZH: Crypto Crack-Up Continues As Stocks & Bonds Sink Ahead Of CPI

… Treasuries were sold today with the short-end underperforming...

10yy WEEKLY: not much of a view from momentum (or from chart, generally speaking)

… for somewhat more and a longer term view, see Stew Taylors visuals below … Not just ‘cuz they are somewhat more bearish leaning but as a CMT, his technical views are worth more of your time than my chicken scratch above.

Also that I used to work with the fella on the evil sellside before he ended his career as a money manager / PM on the buyside … Am happy to say one of the kindest humans I know. And again, he’s ALWAYS been quite a good technician and one that ran in the right circles (Camp Kotok and Ms DiMartino Boothe, etc …) so before you get there … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are maybe a hair higher with the curve a touch flatter as investors (Equity guys especially) hold breath for this morning's US CPI release. DXY is little changed while front WTI futures are modestly higher (+0.55%). Asian stocks were mixed but China's shares had another good day, EU and UK shares markets are all higher (FTSE 100 especially at +1%) while ES futures are showing +0.25% here at 6:50am. Our overnight US rates flows saw better real$ selling in the front-end amid a sideways tape during Asian hours. After the London crossover, it was more sideways action amid position squaring and real$ buying in the front-end despite the general flattening bias in curves this morning. Overnight Treasury volume was ~ average overall with relatively elevated turnover seen in 2's and 3's (170% each), matching our activity…

… Treasury 10yr yields so far respecting resistance near 4.05% derived by September's low there. Daily momentum is beginning to look a touch 'overbought' as the 4.05% area is probed and respected. Not much stands out here with 3.80% and ~4.33% still your assumed major resistance and support zones, respectively.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities mostly firmer, JPY lags post-Ueda and Gilts bid after the UK's jobs report; US CPI due … Bonds are modestly firmer, taking the lead from Gilt outperformance following the region's jobs data

… Duration rally at risk of unwind: Tuesday’s US CPI report and Thursday’s retail sales are the key events of the week. Both we and market consensus expect evidence of firm inflation pressures, while retail sales are likely to benefit from improved weather patterns.

Assessing the risks through our BERT framework, we see these as skewed to the upside, potentially triggering a change of market regime – from a ‘Buying assets’ regime to an ‘Expansion’ regime. This would mainly be reflected in a rise in bond yields…

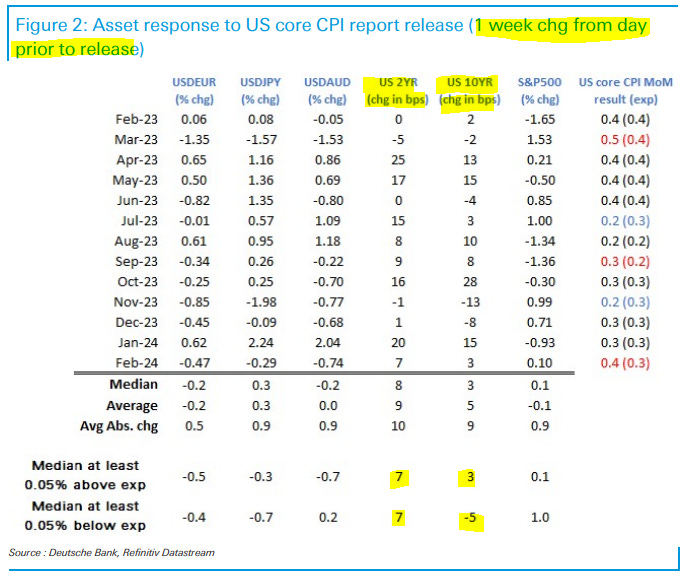

… Adding short duration where it appears overbought: US 10y yield appears 1.3 z-scores too low according to MarFA™ trading, but this is only 7bp. Australia 10y has a larger mispricing, appearing 17bp below its MarFA™ Macro fair value of 4.12%.

