weekly observations (09.30.24): month-end coming…#GotBONDS?; "...The 10y UST yield may be too low" (BNP); learning from history of steepeners (JPM); some 10y shorts covered (move out to BONDS)

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Middle East / geopolitical NEWS on Friday set the markets on alert and resulting F2Q bid bonds ahead of the weekend where month end is Monday afternoon (4pm — see notes below from FRBNY and myself in years past) and this helped drag 10yy back to / below (WEEKLY)TLINE noted … For those who, like ME, may not have known who this fine young man was … Hassan Nasrallah Wikipedia HERE…

ZH: Israel Expands Bombing Of Southern Beirut As Nasrallah's Fate Unknown RTRS: Israel pounds Hezbollah in Lebanon and hits Houthis in Yemen as violence widens

…Nasrallah's body was recovered intact from the site of Friday's strike, a medical source and a security source told Reuters on Sunday. Hezbollah has not yet said when his funeral will be held…

It would appear the data AND geopolitical news) Friday soothed fears (and then stoked others) and was considered positive for markets … at least as far as 10s vs approx 3.64% (noted here) concerned … Lower rates = higher stocks. Moving on but first …

30yy DAILY: support up nearer 4.15%, month-end coming…#GotBONDS

…momentum swing from overbought to overSOLD and TLINE support holding just as geopolitical concerns fire UP and, well … month-end comin … more on how / why to watch in / around 4pm tomorrow, MONDAY, which is now the (not) new 3pm …

… always best to check in on and vet MY levels with those noted HERE(offered by some of the best techAmentalists out there which I’ve followed for nearly 30yrs…).

NOW, lets deal with a couple / few things items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) …

ZH: Fed's Favorite Inflation Indicator Hottest Since April, Govt Handouts Continue To Soar

Bonddad: Personal income and spending hits a triple, plus a big positive surprise revision

CalculatedRISK: Personal Income increased 0.2% in August; Spending increased 0.2%

WolfST: Fed Favored Annual Core PCE Price Index Accelerates to 2.7%, Highest since April, on Higher Core Services Inflation (+3.8%). Durable Goods -2.2%, Energy -10%

… and SOME of Global Walls reactions and reflex in ‘click bait’ form for you to pick and choose whichever you’d wanna investigate further …

BMO: Savings Rate Drops, Core-PCE +0.13%, TSY Rally ING: Benign US inflation allows the Fed to focus on jobs

… AND there was some other funTERtainment in as far as macro eco FUNduhmentals came and went …

ZH: UMich Consumer Sentiment Survey Confuses In September

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW …

Core PCE prices rose 0.13% m/m in August, taking the annual rate higher to 2.7% on unfavorable base effects. Annual benchmark revisions to the price index were minor. On balance, the data still indicate that inflation is on track to reach the FOMC's 2% target. We maintain our baseline call for two more 25bp cuts this year.

BARCAP: The Blue Drum: This too shall pass (with a visual which made ME mad … dunno why BUT…)

Oil markets are experiencing a panic attack, in our view. Investor positioning is disconnected from spot fundamentals and has likely gone too far in foreshadowing weaker fundamentals next year.

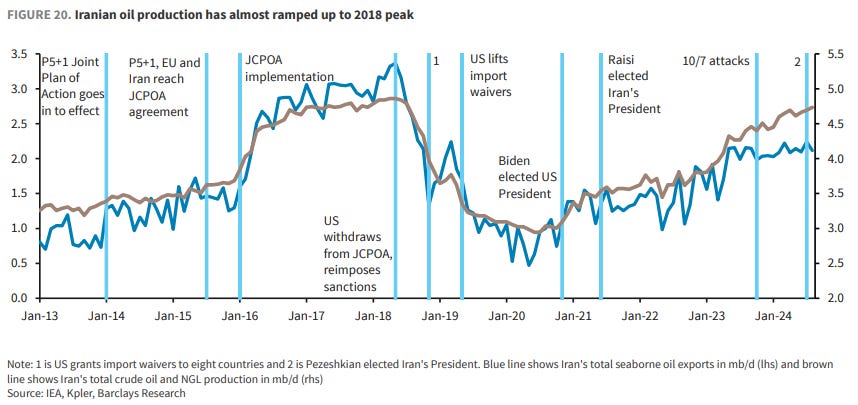

… With the US elections just around the corner, it is probably worth reiterating that a potential change in the US Middle East policy could be the single most consequential change for the short-term oil market outlook, especially given the geopolitical drift of late characterized by a continued increase in regional tensions amid advancements in Iran's nuclear program, with a simultaneous ramp up in the country's oil output and exports. According to the IEA, Iran's oil output stood at 3.4 mb/d in August, just 400 kb/d shy of the peak in 2018, before Trump reimposed oil sanctions (Figure 20).

