while WE slept: all things are 'on sale' as markets continue to marinate in these Moody's Blues; "Unlikely to see forced selling of Treasuries" -BNP; updated f'casts (JPM) as narratives follow price..

Good morning … Markets are continuing to marinate in these Moody’s Blues (noted over weekend) and everything appears to be for sale … PiQ summarizes best what’s happened since Friday afternoon …

Risk off with US bonds and the Dollar pressured after Moody’s Ratings cut the United States’ sovereign credit rating down one notch to Aa1 from Aaa on Friday, citing the growing burden of financing the federal government’s budget deficit and debt. (Newswires)

… see below for link and I’d add TO the above that not only is risk OFF but bonds are NOT … repeat NOT … acting as one might think (and which it did in previous episodes) and bonds are also being sold off, too…

Given the lack of safety valve and the DV01 move here / now, lets have a look at long bonds back UP ABOVE psychologically important round number of 5.00% …

30yy DAILY: romancing levels here above 5.00% that aren’t completely without precedent …

… momentum becoming overSOLD (rent-to-own?) but TIMING, is as always, the issue …

… and while Moody’s stealing all the oxygen from the room, the next item on the docket pushing bonds around will be the funding / tax bill … WATCHING and ready / willing / able to redraw TLINEs if / when necessary but for now … back TO … the Moody’s Blues …Here are some more resources and SPIN if you wish …

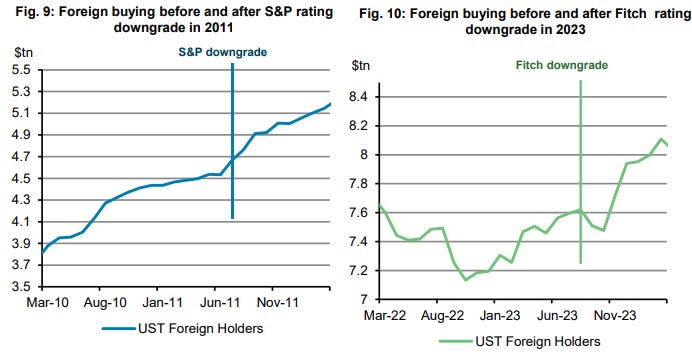

… Cooler heads soon prevailed as the 2011 downgrade left the US Split-Rated AAA (Moody's Aaa, Fitch AAA, S&P AA+). So, the US was still an AAA country and not in violation of these contracts.

The shot across the bow was heard/seen. It was only a matter of time before the US lost its AAA status. So, in the years after 2011, those contracts were rewritten from "AAA securities" to "government securities," thereby excluding the credit rating qualification.

That’s why, in August 2023, when Fitch downgraded the US to AA+, and the US became a split-rated AA+ country (S&P and Fitch AA+, Moody's Aaa), officially losing its AAA status, it had almost no effect on the bond market. No one was forced to do anything…

… The MESSAGE of Moody's downgrade matters, and matters a lot. The US fiscal situation has become untenable. But did we really need Moody’s to tell us this? It was hardly a secret.

That said, the ACT of downgrading the US will not force anyone to do anything. No one will have a forced liquidation like the worry when a company/country loses its investment grade rating. Besides, the US was already split-rated AA+ due to the previous S&P (2011) and Fitch (2023) downgrades. So Moody’s downgrade changed nothing; they just aligned with S&P and Fitch.

May 18, 2025, 9:32 AM Discipline Funds: Three Things – Downgrading the Weekend

… But back to downgrade – does it matter? I would say 100% no. It might cause a market reaction, but again, we’ve seen this before. S&P downgraded the USA In 2011 and they had egg on their face just a year later. Fitch downgraded US government debt in August of 2023 and rates are largely unchanged since then. It was at least a little different in 2011 when the change from AAA impacted some derivatives contracts that could only be tied to AAA debts, but the USA hasn’t been a AAA entity according to the other agencies for a long time now so I don’t see the impact here.

Of course, if you’re making an inflation argument that’s a very different (and more valid) perspective. Then again, if you were going to downgrade US government debt based on inflation risk the time to be doing that was during Covid, not after inflation has come down to 2.5% and appears to be softening broadly. So, this just looks like a big nothingburger to me…

… AND I’ll quit while I’m behind and continue to let these markets and their Moody’s Blues marinate but first … here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Moody start to the week in sell-America trade after US AAA rating stripped; ES -1.2% … USTs have started the week on the backfoot as the complex reacts to Moody’s cutting the US by one notch, joining S&P (cut August 2011) and Fitch (cut in 2023, after covid), with an AA1 rating. A cut which sparked on Sunday a sell-US trade. The announcement by Moody’s came amid US House Republicans blocking the passage of the Republican tax/spending bill due to concern that it would lift the short-run deficit. USTs themselves at the bottom of a 109-23 to 110-08 band, slipping from Friday’s 110-10+ close. Ahead, the US session is dominated by Fed speak, featuring Bostic, Williams, Logan and Kashkari.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

A couple notes on Chinese data from ‘across the pond’ …

19 May 2025 Barclays: China: De-escalation brings some relief

While the trade détente lifted asset markets and the export outlook, it reduces the urgency for new stimulus and the tariff trajectory remains uncertain. Our pulse checks point to a weaker property sector, softer consumer sentiment as job market pain persists, and higher SOE investment.

April retail sales and investment data below expectations, indicating weak domestic demand. Slow, but still solid, IP growth on resilient exports in April. While the tariff rollback has improved the export outlook, we maintain our 4% growth forecast for 2025 on weak domestic demand.