DB: Trading US CPI (even WITH this ‘analysis’ if you gave me the data am not sure i’d be on the right side of the trade…)

On three of the last four CPI release days, we have had double-digit basis-point close-to-close changes in the US 2y yield, and yet core CPI has not missed by more than 0.1% on any of these days, all of which highlights the abiding power of CPI to move markets. This should be no different this time around. More than 80% of Bloomberg surveyed forecasts are at 0.3%, which in part explains how a 0.1% miss on either side of the median has the potential to create outsized reactions. Not that a 0.3% core CPI number is that impressive. A 0.3% m/m February number would represent a 3.8% annualized core inflation rate over the last four months, hardly a calling card for an early or quick Fed rate-cutting cycle.

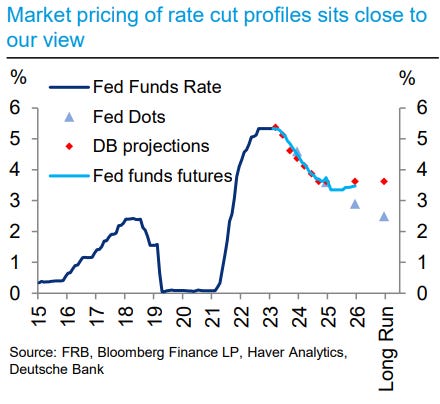

Summary: Fed Chair Powell reiterated that rate cuts at “some point this year”, and not “far from” achieving the confidence to cut DB View: The economy will achieve soft landing. First cut by 25 bps in June, a total cuts of 100bps in 2024 occurring in Jun/Jul/Sept/Dec

We expect a 0.32% increase in February core CPI (vs. 0.3% consensus), corresponding to a year-over-year rate of 3.71% (vs. 3.7% consensus). We expect a 0.44% increase in February headline CPI (vs. 0.4% consensus), which corresponds to a year-over-year rate of 3.15% (vs. 3.1% consensus). Our forecast is consistent with a 0.38% increase in CPI core services excluding rent and owners’ equivalent rent and with a 0.21% increase in core PCE in February. We will update our core PCE forecast after the CPI is released and again after the PPI is released.

We highlight three key component-level trends we expect to see in this month’s report. First, we expect the temporary boost to core CPI from start-of-year price increases to fade, which should result in a slowdown in the medical care services, personal care services, communication, and daycare categories. Second, we expect used car prices to decline 0.4% and new car prices to decline 0.3%, reflecting lower auction prices and higher dealer promotional incentives. Third, we expect shelter inflation to slow on net (we estimate +0.42% for rent and +0.47% for OER), as the gap between rent and OER growth normalizes following last month’s jump.

Going forward, we expect monthly core CPI inflation to come down to 0.20-0.25%. We see further disinflation in the pipeline in 2024 from rebalancing in the auto, housing rental, and labor markets, though we expect small offsets from a delayed acceleration in healthcare and the outperformance of rent growth for single-family units relative to multifamily units. We forecast year-over-year core CPI inflation of 3.0% and core PCE inflation of 2.3% in December 2024.

China’s producer prices and export prices dropped by over 11% in 2023, the largest decline since 2005. Despite the decline in trade between US and China since 2017, goods imports from China still accounted for 11% of total US imports in 2023. The collapse in China’s producer prices has already driven the cost of these imports down by 3%, potentially contributing to disinflation in the US.

We quantify the spillover effects to US inflation in two steps. First, using the input-output tables, we find that direct imports from China account for 1.2% of the value of US core consumer spending. Second, we estimate that lower producer prices in China pass through fully to US consumer prices, with about half of the impact occurring in the first three months and the rest over the next eight months. Combining these steps, we estimate that spillovers from China generated a roughly 0.1pp drag on US year-on-year core inflation in 2023. This rises to about 0.15pp if we instead use China’s 2017 import share on the assumption that the decline in its exports largely reflect rerouting.

Looking ahead, we expect that price spillovers from China will remain modestly deflationary this year, but the impact should gradually fade in the second half of 2024 as China’s producer prices climb out of deflationary territory.

US February consumer price data are due. It is the detail that will tell us about the strength of disinflation forces. The January number had less headline disinflation than anticipated, but this owed much to the fairy tale of owners’ equivalent rent—a price no one pays. The inflation experience of homeowners is a lot less than headline consumer prices, which means their spending power is better.

Start of year price increases should fade, and in the lottery of used car prices disinflation is also likely. Regional inflation figures should continue to show most parts of the US (except Florida and Texas) are in a low inflation environment. This is all consistent with the Federal Reserve following inflation lower with a second quarter rate cut….

