Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP a ‘programming note’ … I will be travelling in the week just ahead and there will be NO daily drivel / spammation after Monday. I will have little to no access to the intertubes and this ‘Stack. I HOPE to be back into the spammation biz by the weekend. I’ll ask your patience and remind you before reachin’ out for a reFUNd, that while freedom isn’t free, this ‘Stack IS :) …

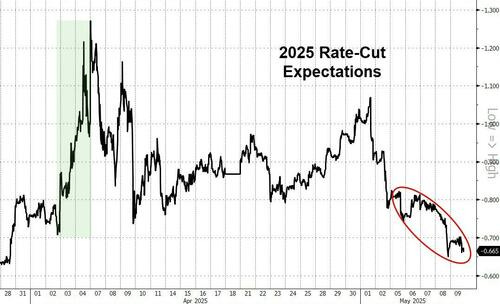

I’ll jump right in and begin with a look at the belly — 5s — in this case — on a daily and then on a weekly basis …

5yy DAILY: support up nearer 4.10% …

… and as we romance levels just above 4.00% with an eye on support (4.10) I’d then note momentum (stochastics, bottom panel) nearing overSOLD levels and if / when we get up nearer 4.10% (?) might be more funTERtaining risk / reward setup … depending, of course, whatever is going on ‘out there’ in the world at that moment

5yy WEEKLY: support up nearer 4.10, resistance 3.50 THEN 3.10 but …

…momentum here, on bigger picture, WEEKLY context, well, just not as compelling for bigger picture traders / investors …

… In as far as the rest of this section of my weekly notes / thoughts, normally reserved for some sort of view but with Team Trump meeting with Chinese officials over the weekend, I’ll quit while I’m behind and maybe drop in tomorrow — Mothers Day — don’t mess this up, fellas — time and ‘weather’ permitting.

For now, as the day and week came to a close, ZH sums it up far better than I could …

ZH: Crypto Soars, Stocks Snore, Rate-Hawks Roar As Trade War Tension Floors

Trade policy uncertainty continued to tumble this week...

… Exactly one month after the White House's surprising decision to pause its week-old reciprocal tariffs, the S&P 500 now sits 835 points higher (+17%) than it was at its recent low seen back on April 7th (but the S&P is still below pre-Liberation Day levels - having tried and failed to breakout) ...

Goldman's Chris Hussey sums up the week:

And like we saw on Apr-9, the White House pivoted again this week in its trade policy with the UK. Markets ran higher on Thursday's news of a UK deal, reminding investors of the risk of being short in a market where the news flow can turn positive at any time even if some measure of fundamental economic policy damage remains in place (UK imports are still likely to be subject to the 10% baseline tariff).

In addition to White House policy, we also heard from the Fed this week on the back of its scheduled May meeting. And the news was uneventful. The Fed does seem to have set a higher bar for rate cuts, but that makes sense given the higher inflation impulse that the current tariff regime may set off. Indeed, Ronnie Walker and Elsie Peng raised our core PCE inflation forecast by 30bp this week as they now see a weaker dollar and shifting supply chains pressuring US inflation.

Finally, in addition to the macro news, markets received a flurry of stock-specific news as earnings season continued and investors digested news around GOOGL and AAPL. Overall, 1Q25 earnings season continues to trend very well and this week's earnings probably only added to the EPS growth outperformance. A week ago, 1Q25 S&P 500 EPS growth was trending up 12%, double what bottom-up consensus was expecting going into earnings season.

Against this backdrop, however, Peter Oppenheimer leans towards fading the rally in a Tuesday note, "Asymmetric risks." Why? The opportunity set facing markets today does not appear to be aligned with a 22.5X 2025E P/E multiple. The US still faces a 45% probability of slipping into recession this year as Jan Hatzius reiterated in a Tuesday note as well, "On the Precipice."

All of which sent rate-cut expectations (hawkishly) reeling lower...

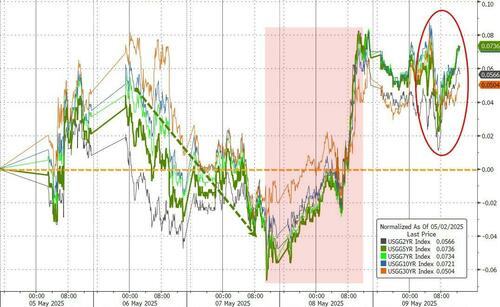

Treasury yields were all higher on the week with the belly underperforming modestly...

… Alrighty, then.

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox

Flows to show and so, you’ll be IN THE KNOW …

08 May 2025 BAML: The Flow Show Run tariffs, run tariffs, run, run, run

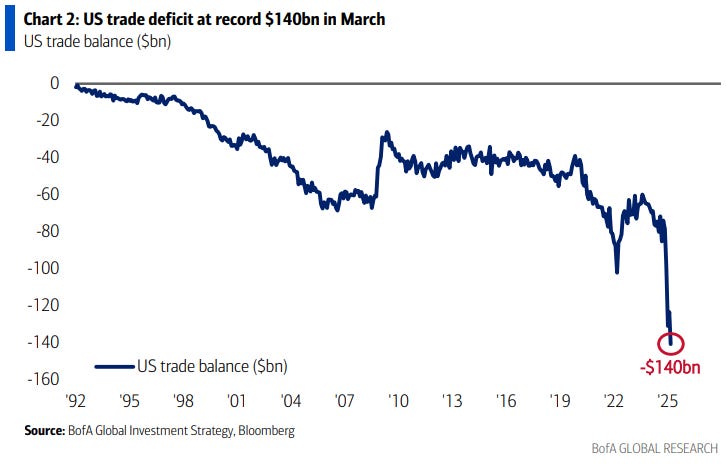

… The Biggest Picture: US trade deficit in March hit record $140bn (Chart 2 – US last ran trade surplus in 1975)…why US now protectionist; but flipside of big deficit…big $540bn foreign inflows to US assets past 5 years; if tariffs cause higher inflation/weaker US$, threatens funding of US deficits via higher bond yields; nothing reverses US macro policy more quickly than risk of >5% Treasury yields…why tariffs to fall in Q2.