France weighs on on downgrade, China data AND thinkin’ tactically of curve flatteners BUT …

19 May 2025 BNP US: Downgrade is another step towards unpredictability

KEY MESSAGES

US debt has not been unanimously AAA-rated since 2011, and the fiscal and structural drivers of Friday’s Moody’s action were well known.

Ongoing tariff uncertainty means elevated risk of a recession in the US. If a recession occurred, we think that concerns about debt sustainability would mean a less robust countercyclical fiscal response than observed in prior business cycles. This would mean a longer and deeper recession, with a larger monetary policy response.

An increase in concern about the high level of US public debt would raise the stakes in debates over monetary policy independence, especially given the US’ post-World War II experience with resolving high levels of debt with inflation.

For US Treasury yields, the meaningful driver will be the headlines around deficits from the current tax bill, as opposed to the ratings downgrade. We expect a stable dollar deficit path, and a contractionary impulse to emerge from net fiscal spending, supporting curve flattening.

…US rates: The tax bill - a crucial checkpoint for USTs Ratings downgrade Fig. 7: UST30y after last 2 ratings downgrades* is fuel to the already lit fire in the Treasury market: The rationale behind the sovereign rating downgrade by Moody’s is unlikely to surprise any US Treasury investor. If anything, it is likely to fuel an already lit fire. Concerns around fiscal sustainability, riskfree status, and hedging properties of Treasuries are already rife, and the ratings downgrade will only feed the narrative.

A significant consensus has formed among investors that the US’ fiscal problems will keep long-term Treasury yields going higher, steepening the yield curve. Curve steepeners are a strong consensus trade. And the latest news, while not surprising information, could embolden investors to add even more to the popular view, adding a risk to our current 2s10s bull flattener suggestion.

Looking at the last two rating agency downgrades – S&P downgrade in 2011, and Fitch downgrade in 2023 – the market reaction in yields were the opposite. Back in 2011 the ratings downgrade drove “flight to quality” bull flattening into Treasuries, whereas the 2023 Fitch downgrade – amid a stronger economy – drove bear steepening (see Fig. 7).

We expect the 2023 template to apply in the current times. Interestingly, and unsurprisingly, the immediate reaction on swap spreads was tightening on both occasions (see Fig. 8), and we expect tighter spreads in the long-end.

Possible silver lining from the downgrade: Will Congress turn bond vigilant too? We have noted for some time that the administration has shown a significant amount of bond (market) vigilance, in a bid to keep bond vigilantes at bay. The most notable example being the 90-day pause in tariffs that was announced in response to the “tariff tantrum” in the Treasury market in the week after Liberation day (7-9 April).

Recent focus in the US Treasury market has turned from tariff policy to the tax-bill currently being negotiated among Republican Congress members. We think the Treasury markets are unlikely to react as much to the Moody’s downgrade as much to the headlines around the tax-bill and ensuing fiscal deficits.

While members of Congress may normally not be as reflexive to the deficit concerns in the bond market, we could see the Moody’s ratings downgrade spotlight the deficits issue, and the bond market (interest rates) headlines around it.

As a result, lawmakers could start treating the bond market as a scorecard for their negotiations – and become more bond vigilant, like the administration.

Given these fiscal concerns, we think the ultimate outcome from the tax bill, coupled with increased revenues from tariffs would mean that deficits will stay stable in the coming years in dollar terms (around ~1.8 trillion), and will provide slightly contractionary impulse to growth in the economy.

If our views on a bond vigilant Congress and deficit trajectory realizes, we think the yield curve is likely to flatten, albeit with the risk of curve steepening in a knee jerk reaction to the Moody’s news.

US rates: Unlikely to see forced selling of Treasuries Don’t expect forced Treasury selling from the ratings downgrade: One question investors will be asking is whether a downgrade below AAA for US Treasuries will drive some investors to be forced to sell Treasuries. We think this is unlikely to be the case.

Feedback from investors over this issue has revealed that most investors prepared for future ratings downgrades in the aftermath of the 2011 S&P downgrade itself.

Most domestically domiciled investors either limited a reliance on AAA ratings, or simply made a special carve out for US treasuries in their internal mandates – insulating the risk of forced selling into another such downgrade…

…Foreign buying data suggests low concern for Treasuries: Unsurprisingly, then, the latest Treasury International capital data (updated up to March 2025) shows that foreigners continued to be net buyers of US Treasuries after the last two rating downgrade events in 2011 and 2023 (see Fig. 9 and 10).

…Margin of error has compressed, opening the door open to a Liz Truss moment: While our base case is that Congress turns bond vigilant, and deficits stabilize in dollar terms, and provide a contractionary growth impulse – we understand perception can be reality in markets. The bond market is in a delicate state, and the risk of a Liz Truss moment – something we explored in our Grey Swans piece earlier in 2025, is a non-trivial possibility in current conditions.

The tax bill currently being discussed by Congress is a crucial checkpoint – and possibly an inflection point for the US Treasury market.

19 May 2025 BNP China: Modest slowdown likely in Q2 despite tariff relief

Latest data suggest China’s GDP growth is likely to have slightly moderated in April from the 5.4% y/y official reading for Q1.

However, with GDP growth likely holding up above the 5% growth target and the latest reduction in US tariffs, authorities may feel less urgency to make growth-supporting measures in Q2, in our view.

We expect a more muted policy response, combined with the likely further cooling of the property market and the lingering hit from tariffs, to keep China’s Q2 growth on a downward trend.

