Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First up … NYCB downgraded to JUNK …

Bloomberg(via Yahoo): NYCB Downgraded to Junk by Fitch, as Moody’s Goes Even Deeper

… shocked? No, hardly. MORE shocked by what I heard markets reacted to yesterday — namely THIS Wall-E speech …

Operation TWIST?

Lets twist again like we did last crisis?

Is this what we’re told to take from Wall-E speechand the ensuing price action? Apparently yes — more in a moment but first a look at front-end price action …

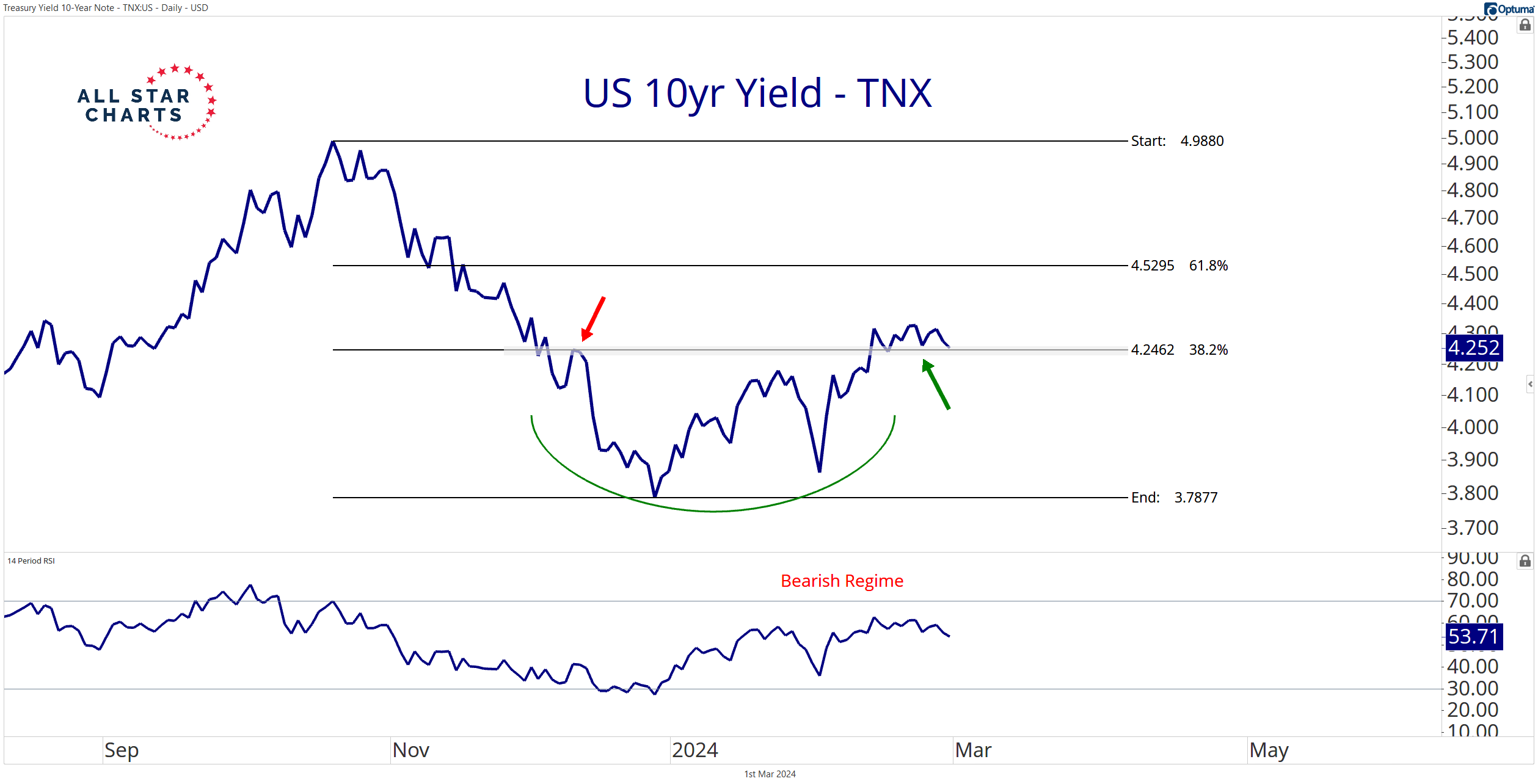

2yy DAILY: bullish momo nearing but NOT YET extreme levels warranting caution

… as Wall-E speechinspired some buying … looking at big picture RANGE (5.25 - 3.55) noting 50% retrace would be down nearer to 4.40% … perhaps before THEN we’ll have more data and clarity as to whether or not Fed will CUT and by how much…OR if they are gonna … nevermind, NOT gonna say HIKE … price action not YET indicating time to worry …

Front-end aside, here’s a longer-term MONTHLY chart that might not quite register any of the shorter-term price action based ON Wall-E speechand any nuanced interpretations …

30yy MONTHLY: momentum middling, ‘support’ (4.42) holding … for now …

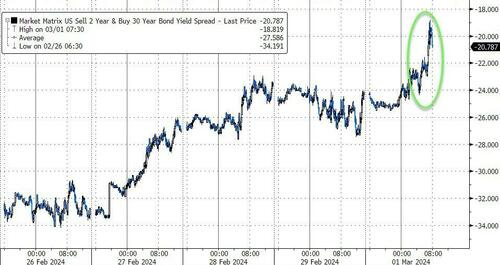

… and price action lacking a signal or go-with would make ME then have to lean on techAmentals where a rate CUT might lead to HIGHER rates (steeper curve … dare I say a BEAR steepener which likely hurts MORE who are currently positioned for the bullish steepener on economic armageddon and Fed sticksave…and have been ‘sellin’ the bull steepener now for couple years …)

Not seeing much other than continued CAUTION if, say bearish (higher yield) price action (2s, 30s) were ever allowed to pick UP and enter the conversation again and essentially log vote of NO confidence in Fed (and / or fiscal position) as some consider another Operation Twist ahead of presidential election.