… The Big Flow to Know: past 5 years have seen $2.5tn inflows to US assets (Treasuries, corporate bonds, stocks – Chart 5), and $1.3tn inflows to US stocks alone (note there were outflows from US stocks in the 2010s – Chart 6); since “Liberation Day”, very little evidence investors dumping US assets (domestic institutions have sold $10.3bn, foreign institutions bought $4.5bn), but Fed Flow of Funds shows foreign investors own huge $16tn US stocks (18% of total), $8.5tn US Treasuries (33%), $4.4tn US corporate bonds (27%), and long-term money moves slowly; global capital no longer exclusively chasing US assets, and just a small reallocation of US stocks from 64% of global equity market cap ($49tn) to say 60% (average of 2020s – Chart 4) = big positive impact on Rest-ofWorld (note US equities have averaged much lower 50% in past 25 years).

… in context of 5yy being a ‘fan favorite’ these days AND that it took a peek above 4% just last week AND I laid out support / resistance visual Friday (HERE) — note their update and entry level … something highlighted too (HERE) … an update …

8 May 2025 Barclays: Global Rates Weekly In no rush

In the US, the Fed looks increasingly reactive, but the likely magnitude of the trade shock suggests markets should put more weight on less now and more cuts later. In Europe, EUR rates continue to look for direction but with little success. In Japan, June QT plans could affect term premium…

…United States: Interest Rates: In no rush The Fed looks increasingly reactive, but the likely magnitude of the trade shock suggests markets should put more weight on less now and more cuts later. We maintain our long 5s view. Separately, we recommend 10s30s Treasury curve flatteners and buying ATM-100 10y20y receivers on better fiscal news.

US Treasury yields were modestly higher over the week as hard data remained resilient and Fed is still in no rush to cut. Figure 1 shows that 10y yields rose 5bp from Friday's close. Across the Atlantic, Bunds were unchanged over the week but gilt yields sold off a touch. Meanwhile, the Japanese yield curve bear steepened sharply amid concerns about the fiscal and demand dynamics at the long end (see the Japan Rates Strategy piece). Figure 2 shows that on a real yield basis, the move in the US was muted relative to other bond markets. Risk assets have continued to rally, with US equities up 2pp and credit spreads continuing to grind tighter amid rising optimism.

We continue to recommend being long 5y USTs (entry: 4.10%, current: 3.99%) as markets have overreacted to the stability of hard data, when in fact the lags between soft and hard data surprises could be a few months. While the US-UK trade pact was touted by the administration as a success, the baseline tariff rate remains at 10%, which points to a likely minimum 10% tariff rate on all trading partners 1 . This also suggests that should negotiations not go well, the tariff rate could rise on those countries after the 90 day suspension ends in early July. Hence, the trade shock is still likely to be meaningful. The FOMC meeting outcome suggests that the Fed is likely to be reactive, which means the market should put more weight on a deeper cutting cycle down the road, which would benefit 5s.

Separately, fiscal news flow has actually been conducive to lower long-term yields, as many House Republicans continue to insist on significant spending cuts and for any budget bill to effectively reduce deficits versus current policy 2 . Long-term forward yields above 5% suggest that the markets are not putting much weight on this outcome. We recommend 10s30s Treasury curve flatteners and buying ATM-100 10y20y receivers…

Best in show says … LONG 2s (3.90) and lookin to ‘fade a rally in 10-year breakevens on falling recessions odds’ … read on or BUY 2s first thing Sunday night?? Just kiddin’ NOT investment / trading advice …

In the week ahead, the evolution of US inflation will once again be in focus. Expectations are for a 0.3% monthly core-CPI gain in April with the headline pace also seen at 0.3%. While there might be pockets of core goods inflation associated with the new tariffs, we’re looking toward the June/July series to be more relevant in gauging the inflationary impact of the trade war. After all, Trump’s pause on reciprocal tariffs doesn’t end until July 8th. In the interim, there will undoubtedly be fresh carve-outs and reductions that will lower the ultimate increase in the effective tariff rate in the US. That being said, the weighted average tariff on imported goods will unquestionably be higher than the 2.5% in 2024 – the open question still remains how much higher? Estimates have been reigned in from the mid-20s to somewhere between 15% and 20% – although there is understandably limited conviction to any projection at this stage given how quickly the Administration has been changing levels and demands.

Investors' focus will also be on interpreting any headlines and actions resulting from this weekend’s US/China trade talks. No one is anticipating an agreement, although the simple fact that a dialogue has been started has been interpreted as a net positive for the prospects of a bilateral deal at some point. We’re wary that the market is expecting more from the initial round of negotiations than is likely to be on offer. While the classic management adage holds that any meeting that results in another meeting was a bad meeting, that isn’t the case as it pertains to the trade negotiations between Washington DC and Beijing. Instead, we’re anticipating that incremental progress will be the theme. A slow but steady thawing of trade tensions between the two partners appears to be the best outcome at this stage. One shouldn’t expect a US/UK style announcement in the week ahead.

What has apparently become the ritual of increasing and subsequently lowering tariffs has complicated an already convoluted process of attempting to project what the trade war means for the US inflation profile. In short, it will be higher; although the extent to which it becomes self-perpetuating is the biggest wildcard. Powell’s decision to bring ‘transitory’ out of retirement is consistent with the Fed’s messaging that tariffs represent one-time price adjustments rather than true, demand-driven inflation of the sort that would warrant a monetary policy response. This isn’t a foregone conclusion however – and when combining the potential employment impact from Trump’s immigration agenda, there is meaningful uncertainty as to the extent to which nominal wage gains also prove sticky. The President’s attempts to redefine the global trading landscape were always going to involve an innumerable number of moving parts, it’s the 'on-again, off-again' levy strategy that has materially lengthened the timeframe of uncertainty for the real data.