In FX, we continue to see room for USD weakness and expect carry trades to do well in the coming months.

In US rates, stable foreign demand suggests a tactical curve flattening opportunity, but we favour long 2y swap spreads due to T-bill paydowns and normalised dealer balance sheets.

In EUR rates, we believe that a structural steepening bias will reassert itself ultimately, but we would look for a more favourable entry point.

… US rates: After the volatility surrounding ‘Liberation Day’, short-end UST yields have returned to levels seen in March, but longer-end yields are 20–30bp higher. A steeper curve appears to reflect the risks of wider budget deficits amid tax cut discussions, and perceived risk of foreign UST selling. The perception around foreign selling appears to be just that – perception. Treasury auction demand, the Fed’s custody holdings and – most recently – data from Japan show no dent in foreign demand since Liberation Day. Before investors could appreciate the stability of foreign demand, markets turned their focus to the deficit impact of the 2017 tax cuts, driving even more curve steepening. Given the bond-vigilant administration, we see a tactical curve flattening opportunity here – we like a 3m2y A-2.5bp vs 3m10y ATMF conditional bull flattener. Separately, we also favour long 2y swap spreads based on three emerging tailwinds: continued T-bill paydowns after moving the debt ceiling X-date forecast to early September, normalised dealer balance sheet capacity utilisation and the potential for increased bank balance sheet capacity stemming from SLR relief.

Fig. 3: Tactical flattening with a return to pre-Liberation Day levels\

…. one of Germany’s BEST(s) on markets (an early morning REID) as well as downgrade …

19 May 2025 DB: On the US Moody's downgrade George Saravelos

We wrote in a special report last week that US fiscal risks are rising sharply. The key problem is that the market has over the last two months structurally re-assessed its willingness to fund US twin deficits. We demonstrated how America's net external asset position is the best metric to measure fiscal space and this is on a rapidly deteriorating path. To be sure, as Treasury Bessent argued over the weekend, the Moody's rating agency downgrade is a lagging indicator of fiscal health. But the key problem for the US is that both the bond and currency market have been insufficiently pricing in fiscal risks in the first place.

The US has an additional problem: whatever the Republican Congress decides to do with fiscal policy over the next few weeks, it will most likely be "locked in" for the remainder of the decade. The very difficult reconciliation process and the potential loss of a Republican majority in the mid-terms essentially leaves space for only one major fiscal event during the current Trump administration. Once this concludes, there will be very little that can be done to change the fiscal trajectory for the foreseeable future. This is different to many European countries which were able to pivot fiscal policy quickly (within days, during Lizz Truss' premiership) in the event of market pressure.

The combination of diminished appetite to buy US assets and the rigidity of a US fiscal process that locks in very high deficits is what is making the market very nervous.

How to think about the bond - FX relationship in this environment? A dollar fiscal frown is the best way to picture things. At one extreme on the left is a fiscal stance that is too easy. This leads to a combined drop in US bonds and the dollar - as we are once again witnessing this morning. The persistence of this pattern would be a clear signal the market is losing its appetite to fund America's deficits and rising financial stability risks. At the other extreme on the right of the frown is a fiscal stance that tightens too quickly, closing the deficit sharply but forcing the US into a recession and a deep Fed easing cycle. In this more conventional world, the dollar drops and bond yields rally at the same time.

Will market pressure impact current US budget negotiations? Which part of the dollar frown will we end up in? The US Congress will decide over the next few days.

…Its likely that fiscal developments in Washington will take centre stage with the House expected to vote on its reconciliation package this week just as Moody's removed the US's last remaining triple-A rating late on Friday night. As our economists discussed last week (see "Tax bill details suggest still-elevated deficits in the near term'), though the specific components of additional tax cuts on top of the TCJA extension differed from what they had previously outlined (see "US outlook: Tariff-struck"), the JCT score of the Ways and Means mark-up was largely in line with our top-line deficit assumptions. Assuming House Republicans are able to resolve their outstanding policy disagreements and vote on the tax package this week, the Senate will then start to mark up the bill, where even more policy disagreements await. On thing stands out though, and that is that at this stage there are no signs of any serious deficit restraint.

On that topic, Moody's cut the US credit rating on Friday night from Aaa to Aa1 (stable outlook). This is a major symbolic move as Moody's were the last of the major rating agencies to have the US at the top rating. Moody's have had them on watch since November 2023 and if there is going to be a change then it tends to happen within 12-18 months so this news shouldn't have been unexpected. Remember S&P was the first to downgrade the US from AAA back in August 2011 which brought a brief market panic at the time. The S&P 500 fell -6.7% on August 8th (the Monday after the cut) while Treasuries actually rallied 20bps on a flight to quality bid. A slightly different reaction this time given they are "only" playing catch-up on one hand, but with debt sustainability now more of a concern on the other. 10yr USTs spiked +4bps in very late trading on Friday on the news. This morning 10 and 30yr USTs are another +3.8bps and +5.2bps higher, respectively, with the latter now at 5% again and +10bps higher than just before the announcement late on Friday. If we stay at these levels this would be a higher yield than that seen at the worst close after Liberation Day. In fact it's only just over 10bps below the highest point in 2023 when inflation concerns were still bubbling. Prior to that you'd have to go back to 2007 to see 30yr yields higher than current levels.