UBS: State Sahm Rule: Not yet in the red, but closer (for those keeping granular scorecard at home …)

Weighted by state labor force size, 42% of U.S. states are currently triggering Claudia Sahm's eponymous recession indicator.

The Sahm Rule says "recession" in an elevated share of U.S. states

… And from Global Wall Street inbox TO the WWW,

FirstTRUST Monday Morning Outlook - Is the Job Market Really That Strong?

… Notably, among those who do answer the survey, civilian employment among the native-born population is down around 900,000 from a year ago – the first drop since the onset of COVID – versus an increase of about 1.5 million among the foreign-born.

Only time will tell the true underlying health of the labor market. There is no clear signal we’re in a recession, but the patient isn’t looking well. What is clear, is that economic risks abound, and a soft landing is far from guaranteed.

FRBNY Research Update: Survey of Consumer Expectations (seems like it’s time to cut and ease, right? a friend at BREAN sent some comment from Conrad Dequadros … “Although one-year median inflation expectations held at 3.0%, three-year expectations rose to 2.7% from 2.4% and five-year expectations increased to 2.9% from 2.5%. However, Powell has downplayed this survey (given its short history) and tomorrow's CPI report will obviously be far more important for the Fed's thinking about the inflation outlook. In other areas of the report, year-ahead earnings and household income growth expectations remained steady, but the mean perceived probability of losing one’s job in the next 12 months increased to the highest level since April 2021 and the NY Fed also reports a deterioration in households' assessments of both current and expected household finances…”)

Inflation Expectations Stable at the Short-Term, Rise at Medium and Longer-Term Horizons

Median inflation expectations remained unchanged at 3.0 percent at the one-year horizon, increased to 2.7 percent from 2.4 percent at the three-year ahead horizon, and increased to 2.9 percent from 2.5 percent at the five-year ahead horizon, according to the February Survey of Consumer Expectations. The average perceived likelihood of voluntary and involuntary job separations increased, while the perceived likelihood of finding a job (in the event of a job loss) declined. Perceptions and expectations about credit access turned less optimistic.

The US economy as a whole has been consistently surprising to the upside, but the manufacturing sector has been languishing. Even so, a growing belief in a soft landing and the potential for significant interest rate cuts could bring renewed vibrancy to the sector. Politics, trade and policy missteps are all potential threats to be aware of

Investopedia: Reviewing the Big Four (yesterday mornings read offering today ahead of 10yr auction AND written by a guy I’m proud to say I know personally … we worked together for awhile before he ended his career with several years on the buy side … Great read, Stew!)

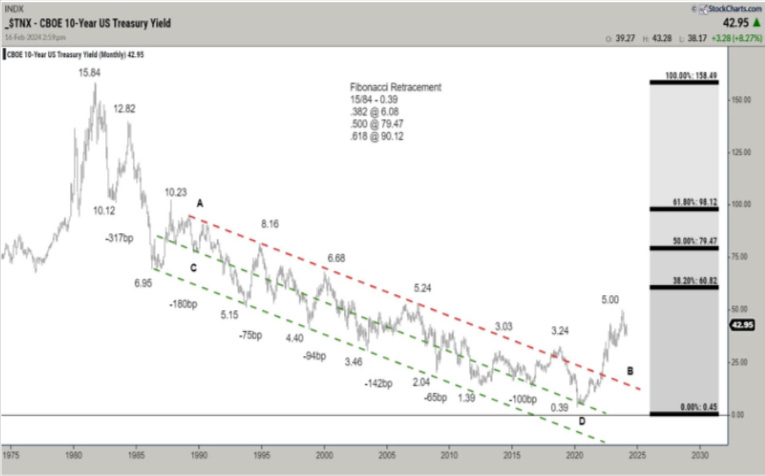

10-Year Treasury Rates: A Monthly/Secular Perspective Overview

I begin each year by reviewing the long-term technical positions and behaviors of what I think of as the “Big Four”—10-Year rates, S&P 500 ($SPX), Commodities, and the US Dollar. I believe that rates, particularly in a credit dependent/leveraged system, generally drive both the economic and market cycles. And, since by profession I am a rates/credit portfolio manager, strategist and trader, I always begin there.

