Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this UPDATE and additional holiday long weekend special …

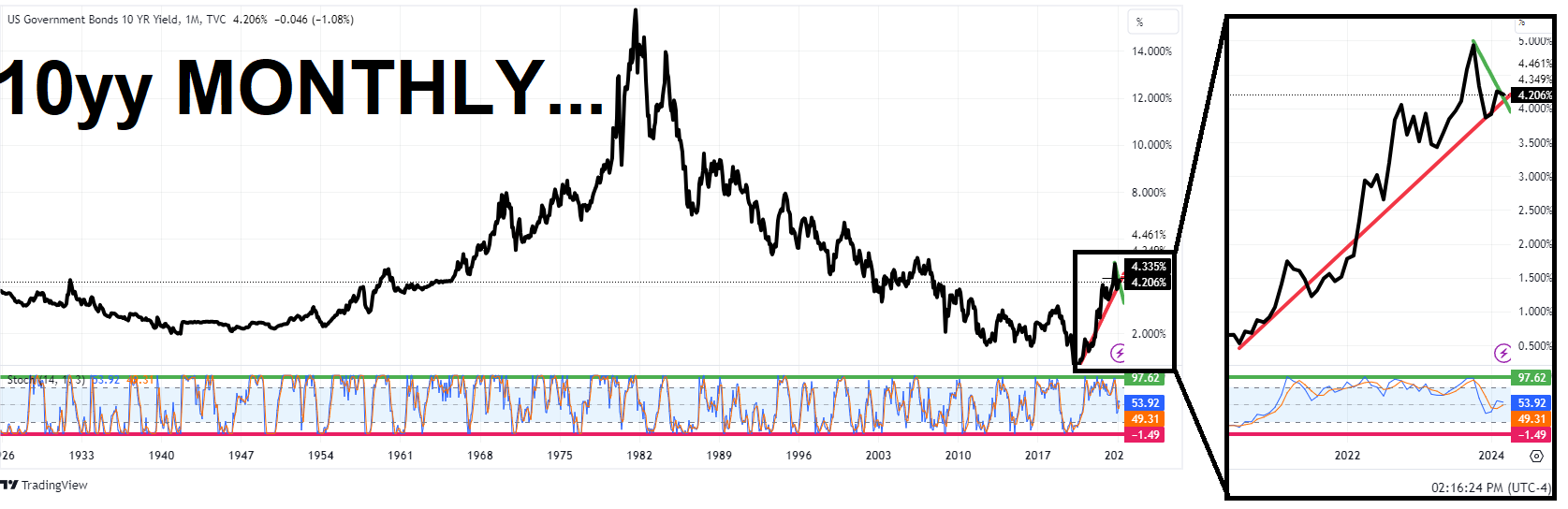

In the case Yesterday’s note left you wanting / needing more and in addition 2yy and 30yy monthly visuals …

10yy: I’m getting sense that while momentum (stochastics, bottom panel) are sort of middling, there’s a larger move waiting in the wings … my Magic 8 Ball not yet back from the dry cleaners so I’ll leave it to you to (over)interpret and flip whatever coins you’d like to but …

… can’t WAIT to see how mkts respond tomorrow — Easter — when they reopen at 6p.

Meanwhile, yesterday, JPOW spoke AFTER we got PCE data … below is a link with a visual as well as the entire video for your review …

ZH: Watch Live: Fed Chair Powell Speaks With Global Markets Closed

Watch Live: Fed Chair Powell Speaks With Global Markets Closed

With global capital market closed, crypto maybe the only price action to monitor to judge if Fed Chair Powell says anything new this morning.

Powell is due to participate in moderated discussion before the Federal Reserve Bank of San Francisco Macroeconomics and Monetary Policy Conference.

The market is still pricing in a just better than 50-50 chance of The Fed's first cut coming in June, and the question is whether - like Waller earlier in the week - Powell will signal a longer pause...

Watch live here (due to start at 1130ET):

… and as the PCE was addressed directly, early on and you should watch / listen for yourself and jump to your very own conclusions and assumptions as to how prices may / may NOT react once given a chance.

I passed along some data related links Yesterday, meanwhile, a few observations readily avail on the intertubes …

Fed chief says PCE inflation data ‘in line with expectations’

Says inflation will continue to ease on ‘sometimes bumpy’ path

Bloomberg: Fed’s Core Inflation Gauge Posts Biggest Sequential Gain in Year (kinda makes the link just above make a whole lotta sense … unless, since I’m long gone from that seat … I’m missin’ something? anyone??)