BMO US Rates Weekly: Powell's Payrolls Peril (stay with, add to steepeners)

…We’re certainly sympathetic to investors’ focus on payrolls as the pivot point and suspect that it will initially be traded as such. The current consensus forecast is for a modest 130k gain in headline payrolls – a deceleration from August’s 142k print but still >100k. The unemployment rate will potentially be more relevant to the Fed’s perception of the health of the labor market. Expectations are for the measure to be unchanged at 4.2%; although the recent upward pressure has left the market wary of another tick higher. The grind toward a higher unemployment rate has been steady thus far in the cycle, which is atypical given that historically when the jobs market turns, it does so quickly and dramatically. This history has been an underpinning of the widely held concern that there is greater downside yet to be realized for the labor market.

The prospect for another leg lower on the jobs front is undoubtedly a concern for monetary policymakers as well, contributing to the case made for a half-point departure for the normalization cycle. As we watch the futures market continue to price in >50% odds of another half-point reduction, we’re comfortable concluding that 50 bp will most likely prove to be the path of least resistance unless there is a dramatic improvement on the labor front. There has been some concern that a dockworkers strike could provide a fresh reflationary impulse and quickly become a policy consideration – if not an election factor. The echoes of supply chain disruptions are certainly not wasted on us, although the recent trend of goods deflation provides a meaningful offset. In addition, the Fed’s reaction function to inflationary risks has softened as the employment component of its mandate has quickly taken center stage. It isn’t difficult to envision the Committee characterizing a near-term spike in costs as a tax on real consumption in light of the current macro backdrop.

BNP: US rates: How the UST curve reacts to Fed rate cuts

5s10s may be the most attractive curve steepener across different economic outcomes.

Unsurprisingly, curve segments including the 30y UST exhibit the least reliable signal during Fed cycles.

Both 5s10s and 2s10s UST appear favorable compared to the forward curve. This may imply that the 10y UST yield is trading too low, which is corroborated by our 10y UST fair value model.

Trade: Enter 5s10s UST steepener at 24bp. Target: 70bp. Stop: 8bp…

…We come to two conclusions:

The 10y UST yield may be too low: Across all scenarios for 2s10s and 5s10s, we project a flatter curve only once. 2s10s UST would be projected to finish flatter than the current forward curve in the softer landing scenario, which sees the Fed cut to only 4%. This is corroborated by our 10y UST model, which estimates the current yield as 20-25bp too low and fair value at approximately 4% (see Figure 7 on the following page).

…5s10s UST may be the most attractive curve steepener …

…US data has surprised positively in recent weeks and we expect payrolls to continue the trend with a 150k increase while the unemployment rate remains at 4.2%, but risks likely remain asymmetric towards weaker data and we have entered a 5s10s UST steepener.

DB: Investor Positioning and Flows - No Let Up In Inflows

Our measure of aggregate equity positioning crept up further this week but is still only about mid-way in the upper half of its longer run band (z score 0.47,71st percentile). Discretionary investor positioning rose further and is now somewhat elevated although well supported by rising growth and falling rates volatility (z score 0.76, 89th percentile). Overall positioning is still being held back by systematic strategies, whose positioning has been going sideways slightly above average (z score 0.18, 50th percentile). Systematic strategy positioning should rise as volatility recedes after the back-to-back pullbacks of the last 2 months. Meanwhile, there is no sign of a let up in the strong pace of equity fund inflows with another $25bn this week. Equity funds have now seen cumulative inflows of $325bn since mid-April and $525bn since last November. This week, while US funds ($11bn) continued to get robust inflows, there was a notable surge of inflows into China funds ($8bn) following the stimulus announcement. Bond funds ($12.7bn) also continued to get solid inflows albeit with a divergence within, as government bond funds (-$1.6bn) saw outflows for a second week in a row but credit funds such as IG ($3.8bn), HY ($1.2bn) and EM bonds ($1.2bn) received robust inflows. Finally, money market funds ($129.1bn) received massive inflows this week, their largest in 18 months.

