Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this evenings note.

I’m sending along this evening as I’m going to be attempting to accommodate incoming travelers, weather permitting, and only have a couple / few things to add TO the recent Team Rate Cut denting price action…

5yy: triangulating as yields approach supportive TLINE (just beneath 4.40) as momentum oversold but not yet an extreme FADE signal…

(this visual inspired by the ‘ascending triangle’ noted in far better detail by Citi HERE earlier today)

… And so, a couple / few days does NOT an economy heal. There are certain things going on under the surface which I’m unable to readily dismiss AND speak to a need for cuts. Take, for example, this visual from twitter

For the life of me I can't figure why this hasn't gotten more attention. I've been routinely chided that consumers are spending on services/experiences instead of stuff. But restaurant sales&traffic are the weakest since they were CLOSED during covid, and the GFC before that, these last 2 months!! Hellooooo..…

… I’m struggling to reproduce this with data from NRA on my own and she’s plenty more than credible so we’ll just leave well enough alone.

Bond market price action past couple days have served as a(nother) warning shot across the bow and whether or not these funny things happening to Team Rate CUTS the past several days prove to be correct, well, remains to be seen…

Friday’s data and JPOW commentary — reiterating— and Mondays data then combined with today’s JOLTS data left us all again in that precarious position whereby good news is turning out to be BAD for what’s supposed to be either the BEST month or the 2nd BEST month<please choose one> of the year for stonks.

Why? Cuz bonds, you know. AND so …

ZH: Gold Hits Another New Record High But Bonds, Stocks, & Bitcoin Battered On 'Good' News

… and with the price action embedded in that end of day ‘wrap’ came yet another hawkish reflex in bond markets …

ZH: Market Now More Hawkish Than The Fed As June Rate-Cut Odds Fade

… Moving from a few words, a visual and ZH links on to some of THE VIEWS you might be able to use…SOME of what Global Wall St is sayin’ …

This monthly chartbook highlights our top charts for understanding the current state of the US economy and the outlook for 2024-25. The document features several sections including discussions of: the Fed rate cut debate; the near-term economic outlook; why steady state employment gains might be higher in the near-term; the bumpy road to price stability; our baseline view for the Fed; and longer-term issues related to growth, inflation and fiscal deficits and debt.

…DB Fed expectations: First cut in June, 100bps of cuts in 2024, nominal neutral rate ~3.5%

…A tentative ID of the 2024 dots

Goldilocks: Factory Orders Above Expectations; Job Openings Broadly in Line With Expectations; Boosting Q1 GDP Tracking to 2.3%

BOTTOM LINE: Factory orders increased by 1.4% in February, above expectations, while growth in January was revised down slightly. Job openings increased were little changed at 8,756k in February, broadly in line with expectations. Job openings have remained stable in recent months. After incorporating today’s JOLTS data, our jobs-workers gap based on the JOLTS, Indeed, and LinkUp measures of job openings stands at 2.0mn in March.

Private job openings rate remains elevated at 5.5%, while the private hiring rate is still low at 4.0%.

The gap between openings and hires is unusually wide

… And from Global Wall Street inbox TO the WWW,

Apollo: Strong Labor Market Continues (NOT what Team Rate Cut wanted to hear / see)

After the Fed started raising rates in March 2022, the labor market started softening, with households saying that it was harder to find a job. This changed after the Fed pivot, see the first chart below.

Since December 2023, households have said that it is easier to find a job, reflecting a rebound in corporate confidence, see the second chart.

The bottom line is that the improvement we have seen in the labor market in January and February is real. Combined with low jobless claims, nonfarm payrolls are likely to surprise to the upside again in March.

… Stocks Trump Bonds The chart below was included in today's Chart of the Day sent to subscribers titled "S&P 500 Up 30% in a Year. Now What?"

Incredibly, the S&P 500's one-year return has beaten the one-year return of long-term Treasuries for 40 months in a row! That's easily a record going back to the late 1970s!

Anecdotally, we've seen a pretty big shift in rate cut expectations over the last few months. At the start of the year, it seemed like everyone was looking for 3 to 6 cuts in 2024, and markets were pricing about that many cuts based on Fed Fund Futures. This week, though, we're hearing a lot of chatter from speculators that there won't be any cuts at all in 2024. While Fed activity this late in election years has historically been low, we'd note that market pricing for zero rate cuts at all this year is still extremely low as well. As shown below, the current odds that the Fed Funds Rate will still be where it is now at year end are just 1.7%.