Even as the April CPI report approaches, the market will be looking beyond the current pace of consumer inflation toward what occurs during the summer months. Investors’ bias to dismiss the recent reports as stale information isn’t likely to change in the near-term. Even as reflation is expected to materialize in June/July, the bilateral deals struck over the coming months will lead to a further discounting of the incoming data. After all, the trade rules are still being rewritten, and it's not until the ink is finally dry that investors will have sufficient confidence that assumptions won’t be completely upended yet again. As uncertainty becomes the new norm, choppy price action in US rates with 10-year yields in a 4.20% to 4.50% range will remain the path of least resistance.

Charts of the Week …Our second chart helps illustrate the decoupling between short-term inflation expectations and year-ahead rate cut pricing over the last several months. The two measures tracked closely through much of the 2023-2024 period but sharply diverged as Trump’s Presidency (and tariffs announcements) got underway in 2025. In the wake of Liberation Day, the 1-year inflation swap rate reached as high as 3.61% (a nearly 3-year high) while the futures market priced in as much as 118 bp of rate cuts over the next 12 months. The market is clearly overweighing the employment side of the dual mandate with a nod to the elevated recession odds.

It's the downside risks to growth and employment that have left many biased for the Fed to soon begin cutting rates again despite the fact that near-term inflation expectations are at multi-year extremes in both market pricing and sentiment surveys. At its essence, the above divergence shows investors' concern that the trade war will be short-term inflationary but medium-term recessionary…

…Trading View We bought 2-year notes on Thursday, May 8th at 3.90%. Our target is set at the month-end close from April 30th at 3.60%. Overhead, our stop level is 4.04% – a level that should be well defended by several key technical hurdles. First, we see an opening gap from 3.945% to 3.960%. Note that 3.960% is a weekly close and the high yield close for the 2-year sector since “Liberation Day.” Second, a handle change at 4.0% is an obvious line in the sand. Third, the post-Liberation Day yield peak comes in at 4.031%. Away from the technical factors, the hawkish shift in rate cut pricing has reached a point that’s left us biased to play the 2-year sector from the long side. Largely given the risk that political headwinds translate to a downturn in consumption and employment in the coming months and quarters.

As for our forward entries, we'll continue to look for an opportunity to fade a rally in 10-year breakevens on falling recessions odds – either as a function of stronger data or a fresh round of trade deal optimism. We're holding our target entry level at 237 bp. We'll also look to fade a spike in near-term (June/July) rate cut pricing if the August 2025 Federal Funds Futures Contract (FFQ5) climbs above the NFP-day close from May 2nd at 95.930. Fully pricing a rate cut over the next two Fed meetings would be overly discounting the Fed's hawkish resolve.

… ‘FIRE in the hole!’, so to speak …

09 May 2025 BNP: US: Spring detonation, summer impact for tariffs

KEY MESSAGES

We are nearing the point at which our long-held view that tariffs will drive a material increase in US consumer prices transitions from expectation to reality.

Our analysis of inventory levels, import dynamics, and recent historical examples of price responses to tariffs and supply shocks suggests that tariff-driven increases in inflation will materialize by the summer.

While heightened policy uncertainty may delay price adjustments temporarily, we think US companies will ultimately have to respond to sustained tariff pressures by adjusting prices.

… Regime uncertainty may make it more rational for companies to adopt a “wait and see” approach rather than act immediately. Unlike a traditional supply shock that stems from physical constraints, tariffs are policy-induced and potentially reversible. That makes their perceived permanence lower, especially when announcements are changed and there is a lack of operational clarity. The administration’s tariff rollout has been inconsistent and difficult for firms to plan around. As a result, companies are operating in a fog of uncertainty, where strategic patience may be preferable to a rushed response.

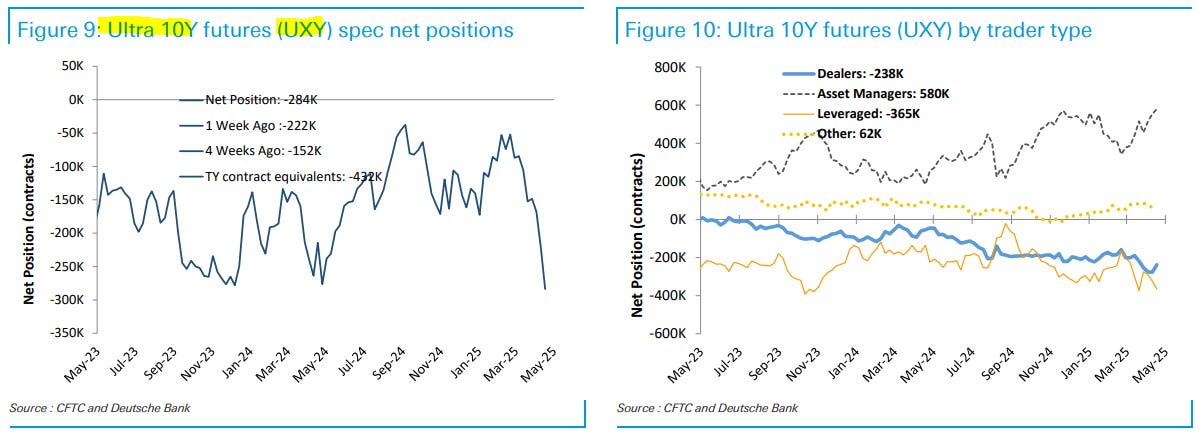

Positions. Lives. Matter … even those evil speculative ones and so … when I see ‘record net’ (SHORT / long ) I pause and remind myself for every single seller there has to be a buyer …

09 May 2025 DB: Commitment of Traders - Weekly Update

Interest Rates: Speculators were bearish in Treasury futures, extending their net short positions by 194K contracts in TY equivalents over the week prior to May 6th, 2025 (Tuesday).

Asset managers boosted their net long positions by 56K contracts in TY equivalents, while leveraged investors added 235K contracts in TY equivalents to their net short positions. All Treasury futures contracts except for TU, and WN saw increased asset managers long positions, while leveraged investors extended their net short positions in all Treasury futures except for TU. Dealers removed 163K contracts in TY equivalents from their net short positions.

Speculators sold 4K and 62K contracts in FV and UXY to extend their net short positions to record -2,296K and -284K contracts, respectively.