No let up in inflows

JPM: U.S. Fixed Income Markets Weekly (an effort to teach by / learn from reviewing bear steepening episodes throughout history)

…Treasuries October...And kingdoms rise and kingdoms fall

We think Treasury yields should be biased lower in the near-term, as a rising unemployment rate should increase the probability of a 50bp ease at the November meeting

Curve valuations appear closer to fair after adjusting for Fed policy and inflation expectations. Steepeners offer value as a way to express a bullish view, particularly given where we are in the monetary policy cycle, and how supply-demand dynamics should bias term premium higher over the medium term: initiate 3s/20s steepeners

We look deeper into bear steepening episodes. Over rolling one-month horizons, bearish steepening in 2s/10s has been more common than bullish steepening over the last 35 years. However, when we strip out the ZIRP era, we find a balance between both bullish and bearish steepening...

Bearish steepening is a less frequent occurrence at the long end, especially when we strip out the low-rate era. We identify 6 other significant bear-steepening episodes: the curve tends to steepen for 6 weeks on average, peaking a month before long-end yields do. This was evident during the 1990, 2001, and 2008 easing cycles

MS: The Inflation Ouroboros | Global Macro Strategist

Are high prices the cure for high prices or is restrictive central bank monetary policy? As central banks tried to destroy their above-target inflation tail, they may have led to the rebirth of below-target inflation – a circle of rebirth and destruction of which markets increasingly price risks.

…Interest Rate Strategy

United States | Time to pay the payroll piper

Given how most investors interpreted the FOMC's reaction function at the September FOMC meeting, and the possibility for downside volatility around a decelerating hiring trend, we continue to suggest US Treasury 2s20s yield curve steepeners and receiving the November FOMC OIS rate.

Investors should focus most on the upcoming labor market data for August (JOLTS) and September (payrolls, ADP, and unemployment claims). Our economists expect JOLTS job openings to show no further drop in August, 220k for initial claims (vs. 218k this past week), and 160k for total nonfarm payrolls (vs. 3-month moving average of 116k and Bloomberg consensus at 146k).

We discuss our revamped US rates butterfly analysis. We highlight the best butterfly structures for investors looking for higher rates into the US election (pay 3y fixed on 2s3s30s 50:50 SOFR swap butterfly), and the best butterfly structures for investors looking for lower rates (received 5y fixed on 2s5s30s 50:50 SOFR swap butterfly).

MS: US Economics: Employment report preview: Solid September

We forecast payrolls rose 160k, average hourly earnings rose 0.3%, and the unemployment rate stalled again at 4.2%. September payrolls are solid, August is revised up, and there's no sign that July weakness persists.

MS: Sunday Start | What's Next in Global Macro: Is Policy or Data More Important for Markets?

Heading into the last Fed meeting, I thought that the best short-term case for equities was the Fed delivering a 50bp cut without prompting growth concerns (see Weekly Warm-up, September 16, 2024). Indeed, Chair Powell was able to thread that needle, and equities have responded favorably. However, I still believe that over the next 3-6 months, equity performance, at both the index and sector/factor level, will be determined more by labor data than anything else.

The next round of employment data arrives at the end of this week. I believe we would need an upside surprise to drive a sustainable cyclical rotation in the US. To be specific, we think the unemployment rate probably needs to decline alongside above-consensus payroll gains, with no material downside revisions to the prior months (Exhibit 1). Beyond the labor data, I’m watching several other variables to determine the trajectory of growth.

First, earnings revisions breadth, the best proxy for company guidance, in my view, continues to trend sideways for the overall S&P 500 and negatively for the Russell 2000 small cap index and other lower-quality sectors and stocks. Seasonal patterns mean that revisions breadth likely faces headwinds over the next month.

Second, the ISM Manufacturing PMI has yet to reaccelerate after languishing for more than two years, although ISM Services has been resilient.