S&P 500 (-1.0%) and NASDAQ (-1.27%) futures are also weaker on the news along with the Dollar (-0.26%). Mixed China data isn't helping the general Asia mood with Retail Sales growth slowing to +5.1% y/y in April, falling short of Bloomberg's forecast of +5.8% and down from +5.9% in the previous month. Fixed-asset investment for the first four months of this year increased by +4.0%, slightly below the anticipated +4.2%. The real estate sector continues to exert downward pressure on fixed asset investment, with a year-on-year decline of -10.3% as of April. Nevertheless, industrial production has exceeded expectations, growing by +6.1% y/y in April, compared to the expected +5.7%, although this represents a slowdown from the +7.7% increase recorded last month…

… a note on China from Netherlands …

19 May 2025 ING: China April slowdown shows the impact of economic uncertainty

Trade war uncertainty is denting Chinese confidence, resulting in slower economic activity in April. Retail sales and fixed-asset investment both underperformed forecasts amid heightened caution. Yet the impact on manufacturing was less than feared.

…and in the case one needed reminder that NARRATIVES (not unlike all of these we all pay so much attention to and hold in such high regards) FOLLOWS PRICE … an upwardly revised yield f’cast after getting stopped outta 2yr longs (another traded out bull) …

…Governments Following the de-escalation in the trade war with China, we revised our Fed call and adjusted higher our Treasury yield forecast;we see 10-year yields reaching 4.35% by year-end, up from 4.00% previously. We remain neutral on duration but hold 2s/5s steepeners. We expect minimal impact on yields if the reconciliation bill is passed. The deficit impact is estimated to be small relative to the $21tn of projected deficits in the current law baseline. Meanwhile, the 5s/30s curve has already steepened dramatically versus fundamentals, and the technical backdrop appears more benign. TIC data showed foreign investors bought $123bn Treasuries in March, the most since August 2022. We revise higher our breakeven forecasts across the curve to 225bp by year-end. Maintain 10Yx20Y inflation swap longs given attractive valuations…

…Treasuries Fiscal policy takes center stage

Treasury yields rose sharply following a de-escalation in the trade war with China but retreated from their highs later in the week, as economic data softened. Given the tariff news, we have revised our Fed call to look for later and shallower Fed easing...

...accordingly, we have also revised our Treasury yield forecasts over coming quarters. We now see 2- and 10-year yields ending the year at 3.50% and 4.35%, respectively, up from 3.10% and 4.00%, previously

With markets priced for a Fed path close to our revised forecast and near-term risks two-sided, we remain neutral on duration but hold 2s/5s curve steepeners

We review the implications of the reconciliation bill making its way through Congress. Recognizing the uncertainties with respect to the final details of the bill as well as the timing, we think that risks are skewing toward modestly larger near-term deficits and a more positive fiscal impulse on GDP in FY26 than we previously assumed

However, if passed, we expect a minimal impact on yields. The estimated $3.3tn increase over 10 years is likely not far from market expectations and is still relatively small versus $21tn of projected deficits CBO current law baseline...

...Meanwhile, the 5s/30s curve has steepened dramatically versus fundamentals in recent months, and the technical backdrop appears more benign than in early April, with investor positioning cleaner and market liquidity more robust

After the market close, Moody’s downgraded U.S. debt from Aaa to Aa1. We estimate a one-notch downgrade from Moody’s should narrow 30y swap spreads by roughly 5bp, all else equal, though Treasuries already seem to display a higher risk premium than other similarly-rated DM sovereigns

TIC data show foreign investors purchased $123bn of long-term Treasuries in March, the most since August 2022. Geographically, demand emanated from Europe and the Cayman Islands. Looking ahead, we expect foreign demand for Treasuries is likely to remain weak over coming months

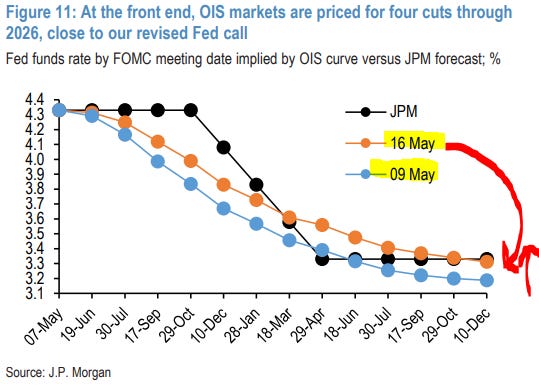

…Looking ahead, given the significant de-escalation in the trade war with China, we now project real GDP growth for this year at 0.6% (4Q/4Q), up from 0.2% previously, core PCE inflation ending the year at 3.5%, down from 4.0% previously, and a first Fed cut in December, versus September previously. After December, we see a further three sequential cuts, taking the funds rate target range to 3.25-3.5% by 2Q26 (see An update on the economic outlook, Michael Feroli, 5/13/25). Indeed, markets have repriced quickly on the back of the tariff reductions, with the OIS curve now implying only slightly more than four cuts through end of next year — not far from our revised Fed call (Figure 11)…

Against this backdrop, we revised up our Treasury yield forecasts earlier this week, and we now see 2-year Treasury yields ending the year at 3.50%, versus 3.10% previously (Figure 12). Further out the curve, we still assume term premium is likely to remain elevated and now see less room for long-run inflation expectations to fall. As we noted last week, though 10-year yields appear roughly 26bp too high versus our fundamental model, controlling for Fed, growth, and inflation expectations, as well as Fed guidance and the size of the SOMA, we think the ratcheting up of tariffs since late March justifies a more permanent discount in long-term Treasuries (see Treasuries, US Fixed Income Markets Weekly, 5/9/25). Thus, we now forecast 10-year yields will end the year at 4.35%, up from 4.00% previously…

…Given the shift in fundamental outlook as well as lingering risks, we stopped out of 2-year duration longs earlier this week and turned neutral on duration (see US Treasury Market Daily, 5/12/25). That said, we maintain 2s/5s curve steepeners — we think this exposure offers asymmetric upside in the current environment, as the curve is likely to steepen sharply in the event that a deterioration in labor market data over coming months drives market expectations of deeper rate cuts.

