Good morning … Another ‘historic’ rate CUT by China overnight …

Bloomberg: China Cuts One-Year Policy Rate by Most Ever in Stimulus Drive

PBOC lowers rate of medium-term loan facility to 2% from 2.3%

MLF trim is prelude to more easing measures to lift economy

ahead of this afternoons $70bb 5yr auction, I thought a good place to start might be …

5yy DAILY: Support up nearer 3.75 and here, just ‘bout 3.45% …

… 3.45 is clearly a level of interest (lows on Monday Aug 5 and TLINE drawn up from July … of 2023) …

… for somewhat more and bit more static look at some key metrics to consider ahead of the weeks $183bb coupon supply … from someone with a Terminal and LOTS of time …

CHARTbeat: Fixed Income: Treasuries Weekly rotation of debt-based charts

… yesterday was going along just swimmingly with a concession being put into the markets early THEN … the data hit, sparking a bid for bonds, and more discussion of macro economic deterioration.

It’s with that in mind, I’d ask … did you buy a dip and will you be utilizing this afternoons liquidity event?

#Got5s?

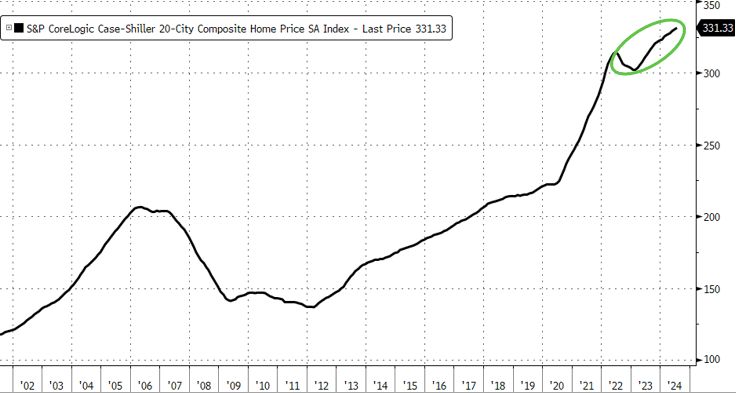

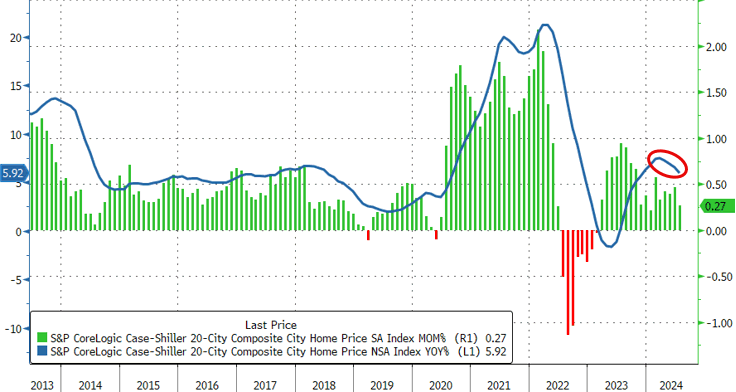

Now as the day started out yesterday … there was some, dare I say, good news … your largest asset (well, most of us anyways) just hit new record high …

ZH: US Home Prices Hit New Record High, But YoY Appreciation Slows Significantly

…US Home prices are at record highs (a great time to cut rates)...

… but it would appear that rate of appreciation, there (YoY) is slowing ‘significantly’ …

…The 20-City Composite index rose 0.27% MoM (less than the +0.4% expected), which left the YoY price change at +5.92% - its lowest since November...

Dangit!