…The so-called core personal consumption expenditures price index, which strips out the volatile food and energy components, increased 0.3% from the prior month, data out Friday showed. That followed a 0.5% reading in January, marking the biggest back-to-back gain in a year. From a year ago, it advanced 2.8% …

… The core PCE data, on a six-month annualized basis, accelerated to 2.9%, the fastest since July. And the end of last year, it briefly slipped below the Fed’s 2% target…

Bloomberg: Charting the Global Economy: US Inflation Cools; Japanese Yen Stays Weak (this link cuz of visual helping contextualize all the above … Patience, then, is to be hotly debated virtue for any / all them virtue signal callers…in any case, see whatever you wanna see, then, I suppose … )

A key measure of underlying US inflation favored by the Federal Reserve cooled last month, and consumer spending rebounded sharply…

… The Fed’s preferred gauge of underlying inflation cooled last month after a stronger January increase than initially reported. Chair Jerome Powell spoke after the figures were released Friday, saying they were “pretty much in line with our expectations” and reiterated the central bank is in no rush to cut interest rates.

Bloomberg: Bullish Stocks Narrative Seen as Intact After US Inflation Data (couldn’t NOT let the day go by without this final BBG link and perhaps the most important — at least for any / all long stocks trading rate CUTS which are then to become EASING cuz, you know … so bad things are good?)

Inflation view won’t shift, Richard Bernstein Advisors says

Mismatch between spending and income is worrying, Sosnick says

… US equity and bond futures will open as usual at 6 p.m. New York time Sunday following the holiday …

at BiancoResearch (offering this tweet and observation of PRICE ACTION …

*POWELL: CAN HOLD RATES STEADY IF INFLATION DOESN'T COME DOWN

*POWELL: DON'T THINK RATES WILL RETURN TO PRE-PANDEMIC LEVELS

*POWELL: ECONOMY NOT SUFFERING FROM THIS LEVEL OF RATES

*POWELL: NO REASON TO THINK ECONOMY IN OR ON EDGE OF RECESSION -- Only one market is open today ... crypto/Bitcoin. It is sold off as Powell spoke, Views his talk as hawkish.

BARCAP: February PCE price inflation: Legally blind (not to be confused with the band …)

Core PCE price inflation softened to 0.26% m/m in February following January's upwardly revised 0.45% m/m, keeping a June Fed cut likely. The softer-than-expected reading mainly reflects an idiosyncratic decline in the index for legal services. Even so, core PCE is running at 2.9% 6m saar, up from December's 1.9%.

… Today's estimates provide some hints about why Powell was expecting a softer core than private estimates, but the details also pose new uncertainties. Relative to our own translation, most of the miss came from the legal services component of "other services." The estimated price index for this category, which accounts for 0.8% of nominal core PCE, abruptly fell 5.5% m/m in February, more than reversing January's 0.8% m/m increase (Figure 1, Figure 2). This decline subtracted about 4bp from the overall monthly core PCE reading, in % m/m terms, against our expectation of a small positive contribution, explaining nearly 5bp of our 7bp miss for core. The BEA's source data for this category, which come from details in the CPI, are published only through September. According to our conversations with the BEA, its more recent estimates derive from BLS data that are not shared with the public. (We do not know whether the Fed is privy to these unpublished data.) Even so, the magnitude of the estimated decline in this category is somewhat surprising and does not align with any anecdotes we have heard about price trends for legal services. It also seems much at odds with the competing PPI deflator for legal services, which shows a 0.4% m/m increase in February. Regardless of whether we take this at face value, the softer-than-expected core strikes us as idiosyncratic, at best, with risks that that the drivers of this surprise may reverse in the coming months….

… We maintain our call for the FOMC to initiate the first rate cut at the June FOMC meeting, of 25bp, followed by two more 25bp cuts in September and December.

BARCAP: February personal income: Virtuous cycle intact (hmmm)

Real PCE bounced back in February following January's weather-related drop, led by increases in spending on services. This suggests solid real PCE growth in Q1. Meanwhile, personal income was supported by solid labor compensation growth, even if it surprised to the downside due to declines in dividend income.

