Good morning … I will try (and am quite likely to fail in efforts) to keep this brief but with almost an entire day outta pocket away from these screens, I have some catching up to do.

JPOW yesterday apparently reiterated what he had reiterated the end of last week …

Markets recovered their poise over the last 24 hours, as investors were relieved after Fed Chair Powell stuck to his recent views on the economic outlook. In his remarks yesterday, he said that recent data didn’t “materially change the overall picture” and that on inflation “it is too soon to say whether the recent readings represent more than just a bump.” In addition, he reiterated that if “the economy evolves broadly as we expect, most FOMC participants see it as likely to be appropriate to begin lowering the policy rate at some point this year.” So that all helped to validate market pricing, which still expects 71bps of rate cuts from the Fed by the December meeting… -DB Early Morning Reid

First thing I’m noticing is that the big bond selloff has paused a bit or slowed down a touch, at least yesterday … In fact, it appears that 5yy triangulation noted HERE — with a link thru to its inspiration — Citi HERE — have stalled and respected TLINE ‘support’.

Safe then to say that JPOWs commentary helped provided needed support despite / because of the days earlier data …

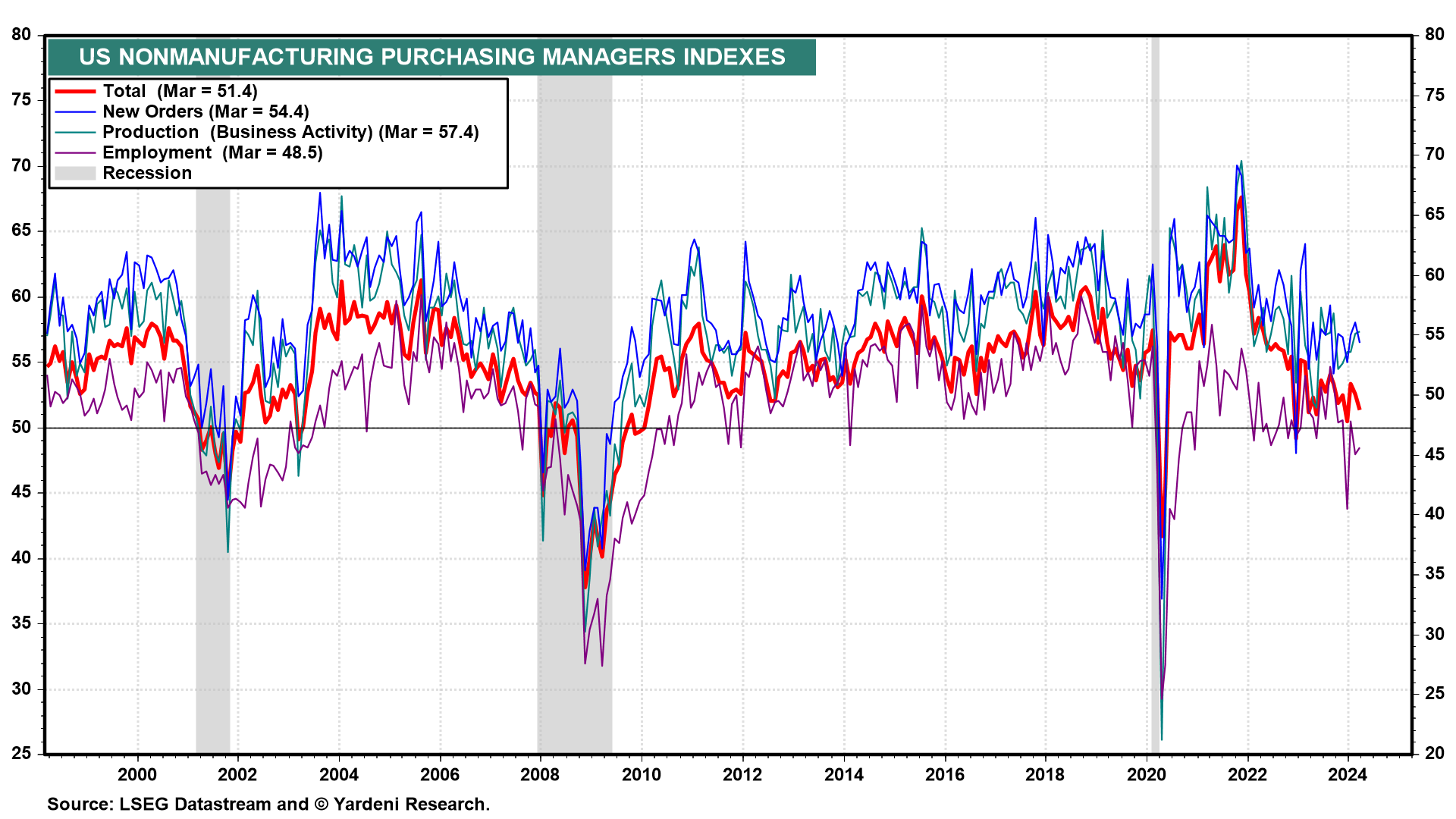

… The 10yr yield was near flat yesterday (-0.2bps) at 4.35%, but that was actually a sharp decline from earlier in the session, when it hit an intraday peak for 2024 of 4.43%, and overnight there’s only been a modest +1.8bps move back up to 4.37%. That turnaround was partly due to Powell’s remarks, but was also because of the ISM services print for March, which unexpectedly fell to 51.4 (vs. 52.8 expected). And encouragingly on inflation, the prices paid component fell to 53.4 (vs. 58.4 expected), its lowest since March 2020. That contrasted with the upside surprise in the ISM manufacturing on Monday, and combined with Powell’s comments, the release helped to push back against some of the more hawkish narratives over the last couple of sessions.

… it had been a very different story earlier in the day. That was particularly the case after the ADP’s report of private payrolls for March came out, which rose to 184k (vs. 150k expected), and February’s number was revised up by +15k. So that was a fresh sign that the labour market was in good shape ahead of tomorrow’s US jobs report, and it was that release which pushed the 10yr yield up to its intraday peak for 2024 so far… -DB Early Morning Reid

… And so … Jay to the Rescue, then it is (for more see John Authers’ latest OpED below) and for now, a bit further out the curve then, it was clearly a bit of a different story …