Finally, the Conference Board’s Leading Economic Indicator and Employment Trends Index remain in well-defined downtrends.

Overall, these data are typical of a later-cycle environment and suggest investors should stay up the cap and quality curves, despite last week’s surprise announcement of policy stimulus in China. While these actions are unlikely to materially affect US growth or labor dynamics, Materials and Industrials stocks are most likely to respond positively in the short term.

It's also important to note that the August budget deficit came in nearly US$90 billion above forecasts, continuing a string of greater-than-expected deficits this year. While fiscal policy has been substantial and positive for growth throughout this cycle, I believe it has also crowded out some of the private economy and financial markets, contributing to the K-shaped recovery we’ve seen. However, with debt/GDP near record highs and growing, inflation falling below target could call into question the deficit’s sustainability.

Avoiding a recession is desirable if the costs aren’t too high…

MS: Friday Finish – US Economics: Road to November

Markets are currently pricing even odds of a 50bp cut in November. This week's data reinforced our baseline view that inflation is soft and the real economy has momentum. The only thing to alter our view then, would be a change in trend in the data or a change in the reaction function.

Investors have been positioned for steepeners ahead of rate cuts, but prohibitive carry has made the trade painful for many market participants. Carry has now become less prohibitive, falling to less than 1bp per month for 5s30s

If the Fed is able to soft land the economy with 250bp of rate cuts, the 2s10s curve may not have much further to steepen. The 5s30s curve has lagged, and we see more steepening potential relative to other curves.

Forwards have historically been poor predictors of steepening at the start of cutting cycles, typically underestimating the amount of steepening that eventually occurred. 2s10s forwards look fairly priced relative to our forecasts, but the 5s30s curve has more room to steepen.

We like 5s30s steepeners due to their less negative carry profile and greater steepening potential, but would look to any correction flatter to enter steepeners.

The pain trade starts to work Investors have been positioning for a steeper curve ever since the 2s10s curve first inverted in mid-2022…

UBS - Interest rates strategy: After the Fed cut, now what?

Bond yields had declined in recent weeks, particularly in the front end of the curve leading up to the Fed's first 50bp rate cut at its September meeting. Going forward, we forecast that moves lower will be more moderate given the magnitude and speed of what is currently priced.

Our view currently assumes that macroeconomic fundamentals—inflation and growth—will continue to trend lower. However, the Fed will not need to maintain a 50bp cut per meeting pace. This suggests a slight recalibration of the market's shortterm rate cut expectations, though we are currently in alignment with the Fed's projections and marketimplied expectations for a 3% end point for policy rates. This should continue to exert slight downward pressure across the yield curve, along with evolving probabilities to a sharper economic slowdown

Increased volatility is expected as the November US election draws nearer. Currently, the US fiscal trajectory is on an unsustainable path, though the rates market has been more focused on Fed rate cuts and there has been strong demand for Treasury supply. However, the market's focus can quickly change and result in more term premia priced further out along the curve as policy priorities become clearer.

Wells Fargo: U.S. Consumer Has a New Lease on Life

Summary Look past the bland headline income and spending number for August to find data revisions that put the consumer on firmer footing. Income and spending are now stronger and households have been stashing away a bit more savings than previously thought.

Wells Fargo: Soft-Landing, or No Soft-Landing, That is the Question A Compendium

Summary We developed a new framework that predicts the probability of stagflation, soft-landing and recession as well as the six-months-out probability of a policy pivot and the fed funds rate up to four FOMC meetings out. In a five-part series of reports, which we collate in this compendium, we detail our methodology and share how our framework can help decision makers quantify potential risks to the economic outlook.

In all, we believe our proposed new framework would help decision makers move away from the traditional approach of just forecasting recession probability and/or GDP growth rates for the near future. In the post-1950 era, our framework effectively predicted periods of soft-landing, stagflation and recession using a threshold of 33%. While the frameworks' prediction of a recession occurring in recent years did not match with a recession occurring in the economy as of June 2024, the framework accurately predicted the stagflation episode in 2021. Essentially, concentrating on more than one risk would increase the chances of predicting potential risks to the near-term economic outlook, providing an effective tool for analysts.