…Technical Analysis …Figure 23: The 2-year note bounces from the 4.04-4.15% medium-term support zone. Key short-term resistance now rests at 4.83-4.89%, which had been support heading into the US-China summit weekend. We still see the possibility that the market bullishly rebases ahead of the 4.04-4.15% support zone, but the shift in trade policy and the equity market's response to that outcome risk a further hawkish repricing and at least limit the rally potential over the near-term.

…Figure 26: The 30-year bond backup finds initial support near the 4.99-5.045% support cluster. A release cheaper would risk a backup to the next support levels at 5.18% Oct 2023 cycle cheap, then 5.32% AprMay equal swings objective and 5.41% Sep 2024-Apr 2025 equal swings objective. Short-term resistance rests at the 4.75% May 7 yield low and 4.71% 50-day moving average.

… this next couple / few notes is from an excellent US based shop and set of stratEgerists where one is from head stock jockey in chief, another is some economic ‘notes from the road’ and finally, a few thoughts from Sunday where they attempt to define ‘detente’ …

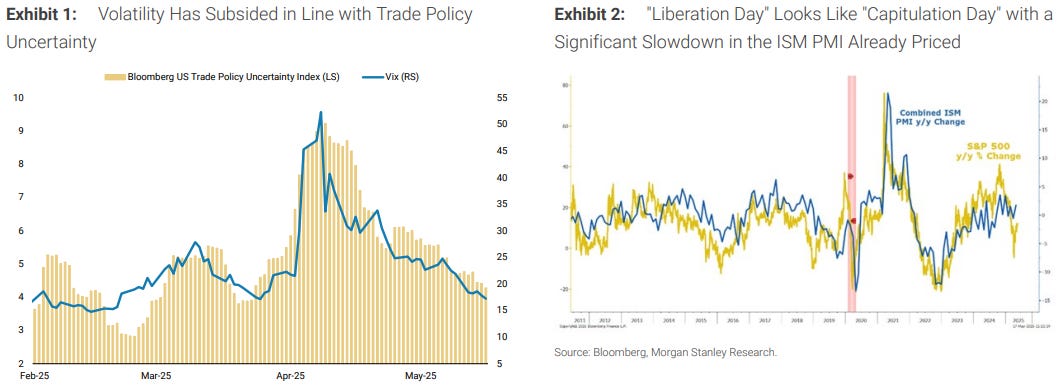

May 19, 2025 MS: Weekly Warm-up: Volatility Subsides Along with Trade Policy Uncertainty Michael J Wilson

We've checked one item off our list for a more durable rally—a trade deal with China. Upside progress through 6100 in the near term is dependent on a continued reacceleration in earnings revisions breadth as interest rate relief remains elusive for now.

Volatility Subsides Along with Trade Policy Uncertainty...

Earnings Revisions Breadth Continues to Reaccelerate...

The Main Risk Shifts from Growth to Rates...The 10-year yield has continued to hover around 4.50%, which has been an important level for equity market valuation over the last 2 years. Our work shows that initial upside breaks through this level have tended to coincide with modest valuation compression. Further, the equity return/bond yield correlation is right around 0, having declined from the early April highs of 0.6. In other words, rate sensitivity is on the verge of increasing for stocks. On the monetary policy front, our economists don't see the Fed cutting rates this year. Thus, the burden is on rebounding EPS revisions to push the rally beyond 6100 short-term as rate relief appears less likely at both the front-end and back-end of the curve.

… Exhibit 1 illustrates that equity market volatility has subsided considerably amid the decline in trade policy uncertainty. Both of these measures peaked well before the deal with China came together and are now back below where they were pre-Liberation Day. These indicators suggest that trade headwinds have likely peaked in rate of change terms. This would fit with the capitulatory price action we saw in early April, and the fact that the average stock in the S&P 500 has already experienced a ~30% drawdown this year. Thus, while lagging hard data is likely to come in softer over the coming months, the equity market likely priced it in April. In the event a recession still arrives (our bear case), we think the April lows will hold assuming it's a mild one with manageable risk to credit/ funding markets. Bottom line, we check off the first item on our list of catalysts for a more durable rally—a trade deal with China.

…With recession odds reduced as discussed previously, we think the primary near-term risk for equities is tied to back-end rates. The 10-year yield has continued to hover around 4.50%, which has been an important level for equity market valuation over the last 2 years. As Exhibit 10 illustrates, initial upside breaks through this yield threshold have tended to coincide with valuation compression. The fact that this is an important spot for bond yields from an equity market standpoint is also reflected in Exhibit 11 , which shows that the equity return/bond yield correlation is right around 0%, having declined from the early April highs of 0.6. In other words, rate sensitivity is on the verge of increasing for stocks (i.e., a negative correlation in this relationship). In our view, a breakout of the 10- year yield above 4.50% would take this correlation negative, and drive more rate sensitivity for equities. Moody's late-day downgrade of the US credit rating last Friday is also worth considering in this conversation, though Moody's is the last ratings agency to downgrade the US credit rating, a process that began 14 years ago in the summer of 2011. In short, a break above 4.50% in the 10-year yield can lead to modest valuation compression (5% compression is around what we've gotten in prior historical analogs)— we would be buyers of such a dip.