30yy: TLINE support broken, might need to move goalposts soon; momentum (stochastics, bottom panel) not yet overSOLD extreme (buy signal) … lets check back over weekend with longer-term (ie weekly, monthly, quarterly) charts…

As I continue to sift through my emails from a couple days worth of Global Wall St spamification, one from a friend stood out …

Bloomberg: $1.7 Million Options Play Targets Bigger Bond Selloff by Friday 2024-04-03 13:30:41.94 GMT

By Edward Bolingbroke (Bloomberg) -- Early action in the Treasury options market has included a large amount of Weekly options bought in the 10-year tenor, targeting a yield rise to almost 4.50% ahead expiry on Friday. * Via one screen trade 10,000 Treasury Week 2 109.00 puts bought at 11 ticks, says London trader * Premium paid on the position roughly $1.7 million; total screen volumes on the day in the strike sit at 18.3k with open interest at 28.4k, meaning Wednesday’s buying could be new bearish hedge or covering a short position in the strike * US 10-year yields trade at 4.41%, cheaper by about 6bp vs. Tuesday, near highs of the day in the aftermath of ADP data; risk events ahead for Wednesday include upcoming PMI and ISM data along with comments from Fed Chair Powell later in the session * Some information comes from rates traders familiar with the transactions, who asked not to be identified because they are not authorized to speak publicly

… I don’t have access to the story which likely contains a better-than-avg infographic showing positions and pain points (EBB one of the best in the biz and I’m grateful for my friend who sent this one along from his Terminal, too). I think this all goes to show how the street works … as Gartman always used to talk about … throwing your stones into the wettest paper bag …

Concept is of the path of least resistance. Traders trade and are not looking to be ‘wrong or right in macro conclusion’ they are simply to buy low and sell high, so to speak. whatever happens on Friday is besides the point and traders likely to have booked their gains ahead of the print.

Thats the beauty of leverage and how options work … digging a bit deeper, I did find another story from EBB from 4/2nd, worth mention …

Bloomberg: Bond Traders Load Up on Bearish Wagers as Rate-Cut Odds Dwindle April 2, 2024 at 8:30 PM UTC

JPMorgan survey shows biggest outright short bets since Jan. 1

In futures, bearish positions fueled Monday’s Treasuries slide

Bond traders are piling into bearish bets, fueling a selloff in benchmark Treasury securities, as fresh evidence of robust US growth triggers a recalibration of expectations for Federal Reserve interest-rate policy.