Additionally, our framework accurately predicted episodes of policy pivots in the post-1990 era using a threshold of 35%. In our view, accurately predicting periods of monetary policy pivots is vital, as a rate cut that comes too soon or too late would be harmful to the economy and damage the FOMC's reputation. Given the historical accuracy of our framework, we believe it can provide useful insights for decision makers, as it can be updated in real time to gauge the likely duration of the upcoming easing cycle. Our framework also predicted the turning points in the fed funds rate, at times more accurately than the Blue Chip consensus and the FOMC'S SEP.

In conclusion, using our framework to predict potential risks to the economic outlook and utilizing those probabilities to forecast policy pivots as well as the pace of adjustments to the policy stance would help decision makers to design effective policies.

Wells Fargo: Reasons Not to Panic About Looming Port Strikes

Summary Prolonged port strikes would eventually be problematic for supply chains, but fattened inventories and a compelling case for presidential intervention suggest to us that worries of imminent disruption are overblown.

… AND more. MUCH, much more…

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

First up, GROWTH …

FRBATLANTA: Third-Quarter GDP Growth Estimate Increased - September 27, 2024

For somewhat MORE on GDP, and some snark …

ZH: Mystery Of Upward GDP Revision Solved: You Are All $500 Billion Richer Now According To A Revised Biden Admin Spreadsheet

… for even MORE on growth and a potential source of said growth …

Apollo: Goldilocks Has Arrived, but the Story Doesn't End Here

…Summing up, current economic conditions can be best described as “goldilocks.” Not too hot, and not too cold. But the story doesn’t end here. The risk with cutting interest rates too much too quickly is that the economy becomes too hot again.

See our chart book with daily and weekly indicators.

…A key indicator of inflation is the comprehensive assessment of money and credit within the economy. Logically, when this measurement exceeds normal levels, inflationary pressures become more pronounced. Observe in the chart below how global money supply is beginning to rise once more, having increased by $7.3 trillion over the past year—representing the highest growth rate in two years. We believe this rebound in money supply growth is poised to lead to additional inflationary challenges.

Disclosure: Global Money Supply as referenced in the above chart is defined in ‘Benchmark’ section below.

…In our opinion, a primary driver of the fiscal and monetary stimulus implemented over recent years—continuing today as money supply accelerates worldwide—has been the inherent upward pressure on commodity prices, which likely reached a historical bottom during the pandemic-induced market crash. We believe the likely increase in natural resource prices may serve as a critical contributing factor to the inflation narrative anticipated in the coming decade.

Disclosure: Indices referenced in the above chart are defined in ‘Benchmark’ section below…

WolfST: Consumer Income & Savings Rate Revised Massively Higher for 2 Years, Spending Revised Up Too. Stunning Numbers

Our Drunken Sailors earned and saved a lot more than we thought, spent more too, causing substantial up-revisions to post-pandemic GDP.

POSITIONS matter and some spec shorts were covered…and it would appear to me that ‘short’ has moved out the curve …

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

… Regardless how it resolves in the months and quarters to come, it feels like markets are beginning to expect higher inflation from here on. In other words, they expect the ongoing easing cycle to be inflationary. Before last week’s cut, the benchmark rates were left at a range of 525 basis points to 550 basis points since July last year. Earlier, they were tightened from a range of zero to 25 basis points in March 2022.

Since the easing on the 18th, the 10-year treasury yield has rallied 11 basis points to 3.75 percent, even as its spread with the two-year yield, which tends to be the most sensitive to the central bank’s monetary policy action, widened from three basis points to 18 basis points. The Fed is lowering short-term rates, but the long end of the yield curve is threatening to go the other way. This is precisely what non-commercials are positioned for, with net shorts in 10-year note futures near record highs.

The 10-year faces lateral resistance just under 3.8 percent. Once this gives way, there is trendline resistance at mid-4.2s from April this year, with the 200-day moving average at 4.17 percent. If bond bears (on price) succeed in steamrolling past this hurdle, then we know serious inflation worry is building.

30-year bond: Currently net short 152.6k, up 42.9k.

AND … more charts…

Sam Ro from TKer: You said you love charts. So here are more charts!

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Isn't today's Jets loss extra hilarious after a wk of delusional SB hype🤣