Good morning … Overnight saw Chinese PMI falling TO 49.1 from 49.2 …

RTRS: China's factory activity shrinks for 5th month, raises pressure for more stimulus

… as expected … Sounds bad BUT, on the other hand, the private Caixin report came in at 50.9 up from 50.8 last time and so, we’ve got THAT going for us … which is nice.

Meanwhile, data here yesterday was IN LINE is the new DOWNSIDE BEAT but any / all ‘super users’ likely already knew what was coming, amIright? I’d love to get some ‘super users’ view on where long bonds are going to go next …

30yy DAILY: 4.50% held and 4.25 is most recent low … as momentum becoming overBOUGHT

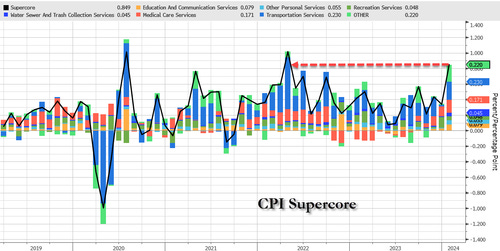

… Has bullishness run its course and what say the more longer-term weekly and now MONTHLY charts? I’ll head to them for guidance over the weekend but for now, on TO some links where this first is on SuperCore for all you ‘super users’

ZH: SuperCore Inflation Soars In January, Services Costs Re-Accelerate As Govt Handouts Spike

GOOD NEWS... One of The Fed's favorite inflation indicators - Core PCE Deflator - dropped to +2.8% YoY in January (as expected) - the lowest since March 2021…

… BAD NEWS... Even more focused, from The Fed's perspective, is Services inflation ex-Shelter, and the PCE-equivalent actually ticked up on a YoY basis to 3.45%, thanks to a large 0.6% MoM jump, considerably bigger than the last few months increases...

… Finally, while the markets are exuberant at the headline disinflation, we do note that it's not all sunshine and unicorns. The vast majority of the reduction in inflation has been 'cyclical'…

Source: Bloomberg

Acyclical Core PCE inflation remains extremely high, although it has fallen from its highs.

Is The (apolitical) Fed really going to cut rates 4 times this year with a background of strong growth (GDP) and still high Acyclical inflation?

… AND then we got Chicago PMI …

ZH: Survey-Based Sentiment Slump Continues As Prices Paid Accelerates in Plunging Chicago PMI

… All told, at months end …

ZH: Leap-Of-Faith: Feb Favored Bitcoin-Bulls, Bond-Bears, AI-Advancers, & Anti-Obesity Advocates

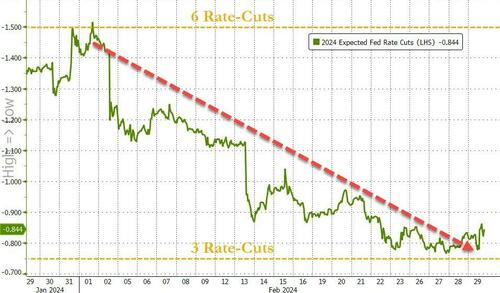

… Endlessly hawkish FedSpeak (confirmed by the FOMC Minutes), and troublingly sticky inflation prints (hard and soft) sent 2024 rate-cut expectations reeling from over 6 cuts (154bps) at the start of the month to less than 4 cuts (84bps) at the end, as better-than-soft-landing data spoiled the "rescue-me" fantasy so many had for The Fed...

… As rate-cut expectations fell and better-than-soft-landing data showed up (and stickier than expected inflation data), so bonds were battered in February with the short-end monkey-hammered over 40bps higher in yield while the long-end rose around 20bps...

Which means the yield curve (2s30s) is bear-flattening significantly...

… AND here is a snapshot OF USTs as of 801a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and outperforming peer markets overseas and an embattled NY bank came under severe new pressure (link above) amid mixed global manufacturing PMIs and inflation readings. DXY is modestly lower (-0.1%) while front WTI are higher (+1.5%). Asian stocks were generally higher (NKY +1.9% to fresh record high), EU and UK share markets are mostly higher (SX5E +0.3%) while ES futures are little changed here at 7am. Our overnight US rates flows saw a quiet Tokyo session that featured mainly 2-way activity in intermediates. Prices were drifting lower into the London crossover before a spike higher on light volumes was seen as the NY bank headlines made the rounds. Overnight Treasury volume was ~110% of average overall with 10yrs (144%) seeing some relatively elevated turnover overnight…