JPMorgan Chase & Co.’s latest client survey showed that outright short positions in US Treasuries rose to the most since the start of the year in the week leading up to April 1. That bearish sentiment spilled over into this week, helping to drive US 10-year yields to as high as 4.4% on Tuesday, a level not seen since November…

… With the market leaning so bearish, some traders are starting to take the other side of the bet. Tuesday’s activity in both Treasury options and those linked to the Secured Overnight Financing rate — which closely tracks the central bank’s key policy rate — included some large bullish wagers. The trades look to target a rally in the so-called belly of the curve — around the five-year maturity area — as well as half a percentage point of Fed rate cuts by the central bank’s September policy meeting…

…Treasury Clients Short JPMorgan client short positions rose 7 percentage points in the week leading up to April 1 to the most since Jan. 1 on an outright basis. With long positions dropping 3 percentage points on the week, the net positioning shifted to the least long since Feb. 20.

… funny thing is, this story written day before the $1.7mil option play and so one might assume these positions a known and factored in to ones decision to play for higher yields in the short-run. Perhaps these factoids were some of the determining factor as the story from 4/2 goes on to detail how hedging for bond selloff has gotten … more expensive …

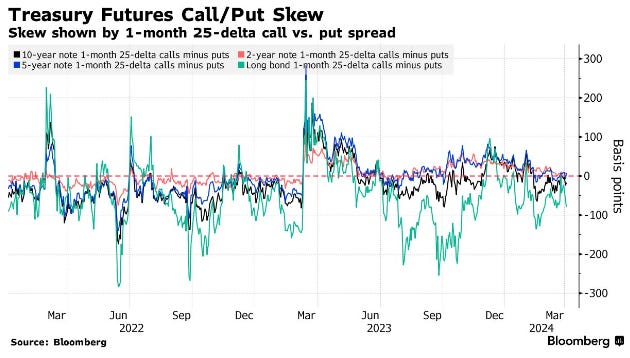

…The premium paid to hedge a selloff in Treasuries is on the rise. The cost to protect against yields rising on the long end of the curve reached the most expensive since the end of February during Tuesday’s session, as reflected by the so-called put/call skew on long-bond futures. In the Treasury options market, short volatility plays remained popular last week in both five- and 10-year tenors. Tuesday’s action has seen a couple of large bullish trades in the five-year tenor.

… AND the story continues talking of how it is ‘deleveraging resumes’ just as the very next day, then, EBB would alert us all as to how some ‘re-leveraging’ (via a YUGE options trade) would then reappear!!

FunTERtainment continues on in the bond markets and enough outta me … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are just a hair cheaper this morning, somewhat tethered by the outperforming Gilt market (UK-US 10's -4.7bp) and, to a lesser degree, by Bunds (US-Germany 10's +3bp). DXY is +0.2% while front WTI futures are UNCHD. Asian stocks were mixed, EU and UK share markets are modestly higher on balance while ES futures are showing +0.35% here at 7:15am. Our overnight US rates flows saw ranges during the Asian session and little flow amid a Hong Kong holiday. In London hours it was another quiet session there with light buying noted alongside interest in curve steepeners. Overnight Treasury volume was ~70% of average overall with 30yrs (112%) seeing relatively standout average turnover again this morning.

… This soggy backdrop is appropriate for the US rates market given that key rates benchmarks have spent recent sessions somewhat adrift near key range supports like the 4.36% level in Treasury 5yrs shown in our first attachment this morning. We have been locally impressed by the price action over the past few sessions as bearish forays above said range supports have been quickly rebuffed by either buying, receiving or covering. The daily chart of Treasury 2's looks predictably similar and even more textbook, technically. It's interesting how market narratives have shifted this year, moving the super well-defined ranges down and up in doing so... The one thing that stands out in this chart of 2's is that yields are nearing the apex of their Ascending Triangle. Truth or Dare time for them this week???

… never a fan of truth or dare — then or now — but so it goes … and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Upward revisions to European PMIs support bourses & EUR modestly … EGBs bid despite PMI pressure though off highs in somewhat limited newsflow, USTs flat

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ about everything from ADP to ISM and all sorts of things inbetween…

The ISM services composite softened somewhat in March, but remained in a range consistent with solid service sector growth. March's decline appears to reflect easing supply chain issues, with supplier deliver times and input prices both easing following early in the year disruptions. Demand conditions remain solid.

We think carry trades can still perform as vol-adjusted carry remains high, global liquidity is still abundant, the Fed’s reaction function is dovish and US growth revisions are positive.