Fed funds futures: Speculators sold 8K contracts to extend their net short positions to -116K contracts.

SOFR futures: Speculators bought 11K 1M SOFR contracts to bring their net short positions down to -8K contracts. They sold 173K 3M SOFR contracts to extend their net short positions to -738K contracts.

Positions and flows to knows … even IF they aren’t, in this next note’s case, bond related — worth a look …

09 May 2025 DB: Investor Positioning and Flows - Waiting For Substantive Trade Relief

…Positioning for discretionary investors has gone largely sideways over the last two weeks, slightly below neutral. Discretionary investor positioning had fallen nearly -1sd below average immediately after Liberation Day but popped higher once the 90-day pause was announced a week later, then continued moving higher over the next two weeks on further exemptions, the assurance that there was no plan to fire the Fed chair, and a steady stream of news about ongoing trade deal negotiations. It has gone largely sideways over the last two weeks and at just a little below neutral, discretionary positioning is in line with earnings growth falling to near zero but not with outright earnings declines. If tariffs are sustained, we see significant downside for earnings, and in our reading near-neutral discretionary positioning is implicitly in line with the tariff drag being modest and temporary (Tariffs And Equities: Lowering Estimates And Target, Apr 23 2025).

…Rally over the last month occurred largely during NY cash trading hours while overnight returns were muted. We noted a month ago that the selloff in the S&P 500 this year had largely occurred during overnight hours rather than during the cash trading hours, a reversal of the pattern of the past several years. Since then, the market has rallied strongly but most of the upside has been during the cash trading hours while overnight returns have been muted.

Jan Joey’s actual swan song, final note from earlier in the week …

This is my final note at J.P. Morgan, having decided now is a good time to retire after nearly 40 years in research at the firm. Alex Wise, who has written many issues of The Long-term Strategist with me over the past 4 years, takes over. You are in good hands with him.

I have written twice before about lessons learned, one in 2017 at the end of my tactical strategy years, and one in 2023 about long-term investing. Here are some closing thoughts.

As analysts and investors, we are constantly poring over data for patterns and lessons on what to expect next, as if markets and economies are stationary systems. I find, though, that the only real constant is change as people, policy makers and investors constantly learn and adapt. It is dangerous to expect past patterns will persist or that macro variables and assets prices/IRRs will always return to past means.

Each of us wants to believe we know better than the market, which is driven by the sum of all of us. Clearly this does not add up. I find it better to start the presumption that markets are quite good at pricing the future and then look for exceptions where a decent case can be made for a mispricing.

The market reflects the “crowd.” Is there wisdom in the crowd, as is frequently argued, or instead madness? I think most of the time, the crowd’s wisdom dominates, but it is at extremes that madness takes over, in bubbles and panic. Keep an eye out for extremes in long-term value to tell you when wisdom is turning to madness.

Being long term does give you advantages. Saving for old age is the main reason why we save and invest, and the long-term perspective should thus dominate asset pricing. But I find market attention, models, news, and data focus on the near term, making truly longer-term investors the minority and thus better able to pick up assets that are priced for the short term investor, making them attractive for the long-term one.

One principle I have been living by is to always keep things simple, in analysis, writing, speaking, and investing. Simple words, short, clear and blunt language, and simple and cheap products are best.

Words, words, words: Long or short term; fundamental or technical; cycle or structure; regimes and paradigms are all words that aim to describe and explain reality, but they exist only in our mind.Do use them, but do not think of them as facts and reality…

… Our Strategic Asset Allocation (SAA) represents our recommended longer-term strategic allocation across asset classes. SAA is different from J.P. Morgan Research’s TAA, which recommends shorter-term devia tions from an investor’s own SAA.

We keep a generic, fixed 60/40 equity-bond allocation as this should be driven by the investor’s own invest ment horizon, return objectives, and risk tolerance. We follow broadly our “Keep It Simple” KISS principle. Allocations within bonds and equities each start from global outstandings for maximum diversification (Table: World Financial Market). From this, we cut parts we do not want to invest in strategically and add others we’d like to hold more of. Allocations do not distinguish between public and private asset classes. We have no reason to either exclude or overweight private assets. Most of our suggested asset classes can be held through mutual or exchange-traded funds (ETFs), except for private assets and hedge funds. We do not distinguish between passive or active funds, leaving that to the investor. Our portfolio does hold tactical risk through specialized managers – hedge funds. All allocations are FX unhedged, except for credit and securitized bonds.

Check me if I’m wrong here but if we cut coupon auction sizes, there’ll be less to bid on and should, theoretically, on paper, make auctions better (looking, at least) and easier …

May 9, 2025 MS: The Path to a 30% Bill Share | US Rates Strategy

We offer a thought experiment about the issuance strategy of the US Treasury. Imagine it’s the end of the year and trade uncertainty persists; investors require more term premium. In this scenario, Treasury could respond by cutting coupons, putting the bill share on a path to 30%.

Key takeaways

Treasury issuance is a popular topic among investors, in consideration of large US budget deficits, rising term premium, and concern about foreign demand.

While Congress decides "how much" the government spends and "how much" to raise in taxes, Treasury is responsible for "how" the government is financed.

We offer a thought experiment on an issuance strategy: what would happen if Treasury were to reduce the supply of coupons in order to meet lower market demand?

We think this hypothetical scenario would likely put the bill share of total outstanding marketable debt on a path to approach 30% by 2027.

MMF AUM growth, a shorter SOMA WAM, and stablecoin growth are sources of bill demand, offering Treasury flexibility to at least hold coupon sizes for longer.