… Our next four attachments contribute to this tactical bull story. Take a look in the lower panels of the pictures to see how the long-oversold momentum studies are flipping bullishly and perhaps indicating that buyers have begun to take control over the sellers here. The four benchmarks chosen are Treasury 2yrs (which have gamely held support at 4.735%),

… and for some MORE of the news you might be able to use…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP US Economics Research: Core PCE inflation accelerates in January

The run of soft PCE price inflation reversed in January, with the core posting a 0.42% m/m increase, implying annualized inflation of 2.5% on a 6m saar basis, after two months of running under 2%. That said, PCE price inflation continues to run well below the CPI measure, which showed January core at 3.6% 6m saar…

… The "supercore" measure (core services ex-housing) of inflation rose 0.60% m/m (3.5% y/y), firming from a string of relatively soft readings in the prior three months. This reflects a broad-based increase in price pressures, including in heavily weighted categories such as health care services, food services and finance and insurance. Smoothing through some of the noise, the 3mma is at 0.34% m/m, about 0.2pp higher than its pre-pandemic average…

… We leave our core PCE forecasts unchanged for 2024 and 2025 …

… We maintain our call for the FOMC to initiate the first rate cut in the June FOMC meeting, of 25bp, followed by two more 25bp cuts in September and December this year.

Personal income contained no major surprises regarding household spending, with PCE holding up despite January's drop in retail sales and revisions implying minimal changes to prior carryover effects in Q1. Pretax income surprised, but had roughly neutral implications for after-tax disposable income.

Equities have been remarkably resilient in the face of both higher rates and choppy disinflation, but markets likely expect to see progress on both fronts over the coming weeks. SPX forward implied volatility signals that jobs, CPI and, above all, the March FOMC meeting are the biggest upcoming macro catalysts for equities.

The services PMI showed a big rebound in February thanks to Lunar New Year spending. Weaker employment and the subdued outlook mean a sustained rebound in services/consumption is unlikely. The continued drop in construction PMI suggests property remains a key risk. The NBS manufacturing PMI remained stuck in contraction.

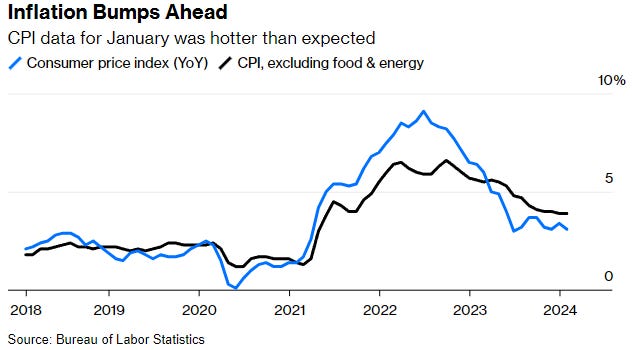

…Month in Review - The high-level macro overview February had several ongoing stories that were relevant for markets. The first was that global data was still robust for the most part, and hopes for a soft landing continued. For instance, the US jobs report for January showed nonfarm payrolls up by +353k, along with positive revisions to the previous two months. Moreover, the ISM manufacturing print hit a 15-month high. But even as growth remained strong, there were further upside surprises on inflation, which raised fears that the path back to target was unlikely to be a smooth one, and raised questions as to whether the economy would face a “no landing”. In particular, the US core CPI print for January came in at a monthly +0.4%, which pushed the 3-month annualised rate for core CPI up to +4.0%.

With inflation above target and growth remaining strong, that led investors to push out the timing of future rate cuts once again. At the Fed, futures moved from pricing 146bps of cuts by the December meeting, to 85bps, a reduction of 61bps over February. In addition, they pushed out the likely timing of the first rate cut to the June meeting. As a result, sovereign bond yields rose further, and US Treasuries (-1.4%) posted their worst monthly performance since September. Similarly in the Euro Area, investors reduced the expected cuts by December from 160bps to 91bps, and Euro sovereign bonds fell -1.2%. Lastly in Japan, expectations grew that the BoJ might end the negative interest rate policy as early as April, and yields on 2yr JGBs were up +9.7bps to 0.17%, marking their highest level since 2011.

…Which assets saw the biggest losses in February? Sovereign Bonds: As investors pushed out the timing of rate cuts, sovereign bonds saw further losses. That included US Treasuries (-1.4%), Euro sovereigns (-1.2%) and gilts (-1.3%)

In this short chartbook we detail five factors supporting Fed rate cuts this year and five factors arguing for greater caution around rate reductions. As a reminder, our baseline view is that the Fed will cut rates 100bps this year, with the first 25bp cut coming in June (see here). We have also detailed economic conditions that could lead to no cuts (see here) as well as reasons to frame the Fed outlook as a two-stage process, in which the Fed begins with a mid-cycle adjustment (see here).