"First, I would like to see the Fed's agency MBS holdings go to zero. Agency MBS holdings have been slow to run off the portfolio, at a recent monthly average of about $15 billion, because the underlying mortgages have very low interest rates and prepayments are quite small. I believe it is important to see a continued reduction in these holdings.

Second, I would like to see a shift in Treasury holdings toward a larger share of shorter-dated Treasury securities. Prior to the Global Financial Crisis, we held approximately one-third of our portfolio in Treasury bills. Today, bills are less than 5 percent of our Treasury holdings and less than 3 percent of our total securities holdings. Moving toward more Treasury bills would shift the maturity structure more toward our policy rate - the overnight federal funds rate - and allow our income and expenses to rise and fall together as the FOMC increases and cuts the target range. This approach could also assist a future asset purchase program because we could let the short-term securities roll off the portfolio and not increase the balance sheet. This is an issue the FOMC will need to decide in the next couple of years."

Translation: Waller is hinting at an 'Operation Reverse-Twist' which will lower short-term yields and steepen the yield curve.

While much chatter has been about the tapering of QT, they will of course not call 'Operation Reverse Twist' by its proper name - QE - because that would reignite animal spirits further and put The Fed in the awkward position of buying short-term bonds at the same as it is hiking rates.

...bull-steepening the yield curve...

… um … Meet the new year. Same as the old year. 2024. The year of the bull steepening.

Thanks, Wall-E …

… Who are we gonna believe, now?

On the one — somewhat OFFICIAL hand — we’ve got Wall-E & Co.

On the other hand, we’ve got the likes of Slok (The Fed Will Not Cut Rates in 2024), noted YESTERDAY …

Jim Bianco who was recently on MacroVOICES … HIGHLY RECOMMEND you pause and LISTEN to his arguments putting some further context (transcript HERE) TO what Slok noted Friday.

Clearly, the bond market voted Team Wall-E … Friday.

Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES… some of THE VIEWS you might be able to use.