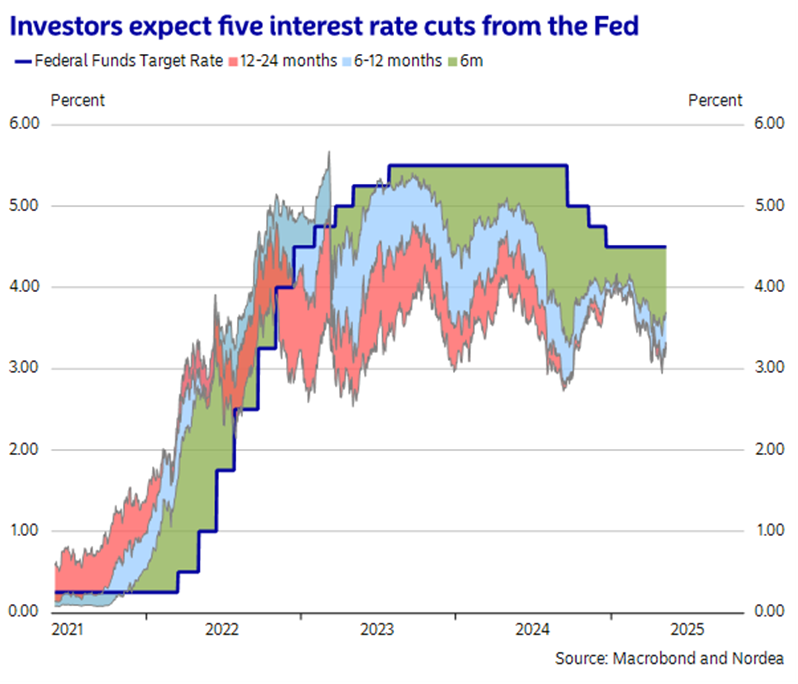

Investors, they say, are expecting 5 rate cuts from the Fed …

9 May, 08:09 NORDEA Macro & Markets: Increasing optimism ahead of stagflation risks

… In reality, the Fed is unlikely to cut its policy rate anytime soon. Instead, the Fed will very likely wait, which was the word Powell used most frequently at his latest meeting, and keep its policy rate unchanged, like we have projected in our forecast, unless it is crystal clear that the economy is slowing down. Given this reaction function, it would make most sense if the market did not expect any interest rate cuts in the short term, but rather multiple interest rate cuts late this year or next year, to reflect the increasing downside risks to the economy.

This cautious reaction function is very important today when the Fed needs to maintain trust and confidence, while facing public challenges to its independence from President Trump. If investors lose confidence in the Fed’s commitment or ability to control inflation, it could put a lot of upward pressure on long-term bond yields in order to discount higher inflation risks and political uncertainty. Similarly, if the stock market loses confidence in the Fed, it will put downward pressure on valuations from investors demanding a higher risk premium to compensate for increasing economic and political uncertainty. Lastly, the safe-haven dollar could strengthen in a risk-off situation, but it could also weaken substantially, if investors respond to mistrust by selling US assets and the dollar.

This is exactly what happened when Trump said he wants Powell to lower interest rates and Kevin Hassett announced they were investigating whether a president could fire a Fed Chairman. The dollar reacted sharply to Trump’s attack on the Fed and weakened, even as stocks and bonds sold off. This in contrary to typical cross asset risk-off patterns and suggests that investors were reducing exposure to US assets and the dollar simultaneously, reflecting broader concerns about Fed independence and policy credibility.

Covered wagon’s week ahead … rates, FOMC on HOLD …

May 9, 2025 Wells Fargo: Weekly Economic & Financial Commentary

United States: Risks Have Risen (but Haven't Materialized Yet) The trade deficit blew a hole in Q1 productivity growth, and tariffs are anecdotally increasing price pressures in the services sector. But beyond temporary trade-related distortions, tariffs have yet to meaningfully impact the economic data. We anticipate that tariffs will be negotiated down from current levels but still create a stagflationary environment by year-end.

… Interest Rate Watch: FOMC's Holding Pattern Continues As universally expected, the Federal Open Market Committee (FOMC) decided to keep the target range for the federal funds rate unchanged at 4.25%-4.50% this week. After cutting rates by 100 bps last year, the Committee has now been on hold for three consecutive meetings. The decision to keep policy unchanged was unanimously supported by all 12 voting members.

In the absence of a Summary of Economic Projections (SEP), the Committee's primary avenue for forward guidance was its post-meeting statement. Yet, the statement was noncommittal. The Committee tacked "further" on to the end of a sentence from its March statement: "uncertainty around the economic outlook has increased." The addition nods to President Trump's announcement of "Liberation Day" tariffs that were much higher than expected. The FOMC also noted that "the risks of higher unemployment and higher inflation have risen," more explicitly gesturing to the potential stagflationary shock generated by tariffs.

The effective tariff rate stands at roughly 25% today by our estimates, which is the highest in more than a century. While a return to the 2% rate of 2024 is highly unlikely, we think tariffs will recede somewhat as the Trump Administration finalizes some deals. For the purposes of our forecast, we assume the effective tariff rate will fall to 15%.

Nevertheless, the rise in the effective tariff rate will cause inflation and the unemployment rate to move higher in the coming months. On one hand, the FOMC would want to ease policy as the jobless rate rises. On the other hand, rising inflation would encourage monetary policymakers to refrain from easing policy, if not tighten it. In other words, the Fed's dual mandate (i.e., "price stability" and "full employment") will likely be in tension.

The best course of action for the FOMC may simply be to wait for more clarity. Indeed, Chair Powell reiterated during his press conference that "we don't think we need to be in a hurry to adjust rates." Given the underlying solid nature of the economy, Powell said that "the costs of waiting are fairly low."

In view of the economy's sustained momentum recently, we now expect the FOMC to keep policy unchanged through the summer. Specifically, we look for the Committee to resume its easing cycle with a 50 bps rate cut at the September meeting followed by two 25 bps rate reductions at the October and December meetings. After that, we suspect the Committee will hold the target range for the federal funds rate steady at 3.25%-3.50% through 2026. For more detail, please see our recently published U.S. Economic Outlook.

We readily acknowledge that uncertainty around our economic outlook remains greater than normal. Our forecast hinges on our expectation for the Fed to “look through” the price level increase caused by tariffs, especially as long-term measures of inflation expectations remain anchored. However, if inflation were to show signs of becoming more entrenched, then the FOMC may be less inclined to ease policy.