AND there’s more (or less, depending on how we view the news) … here’s news which robbed Global Wall of concession for 2s …

ZH: US Consumer Confidence Plunges Most In 3 Years As Labor Market Weakens Significantly

… so is good news bad and bad news GOOD leading to a bid for bonds? What can / will develop today and impact 5yr? Staying tuned to find out but for now … here is a snapshot OF USTs as of 701a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: JPY lags, fixed lower after a soft UK tap, US supply & Kugler due … USTs are essentially flat, Gilts dip lower following a weak auction which also weighed on Bunds … USTs are flat/very slightly lower ahead of 5yr supply later today. Treasuries saw very modest pressure following a poor Gilt auction; a move more pronounced in Bunds/Gilts.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

About that (lack of)confidence data … can’t think of a worse combo — weak confidence AND an increase in inflation expectations …

BARCAP: September consumer confidence shows surprise pessimistic shift

The Conference Board's index of consumer confidence fell to 98.7 in September, based on weaker assessments of future economic conditions and the present situation. This comes alongside an increase in average inflation expectations to 5.2%.

Same great firm on POSITIONS of all shapes / sizes (i’ll focus on bond comments) …

BARCAP: Who Owns What: Cyclicals squeeze a pain trade

…Bonds are in demand, but combined Fed/China put may play for equities The balance of risks between growth and inflation has been beneficial to bonds more than equities in Q3, as soft activity data reignited recession fears, helping the Fed to finally join the easing cycle, but which obviously saw bonds rally/yields fall. Inflation protection has steadily gone out of vogue among investors and bonds have narrowed the performance gap with equities since the start of the summer.

Demand for bonds has been widespread, as CTAs turned long earlier in the summer and are now well exposed to the space, while they reduced equity exposure in the last couple of months. Similarly, long only investors have been diverting more flows towards bonds than equities since the start of the year.

So x-asset flow dynamics are suggesting some degree of caution…

A reminder from Citi on how it may be that 2yy are on verge of BIG MOVE LOWER … also some morning notes yesterday B4 confidence data released …

US 2y yields are edging below support at 3.55% (2023 low), and we have already seen a daily close lower. A weekly close lower resumes the 55-200w MA setup which would point to a ~50bps move lower. We discuss this and the other US yield tenors:

US 2y yields US 2y yields are peeking below an extremely important support level at 3.55% (2023 low), and we have already seen a daily close lower. IF we see a weekly close below this level, it would re-emphasise that a move lower is in the cards. With a 55-200w MA setup in play, we would expect a move towards 2.92%-3.0% range (200w MA, psychological support). This equates to another ~50bps move lower.

Weekly slow stochastics, while in 'oversold' territory, continues to tick lower, adding weight to the case for a move lower in yields.

…US 30y yields Here, the story is a little different. We have seen a 'bullish' outside week off 3.94% support (Dec 2023 low). This is a reversal indicator and suggests higher yields i the short term. However, we think we will find resistance at 4.19% (55d MA), and do not expect a large move higher in yields.

Medium term, we continue to expect a move lower as well, with 3.94% (Dec 2023 low) still being the key support level to watch.

…Conference Board vs Curve - As you may recall, the Conference Board Present Situation - Expectations spread is near and dear to us as a yield curve coincident indicator, so today’s update could provide some fundamental backing as 2s10s and 5s30s sit at fresh multi-year highs with technical indicators still constructive in the near and medium-term.

The spread between the sub-components has been widening consistently for the last 4-months (largely thanks to improving expectations), though we suspect we may see more deterioration in the present situation index going forward, given the weakening in the Univ. of Michigan data current conditions component. After Powell, Waller and Goolsbee bolstered their dovish arguments for preemptively protecting the labor market, today’s Conference Board job-availability indexes may also prove educational. The differential between the jobs-plentiful and jobs-hard-to-get components has narrowed seven months consecutively, into 2017-2018 territory and well below the 48-month moving average that usually denotes an imminent recession (as shown).

JOBS … thematic not just in the political realm but lots of snazzy visuals flyin’ around and so, as they detail MOAR need for continue rate cuts …

…US conference board consumer confidence missed, down 6.9pts to 98.7 in September, consensus looked for a small rise. Miss was driven mainly by a ~10pt drop in the present situation index, which took the index to its lowest level since early 2021. Labour market differential (plentiful less hard-to-get) fell as well, not at lowest level since 2017 when unemployment rate was at 4.4% (currently 4.2%). Cut-off for the survey was prior to the Fed's 50bp rate cut, but still surprisingly weak given the recent resilience in equities and points to labour market worries…