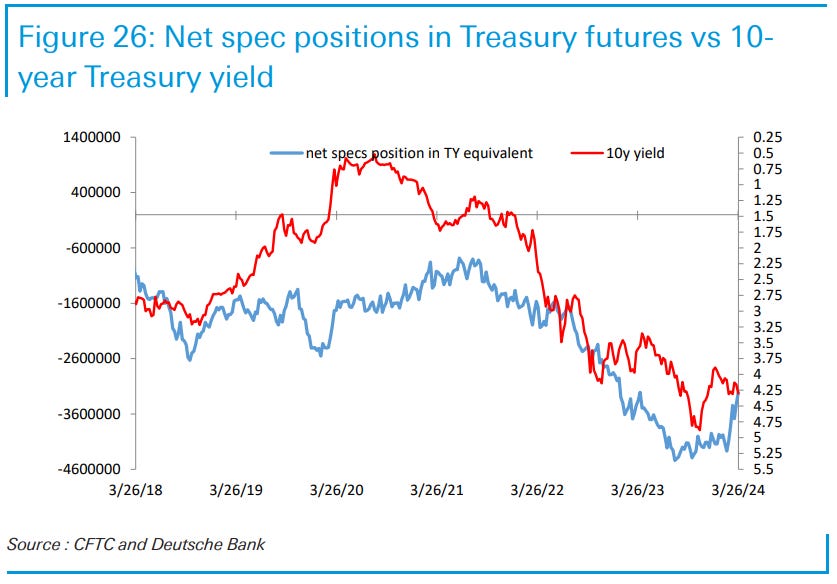

DB: Commitment of Traders (positions. lives. matter…)

Interest Rates: Speculators pared 39K contracts in TY equivalents from their net short positions in Treasury futures over the week prior to March 26 (Tuesday).

Asset managers lowered their net long positions in Treasury futures by 29K contracts in TY equivalents, while leveraged investors removed 35K contracts in TY equivalents from their net short positions. Asset managers saw reduced long positions in TU, UXY and WN and pared leveraged investor shorts. At the same time, asset managers saw increased net long positions in FV, TY and US and leveraged investor shorts. Dealers removed 22K contracts in TY equivalents from their net short positions…

Goldilocks: Core PCE Slightly Below Consensus Expectations; Saving Rate Falls to 3.6%; Boosting Q1 GDP Tracking to +2.1%

BOTTOM LINE: The February core PCE price index rose by 0.26% month over month, below consensus expectations, and the year-over-year rate declined to 2.78%. Core services prices excluding housing increased 0.18%, down from 0.66% in January and roughly in line with the average pace of Q4. Personal spending and income increased by 0.8% and 0.3%, respectively. The saving rate declined 0.5pp to 3.6%, the lowest level since December 2022. The goods trade deficit widened in February, reflecting a larger increase in imports than exports. Wholesale inventories increased above consensus expectations. We have increased our Q1 GDP tracking estimate by 0.3pp to +2.1% (qoq ar).

UBS: Powell and nonfarm payroll employment (economic weekly with some comments of interest, highlighted…all in, though, i’m left with a sense of disillusionment at conflict here — not only UBS but everywhere — and desire to have cake and eat it too — data fine now BUT ‘we expect to deteriorate soon’ but meanwhile, we’re gonna push UP our growth f’casts … clear as mud, at least to me)

We expect a better-than-consensus expects March employment report next Friday. Chair Powell stuck to the script today.

Economic Comment: will strong job gains derail the rate cuts? Chair Powell remained pretty balanced in his comments today, in our view, retaining the same general message from the press conference last week and testimony three weeks prior. In our view Governor Waller's comments remained consistent with the March Summary of Economic Projections (SEP) too. We expect a March employment report that would exceed consensus expectations across almost all dimensions, yet we do not think that will derail the plan to dial back the restrictiveness of monetary policy at the June FOMC meeting. There is a lot of other information between now and then that could derail the plan, or keep it on track. We expect the factors pushing up March employment to give way in the coming months…

The Week in Review: Core PCE inflation moves down Core PCE prices rose 0.26% in February, leaving the 12-month inflation rate at 2.78%, 10 bps below January's 2.88%. Real spending climbed 0.4% in February, with downward revisions to prior months. However, we nudged up our GDP tracking this week to 2.0% taking on board the incoming data. In the final release, real GDP in Q4 was revised higher, making the four quarters of 2023 even stronger…

…Core PCE inflation slides 10 bp to 2.78% Core PCE prices rose 0.26% in February — down from the upwardly revised 0.45% increase in January and close in line with our 0.27% expectations. That leaves 12-month core PCE inflation through February at 2.78%, 10 bp below the 2.88% revised January estimate. With the 0.26% February increase replacing a weaker 0.10% August increase, the 6-month annualized pace for core PCE prices increased to 2.89%, up from January's 2.56% reading. It spent a couple of months at the end of 2023 below the Fed's 2.0% inflation target. Headline PCE prices rose 0.33% in February (in line with our 0.35% expectations), leaving 12-month PCE inflation up 2 bp from January at 2.45%. Both headline and core PCE 12-month inflation are now currently at their lowest levels since early 2021, right at the start of the inflation surge. Base effects should be a solid downward influence on inflation in coming months. We expect 12-month core PCE inflation will continue to edge down over the first half of the year until reaching a 2.35% pace in June

… Booming manufacturing construction has propelled structures investment, a trend we highlight in a recent special report. Government outlays were also revised higher, but the leg-up in consumer spending, specifically services outlays, was the primary driver of the upward revision to GDP. Although sustained consumer spending in the sector is on its face an encouraging sign for growth, it may be preventing a sustained cooling in services prices.

