Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP, happy yield lows-A-versary.

On this day in 2020 the 10yr traded at approx 31bps and long bond traded @ approx 70bps.

In that context, perhaps this coming weeks supply of 3s, 10s and bonds will be viewed as having SOME intrinsic portfolio value despite whatever it is you think you think AFTER yersterday’s NFP and ahead of Tuesday’s CPI and ensuing rate CUT (which does not automatically mean EASING) cycle.

Now I realize how tempting it is to begin by dealing with NFP in the week just passed.

The fact that there was, as normal, something for everyone, gives some confidence in beginng with some visuals ahead of this coming weeks reFUNding supply …

3yy WEEKLY: herein lies the rub — the shorter maturity up for sale Monday which is most closely related TO Fed policy showing not much … triangulating between 4.50 and 4.00 (and we closed right in the middle of that range …) and so I’ll let YOU flip the coin

10yy DAILY: momentum (stochastics) appear overBOUGHT and with 10yy auction coming on heels of CPI there may be a concession in wake of the data (which may very well scare folks off) and some levels to keep in mind … 200dMA (4.195) and if things get outta control (?) a TLINE (4.33)

30yy DAILY: as week came to a close, long bonds look vulnerable to me … support up nearer 200dMA (4.33) and then TLINE (4.42)

30yy WEEKLY: triangulating with NO momentum signal whatsoever only good thing one MIGHT say is a breakout may very well be close at hand … next question is fade or go with …

For somewhat more on what do DO and make of all this I’d refer you to a couple things (just below). DB note on auction concessions and BMOs idea to BUY 10s IF …

SOMETHING in market pricing mechanism FOR EVERYONE as usual, see whatever you want to see. Much the same is the case when it comes to yesterdays NFP.

BEWARE, Global Wall will sell whatever is in their desks best interest.

GOOD: BEAT

LESS good: REVISIONS downward, hourly earnings

Politically charged questions on IMMIGRATION angle?? Surely there must be something to this all and a clear path forward to reading the data? For the best read on this kindly see Morgan Stanley thoughts HERE (noted below)…

Sure that may have been the case but truth be known, a view predominantly based on ones position (trading and / or investment stance … tell that to NYCBs HTM portfolio managers, amIright) and NO matter what I ‘think I think’, a friend sent me ‘redhead’ at 852a (about 10min old after the print)

(BN) *FED SWAPS FULLY PRICE IN QUARTER-POINT RATE CUT IN JUNE 2024-03-08 13:42:49.132 GMT

OH… ok ok SO it’s been resolved and we all agree cuts (which again are not, at least initially, an easing of conditions — which are easing in / of themselves ?) is coming.

Heading TO the intertubes then for a couple / few LINKS for some of the (snarky)details

Academy Securities (Tchir via ZH): A Disturbingly Weak Report... BondDad: February jobs report: the Household Survey is downright recessionary, while the Establishment Survey is decidedly mixed CalculatedRISK: February Employment Report: 275 thousand Jobs, 3.9% Unemployment Rate

ZH: February Jobs Soar By 275K, Smashing Estimates, But January Revised Sharply Lower And Unemployment Rate Jumps To 2 Year High ZH: Inside The Most Ridiculous Jobs Report In Recent History: Record 1.2 Million Immigrant Jobs Added In One Month

Clear as mudd … what else is new?

Ok, I’ll move on AND right TO the reason many / most are here … some UPDATED WEEKLY NARRATIVES … some of THE VIEWS you might be able to use — and on this day of the month, you’ll find the cursory NFP recaps and victory laps and along with all that, THIS WEEKEND, a couple / few OTHER things which stood out to ME …

BAML rates weekly, “Double WAMmy” (specifically on technicals ahead to consider as we face supply this week - 10s just AFTER CPI - almost sounds too easy if you ask me but…)

… US Yields: Higher in Q1, then peak, then lower on year

BMOrates weekly, “There yet? Not Far” (booked 2s30s flattening profits now looking to buy 10s, “…at the auction clearing level on Tuesday but only in the event of a benign core-CPI read…”)

DB FI weekly(for the following section again, a must read IMO ahead of 3s, 10s and bonds although it reads to ME like just buy IF a good auction … refer then back TO BMO above … everyone drinkin’ same Kool AID?)

…Treasury auction performance and yield movements

With continued increases in Treasury issuance and notable streaks of weak auctions in 2023, we examine 3yr, 10yr, and 30yr auctions (the first set of auctions each month) from last year and investigate yield movements around these liquidity events.

We find that on days with strong auction performance, yields for the auctioned tenor tend to fall over the remainder of the trading day. However, the connection between days with poor auction performance and a subsequent increase in yields is weaker.

Overall, the strongest finding from our analysis suggests going long the auctioned maturity for the rest of the trading day following a strong auction. Additionally, although notable auction concessions were unreliable last year when used as a sole predictor of auction performance, they are still worth paying attention to for the overall forecasting process.