With the November Presidential Election now just seven months away, last week we published a brand new slide deck titled "Investing and Politics." This PDF provides eleven simple slides summarizing the impact (or lack thereof) of DC on financial markets. Topics covered include historical equity market performance under various Presidential administrations, performance under Democrats versus Republicans, whether or not the stock market can predict election outcomes, a look at the politicization of sentiment surveys, and just how often the Fed typically hikes or cuts rates in election years…

Bloomberg: Let’s Applaud the Good News for the World Economy

Some important bellwethers of global commerce are looking better.

WolfST: This Labor Market Is Not Loosening Further: Fed Gets More Reason for Wait-and-See

But the headlines-grabbing layoff announcements had the effect of calming the churn.

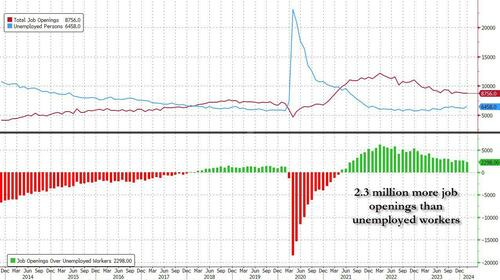

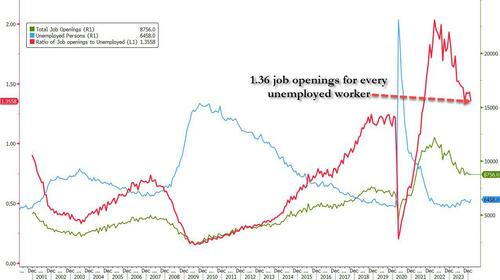

ZH: JOLTed Snoozer: Job Openings Unchanged As Hiring And Quits Unexpectedly Rise

…And speaking of revisions, just like in the payrolls report, here too the BLS appears to be tasked with making a great, if erroneous, first impression then quietly revising it lower, and sure enough, 12 of the past 14 months have seen job openings revised lower, just like everything else in Biden's economy.

Accurate or not, the unchanged number of job openings coupled with the recent jump in unemployed workers meant that in February, the number of job openings was 2.298 million more than the number of unemployed workers (which the BLS reported was 6.458 million), down significantly from last month's 2.624 million.

Said otherwise, in January the number of job openings to unemployed dropped to 1.36, a sharp slide from the January print of 1.43, and matching the lowest level since August 2021 and almost back to pre-covid levels of 1.3.

What was more interesting than the snoozer of a headline job openings print - which we are certain will be revised lower again next month as has been the case with everything under the Biden admin - was the number of quits: here we find that the number of people quitting their jobs, an indicator closely associated with labor market strength as it shows workers are confident they can find a better wage elsewhere - rose for the second month in a row, to 3.484 million up from an upward revised 3.446 million (vs 3.385 million reported initially).

And another interesting twist is that amid the stagnant level of job openings, not only did the number of quits increase, but so did the number of hires, which rose to 5.818 million - the highest since October 2023 - from 5.698 million despite a 44K drop in durable goods manufacturing hiring.

Finally, no matter what the "data" shows, let's not forget that it is all just estimated, and it is safe to say that the real number of job openings remains still far lower since half of it - or some 70% to be specific - is guesswork. As the BLS itself admits, while the response rate to most of its various labor (and other) surveys has collapsed in recent years, nothing is as bad as the JOLTS report where the actual response rate remains near a record low 33%

Happy house guest hosting! Hope they aren't Houseguests from HELL :)! Having slept on my share of friends couches, floors, and garages, I learned a simple yet effective principle: Leave your hosts before they WANT you to leave; better yet Leave on a High Note. And if you leave your drunk(er) friends in the dark after they've passed out they'll feel Guilty about it next day :) as I learned last month!

Happy house guest hosting! Hope they aren't Houseguests from HELL :)! Having slept on my share of friends couches, floors, and garages, I learned a simple yet effective principle: Leave your hosts before they WANT you to leave; better yet Leave on a High Note. And if you leave your drunk(er) friends in the dark after they've passed out they'll feel Guilty about it next day :) as I learned last month!