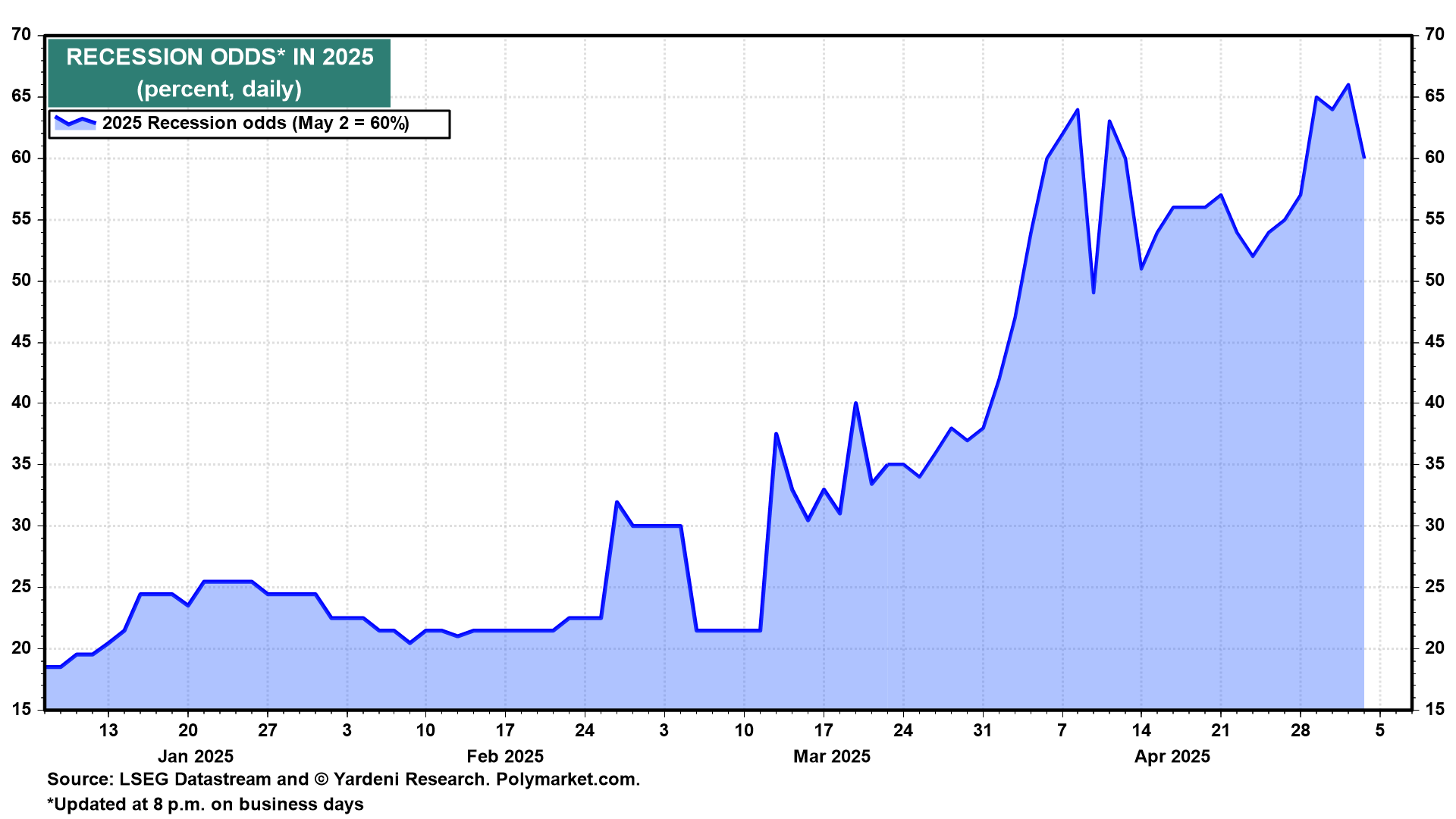

… finally, the wait for Godot (recession) is over as it came and went already and we missed it? RECESSION ODDS DOWN but not yet raising S&P tgt up … go figure …

During 2022, 2023, and 2024, most economists and investment strategists expected that the dramatic tightening of monetary policy would cause a recession. They observed that the inverting yield curve and the falling Index of Leading Economic Indicators were confirming this outlook. We argued that the recession was the most widely anticipated recession of all times that wasn’t likely to happen. We called it the “Godot recession.” We focused on the reasons for the underlying resilience of the economy and dismissed the widely followed leading indicators of recession as misleading.

The Godot recession may be back in 2025. This time, the cause of the widely anticipated downturn is Trump’s Tariff Turmoil.

According to Polymarket.com, a trading platform, the chance of a recession was relatively low around 20% from the time President Donald Trump was inaugurated on January 20 through March 11 (Fig. 1 below). The odds then shot up dramatically, especially after April 2 (“Liberation Day”), reaching 64% on April 8. They fluctuated around 55% after Trump postponed for 90 days the reciprocal tariffs that he had announced on April 2 for all countries with one notable exception: China’s tariff remained 145%. The odds of a recession rose to 66% on May 1 following last week’s batch of weak economic indicators (i.e., consumer confidence, ADP payrolls, M-PMI, and jobless claims). The odds fell to 60% on Friday, May 2, following the release of a stronger-than-expected employment report for April.

Figure 1

While economic growth remains our base-case scenario, we did raise our subjective probability of a “tariff-induced” recession from 20% at the start of the year to 35% on March 5. We wrote, “We are still betting on the resilience of consumers and the economy. However, Trump Turmoil 2.0 is significantly testing the resilience of both. That’s why we’ve recalibrated our subjective probabilities.” On March 31, we raised the odds again to 45% and blamed Trump’s Reign of Tariffs. We wrote, “That 45% is also the probability we see that the stock market’s correction will deepen into a bear market in coming months. Yet we still expect an up year, with the S&P 500 rising above 6000 by year-end.”

In other words, we remained, and remain, believers in the resilience of the economy. It withstood the tightening of monetary policy over the past three years. We expect it will withstand this year’s tariff turmoil.

US Economy II: Lowering Our Odds of a Recession.