Granted, a macro view doesn’t often inform short term trading, but anything that helps me understand the ebb and flow and interconnectedness of markets is helpful. More importantly, recognizing markets that are aligned for significant macro change can be invaluable, particularly in terms of risk management.

Since most good technical analysis is fractal, the same techniques used to describe the macro ebb and flow can often translate to shorter time frames. For the first two decades of my trading career I kept a manual grid of the big 4 plus a few other markets (gold, oil, 2-year Treasury and so forth) that I updated hourly with price and the change from the prior hour. By doing so, I learned a great deal about market interactions and interrelationships.

Monthly 10-Year Note Yield

<<A reminder that falling bond yields are synonymous with higher bond prices. In other words, a downtrend in yield = a bull market in bonds.>>

Over the last four decades bond yields had consistently and reliably made lower highs and lower lows. The entire bull market was defined by a broad declining channel (A–B, C–D). The A–B downtrend line represented the “stride of demand” or the zone where buyers consistently emerged and the C–D line represented the “overbought line” or the zone where supply or sellers consistently emerged.

From 2012 forward there were growing signs that the long downtrend was aging. Four things stood out.

The repeated failure to push to the oversold line (C–D).

The flattening out of the decline where each push to a new yield low only covered around 100 bps.

The 2018 spike to 3.24% that weakened the primary A-B downtrend.

In March of 2020 bonds pushed to the area around the center of the channel, failed to push beyond the midline much less into the overbought line (C–D). This change of behavior strongly suggested that demand was tiring. Multiple visible changes of behavior strongly suggested that the 40-year downtrend was in danger of terminating.

Now, the clear break and acceleration above the A–B downtrend has moved the long trend from bullish to neutral. While it’s likely that the move above November 2018 pivot @ 3.24% coupled with the prior changes of behavior mark the beginning of a long-term bear market, a higher low (perhaps forming in 2024) is needed to complete/confirm that change.

Note the additional changes in behavior. The 459 bps move from 0.39% to 4.98% represents the single largest bearish move since the inception of the bull market in September 1981, and the MACD oscillator level far exceeded the levels that marked yield highs over the course of the entire bull market.

10-Year Monthly with MACD

After producing the most overbought reading since the 1980s, the oscillator is trying to roll over and displaying a small negative divergence (suggesting lower yields and higher price). While not a definitive roll, it certainly suggests that there is some potential for a meaningful turn.

Monthly 10 Year Note Yield:

The following are several key fundamental points around rates:

The defining macro characteristic of the 40-year bull market has been the continual fall in the inflation rate. If that is changing (I believe that it has), the secular bond trend is likely to also change.

If the trend in inflation is changing, the negative correlation between bonds and equity that drives 60/40 allocation and risk parity investing is likely to flip and become positive. In other words, bonds and equity would, outside of periods of panic or economic distress, rise and fall together destroying the diversification benefit. This has been the historical norm and I expect that the market will gradually move in that direction.

The caveat being: Quantitative easing removed the value proposition from bonds, when equities began to decline in 2022 bonds couldn’t provide a safe haven. They were already far too expensive, particularly in the context of a Federal Reserve aggressively tightening monetary policy. That is no longer the case. Bonds, while still expensive, can again provide a tactical hedge should risk assets or the economy weaken dramatically.

At first glance, this seems at odds with the change in correlation discussed above, but it is a difference between the secular tide versus the intermediate wave.

Most substantive bond rallies are the result of a crisis that creates a flight-to-quality. In an economy that is overly financialized and levered, rising rates often break the weakest link in the economic chain, creating a new crisis and a subsequent flight to quality rally. While so far, there is little evidence of a systemic crisis, the lagged effect of the rapid increase in rates in an overly financialized system must be top of mind.

While there is still more work to be done to confirm the trend change, I believe the bond trend is finally changing as the world moves from the deflationary backdrop of the last several decades to an inflationary backdrop. I will be a much better seller of rallies and bearish technical setups in the weekly/intermediate perspective.

Good Trading: Stewart Taylor, CMT Chartered Market Technician

ZH: NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

AND before hitting SEND a note — there will be NO update tomorrow and regular programming and spammation shall resume on Thursday … THAT is all for now. Off to the day job…

{kind=link}

Excellent AND Educational!