A bullish view on FX carry does not equate to a bearish view on the USD, which is not an appealing funding currency for carry trades and is itself a high yielder. We favour EUR, CNH and JPY funded carry trades.

Furthermore, carry trade valuations are now less appealing, which suggests that going forward, returns will come more from pure carry than price moves.

We reiterate trade ideas across FX and rates which we expect to perform well in a range-bound regime.

Citi: Initiating a Jun/Jul FOMC OIS weighted flattener (a note from 04/02 and a BULLISH buy the front-end DIP look and they mention how / why it is fine in to NFP as March tend to come in below expectations…)

We like entering a lightly bullish front-end expression via a weighted June/July FOMC OIS flattener

The market has correctly in our view re-calibrated rate cut pricing lower in the face of stronger data. However now that the market is pricing slightly less than one full rate cut by July (July FOMC OIS at 5.10% as of 12:30PM EST on April 2nd vs spot OIS at 5.33%), we think the risk/reward looks attractive to position for a full rate cut by July even with a skip in June. If the Fed doesn't cut by July, the Sep meeting is just before the election, which makes it a tricky proposition for the Fed to start easing then. If the Fed skips July, then it most likely means expectations of no rate cuts this year. We think that is very unlikely….

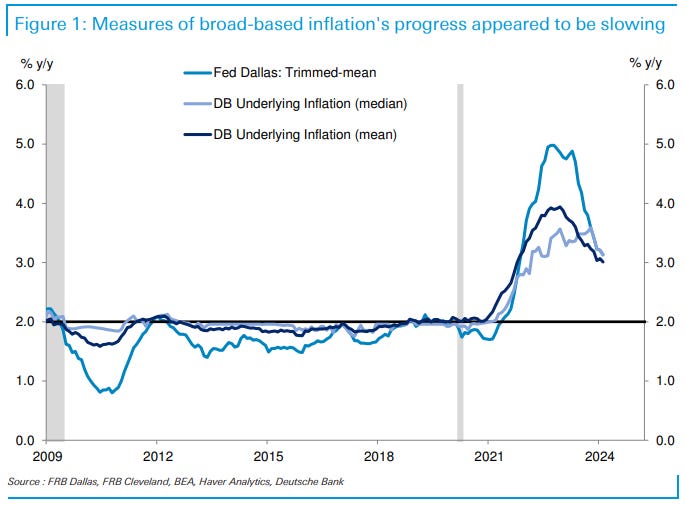

After running below the Fed’s objective in the second half of 2023, progress on PCE inflation slowed to start the year. Year-over-year headline PCE inflation was mostly unchanged in February and core PCE inflation fell 10bps to 2.78%. Updating our suite of statistical models, we find that our monthly mean estimates for trend inflation declined by about 6bps to 3.0%, while the median estimate fell by 8bps to 3.1%. These metrics confirm a slowing in the pace of progress, with both measures staying around the 3% level for the past four months.

Uncertainty about the extent of further disinflation is why Fed officials have stressed that they need to see more data before dialing back the degree of policy restraint (See Monthly charts: You can't hurry cuts. No, you just have to wait and Fed Watcher: Not so fast). The next few monthly inflation prints will be critical to determine whether the disinflation trend is still clearly in place. Assuming ~20bps prints for the March and April core PCE readings, year-over-year core PCE inflation would fall to 2.5% going into the June 12 FOMC meeting. In our view, this would be just enough progress for the Fed to begin cutting rates at that time.

BOTTOM LINE: According to the ADP report, private sector employment increased by 184k in March, 34k above consensus expectations. The March ADP report was stronger than our previous assumptions and adds to the evidence from other Big Data indicators that the pace of hiring was solid. Additionally, the strength in leisure and hospitality and construction jobs— for which the ADP panel has relatively good coverage—is consistent with the boost to nonfarm payrolls we expect from elevated immigration. We are boosting our nonfarm payroll forecast by 25k to +240k ahead of Friday’s report (mom sa).