… DB Fed expectations: First cut in June, 100bps of cuts in 2024, nominal neutral rate ~3.5%

Goldilocks: Core PCE Slightly Above Consensus Expectations; Saving Rate Ticks Up to 3.8%; Jobless Claims Rise

BOTTOM LINE: The January core PCE price index rose by 0.42% month over month, slightly above consensus expectations, and the year-over-year rate declined to 2.85%. Core services prices excluding housing increased 0.60%, partly driven by large increases in the volatile financial services and nonprofits categories. Personal spending and income increased by 0.2% and 1.0% respectively in January. The saving rate edged up by 0.1pp to 3.8%. Jobless claims rose by more than expected. We left our Q1 GDP tracking estimate unchanged on net at +2.4% (qoq ar) and our Q1 domestic final sales forecast also unchanged at +2.6% (qoq ar).

… Where does this leave the January OER change and what about February? This means that the January jump in OER is still largely unexplained. One other sentence of the BLS posting might be informative: The new methodology introduced in January a year ago "may introduce monthly variability in the unit-level weights." This sentence, along with the improbable pace of single family detached housing rents needed to make the large January increase persistent, leads us to return to our prior view that the January OER surge was largely random noise. Such noise in the data occurs occasionally — note similarly large pick ups in OER in March 2018, July 2020, and October 2020 that proved to not be persistent. We think this January jump in OER (and particularly the OERtenants' rent wedge) will prove equally non-persistent. We have not altered our OER forecast over the past few days, though we still project a strong 48bp increase in OER in February.

UBS: Despite strong January increase inflation continues to fall

… Despite the strength in the January increase, both headline and core PCE 12-month inflation fell to their lowest levels since very early in 2021, right at the start of the inflation surge. Headline inflation, at 2.4%, is now 92% of the way to the FOMC's 2.0% inflation target from the peak increase of 7.1% in June 2022, and core PCE inflation, at 2.8%, is now 76% of the way to 2.0% from the peak increase of 5.6% in February 2022. Base effects should be a solid downward influence on inflation in coming months. We expect 12-month core PCE inflation will continue to edge down over the first half of the year until reaching a 2.2% pace in June.

Core inflation continues to ebb

UBS (Donovan): More disinflation, and a lot of Fed speak

The US personal consumer expenditure deflator remains in disinflation. Durable goods prices sank ever deeper into deflation. Market-based prices showed disinflation, as did services excluding financial service (financial service prices often follow market valuation). There was an intensely technical clarification about calculating owners’ equivalent rent—price no real person pays or cares about, but which excites economists. The clarification makes it unlikely OER will add more to inflation this year.

Wells Fargo: Surges in Inflation & Personal Income Both Apt to Be Short-Lived

Summary Personal income growth surprised on the upside in January allowing consumers to keep spending; but after adjusting for inflation, real spending fell 0.1%. The Fed's preferred gauge of inflation, the core PCE deflator, notched its biggest monthly gain since January 2023.

The reality is that the US economy is simply not slowing down, and the Fed pivot has provided a strong tailwind to growth since December.

As a result, the Fed will not cut rates this year, and rates are going to stay higher for longer.

How do we come to this conclusion?

1) The economy is not slowing down, it is reaccelerating. Growth expectations for 2024 saw a big jump following the Fed pivot in December and the associated easing in financial conditions. Growth expectations for the US continue to be revised higher, see the first chart below.

2) Underlying measures of trend inflation are moving higher, see the second chart.

3) Supercore inflation, a measure of inflation preferred by Fed Chair Powell, is trending higher, see the third chart.

4) Following the Fed pivot in December, the labor market remains tight, jobless claims are very low, and wage inflation is sticky between 4% and 5%, see the fourth chart.

5) Surveys of small businesses show that more small businesses are planning to raise selling prices, see the fifth chart.

6) Manufacturing surveys show a higher trend in prices paid, another leading indicator of inflation, see the sixth chart.

7) ISM services prices paid is also trending higher, see the seventh chart.

8) Surveys of small businesses show that more small businesses are planning to raise worker compensation, see the eighth chart.

9) Asking rents are rising, and more cities are seeing rising rents, and home prices are rising, see the ninth, tenth, and eleventh charts.