May 19, 2025 MS: The Weekly Worldview: Notes from the road Seth B Carpenter

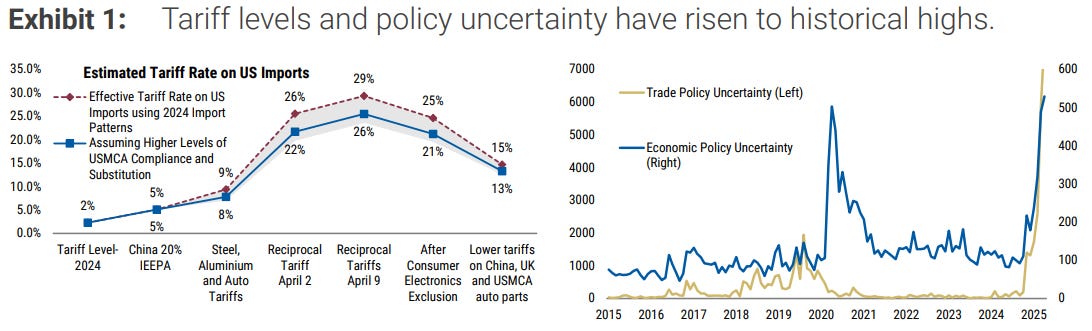

… When I am asked, “what is the objective of the tariffs?” I have no concrete answer, but as a forecaster, the answer should drive plausible scenarios. The candidates include raising revenue, eliminating trade deficits, eliminating foreign tariffs, and negotiating topics beyond trade. We have made a baseline assumption that tariffs on China will be treated differently than tariffs on the rest of the world. We assume they will be higher and more persistent, while for the rest of the world, they will be more easily adjusted. We could always be wrong, and have to change as news comes in.

The most recent de-escalation prompts the question of how much recession risks have fallen. The probability has surely fallen some at the margin, but we never had a recession as a baseline, partly because we assumed the peak announced tariff rates would not last. Recession risk is not gone, however, because tariffs have both direct effects and indirect effects. Even with lower tariffs, the direct drag even is still meaningful. The data show that the tariffs on China in the first Trump Administration were followed by a drop in industrial production and manufacturing employment. Tariffs are taxes, and 2/3 of imports from China are capital goods or intermediate inputs. So tariffs on China are in effect a tax on domestic capex and manufacturing.

The indirect effect comes through uncertainty. An extensive literature in economics on decision making under uncertainty, including a famous paper by Ben Bernanke, notes that long-lived investments will likely be deferred when uncertainty is high. There is an option value to waiting when the cost-benefit is unclear. It is far from obvious that the uncertainty regarding tariffs is gone. For hiring and investment decisions, not knowing where tariffs will be—and therefore domestic demand—means that pulling the trigger on more spending is hard. The difference between a recession and not depends on how big this uncertainty effect is … and that itself is uncertain…

May 18, 2025 MS: Sunday Start | What's Next in Global Macro: The Détente – What It Does and Doesn’t Mean

Following Monday’s announcement of a 90-day pause on reciprocal tariffs between the US and China, the response in risk markets has been resoundingly positive through the first four trading days. The S&P 500 is up 4.5% from last Friday’s close, and year-to-date returns are back in the black after Liberation Day drove steep declines in April. Credit markets have also rallied notably, with investment grade spreads tightening by 11bp and high yield spreads by over 50bp. The Treasury market took out 50bp of rate cuts in 2025, leaving market-implied rate cuts by the end of 2026 at around 100bp. The pricing of the trough fed funds rate in the anticipated easing cycle moved up by about 40bp to 3.34%, which we attribute to the market assessing a lower recession probability on the back of the de-escalation announcement.

These moves across markets are significant. To put them into perspective, we dig into what the 90-day détente in trade tensions implies and what it does not, sketching out the implications for the economy and markets…

…For risk markets, we think that the détente has reduced the risk of substantial drawdowns. While policy uncertainty about the ultimate level of tariffs remains, the return of last month's mind-boggling vicissitudes driven by trade policy seems significantly out of the money now, thus curtailing the left tail of returns distributions. In other words, it is unlikely that we will see markets revisiting the lows of April in the near term. For credit markets, a lower likelihood of a recession is welcome news, especially considering the current strong credit fundamentals. With the market taking out a couple of rate cuts, all-in yields for credit remain in the range to sustain the demand from yield buyers like insurance companies.

I get the sense this next guy was ALSO saying same back in … 2011 …

A credit rating agency (it does not matter which) downgraded the US from something to something else. US President Trump’s current policies are unlikely to place the US on a sustainable debt path. Influential donor Musk’s DOGE efforts are unlikely to reduce the deficit. Market reactions should be muted—there is little new information. Administration officials attempted to frame the decision in a political context, but some comments also suggested a limited understanding of the ratings process.

China’s April economic data showed weaker retail sales but stronger-than-expected industrial production. There were slowing sales of consumer goods and autos, which is concerning. Trump’s latest tariff retreat might be used by US importers as an opportunity to buy early for Christmas. This could support China’s production data…

…There are no fewer than six Federal Reserve speakers scheduled today. Investors will give special attention to comments on fiscal policy, in the wake of the downgrade, and on the growth and inflation impact of tariffs.