MORE on the (lack of)confidence data …

ING: US households are noticing the cooling jobs market

The latest Conference Board consumer confidence report suggests households are noticing the jobs market is cooling quickly. Historically this has been a major warning signal that unemployment is going to rise. This report suggests a breach of 5% is possible before year-end, which would undoubtedly raise the odds of a second 50bp Fed rate cut

Consumers are feeling a cooler jobs market, which points to further rises in the unemployment rate

AND in case you hadn’t heard …

Wells Fargo: Consumers Remain Downbeat About Jobs Market

Summary Consumers are worried about the jobs market and that's weighing on overall moods. Consumer confidence remains within its narrow range of the past two years, though there are some glimmers of hope about expectations for lower interest rates…

…While we expect there are a number of reasons households are growing more pessimistic, the moderating labor market remains top of mind. The labor market differential, which is the difference between the share of consumers who view jobs as “plentiful” less those who view jobs as “hard to get,” also fell to its lowest reading since March 2021 (chart). The persistent drop in this measure is a clear sign that the labor market is not nearly as tight as it once was. That said, we're hesitant to put too much weight on this data given broader confidence measures have remained depressed this cycle despite resilient spending habits of households.

Same shop with an updated framework writeup predicting Fed Funds which concludes that this model better than any OTHER one you’ll find … obviously …

Wells Fargo: The FOMC, Blue Chip or the New Framework: Predicting the Fed Funds Rate

Summary

This installment presents a new framework to predict the level of the fed funds rate two quarters out.

We compare our framework’s fed funds forecast with the FOMC and Blue Chip forecasts to decide who is more accurate at predicting the near-term fed funds rate.

The framework effectively predicted the turning points in the fed funds rate in the simulation analysis.

The FOMC started providing the SEP in 2012; therefore, we employ the 2012-2024 period to identify whose fed funds rate predictions are the most accurate.

Blue Chip has a higher perfect forecast accuracy rate (67%) than the FOMC (58%).

The FOMC’s average forecast error is slightly lower (21 bps) than the Blue Chip consensus average error (29 bps).

Both the FOMC's SEP and the Blue Chip consensus missed the 2019 rate cuts.

With the September rate cut in the books and high expectations of more rate cuts in the remaining meetings of 2024, both the FOMC and the Blue Chip forecasts suffer a lower average forecast accuracy and a higher average forecast error.

Given the historical accuracy of our approach, we believe our framework would be helpful for decision makers to improve their forecast accuracy.

We also propose that instead of following the traditional approach of forecasting the near-term fed funds rate, forecasters should consider predicting policy pivots in addition to the fed funds rate.

… and why predicting FF is important? Welp, commercial RE clients payin’ attention …

Wells Fargo: Is the Tide Turning for Commercial Real Estate? Easier Monetary Policy Lays the Foundation for Recovery

Summary The Fed Plants the Seeds for a CRE Recovery

The Federal Reserve's 50 bps cut at the September FOMC meeting marks the beginning of the end of the worst CRE downturn since the Global Financial Crisis. Given inflation appears contained and strains are emerging in the labor market, we expect the Fed to follow with a string of rate cuts through the summer of 2025 in order to keep the economic expansion intact.

Lower interest rates are not a magic bullet, but less restrictive monetary policy lays the groundwork for a commercial real estate recovery. Decreased long-term interest rates appear to be easing upward pressure on cap rates and slowing declines in property valuations. Meanwhile, increased expectations for an economic soft-landing look to be giving capital the green-light to move off the sidelines. There's no shortage of obstacles ahead, especially when it comes to the office market. That said, reduced interest rates should prevent distress from spreading and shorten the hurdles coming down the road.