THIS WEEKEND, a few things which stood out to ME …

BMO weekly, “Wagering on Wages” (best in show gets stopped out once and awhile…)

… We were stopped out of our short 10s position as the benchmark rallied through 4.18% in the wake of Friday's disappointing ISM Manufacturing data. With 10-year yields back within close proximity of the 4.196% level that served as meaningful support on several occasions before the release of January’s CPI – the lower departure point suggests there is room for a backup in rates from here in light of the bearish risks that remain on the immediate horizon. However, for a new trade this week, we re-entered a 2s/30s flattener position at -18 bp to fade the substantial resteepening of the curve that is currently in-line with the closing level on the February 13th CPI-day…

JPM FI Weekly — 5yr duration longs and 5s30s steepeners …

… Rates too high vs. our economists' base case for the Fed path Our economists forecast a first cut in June and a total of 8 cuts through June 2025. These inputs would put the 2-year yield at 4.49%, the 5-year yield at 3.85%, and the 10-year yield at 3.87%. Should the market price our economists' forecast, yields – particularly 5-year and 10-year yields – would be meaningfully lower than they currently are

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW …

US Treasuries are taking a back seat to risk assets.

Bond market volatility is declining. Credit spreads are tightening. And Emerging Market high-yield bonds ($EMHY) are breaking out.

Meanwhile, stocks are posting new all-time highs.

So, how high will interest rates climb over the near term?

My gut tells me not far — at least not in the coming weeks or months…

Check out the US benchmark rate finding resistance at approximately 4.33:

Last month’s high marks a logical ceiling for the US benchmark rate.

Those former highs coincide with a key retracement level based on the run-up into the October 2023 peak. Plus, the 10-year yield paused at the same level for almost a month during last year’s rally. That’s not a coincidence.

If the US 10-year breaks above 4.33, volatility will hit risk assets, and energy stocks will likely assume a leadership role.

But a continued rise in US yields seems unlikely now that investors have unwound their aggressive 2024 rate cut projections.

Yet yields aren’t rolling over…

Here’s the US 10-year holding above a retracement level from the 2023 Q4 decline at approximately 4.25:

The US 10-year yield will likely cling to this psychological level for the rest of Q1.

Speculative growth names are ripping. Japanese stocks are hitting new all-time highs. And the commodity bull run is spreading to cocoa and cotton futures. (It doesn’t sound like rate-cut fodder to me.)

Yields will churn sideways as long as both forces remain relevant.

What am I missing?

Do rates catch higher from here?

Or will the Fed start cutting in May?

Apollo: Weaker Transmission of Monetary Policy in the US Through Firms

The US economy is dominated by larger companies, and larger companies generally have fixed rate debt. This is likely a key reason why Fed hikes are having a more limited impact on the economy.

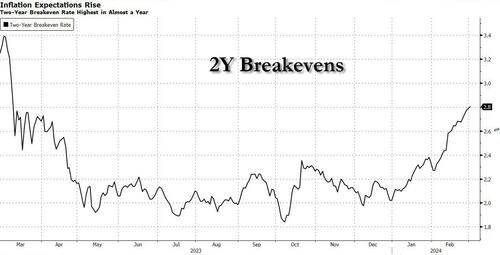

Bloomberg(via ZH): Eye-Catching Jump In Inflation Expectations Threatens Bonds

The US two-year breakeven rate is showing an eye-popping increase and will put upward pressure on yields.

Inflation expectations are climbing as the Fed’s fight against rising prices seems to be sputtering. The latest warning for bond investors came from Apollo Management Chief Economist Torsten Slok, who said that a re-accelerating US economy, coupled with a rise in underlying inflation, will prevent the Federal Reserve from cutting interest rates in 2024.

The numbers tell the tale of a Fed battle against inflation that has yet to be won. Core PCE is the highest in almost a year. CPI and PPI both beat expectations.

All of this comes at a time when breakeven rates and yields are moving together more. This signals breakevens are asserting more influence on yields. The chart below shows the 30-day correlation between two-year breakeven rates and two-year yields is rising.