The week ahead is light on economic indicators. Fed officials undoubtedly will make some headlines. They are likely to reiterate Fed Chair Jerome Powell's basic message during his May 7 presser: "We may find ourselves in the challenging scenario in which our dual-mandate goals are in tension. If that were to occur, we would consider how far the economy is from each goal, and the potentially different time horizons over which those respective gaps would be anticipated to close. For the time being, we are well positioned to wait for greater clarity before considering any adjustments to our policy stance."…

May 18, 2025 Yardeni MARKET CALL: Valuation Mojo Driving Stocks' Big Mo Rally

The meltup scenario is making a dramatic comeback. It was one of our three scenarios until March 24 when we wrote the following in our Morning Briefing: "We've decided to fold our 1990s meltup/meltdown scenario into our Roaring 2020s scenario. The current correction in the stock market suggests that the former has played out already, as the bull market's highflyers have been hit hardest by the current correction. That leaves us with two scenarios: the Roaring 2020s, to which we assign a 65% subjective probability, and a mostly stagflation scenario, with a 35% probability. The former includes the possibility of a rebound in the former highflyers, while the latter includes the possibility of a recession."

The former highflyers have certainly rebounded. On May 12, we lowered the odds of trouble to 25% raising the odds of the Roaring 2020s to 75%. But it may soon be time to consider adding a third scenario again for a another possible meltup/meltdown in the stock market.

The latest correction in the S&P 500 bottomed on April 8 and it has been a V-shaped recovery in the stock market since then. The momentum stocks have been leading the way (chart).

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Who’s buyin’ bonds, you ask … an attempted answer …

May 19, 2025 Apollo: Declining Foreign Participation in US Treasury 30-Year Auctions

Indirect bidding in Treasury auctions refers to bids submitted on behalf of foreign institutions. These bidders don’t participate directly, but instead have their bids placed by intermediaries—hence “indirect.” Looking at foreign participation in 30-year Treasury auctions shows a downward trend in recent months, see chart below.

A dot com with a VIEW … which reads like … it’s different this time … and a markets daily …

May 19, 2025 at 5:00 AM UTC Bloomberg: Moody's blues come for US sentiment It would be a mistake to be complacent about this downgrade.

… It’s also important to note the potential for the unexpected. The S&P downgrade in August 2011 following that summer’s chaotic negotiations over the fiscal cliff proved to be a critical turning point, but not in the way people feared at the time. This is what happened to the 10-year yield and to the New York Fed’s estimate of the term premium — the implicit extra yield that investors demand to take the risk of lending over long periods — before and after that downgrade:

In 2011, investors just bought Treasuries, as they were still safer than anything else. Foreign investors piled in. As it grew obvious that inflation wasn’t coming back, and demand for Treasuries was solid, low yields propped up stocks, which were cheap compared to bonds. This time is very different. Using the classic rule of thumb of comparing stocks’ earnings yield (the inverse of the price/earnings multiple) with the 10-year Treasury yield, stocks now yield less than bonds for the first time in almost 25 years. And Treasury yields are much higher than in 2011:

Covid was another turning point. Since yields hit rock bottom amid 2020’s desperate monetary easing, stocks and bonds have parted company. During the previous two decades, theyhad performed in line with each other. In recent years, the S&P 500 has surged despite rising bond yields. Can this continue?

At some point, higher bond yields bring down corporate profits through heavy interest costs, and provide a compelling alternative for investors. In 2011, S&P was the catalyst for markets to grasp that inflation was beaten (as it was until Covid), meaning great things for stocks and bonds. This time, with markets in a far more precarious place, Moody’s belated judgment could crystallize another sea change in opinion…

May 19, 2025 at 10:24 AM UTC Bloomberg Markets Daily: Moody’s Gives Fresh Impetus to Bond Vigilantes and Stock Bears The 30-year yield is jumping above 5%.

…Selling US bonds The Moody’s downgrade of the US is a powerful symbol of the ongoing deterioration of the nation’s finances, and the market reaction is a reminder that the bond vigilantes have the US in their crosshairs.

Bond investors are selling longer-dated bonds, pushing the yield on the 30-year above 5% to the highest since November 2023. The impact spilled over to other asset classes too, sending US equity-index futures lower and a gauge of the dollar sliding 0.5%, a reminder of the “Sell America” trade that exploded last month.

These vigilantes have the power to curb fiscal profligacy by selling their bond holdings en masse, driving up borrowing costs and volatility to such an extent that the government must relent. Investors are on edge over tax cuts looming in Washington’s latest spending plan without sufficient offsetting cost cuts or revenue to pay for them.

While markets have calmed down since the tumult that followed Trump’s aggressive trade policies unveiled on April 2, that stabilization feels brittle. It all points to bond yields remaining “higher and more volatile” than some investors currently expect, said Michael Arone, chief investment strategist at State Street Global Advisors. —Michael Mackenzie and Alice Gledhill …

… a few (equity)charts to consider, this mornings futures move lower notwithstanding …

19 MAY 2025 Hedgopia: Options Reflecting Heightened Optimism, Although Not Dangerously So Quite Yet

The rally since early-April lows has equity bulls aggressively expressing their sentiment in options, which, should the current trajectory persist, will have potentially reached a dangerous level soon.

Optimism is in the air. Equity longs are expressing this in the options market, aggressively so in the most recent sessions.

In three of the five sessions last week, the CBOE equity-only put-to-call ratio registered readings of sub-0.50, with Wednesday’s 0.412 the lowest since July 2023. The 21-day average finished Friday at 0.52, which is low enough to begin unwinding; that said, several times in the past, the average has continued lower toward the high-0.40s before sentiment goes the other way (Chart 1).