We are now lowering our odds of recession back down to 35% because we believe that China and the US both may be ready to suspend their tariffs on each other while they negotiate a trade deal. In other words, both sides may be starting to blink. Neither side can bear the pain of a trade war, which might be more painful for China’s economy than America’s economy. On the other hand, Americans have less tolerance for pain than the Chinese (for more on China’s “chiku” ethos, see the Morning Briefingdated April 29, 2025).

We also expect that Trump will declare victory in his trade war with the rest of the world. By the end of the 90-day postponement period of his Liberation Day reciprocal tariffs, the US is likely to have signed numerous agreements with America’s major trading partners. Stragglers might come around during a second 90-day postponement period. Trump needs to put the trade issue behind him to reduce the odds of a recession, which would harm the Republicans’ chances of holding onto their slim majorities in both houses of Congress…

…Sure enough: Trump postponed his reciprocal tariffs two days later, on April 9. The S&P 500 traced out a V-shape, bottoming on April 8 and climbing 14.1% since then through Friday’s close (Fig. 2 below and Fig. 3 below).

… Strategy: To Raise or Not To Raise Our S&P 500 Target?

At the start of the year, our S&P 500 target for the end of this year was 7000. When we raised our odds of a recession on March 5 to 35%, we lowered our target to 6400. We lowered it again on March 31 to 6000, when we raised the odds of a recession to 45%.

Now that we are lowering the odds of a recession back to 35%, should we be raising our S&P 500 target back to 6400? We are inclined to do so given the power of the V-shaped rally in the S&P 500. However, we aren’t ready to do so given the following two issues:

(1) Earnings. The outlook for S&P 500 earnings is deteriorating. Tariffs are first and foremost taxes on domestic importers. The 10% baseline tariff on all imports from most countries was announced by Trump on Liberation Day and imposed on April 5. There is also a 25% tariff on autos, aluminum, and steel. The 145% tariff on China remains in force as well.

Over the past 12 months through March, corporate tax receipts totaled $502.19 billion (Fig. 17 below). The currently active tariff rates could raise over $300 billion in import duties over the coming 12 months. That would be a significant increased tax burden on corporate profits unless they are passed through to consumer prices. Some companies, such as those in the auto industry, might find that hard to do.

Figure 17

(2) Valuation. The valuation multiple of the S&P 500 bottomed at 18.1 on April 8. It was back up to 20.5 on Friday (Fig. 18 below). It is very unlikely to bounce back to the 22.1 at which it began the year.

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

First up, a simple chart and consequences to consider …

May 10, 2025 Apollo: Chinese Exports Redirected From the US to the Rest of the World

The US is no longer importing cheap goods from China. As a result, the rest of the world will likely see a significant increase in imports of cheap Chinese goods that China can no longer sell in the US.

This creates a highly unusual macroeconomic situation, with upward pressure on inflation in the US and downward pressure on inflation in Europe, Canada, Australia, and Japan.

The consequence for markets is that rates will be higher in the US and lower in the rest of the world.

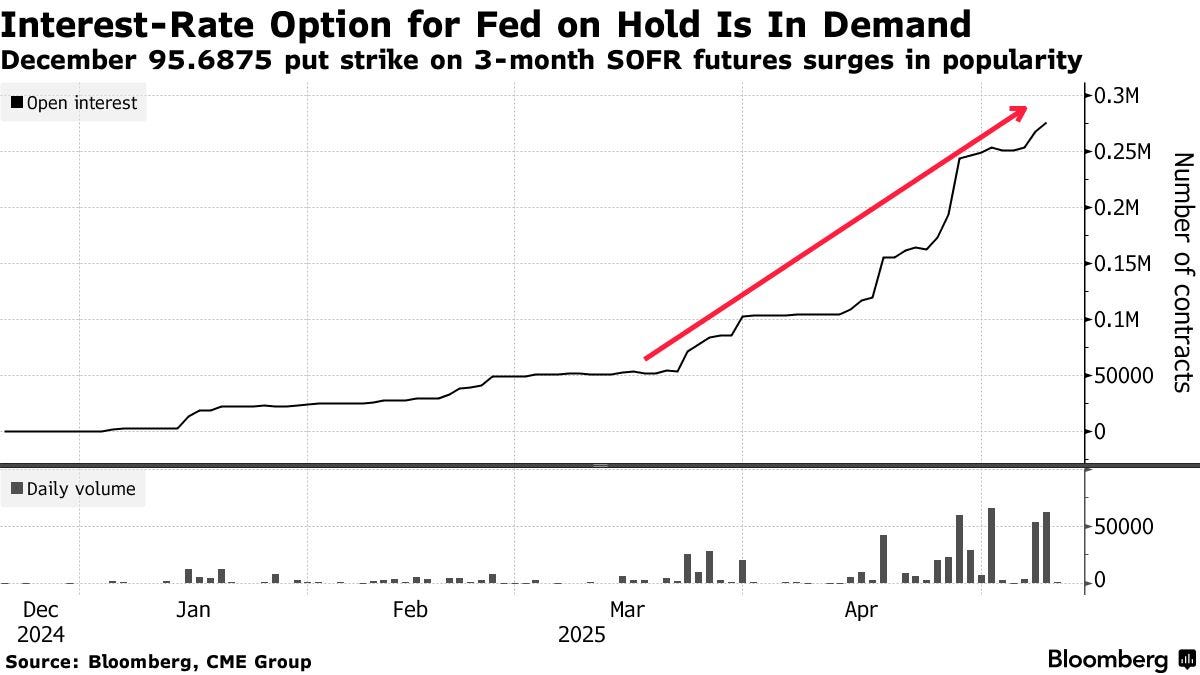

Positions. Lives. Matter — especially those as reported by one of the best in the biz, Bloomberg’s on EBB …

May 9, 2025 at 4:09 PM UTC Bloomberg: Options Traders Flock to Wager That Fed Won’t Cut Interest Rates By Edward Bolingbroke

A contrarian wager that the Federal Reserve won’t cut interest rates this year is exploding in the options market.