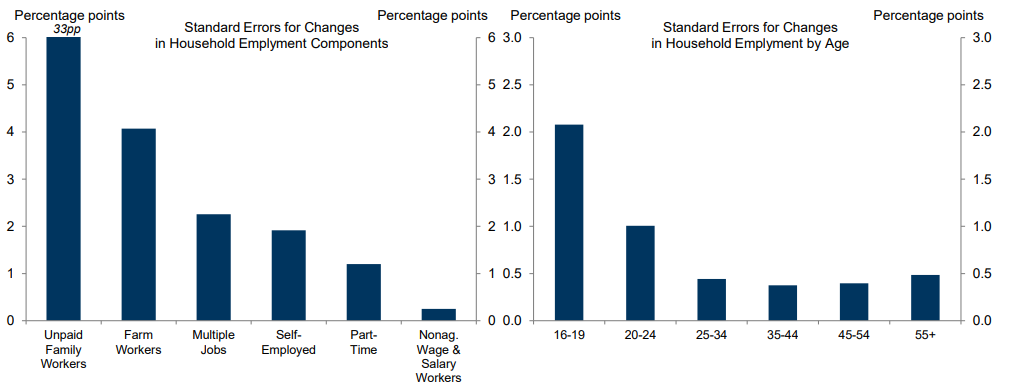

… MULTIPLE JOB HOLDERS, SELF-EMPLOYED, PART-TIMERS, ETC. The most reliable household employment series is employment of nonagricultural wage and salary workers. Estimates of agricultural workers, unpaid family workers, and self-employed workers have much more sampling uncertainty and volatility. Similarly, estimates of employment of younger workers are much more uncertain than estimates of employment of workers aged 25+.

Goldilocks: ISM Services Below Expectations (prices pd 4yr low — not helping prices paid for bonds past couple / few days, though :))

BOTTOM LINE: The ISM services index decreased 1.2pt in March, below expectations. The composition of the report was mixed, as the employment and business activity components both increased while the new orders component declined. The prices paid measure fell to a four-year low.

In mid-January, we turned neutral on duration given several factors: (1) Too much Fed priced in too early, (2) extreme momentum and sentiment around fixed income – the late December/early January bond FOMO rally, and (3) technical reversal signs. We feel that all three of these, to varying degrees, have not only corrected but now may be nearing similar extremes, just in the bearish direction. Thus, we favor scaling into US front end longs here, with the balance likely after payrolls and into or out of CPI next week.

… Given this, we favor scaling into 50% 2yr longs starting here at 4.68%, with room to add the remaining 50% against 4.82% - specifically 4.80% (which if we hit, would reflect what in our view would be quiet extreme reduction in the pricing of the Fed's policy cuts at this juncture). In addition, given our expectations for payrolls this Friday to print +200k (and given recent strength in the activity data overall), we want to leave room for any potential further selloff after payrolls and before CPI.

Strategas: U.S. YIELD FORECAST UPDATE: SOFT LANDING PERSISTS (looks like a note with a message but a message for both Team Soft Landing (60% odds) as well as Team Recession (30% but declining) … so, something for everyone?)

… We believe that in a soft landing, yields have some room to dip across the curve over the next 2 quarters, driven in large part by the much anticipated start of rate cuts and the slowing of QT. But this yield reprieve should prove short-lived, as supply and inflation should once again become concerns by the election, helping to push the curve higher again by the end of 2024 and into early 2025 …

Federal Reserve Chair Powell spoke yesterday. Today, no fewer than five members of the Fed are speaking on the economic outlook, presumably to clarify what Fed Chair Powell “meant to say”. Actually, Powell’s speechwriters did not say much controversial, keeping rate cut expectations alive. Media comment around this has tended to sensationalize—inflation is branded as sticky (it is not), and above target (moot point)…

Wells Fargo: Is a Struggling Service Sector a Sign of Progress? (didn’t seem to help bond prices that were paid much past couple days…:))

A cooling in service-sector activity was on display in the March ISM Services report. The prices paid index dropped to a four-year low and the employment index stood in contraction territory for the third time in four months.

… The eye-catching development in the details is how the prices paid component dropped more than five points to 53.4 (chart). A challenge for the Federal Reserve has been the way robust spending on services has slowed progress in bringing down services inflation. On that basis, the drop in the prices paid component is encouraging, at least at face value. The prices paid index dropped to its lowest reading since March 2020; however, the fact that 13 industries are still reporting an increase in prices suggests that even with some stabilization in the rate of price growth, inflation is still a concern.

Wells Fargo: March CPI Preview: Early-Year Strength in Inflation Noise or Signal?

