I don’t have to remind you. Things, economically speaking, are challenging (to put it mildly) at the moment and the Fed’s got their hands full. Whatever they do next, how markets respond and then, how the Fed reflexes will determine everything.

Consider THISfrom … guess who, where you’ll find this chart — another realization that things may NOT be as good as they appear or we think / HOPE they are …

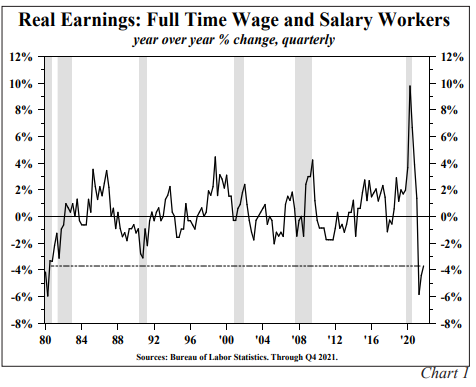

… Most Americans have suffered a substantial fall in their standard of living over the past twelve months. In the latest available twelve-month change, 116.2 million American wage and salary workers suffered a 3.7% decline in their inflation adjusted paychecks, the largest drop since 1980 (Chart 1).

The war in Ukraine has lifted bond yields by a quick 50 basis points, elevating it to nearly one full point above the year-end level of 1.9%. At this current level, the long-end treasury market has value considering the impending recessionary conditions which have always reduced inflation and interest rates. The economic data suggesting negative growth ahead include the following factors 1) the largest twelve month decline in real weekly earnings of 3.3% since this series began in 2000 which covers 72 million people. 2) Real per capita disposable income now stands 1.8% below one year ago levels and has fallen for seven consecutive months. 3) The composite index of the NFIB Small Business Survey sank to 93.2 in March the lowest since April of 2020. 4) Interest rate sensitive sectors such as housing and autos are already declining. 5) Inventories are rising rapidly and will accelerate further with any softness in demand causing cutbacks in production. 6) Fiscal policy turns restrictive in 2022 and there is just a hint of early restraint in Fed policy as total reserves declined by $425 billion since December and the main component of M2, other checkable deposits, has shown just 3.7% growth over the last three months

These and many other harbingers of recession constitute a favorable environment for long-term bond investors. However, should the Federal Reserve cease in their efforts to calm inflation before it has been fully restrained, bond investors should be wary.

Read all about his reasoning and how a low URATE produced 20mil jobs whereas government policies have hurt nearly 175mil Americans …

These are all things you’ve heard here at one point or another BUT as Lacy Hunt puts HIS (and clients) money where his mouth is, well … that saying whereby ALL opinions are created equally and it’s just that some continue to be more equal than others.

His warnings issued and we, collectively, know what we’re looking for. IF/when the Fed reverses course and gets soft on fighting inflation, THEN … break glass in case of emergency and … worry.

READ his comments and let them settle in. His comments may NOT be as raging bond bullish as you might expect (so, it’s different this time) and that, in and of itself says plenty.

Moving on, then here is a snapshot OF USTs as of 707a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are lower but off their overnight lows as bunds and UK gilts outperform on precolating recession fears there (see above). DXY is higher (+0.3%) while front WTI futures are lower (-1.3%). Asian stocks were mostly lower, UK and EU share markets are all lower (SX5E -1.65%) while ES futures are showing -0.15% here at 7:20am. Our overnight US rates flows saw aggressive bear flattening with several more block flows fueling the move. We saw EU real$ names selling across the curve as fast$ names chased the 2s5s and 5s30s curves flatter before flows/trends cooled into the NY open. Overnight Treasury volume was quite solid at ~150% of average overall with standout activity seen in 2's (206% of ave).

… and for some MORE of the news you can use » IGMs Press Picks for today (22 April) to help weed thru the noise (some of which can be found over here at Finviz).

… THAT — HIMCOs LATEST, HERE — is plenty and that is all for now. Off to the day job…

{kind=link}