Optimism has paid off for the bulls – big time. Since 7 April when the S&P 500 bottomed at 4835, it has rallied 23.2 percent to 5958. Prior to this, from the all-time high of 6147 posted on 19 February, the large cap index quickly gave back 21.3 percent.

At the April low, bulls defended dual support, made up of a rising trendline from March 2020 and horizontal support going back to December 2021-January 2022 at 4800 (Chart 2). The move since the April low has been fierce – up in 16 of the last 19 sessions.

The index is now 3.2 percent from the February record, which probably acts as a magnet in the sessions to come. Momentum is strong, with the daily RSI (69.76) just under 70 and the weekly at 56.93; if, however, the weekly stalls around here, that would represent persistent lower highs in this metric since last July, and that would be a yellow flag…

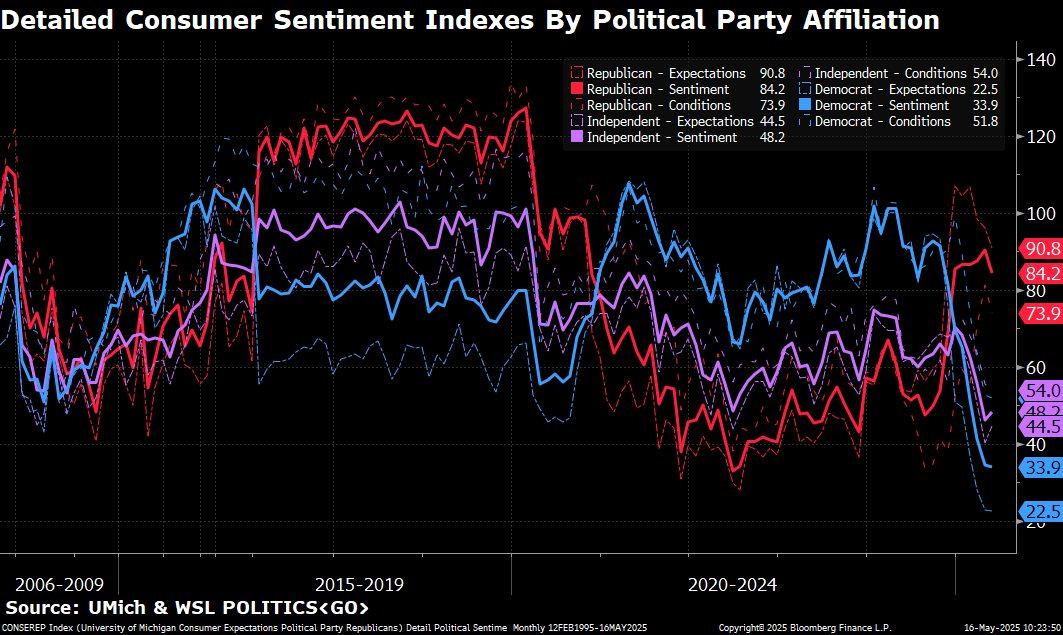

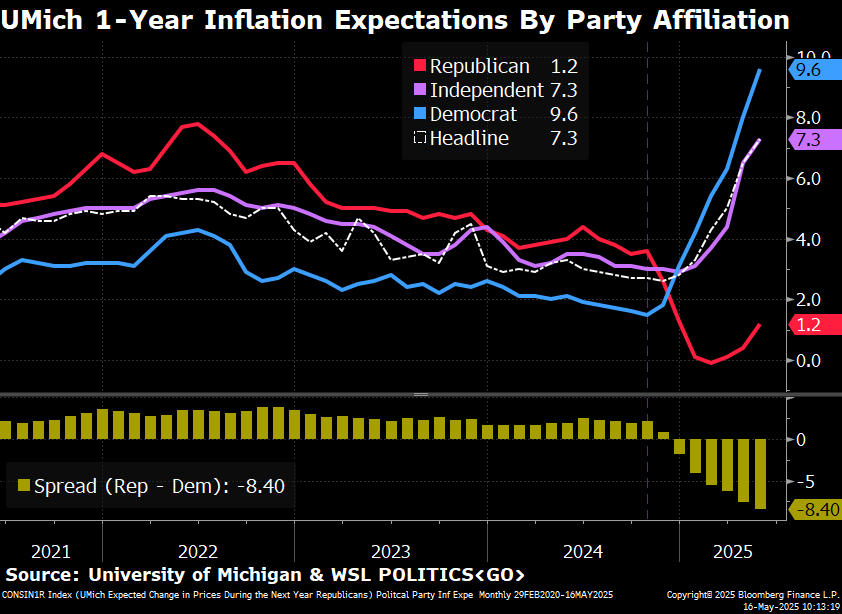

This next weekend note is, as always, a great read through of conditions and markets / economics temps out there with LOTS of ‘eye candy’ … including how very political (and so, USELESS) UoMISSagain sentiment data has become …

May 18, 2025 TKer by Sam Ro: Remembering moments when I thought things took a permanent turn for the worse

… Consumer sentiment is tumbling. From the University of Michigan’s May Surveys of Consumers: “Sentiment is now down almost 30% since January 2025. Slight increases in sentiment this month for independents were offset by a 7% decline among Republicans. While most index components were little changed, current assessments of personal finances sank nearly 10% on the basis of weakening incomes. Tariffs were spontaneously mentioned by nearly three-quarters of consumers, up from almost 60% in April; uncertainty over trade policy continues to dominate consumers’ thinking about the economy.“

going down")

Excellent write up!

Great day...

Your commentary yesterday was

right on the money...

Thanks...