The March CPI report will be a key indication of whether the pickup in inflation at the start of 2024 was a function of early-year noise or if inflation's journey back to the Fed's target has been drawn out materially. We believe it will show hints of both dynamics at play. Headline CPI likely rose by 0.4% for a second straight month, which would push the year-over-year rate up to a six-month high of 3.5%. Excluding food and energy, we estimate prices rose 0.3%—a tick softer than in January and February but similar to the pace averaged in Q4, in a sign underlying progress remains stubbornly slow…

Yardeni: 'Knock On Wood'

Fed Chair Jerome Powell spoke at Stanford University today about the economy and monetary policy. He said, "I think we've gotten to what is, knock on wood, a pretty good place." He added, "We're using our tools to try to bring inflation down the rest of the way to 2%, while all the while keeping the economy strong as well."

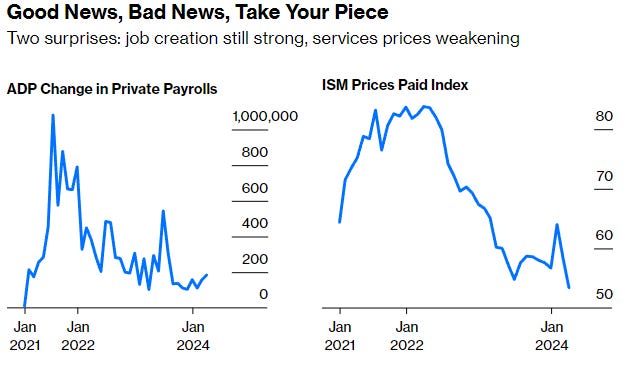

Today's data releases were mixed. According to ADP, private payrolls gained 184,000during March—more than expected. The March NM-PMI was a bit weaker than expected at 51.4 (chart). But the new orders (54.4) and production (57.4) components remained strong. The employment index (48.5) has been relatively weak in recent months, but that doesn't square with the ongoing strength in services payrolls.