The position takes the form of a put option — entitling the holder to sell at a specific price during a defined time window — on the December 2025 futures contract for the Secured Overnight Financing Rate, which closely tracks the rate set by the Fed. The specified price — 95.6875 — is lower than the current futures price, which anticipates close to three quarter-point rate cuts by year-end.

The option will rise in value as the futures price drops toward the strike price, which would happen if rate cuts are no longer expected.

Open interest in the option — the number of contracts in which traders have positions — exceeds 275,000. While that’s dwarfed by the levels for contracts closer to the consensus view, it’s soared in recent weeks — and gained momentum since the most recent Fed meeting.

The number of individual traders involved is unknown, however an estimated $25 million has been spent since March to buy about 250,000 contracts, according to traders familiar with the position and data compiled by Bloomberg.

Open interest in the strike increased again on Thursday as SOFR futures prices fell, according to data from CME Group Inc., which operates the exchange that lists SOFR futures and options. The selloff reflected fading conviction about Fed rate cuts this year based on strong US economic and stock-market performance.

The bet has increased in value since the Fed’s latest policy meeting ended on Wednesday with a decision to leave the target band for the federal funds rate unchanged at 4.25%-4.5%. Discussing the decision in a news conference, Fed Chair Jerome Powell said the level of rates is appropriate for current economic conditions and unlikely to change until it’s clear that conditions are changing.

It increased further on Thursday when US President Donald Trump sparked gains for US stocks by saying people should buy them based on progress toward a trade agreement with the UK.

That could change, however, following weekend trade negotiations with China. Trump Friday floated an 80% tariff on Chinese imports, while people familiar with preparations for the talks said the US side has set a target of reducing tariffs below 60% as a first step.

If the outcome of the talks alters the outlook for Fed policy over the rest of the year, the value of the position could face a setback or increase further.

Daily SHOT w/a shot ‘cross the FOREIGNERS PULLING BACK FROM USTs bow …

…Rates: The percentage of indirect bidders (usually foreign institutions) at this week’s 30-year bond auction hit the lowest level in years.

10s, MBS and curve steepening, OH MY …

May 9, 2025 WolfST: 10-year Treasury Yield Back at 4.39%, Yield Curve Steepens at Long End, Mortgage-Rate Spread Remains Historically Wide

Despite the rumors during bond turmoil, foreigners kept buying Treasuries and the “basis trade” didn’t blow, but the “swap spread trade” made a mess.

The 10-year Treasury yield rose to 4.39% today and is now back in the middle of the range of the past two-plus years, despite the gyrations in between, having brought behind it the deep plunge to 3.99% (bond prices soared) in late March and early April, followed by the brutal re-spike to 4.49% (bond prices dropped) after the announcement of the new tariffs on April 2.

But now the yield has calmed down at 6 basis points above the Effective Federal Funds Rate (EFFR), a short-term money-market rate that the Fed tries to keep locked in place with its policy rates.

Spikes followed by plunges, and vice versa, in an always edgy bond market are part of the deal and don’t indicate long-term trends.

The spread matters. Mortgage rates track the 10-year Treasury yield, but are higher, and this spread varies but is currently relatively wide at about 2.4 percentage points, keeping mortgage rates relatively high with respect to the 10-year Treasury yield.

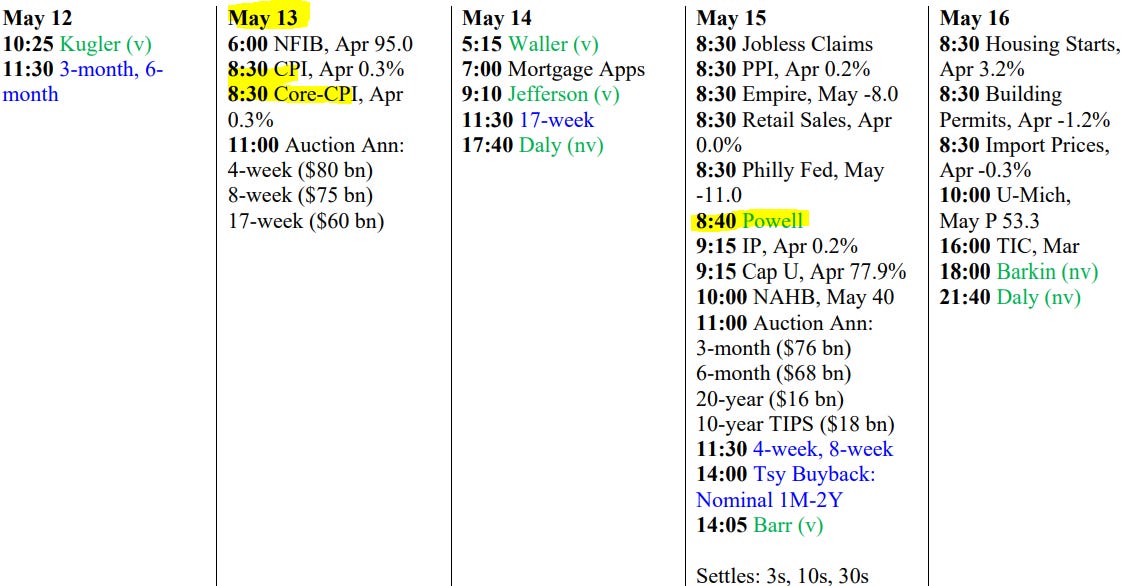

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Amazes me to see how Sentiments and Predictions change by the week,

about the path of our enormous US economy.

Pres. Trump is making progress on Trade.

Maybe Powell is right ???

Have a great week.

For what it's worth; I went out this morning to have sauna at Perspire Sauna Studios, which highly recommend, but there was a ton of traffic. People going everywhere. I don't think there's going be a recession in Phoenix, AZ..this year.

Great articles on some fascinating topics.

Amazes me to see how Sentiments and Predictions change by the week,

about the path of our enormous US economy.

Pres. Trump is making progress on Trade.

Maybe Powell is right ???

Have a great week.

For what it's worth; I went out this morning to have sauna at Perspire Sauna Studios, which highly recommend, but there was a ton of traffic. People going everywhere. I don't think there's going be a recession in Phoenix, AZ..this year.