10) Financial conditions continue to ease following the Fed pivot in December with record-high IG issuance, high HY issuance, IPO activity rising, M&A activity rising, and tight credit spreads and the stock market reaching new all-time highs. With financial conditions easing significantly, it is not surprising that we saw strong nonfarm payrolls and inflation in January, and we should expect the strength to continue, see the twelfth chart.

The bottom line is that the Fed will spend most of 2024 fighting inflation. As a result, yield levels in fixed income will stay high…

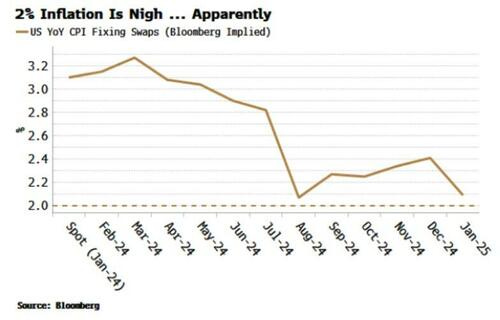

Bloomberg(via ZH): No Asset Class Is Remotely Ready For More Inflation

Stocks, bonds, commodities and other real assets are dramatically unpriced for a resurgence in inflation.

If fortune favors the prepared, then no market is going to have much luck. A re-acceleration in inflation is increasingly on the cards (see here), an eventuality that is materially underpriced across asset classes. That means portfolios are cheap to hedge, as well as leaving markets subject to outsized moves when they do price in inflation’s return.

Inflation complacency can be seen clearly in one chart. CPI fixing swaps foresee a continued steady decline in headline inflation in the US back toward 2% through this year. Not only that, most of the swaps have been falling in recent months as spot inflation has eased. The implied probability of a return of inflation is dwindling to zero.

But it’s not just fixing swaps predicting a return to inflation utopia….

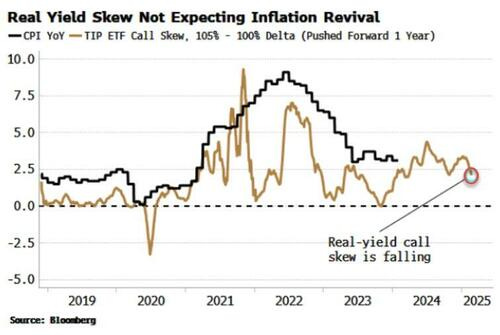

… Real yields too are bereft of any risk premium for inflation. If the Federal Reserve does not immediately react to rising inflation (as happened in 2021, and I suspect will happen this year if and when inflation starts to pick back up), real yields are likely to experience downside volatility, i.e. call skew for TIPS should rise. Again there is no sign of market nerves here.

As the chart above shows, TIPS call skew has tended to lead inflation over the last few years, and thus there is little in the way of rising price growth expected soon. The inflation-bond market may have this one wrong.

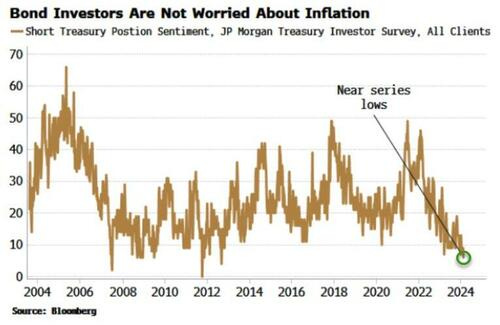

Short-term rates don’t look any better…

… Overall, bond investors just aren’t anticipating more inflation, with the number of investors who say they are short USTs in JPMorgan’s Treasury survey plumbing its series lows.

Stocks are also very much on Team Transitory (and we can make similar arguments for credit).

Bloomberg: The Fed wasn't going to cut rates soon, anyway (Authers’ OpED)

…What Does Any of This Even Mean? Perhaps the single clearest message from looking at the breakdown is that any attempt to measure overall inflation within the economy is going to be fraught with difficulty, and rest on disputable assumptions. That is good to know because both society and the markets are riven by disputes over inflation technicalities. Plenty of people believe the figures are manipulated or even falsified, while the overall numbers can seem to ignore realities for particular individuals on the ground. No two humans will buy the same basket of things each month, so they’ll tend to have slightly different rates of inflation in their living costs…

… And the Markets? This data release was pre-hyped as a big event. The surprisingly strong CPI earlier in the month raised the stakes. That number, in combination with predictions (which turned out to be correct) that monthly PCE inflation would rise a little, helped ensure an unduly aggressive buildup. The eventual numbers, bad but no worse than feared, therefore prompted a sharp fall in yields. By the end of the day, that too had been reversed. The market thinks it’s now got it right that the Fed probably won’t cut more than three times this year, which happens to be exactly what the Fed is saying. Still, someone must have made some money in the course of a turbulent day on the bond market. This is what happened to the 10-year real yield over the course of Leap Day:

Judging by the reaction of stocks, prices already reflect the more conservative outlook on rates from the Fed, and don’t think it matters much.