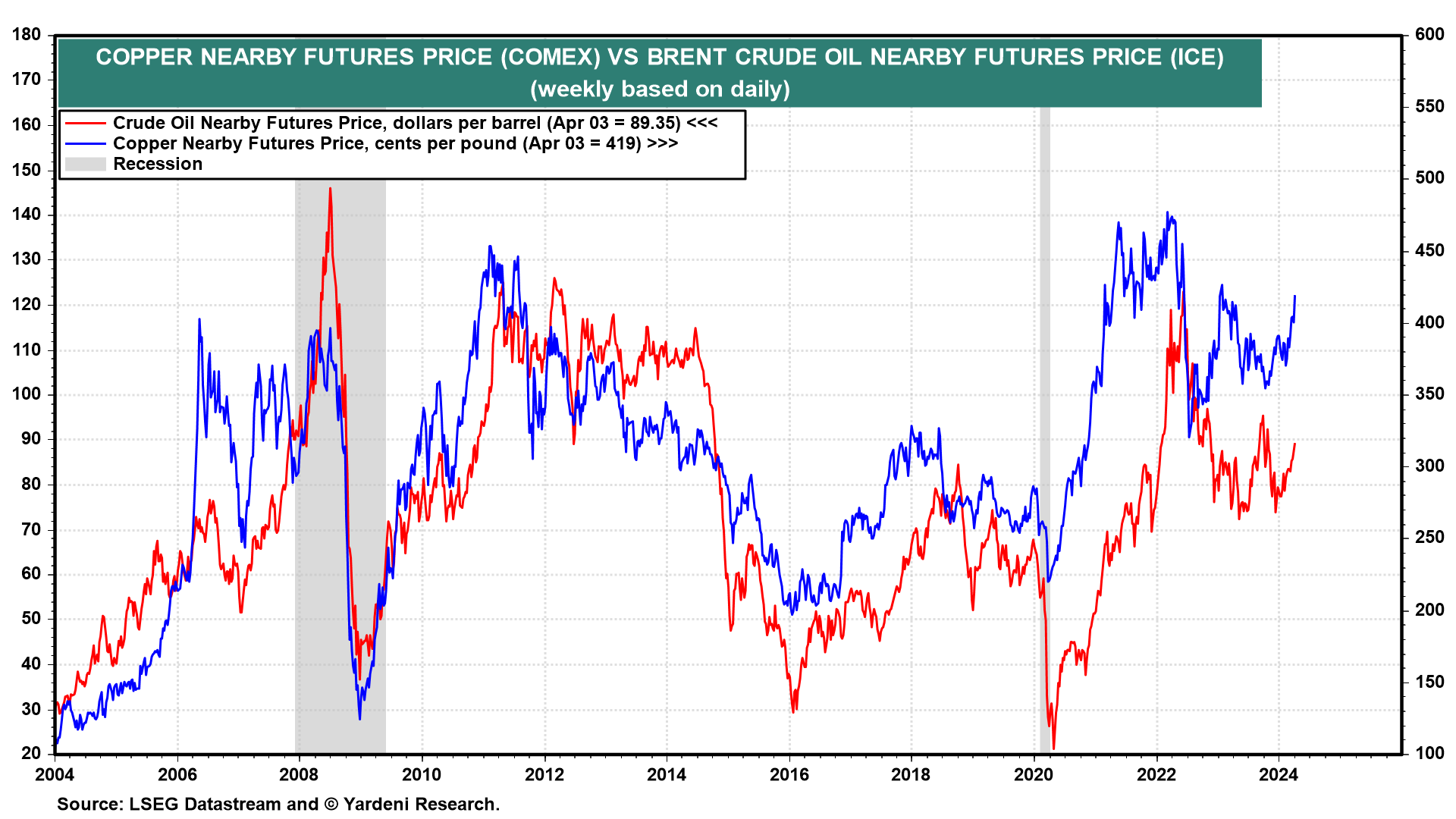

The price of copper continued to rebound suggesting that speculators are speculating that China's economy is improving as suggested by the the March Chinese M-PMI release (chart). The price of a barrel of Brent crude oil remains on the verge of breaching $90.

Stock prices were mixed today in line with our expectations for a pause in the powerful near-vertical rally since October 27, 2023. Apparently everyone agrees with Powell that the economy is in a "good place"--maybe too many people are thinking so….

