Good morning…Happy Tax Day (said nobody ever). With most of the European Union shuttered for Easter Monday volumes (and narrative creation) should be light overnight and on into the day ahead.

That said, here is a snapshot OF USTs as of 708a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are modestly lower and the curve is slightly steeper as financial markets gird for 50bp Fed hike(s) and war (Ukraine/China's Covid Zero policy) outcomes. DXY is higher (+0.15%) while front WTI futures are lower (-0.3%). Asian stocks were mostly lower, EU and UK share markets are closed while ES futures are showing -0.4% here at 6:55am. Our Asian US rates flows saw elevated volumes in intermediates pushing yields higher despite a short session. Despite the further sell-off, our desk flows saw better buying in the long-end- largely from credit-hedgers. This buying allowed Treasuries to end the shortened Asian session off the earlier lows. With London out, our volume tracker is not working properly this morning.

… and for some MORE of the news you can use, head TO Harkster.com … Knowledge without the noise (and if its ALL the noise and links you like, Finviz).

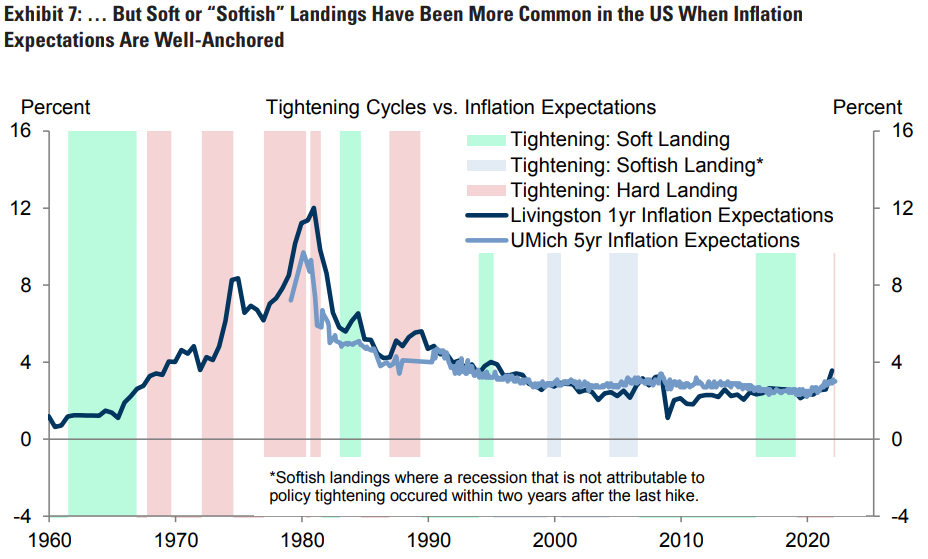

… Taken at face value, these historical patterns suggest the Fed faces a hard path to a soft landing as it aims to narrow the jobs-workers gap and bring inflation back towards its 2% target. We still do not see a recession as inevitable, however, particularly since the FOMC's goal of cooling the economy while avoiding a recession will be helped by post-covid normalizations in labor supply and durable goods prices. Nevertheless, the historical G10 evidence suggests the odds of a recession are higher than normal, and we now assign roughly 15% odds to a recession in the next 12 months and 35% within the next 24 months.

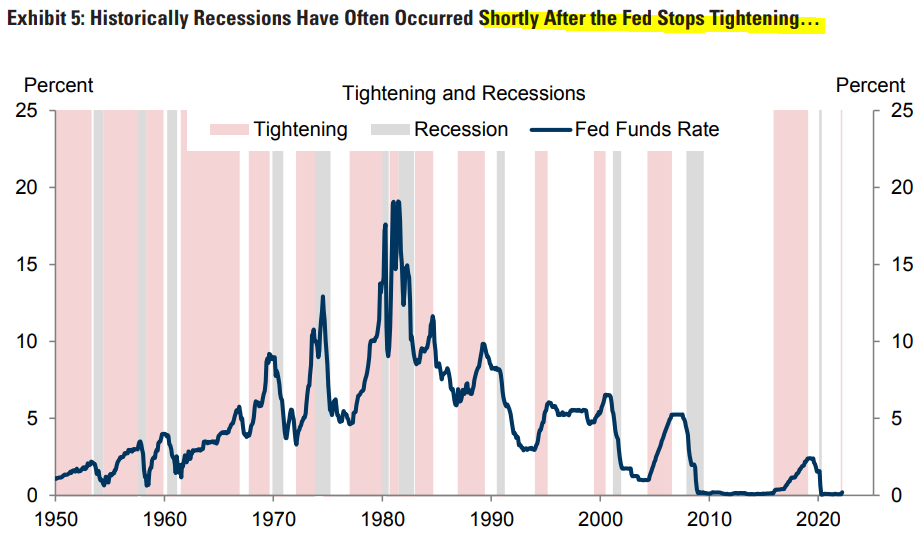

… On the surface, the track record from past tightening cycles in the US also suggests that the Fed faces a significant challenge in achieving a soft landing. As shown in Exhibit 5, US policy tightening cycles have historically been followed by recessions shortly after they end: Eleven out of fourteen tightening cycles since World War 2 have been followed by a recession within two years, implying a success rate of just 21%.