Illustrative of this point, the February personal income & spending report painted a picture of a defiant consumer that continues to splurge on services. Nominal spending rose 0.8%, the largest monthly gain in a year and a half, and once adjusted for inflation rose a still-sturdy 0.4%. But it was a 0.6% jump in real services outlays that stole the show. This was the largest jump in real services spending since the summer of 2021 when consumers were still flush with pandemic-era savings. The surge in services spending is another headache for policymakers. As long as consumers keep splashing out in the service sector, the businesses that provide these services have no incentive to ease up on pricing. To that end, the inflation rate for services less housing, or "super-core" inflation, came in at 3.3% year-over-year, but the three-month annualized rate of 4.5% points to near-term upward momentum (chart). Although the annual rate of the core PCE deflator, the Fed's preferred measure of inflation, came in at 2.8% year-over-year with a slightly smaller-than-expected monthly rise of 0.3% in February, services prices are no longer cooling as they were a few months ago.

And finally, a couple more things I’m reading through, straight from the intertubes…

Apollo: Outlook for Banks (click up / through the chartbook which is linked … i’ll pull forward a chart or two which caught my eyes…)

Since the beginning of the year, the banking sector has been underperforming the S&P 500, and the regional banks have been underperforming the broader banking sector, driven by deteriorating earnings expectations for regional banks, see charts below. Our latest banking sector chart book is available here…

Discipline Funds: Weekend Reading – Inflation, Inflation, Inflation (a couple good pictures and an answer TO the question, ‘Why cut now?’ … not sure i’m fully there and on board yet but … proof all ‘round, I suppose, IF you choose to see it…)

… 1) Core PCE is STILL trending in the right direction.

Core PCE came in at 2.78% on Friday. This was the lowest rate of inflation we’ve seen since March of 2021 right before the big spike. This should ease some concerns going forward as there were concerns that this reading might come in at 2.9% or even higher. But now we can begin to safely assume that the seasonal quirks are behind us. Atlanta Fed’s Nowcast says the March reading will come in at 2.67%. So this is all trending in the right direction and I continue to see it trending that way for the remainder of the year unless something causes a huge commodity spike. Until then there’s just too much pressure in the housing component to overcome it.

The bigger picture here is that even though disinflation has moderated in its downward pace it’s still trending in the right direction. So, I think we can now safely assume that all the 1970s & 1940s narratives were wrong.

The question still remains though – is this enough progress to cut in June or July? We only have two more inflation readings before the June meeting and we’re likely to be at or close to 2.5% by that point. So, is that enough? I’d say yes, but I could also see the scenario where there are some members of the FOMC who are still hesitant and want to wait until July (or even later). That will almost certainly be the case if the next few inflation prints surprise to the upside. But as of now I still think it’s safe to assume that June is the month we get a cut. But it’s looking more like a coin flip between June and July at this point. Not that it matters a huge amount though because the difference between getting two or three cuts this year isn’t going to cause some seismic economic shift….

2) Why cut now?

… The bottomline is that the Fed is trying to manage the risks now. And I think they’re on the right path because the odds of a 1970s double bump look very low now, but the odds of overshooting on the downside look increasingly high. They don’t want to repeat the mistake of 2021 where they were slow to act and so some modest easing of rates here seems like a prudent decision in my view…

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (positions. lives. matter…)

WolfST: Fed’s Wait-and-See about Rate Cuts Supported by Highest-since-July Six-Month Core PCE & Core Services PCE Inflation

WolfST: Our Drunken Sailors Went Partying Again: Consumer Spending on Services, even Adjusted for Inflation, is Red-Hot

… and a live look in at one of my recent market therapy sessions …

… Just kidding! Or am I? :) All kidding aside, this guy’s all the therapy I need …

… Ollie livin’ his best rescued life now 2yrs IN with us and doing so as if he owns the place (he really does!!)

Great letter...

Excellent PCE summary....like splitting hairs..

I'm guessing July or September.

I believe there is no August meeting.

US economy not slowing down quickly.

That's a good thing.

The Rally continues....albeit after

a little disappointed in the PCE

number, not adding clarity to the

Inflation/Rate Cut picture.