Good morning … US equity futures fall a touch after best month since 2020 (CNBC) as yields up a bit as investors weigh recession, hikes and payrolls (CNBC).

30yy, DAILY where one can see yields having gone from oversold to overbought (as per JPM)

… here is a snapshot OF USTs as of 728a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are slightly cheaper and weakening on the wings, the DXY trickling lower, while EU equities (DAX +0.4%) are outperforming their US peers despite contraction in major EU PMIs confirmed this morning. Chinese manufacturing PMI prints on Sunday also showed a return to contractionary territory, against consensus expectations. Our UST trader in Tokyo noted that treasuries are struggling on light volumes (105% 30d ave) some social selling flows in long-end by RM dominating steepening px-action. Here at 7am, we see SPX futures -9.5pts, the energy complex weaker (CL -1.5%, NG -2.6%, BCOMAG -1.6%), while US real rates are slightly higher vs breakevens. UK Gilts are underperforming EGBs (5y UK +4.5bps) after the UK manfg PMI broke the contraction-mold earlier, printing 52.1.

… and for some MORE of the news you can use » IGMs Press Picks for today (1 July) to help weed thru the noise (some of which can be found over here at Finviz).

In as far as what may be on Global Wall Street’s mind as they head back from the <Hamptons / Jersey Shore — pick one IF, in fact, they are heading back on this dreary East Coast Monday morning>, in addition TO a few weekly OBSERVATIONS HERE,

In US rates we recommend positioning for the risk of negative growth surprises by overweighting the intermediate sector … This week the key piece of data is the US employment report (Fri); we expect July nonfarm payroll growth to fade to 275k (consensus: 250k). Elsewhere slowing growth should be reflected in PMI releases (Japan, Canada, Scandies, Mexico, South Africa, Czechia, Poland). But still-rising inflation should lead to 50bp hikes from the RBA (Tue), BCB (Wed) and BoE (Thu). The latter needs to show resolution on inflation or it could lose control of the narrative … The equity rally is unsettling, and investors should fade it. Financial conditions are still loose and US core CPI is yet to fall substantially, so it feels optimistic to believe the Fed can soon reverse course. Markets are buoyed by falling yields but could be brought back down to earth if activity slows further as the cost of living crisis bites, said Emmanuel Cau and colleagues. European Equity Strategy: Equity Market Review - Painful rally amid ambiguous Fed and mixed earnings, 29 Jul 2022

One of Global Wall Streets favorite analysts, DBs Jim Reid starts the day, week and month off with this (and the reference TO Friday’s CoTD caught my attention),

… welcome to August and a spectacular start to H2 for markets with the S&P 500 in July (+9.1%) seeing its best month since November 2020 and 10yr US Treasuries (-37bps and +1.7%) seeing their best performance since March 2020. This follows the worst H1 since 1962 and 1788 respectively. A stunning comeback for 60/40, 50/50 or whatever ratio you chose to allocate. See our monthly performance review, out soon after this mail, for all the details.

It's a complicated outlook at the moment as we don't think the US is in a typical recession yet but will almost certainly be within a few quarters. That delay is supportive for markets relative to what was priced a few weeks ago but it's hard to say the outlook is positive. However the market has more rallied on lower expected terminal rates and the move to price rate cut probabilities within 6 months. We don't think either will come to pass but my rates colleague Francis Yared always tells me not to fight bullish fixed income markets in the summer. Indeed the CoTD on Friday (link here) showed that August is by far and away the best month of the year for bonds.

WHY is August so good for USTs?

… Well the most rational response is that supply grinds to a halt, especially in corporates and thus leaving investors parking cash in Treasuries while they wait for issuance. This trend pre-dated the post GFC era but arguably in an era of QE this could have exacerbated the issue as the seasonal drop in QE was less than that of supply. Maybe now we’re in a world without QE the impact will be less …

… Turning to the labor market, corporate commentary on net indicates easing labor shortages and tentative signs of peaking wage growth. Across the 88 Dow Jones and mid- or large-cap consumer companies that discussed the labor market, 35 companies signaled improved labor availability, compared to only 1 that saw labor shortages worsening. In fact, all three of the human resources and staffing firms that commented cited improved labor availability. While the breadth of upward wage pressures is elevated—noted by 40 of the 88 firms—10 companies signaled an easing in wage growth, compared to only 3 companies for which wage pressures are worsening. This supports our forecast that wage growth will slow over the back half of the year by 1pp to 4½%.

Progress on inflation appears more mixed. Our GS Company Price Announcement Index stopped rising for the first time in eight quarters but remains at record levels. And across the 45 transcripts that discussed output prices, 28 signaled additional price hikes later this year, compared to 8 that expected downward pressure. Similarly, our business inflation expectations composite has edged down but remains very high. Taken together, Q2 earnings season suggests incremental progress towards normalizing inflation but no sea change, consistent with our view that core inflation will lag the labor and commodity markets lower.