1 in 3 seems light to ME when you consider the FISCAL drag at the same time as the monetary policy efforts. See Hutchins HERE (where visual below comes from)

That being said, a chart which just hit Global Wall St inboxes across the land offers a ray of hope in as far as whatever happened Thursday and HOW investors may view it.

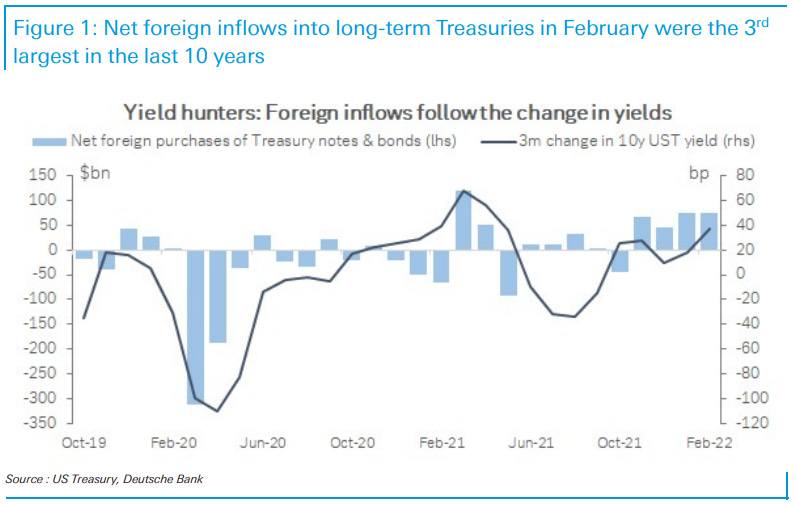

As Treasury yields rose to a cycle high in February and the 10yr note broke above 2% for the first time, foreign investors poured $75.3bn into long-term Treasury securities, according to the TIC data released on Friday. The net inflows were the largest since March 2021 and rank the third largest in the last 10 years. Importantly, it extended a trend of solid inflows that began in November when the Fed announced the tapering of QE purchases…

…The simplest explanation for the strong February inflows is that Treasury yields became more attractive. As the chart shows, foreign inflows tend to track the change in 10yr yields over time. However, it’s also possible that global geopolitics added to the foreign activity in Treasuries. International sanctions against Russia began in late February, and the source of inflows were concentrated in a few offshore centers that could in theory be used to evade those measures. On the official books, Russia’s reported holdings of Treasuries were little changed from the recent preceding periods at $3.8bn.

If you liked ‘em THEN, yer gonna LOVE ‘em now?

Now with recession calls updated and monetary (as well as fiscal) causality) in mind, yield hunters hunting all the while, here are some updated thoughts from everyone’s fav (bearish)stock jockey — Mike Wilson — reminding us of earnings season is NOT without risks.

Earnings Season Brings Risks We make the case that earnings revisions will decelerate amid 1Q reporting season as the MS Business Conditions Index (a survey of our industry analysts) just fell further and margin headwinds mount / are not fully reflected in consensus estimates. Stocks should discount this risk via the ERP channel.

Inflation no longer a net positive for earnings growth...While we appreciate howinflation can be good for nominal GDP and therefore revenue growth, we think inflation is no longer a net positive for earnings growth given the impact on costs that are now showing up in margins. Secondarily, the war in Ukraine has led to a spike in energy and food costs which serve as nothing more than a tax on a consumer that is already struggling with high inflation. In other words, we think the positive effects of inflation on earnings growth have reached their peak and are now more likely to be a headwind to growth, particularly as inflation forces the Fed to remain max hawkish. In that regard, the significant rise in back end rates is having a meaningful impact on interest rate sensitive areas of the economy and market, like housing.

Signs are emerging that 1Q earnings season may be more disappointing than thought... particularly from a guidance/forward estimate standpoint—earnings revisions breadth for the S&P 500 has resumed its downtrend over the past 2 weeks and is once again approaching negative territory, the Morgan Stanley Business Conditions Index (a survey of our industry analysts) fell to its lowest level since April of 2020, and margin expectations look overly optimistic for the balance of '22 given the myriad of cost pressures companies face…

Happy Tax Day (said nobody ever) … for those waiting ‘til the last minute,