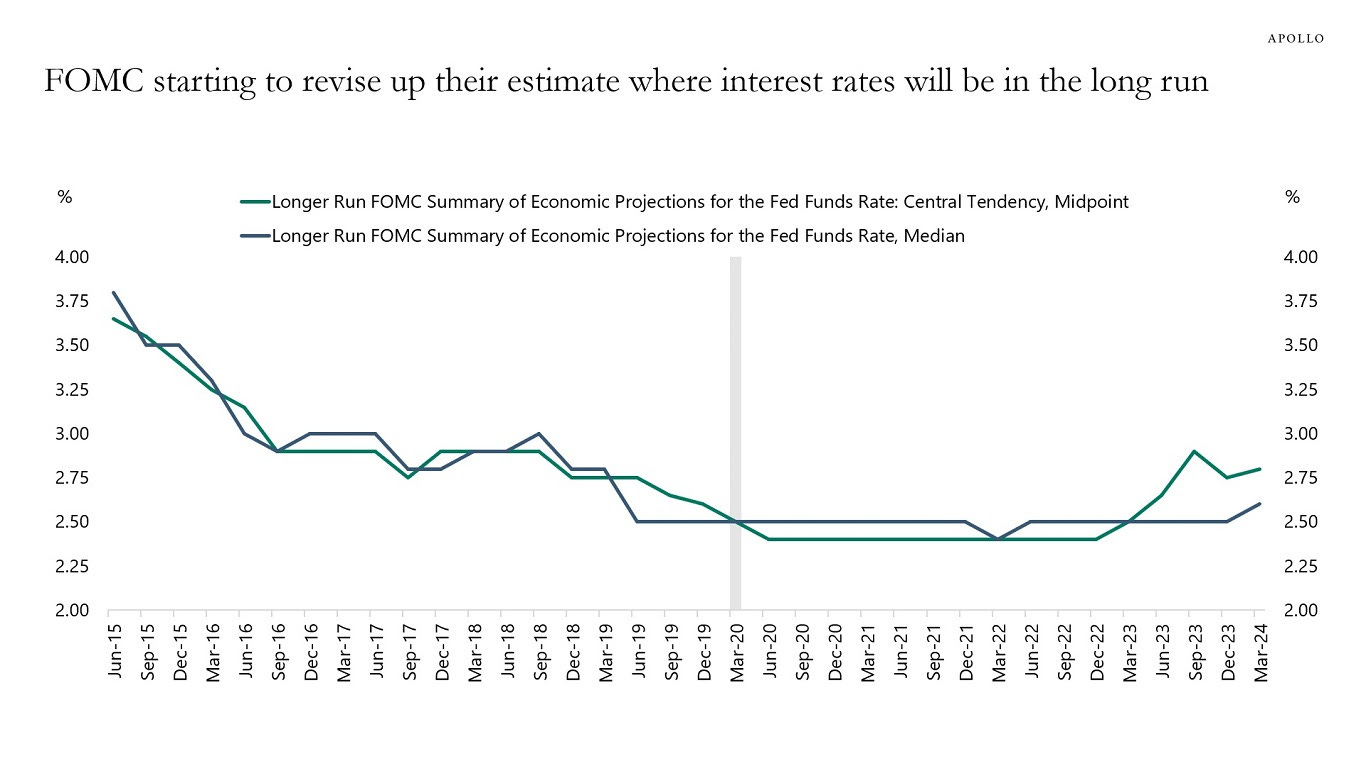

The Fed’s estimate of where interest rates will be in the long run has started to move higher, likely driven by the muted response of the economy so far to Fed hikes and by structural changes in deglobalization, energy transition, and defense spending.

Bloomberg (via ZH): Bond Longs Throw In Towel As Upturn Becomes Undeniable

Bloomberg: Powell’s Familiar Tune Is Music to the Market’s Ears (Authers’ OpED)

Investors think they are at last on the same page as Jay Powell and the Federal Reserve.

… Powell’s umpteenth reassurance did not pass without a reaction after yet another switchback in the economic data. He talked after the market had heard that private-sector payrolls were growing more than expected (suggesting less need for rate cuts), and also less than two hours later that the ISM survey of supply managers in the services sector had found the most benign reading on prices in four years (suggesting rate cuts might go ahead):

This zigzag followed a welter of data that has doused the optimism for multiple rate cuts at the start of the year. Now, there is an increasing possibility of a no-landing scenario with higher-for-longer rates. While Powell’s stance had barely changed, it calmed the markets, as it has time and again in the last six months. The absence of any newly hawkish sentiment was enough to drive a turnaround in the bond market:

Bloomberg: American Exceptionalism Is on Display in the Bond Market (El-Erian OpED and near / dear to me as we used to help friends near and mostly FAR away, travel in this differential … )

The divergence between key fixed-income benchmarks shows the US economy is on a healthier endogenous growth path compared with Europe.

Many of us have our favorite economic and financial indicators. I’m referring to those indicators that don’t get a lot - if any - attention from the television channels geared toward finance and markets and yet can provide important insights. One of my favorites - the divergence between key US and German fixed-income benchmarks - is at a notable level.

More specifically, I’m talking about the difference between the yield on the 10-year US Treasury note and its counterpart in Germany (which also serves as a benchmark for much of Europe). In early trading Wednesday, this differential had risen to 200 basis points in favor of the US, a level only reached three times since the start of 2020. Moreover, and as shown in the chart below, it is now well above the low over the past three years of 90 basis points and just short of the high of 214 basis points.

…Fundamentally, the widening captures the dominance of American economic exceptionalism over European economic stagnation, illustrated most comprehensively by the contrast between 4% growth in US gross domestic product in the second half of 2024 and recession in Germany. With that comes a divergence in inflation rates, with US price increases proving more stubborn than Europe’s in what many view as the “last mile” in central banks’ battle against inflation.

Importantly, there is more to this divergence than just recent economic numbers. The US economy is on a healthier endogenous growth path compared with Europe.

In addition to being supported by a more favorable set of initial conditions – from greater flexibility in factors of production to more agile entrepreneurship – US growth also has been boosted by a bigger fiscal impetus and stronger policy focus on the drivers of future economic growth. Also, as noted recently by Andrew Balls, the Pacific Investment Management Co.’s chief investment officer for global fixed income, in an interview with Bloomberg News, the structure of the US mortgage finance system makes its economy less sensitive to higher interest rates…

WolfST: How the Huge Wave of Immigrants into the US in 2022 and 2023 Impacts the Employment Data of the BLS Household Survey

The BLS uses the Census Bureau’s understated population estimates that ignore the surge of immigrants. But the CBO’s estimates pick them up.

{kind=link}

I'm looking for the BLS to serve us

up a NFP number of 350K+.

Gotta keep the Narrative going...

Absolutely correct..."Jay, to the rescue".

Fed Chair Powell delivers remarks on the economic outlook at Stanford Business School — 4/3/24

https://www.youtube.com/live/k25Fx-EFlA0?si=U4B-sU5_Xoor2I7b