… Green Shoots on Disinflation? …Our quantitative summary measure of Russell 3000 earnings calls suggests stabilization but little progress. As shown in Exhibit 8, the preliminary reading of our GS Company Price Announcement Index is unchanged at a high level in Q2 after rising in each of the previous 8 quarters. However, the sheer number of “inflation” references continues to rise.

Finally from one of Global Wall Streets fan favorite stock jockeys — MSs Mike Wilson,

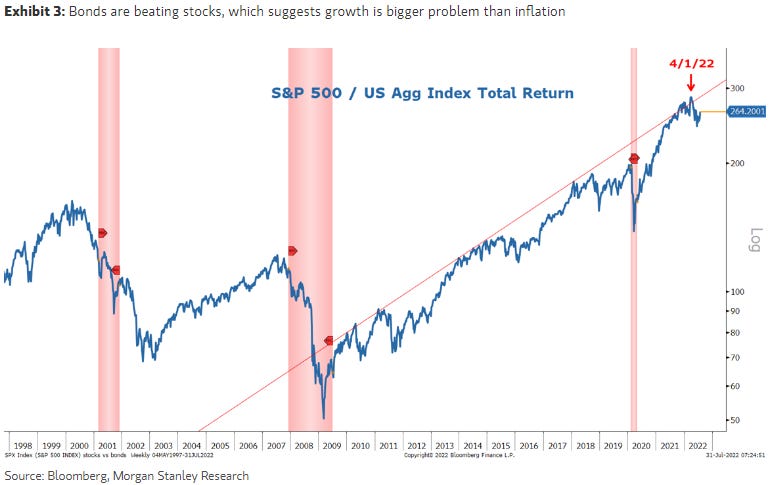

The Fed's Cred Is Back. Is That Good for Stocks? With equity markets continuing to rally last week in the face of a tighter Fed, still high inflation and generally weaker earnings/economic data, we further explore our thesis from last week as to why. Bottom line, the Fed has quickly regained its credibility and that's good for bonds, not stocks.

… since peaking in June, 10-year Treasuries have had one of their largest rallies in history, with the 10s-2s curve inverting by as much as 33bps, another historically low level. Perhaps more importantly, 10-year inflation breakevens have come down significantly, notwithstanding this past week's rally (Exhibit 1). Finally, the Fed's favorite measure of inflation expectations, Fed5Year inflation forwards, has plummeted and now sits very close to the Fed's long-term target of 2% (Exhibit 2). Objectively speaking, it appears as though the bond market has quickly turned from a vigilante to a believer the Fed will get inflation under control.

That's unequivocally bullish for bonds and one of the main reasons we turned bullish on bonds relative to stocks back in April. Since then, bonds have done better even though it's been a flat ride in absolute terms. It also explains why defensives have dominated the leadership board and why we are sticking with it.

As I only have direct/easy access to a few of the sources The Harkster does I appreciate the "WEEKLY Notes" google doc. Admittedly it is sort of a fire hose delivery, but once I get the doc into my preferred pdf reader I try to get through a few of the perspectives I don't normally find the time to hunt down, on yet another web safari into the jungles of distraction, if they register sufficient hits on the search-terms du jour within my pdf-reader. For example, the term "inflation" turned up 3 Oracles of Ancient Ephemera I usually don't have time for unless some kind person puts the link in front of me, of which, 2 of the 3 I don't have access to, out of a total of 4. So hark ye, it is useful, although hearken might have a better ring in UK ears tuned-up in the last century or two. Anyway, if I may hearken back to (not to be confused with to 'hark at', as it would not be my intention) a seemingly cryptic comment in a recent BondBeat post, I have to wonder if my system's auto-generated file name for this WEEKLY Note, "Sellsdie 073122", isn't possibly a freudian slip of sorts?

As I only have direct/easy access to a few of the sources The Harkster does I appreciate the "WEEKLY Notes" google doc. Admittedly it is sort of a fire hose delivery, but once I get the doc into my preferred pdf reader I try to get through a few of the perspectives I don't normally find the time to hunt down, on yet another web safari into the jungles of distraction, if they register sufficient hits on the search-terms du jour within my pdf-reader. For example, the term "inflation" turned up 3 Oracles of Ancient Ephemera I usually don't have time for unless some kind person puts the link in front of me, of which, 2 of the 3 I don't have access to, out of a total of 4. So hark ye, it is useful, although hearken might have a better ring in UK ears tuned-up in the last century or two. Anyway, if I may hearken back to (not to be confused with to 'hark at', as it would not be my intention) a seemingly cryptic comment in a recent BondBeat post, I have to wonder if my system's auto-generated file name for this WEEKLY Note, "Sellsdie 073122", isn't possibly a freudian slip of sorts?