… right. got it. noted. lower rates = higher prices. of just ‘bout everything …

Bloomberg: Traders Boost Fed Bets With November Cut Size Seen as a Tossup

Positions added in 2-year and SOFR futures since Sept. 18

Two-year futures’ December contract has most open interest yet

Simon (White) SAYS …

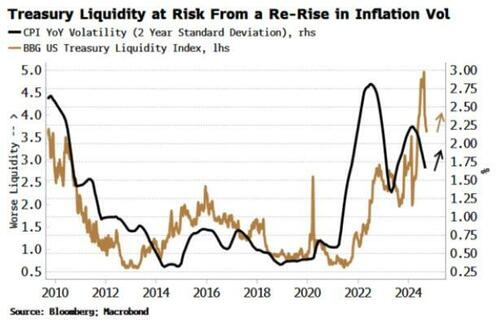

Bloomberg: 'Fool In The Shower' Fed Fiddles While Bond Bears Burn

… Liquidity in the Treasury market also faces a more torrid outlook due to the upward risks to inflation volatility and term premium. Bloomberg’s Treasury Liquidity Index recently reached new highs, indicating poor liquidity in the Treasury market. It has since come off those highs but remains as elevated as it’s been for most of its 15-year history.

Some of the index’s recent rise may have been due to an anomalous reason — some 30-year bonds issued when the US was running a budget surplus in the late 1990s are very illiquid, with their yields trading expensively to the fitted yield curve, which pushes the liquidity index higher. Regardless, liquidity risks are fated to start rising again after the Fed’s easing sets up greater inflation vol.

Rising inflation risks would be enough for the Treasury market to contend with, but it comes at a time when the government is running annual fiscal deficits of $1.5-2 trillion that are not expected to ease off over at least the next decade…

AND back TO ‘officials’ who are thinking and writing about month-end specifically about UST market LIQUIDITY in / around that time of the month …

… Moreover, this end-of-month liquidity improvement has been increasing in magnitude over time, in a manner akin to that for trading volume, as shown in the next chart.

Similar but weaker patterns are observed for other measures of market liquidity. Quoted depth at the inside tier has been about 6 percent higher on the last trading day of the month since 2020, on average, implying better liquidity, as compared to 9 percent lower between 2005 and 2009 (percent differences are first calculated for each of the two-, five-, and ten-year notes, and then averaged across them). Bid-ask spreads have been about 1 percent narrower on the last day of the month, on average, suggesting slightly better liquidity, as compared to 2 percent wider between 2005 and 2009. The weak end-of-month effects for spreads in particular are likely attributable to minimum tick sizes, which cause spreads to vary little outside times of market stress (see this paper, for example).

…Implications Based on this post’s findings only, one might conclude that the last trading day of the month is an especially good time to trade because of the day’s higher trading volume and lower transaction costs. However, the evidence of periodicity in returns from other studies suggests that advantageous times to trade vary for other reasons and differ between buyers and sellers. These monthly patterns also change over time, as shown in this post, warranting close watching of these patterns going forward.

That's quite a report from 1-26-21, looking forward to reading that when I return to my 'screen' on Friday....

Anyone else hear the big guy in Israel wants to ban individuals from owning/possessing gold-silver-cash? What happens 1st in India (banning cash and CBDC instituted) and Israel (vax-passport) eventually lands upon US/EU shores....

A report from the field in my little corner of NE Cali, Susanville to be exact. Last Friday, starting my mtn biking trek to the trails, just happened to notice a large white charted bus in the parking lot of the Social Security Admin Building. No Haitians or roasted pets BUT, lots of Hispanic women & children looking quite lost wandering about the parking lots. Later up the road saw some of the men walking to hotels or their work assignments. No factory workers to displace here (the mills are LONG abandoned), but lots of alph-alpha fields and ranches about.

That's quite a report from 1-26-21, looking forward to reading that when I return to my 'screen' on Friday....

Anyone else hear the big guy in Israel wants to ban individuals from owning/possessing gold-silver-cash? What happens 1st in India (banning cash and CBDC instituted) and Israel (vax-passport) eventually lands upon US/EU shores....

A report from the field in my little corner of NE Cali, Susanville to be exact. Last Friday, starting my mtn biking trek to the trails, just happened to notice a large white charted bus in the parking lot of the Social Security Admin Building. No Haitians or roasted pets BUT, lots of Hispanic women & children looking quite lost wandering about the parking lots. Later up the road saw some of the men walking to hotels or their work assignments. No factory workers to displace here (the mills are LONG abandoned), but lots of alph-alpha fields and ranches about.