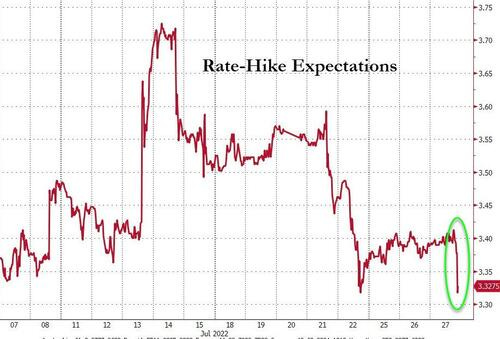

Good morning … Now we know what the Fed thinks it thinks. This all may change after today’s GDP print. Whether you believe it was a hawkish hike or a dovish presser (or both) is completely up to you. It is hard to argue the initial market reaction summarized by THIS from ZH

Markets were all relatively behaving themselves up to Fed Chair Powell's presser. The statement was shrugged off as a nothingburger but as Powell began speaking - beginning with a focus on inflation - he flipped and offered the junkie-market just the fix it needed: "likely appropriate to slow increases at some point" and any further increases will be "data dependent."

Hawkish statement... Dovish presser.

Finally, Powell said "he doesn't see US in recession", and - toeing the Biden admin line - proclaimed, that he takes the first estimate for Q2 GDP (due tomorrow) "with a grain of salt." … …

Will this help / hurt Department of Treasury’s SUPPLY PARTY (aka liquidity event) at 1pm? I can say with some amount of confidence, this mornings selloff in bonds can / may be viewed by some as a concession. Here’s a look at 7yy

Rates appear to be triangulating and are still well below ‘support’ (TLINE just above 50dMA ~3.05%) and I’ll note momentum stretched / overBOUGHT (highlighted in the RED rectangle). Again, some sort of selloff of magnitude may be viewed as an DIPportunity (see just below for more).

… here is a snapshot OF USTs as of 722a:

… HEREis what another shop says be behind the price action overnight in their morning commentary, “Debate on Definition”,

Overnight Flows As overseas investors continue to digest the Fed, we saw volumes pick up as cash traded at 132% of the 10-day moving average. 5s were the most active issue with 27%, but in keeping with the latest monetary policy revelations 2s and 10s share the role as second most active with each taking a 24% marketshare. 3 garnered 7% while 7s took a very solid 10%. 20s accounted for 1% and 30s received a 5% allocation. Flows were light but we saw some selling in the 2-year sector.

… and for some MORE of the news you can use » IGMs Press Picks for today (28 July) to help weed thru the noise (some of which can be found over here at Finviz).

A few items from the Global Wall St inbox with, yes, a couple things related to the FOMC mixed in — sorry.

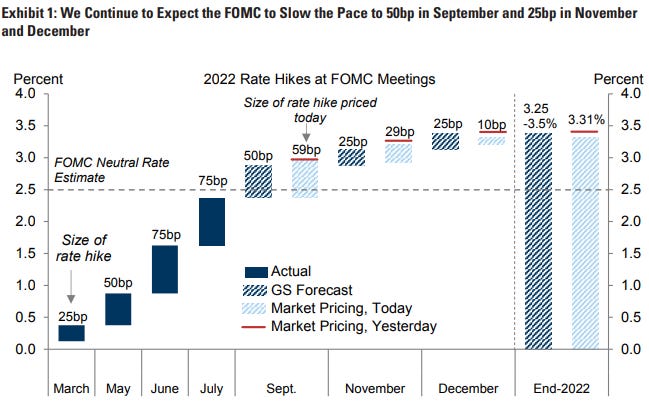

The FOMC largely held serve with the July meeting, sending a mixed bag of messages that did not materially change our views about their reaction function. We retain our view that the Fed will step down to a 50bp hike in September, concluding the hiking cycle at year-end with the target range for the funds rate at 3.25-3.5%.

… We continue to expect a 50bp rate increase in September, followed by another 50bp hike in November and a 4.1% terminal fed funds rate reached in Q1 2023. While a near-term recession could well short-circuit the Fed's tightening cycle, our baseline expects the economy to remain more resilient and inflation to be stickier than anticipated. If this proves to be correct, the market is likely underpricing the terminal fed funds rate and rate cuts in early 2023 are unlikely (see Will the Fed cut rates in early 2023? Policy rules say not so fast). In that case, the substantial easing of financial conditions that occurred in response to today's meeting will ultimately be an unwelcome development for the Fed as it seeks to achieve price stability.

… We heard five arguments for slowing the pace in Powell’s comments. First, he endorsed the message from the June dot plot, which is consistent with our 2022 funds rate forecast. Second, he noted that 75bp hikes are “unusually large” and that it will likely become appropriate to slow the pace as policy tightens. Third, he said the full effect of rate hikes has not yet been felt. Fourth, he said the FOMC would react to growth, labor market, and inflation data, in contrast to a more single-minded focus on inflation in some recent Fed commentary. Fifth, he reiterated that the FOMC aims to rebalance supply and demand through below-potential growth, not a recession.

And for something(S) NOT (directly)FOMC-related, about those (a)Durable Goods, WFC

Not As Strong As It Looks: Defense & Inflation Explain Away Durables Strength At first glance, the durable goods data suggest manufacturing continues to defy expectations for a slowdown in activity. But stripping away defense orders and adjusting for inflation suggests activity is cooling. An ugly end to the quarter for core capital goods shipments positions a weaker Q2 for equipment spending than we anticipated, but advanced data on inventories should offset some of that weakness in tomorrow's Q2 GDP report.

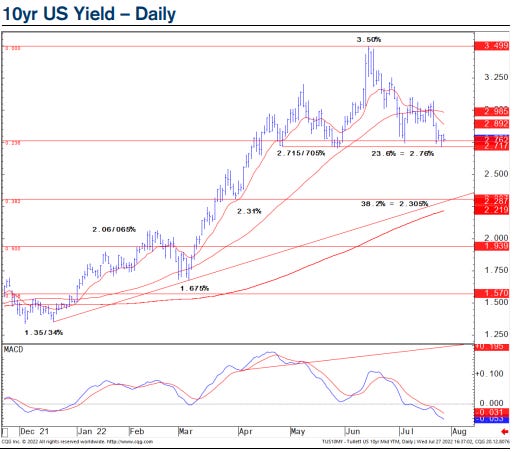

Here are a couple from the TECHNICALS and Charts Department. First, an update from 1stBOSwho will REMAIN ‘tactically bullish’ (ie long) 5s vs 2.905 (stopping out above 3.06% support), stay NEUTRAL 30s and

… We would now turn tactically bullish at support at 2.895%, with scope for an eventual move to resistance at 2.315/305%, where we would turn tactically neutral.

With some technicals in mind AND given I happen to believe EVERYTHING I read on the intertubes (I routinely get my news from FB and TWTR), I thought I’d bring forward THIS TWEET on seasonals (of TY) because in case you did NOT know, I’m a firm believer in them (seasonals, not TY)