Bloomberg: A Fed Held Hostage by Data Is Asking for Trouble (El Erian OpED)

High-frequency inputs on economic activity should inform and influence policymaking, not dominate it.

… A straight road is what the Fed was mostly on as the consumer price index plummeted from a high of just over 9% in June 2022 to 3.1% in January. On the “last mile” of this road, however, policymakers face many more curves as demonstrated by recent updates on CPI and producer price inflation, which came in hotter than expected.

The Fed is highly unlikely to face a straight road from here given the current dynamics of inflation, including the time-variant tug of war between some outright goods deflation and high services inflation. There are also complications with defining some important determinants of its terminal fed funds rate, be they questions about the neutral rate, or r-star, or the appropriateness of a 2% inflation target for the US when the global economy, at the moment, is characterized by changing and insufficiently flexible supply…

ING: US inflation is too hot but softening fundamentals point to an eventual cooling

The Fed's favoured measure of inflation come in at 0.4% month-on-month, which is double the 0.2% rate we want to see, but cooling incomes and spending suggest inflation will moderate again in coming months, leaving the door open to a June Federal Reserve rate cut

WolfST: Worst Monthly Spike of “Core Services” PCE Inflation in 22 Years, and Not Just Housing: Powell’s Gonna Have Another Cow

ZH: Biden's Labor Department Sparks Confusion With Email "Explaining" January CPI Spike (while this was ‘OUTTED’ and made rounds couple days ago, thought I’d live here for posterity sake … just another case where we’re ALL created equally but some “SUPER USERS” are MORE equal than others…? WTaF?)

There was a collective gasp of surprise two weeks ago when not only did CPI and core CPI both come in far hotter than expected, but the closely watched sticky Super Core inflation - Core CPI Services Ex-Shelter index - soared 0.7% MoM (the biggest jump since Sept 2022...

... and while we correctly warned that the inflation print would come in red hot (see "CPI Preview: "There's A Genuine Risk" Inflation Will Come In Hotter Than Expected") most on Wall Street did not, and were scrambling to come up with justifications for why they were again collectively wrong, with Goldman being of particular note, as the bank attributed the spike to what it called a "January effect" and then assured its clients that "while some of the OER strength could persist if driven by the rebound in the single-family market, we continue to expect inflation in non-housing services to normalize in February and March now that the start-of-year price increases have been implemented."

Now the reason why Goldman, and so many others, scrambled to goalseek a narrative that sees the Fed cutting rates in March... or May.... or June (as Goldman now does, after previously forecasting both the former months as the start date of the Fed's easing cycle)... or whenever, is because that's the only thing that will validate the very bullish year-end S&P price targets by various banks which have been aggressively raised in recent weeks as the Wall Street lemming crew chased the momentum ignition sparked by a few AI-linked companies. But there is another reason why the Fed needs to cut: if it does not the odds of the market maintaining its upward glidepath into the November election, not to mention the so-called "strength" Bidenomics, are as dead as the dodo.

In other words, the real shock is not that inflation printed high - everyone knows how high prices are and in which direction they are moving - it is that Biden's Department of Labor Statistics admitted to this fact. So two weeks later, the BLS has realized precisely the error that it made, and as Bloomberg reported today, the US Labor Department’s statistical agency "sowed confusion" on Wall Street this week with an email about a key factor behind the jump in January’s CPI index.

A Tuesday email to a group of data “super users”, seen by Bloomberg, suggested a surge in a measure of rental inflation — which left analysts puzzled — was caused by an adjustment to how subcomponents of the index are weighted…

… somewhat MORE from this NOT ‘super users’ — think WEEKLY and perhaps MONTHLY charts — over the weekend and for now … THAT is all for now. Off to the day job…

Will read soon.

Wanted to post this:

https://youtu.be/-uSLgqw6LLc?si=7O3cqK4SRuKLAoXZ

MacroVoices #417 Jim Bianco: FED Cuts, May, June or Bust?

torsten slok trying to steal the limelight from our man at Santander who said no cuts 3 months ago