Bloomberg’s Correlation Finder shows that two-year breakeven rates are also moving largely in line with five- and 10-year yields, suggesting rising inflation expectations have the potential to buoy yields across maturities.

My theory is being put to the test today because Treasury yields are falling. Still, it’s worth keeping these risks in mind. The most potent warning from these breakevens came after they rose in 2019, 2020 and 2021. The Bloomberg US Treasury Total Return Index went on to tumble a stunning 12% in 2022, its biggest loss based on Bloomberg data going back to 1974 –- the year President Richard Nixon resigned and I turned 10 years old.

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (short covering in 10s after record short just inside 2mos ago…)

ING: US mixed manufacturing messages clouds the outlook ahead of Powell

High inflation, but softer activity data has been the theme this week and means that Fed Chair Powell is likely to give little away in terms of a timetable for rate cuts at his Congressional appearances next week

ISM surveys suggest the economy is weaker than official GDP growth data indicates

WolfST: Inflation Saga Far from Over: Services Inflation in Euro Area Just as Stubborn as in the US, Makes Very Disconcerting Moves

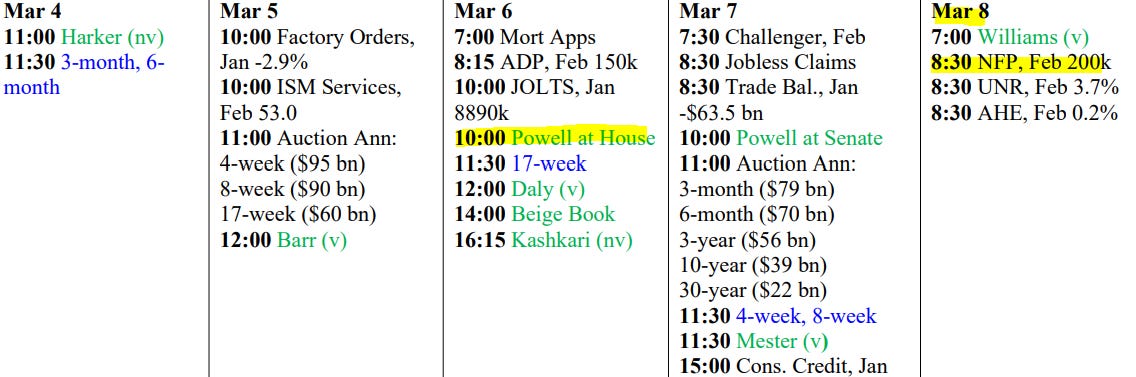

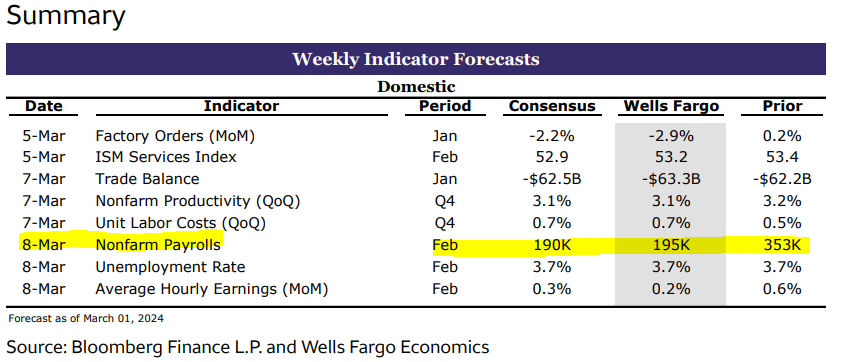

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Here's another Bianco interview you might like:

Jim Bianco: The New Normal - Making Markets, Episode #19

https://youtu.be/ZmzvVwqSd-Q?si=VcjTeYo1JlePNg2E

He talks a little Fixed Income here, about the Flat Yield Curve and the SM vs the BM.

The Macro Voices piece is excellent !!

I do think he's on to what has changed in the US economy and it implications.

Everybody talking about Torsten. Makes me think economist are really like influencers