MS: Friday Finish – US Economics: Immigration Headcount (an excellent NOT ZH recap of the immigration impact on data)

Immigration has been substantial, affecting GDP, labor markets, inflation, and national and local politics. But many of our economic measures do not capture its effects. We run through the data that will, that might, and that won't show its impact.

Trahan: Yes, It's A Real Asset Bubble (a more bullish bond read IMO … a few slides in THE PDF but as example … )

…The Yield Curve … A Difficult Indicator To Dismiss!

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Nonfarm payrolls increased 275,000 in February, beating the consensus expected 200,000. Payroll gains for December and January were revised down by a total of 167,000, bringing the net gain, including revisions, to 108,000.

Private sector payrolls rose 223,000 in February but were revised down by 204,000 in prior months. The largest increases in February were health care & social assistance (+91,000) and leisure & hospitality (+58,000). Government rose 52,000 while manufacturing declined 4,000.

The unemployment rate rose to 3.9% in February from 3.7% in January.

Average hourly earnings – cash earnings, excluding irregular bonuses/commissions and fringe benefits – rose 0.1% in February and are up 4.3% versus a year ago. Aggregate hours increased 0.4% in February and are up 1.0% from a year ago.

Implications: … However, there is good news on the labor market, as well. Total hours worked in the private sector increased 0.4% in February, reversing the decline in January. Hours are up a moderate 1.0% from a year ago. Meanwhile, average hourly earnings rose only 0.1% after a 0.5% surge in January. Average hourly earnings are now up 4.3% versus a year ago. The Federal Reserve will like that a 4.3% gain is slower than the 4.7% gain in the year ending in February 2023 and workers will like that a 4.3% gain is beating consumer prices, which are up 3.1% from a year ago (assuming a 0.4% increase in prices in February). Our view remains that companies have gotten out over their skis in terms of hiring, a recipe for layoffs later in 2024. Total payrolls are up 1.8% in the past year, a pace that would be normal in the middle of an economic expansion when the unemployment rate (and available workers) is much higher than it is today. A weaker job market is heading our way.

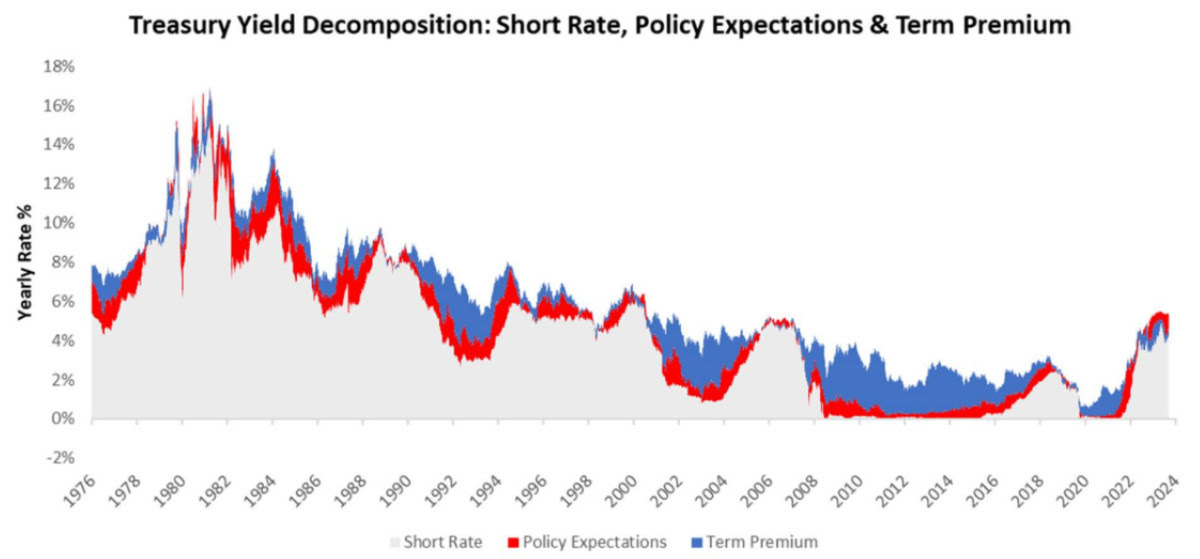

… Changes in the yield of a Treasury security inversely drive the total return on the security. These yields have three components: the realized policy rate, the expected policy rate, and a term premium. We deal with each of these components individually.

… In summary, term premia are a priced function of long-term NGDP, underwritten by demand from economic entities. Outside of periods of monetary policy shifts, term premia are often the dominant driver of treasury excess returns, but rarely during. Until next time.

at RyanDetrick (in case you missed anything from DB past couple / few days)

A historic 19-week move, bears turning into mega bulls, and now a weekly doji on the S&P 500. Dojis can be signs of indecision and many times can mark turning points. Not end of the world stuff, but be aware being bullish is getting quite crowded.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

ZH article is very interesting...a lot of truth, there....

Has the BLS any credibility left ????