Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

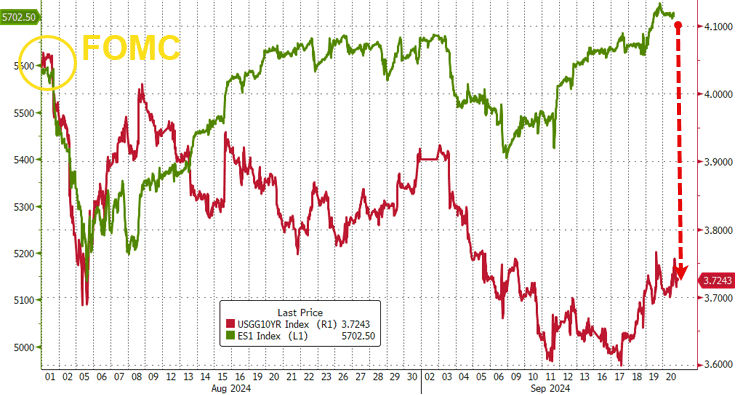

Bonds bought the rumor and appeared to have sold the fact. Rates were cut and yields offered an underwhelming reception (5yy were UP about 7bps on the week — perhaps a concession for this weeks supply?) …

I was heartened to hear / read / listen to some of the best in the business express SOME amount of caution with regards to this past weeks larger than life rate CUT, an emergency cut without an emergency and the largest cut in 32yrs with financial conditions as loose as they are right now …

… and as we reflect on the recent price action … it strikes us that policy rates are down, Treasury yields are UP, and stocks are at record highs, leaving only one real question … What could possibly go wrong from here? -BMO

The caution was to be a tip of the hat and suggestion that rate cuts with stocks at / near ATHs, well, what could possibly go wrong (reflation coming back?) … more at this weekends note concludes but perhaps as far as bond jockeys may have been concerned, this weeks events were a classic buy-the-rumor and sell-the-fact.

Furthermore, with the larger than life rate CUT (needed or not) there was a dissenting (in favor of ‘just 25’ bps) vote. Michelle Bowman’s voice (of reason?) may just be worth pausing and considering …

On Wednesday, September 18, 2024, I dissented from the Federal Open Market Committee’s (FOMC) decision to lower the target range for the federal funds rate by 1/2 percentage point to 4-3/4 to 5 percent. As the Committee’s post-meeting statement notes, I preferred to lower the target range for the federal funds rate by 1/4 percentage point to 5 to 5- 1/4 percent…

… I agree that at this meeting it was appropriate to recalibrate the level of the federal funds rate and begin the process of moving toward a more neutral policy stance. In my view, however, a smaller first move in this process would have been a preferable action.

The U.S. economy remains strong ... Although it is important to recognize that there has been meaningful progress on lowering inflation, while core inflation remains around or above 2.5 percent, I see the risk that the Committee's larger policy action could be interpreted as a premature declaration of victory on our price stability mandate. We have not yet achieved our inflation goal. I believe that moving at a measured pace toward a more neutral policy stance will ensure further progress in bringing inflation down to our 2 percent target…

… Worth noting the last dissent from a Governor prior to this week's was Governor Olson in September 2005 because he thought hiking in the aftermath of Hurricane Katrina was a bad idea. Prior to that, you have to go back to Governor Gramlich in 2002.

That said, a quick look at belly (5s) given ($183bb coupon) supply in the week just ahead …

5yy WEEKLY: 3.50% clearly presents itself as a level to watch …

… as yields falling into what appears to ME to be familiar territory … noting, too, as yields drop, momentum (stochastics) remain very overBOUGHT …

… think concession for the belly? I realize everyone’s remaining in / on Team Steepener and more power to ‘em … last year they stuck with it and maybe just maybe this trade will start to ignite.

As the week came to a close, interesting to note what’s happening with rate cut expectations and so …

ZH: Gold, Oil, & Crypto Soar As Fed Slashes Rates With Stocks At Record Highs

"everything is awesome"... so awesome The Fed needed a crisis-like 50bps cut to keep it awesome!

…Stocks are at record highs (no landing at all); home prices are at record highs (and rising fast); and US macro data has dramatically surprised to the upside since the last FOMC meeting...

...but bonds are 35bps lower in yield (recession)...

…But there's no recession ahead according to stocks, despite the market pricing in massive rate-cuts...

The yield curve dramatically bear-steepened this week to its steepest since May 2022...

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW …

THIS WEEKEND, here a few things which stood out to ME from the inbox …

First, THE bank of the land offering a couple notes on ‘recalibrate’ as well as an annotated look at FedFunds (opposite end of scale — annotated 10yy offered HERE on Fri ) …

The View: My kingdom for a dual mandate Fed aiming to reduce hard landing risks, ECB risking a more persistent inflation undershoot. Watch PCE for GDP tracking more than for inflation. SNB likely to cut, RBA likely to hold. LDP leadership election in Japan could have a bigger than expected curve impact.

Rates: Hawkish 50? Not so fast. Fed = dove coop US: Fed is dovish. Stay bullish duration and in steepeners. We add M5-Z7 steepener. We revise rate forecasts lower with faster Fed cuts. QT end pushed to Q1 ’25…

…New Fed call & US rate forecast revisions Our US economics now expect faster & deeper Fed cuts (see Sept FOMC). They expect another 75bps in ’24 (Nov = 50, Dec = 25, end Dec ’24 FF = 4-4.25%), 125bps in ’25 (Jan/Mar 25 each, 3 quarterly 25bp cuts after, end ’25 = 2.75-3%). The see a modest economic, labor, & inflation rebound in 2H ’25 & ’26.

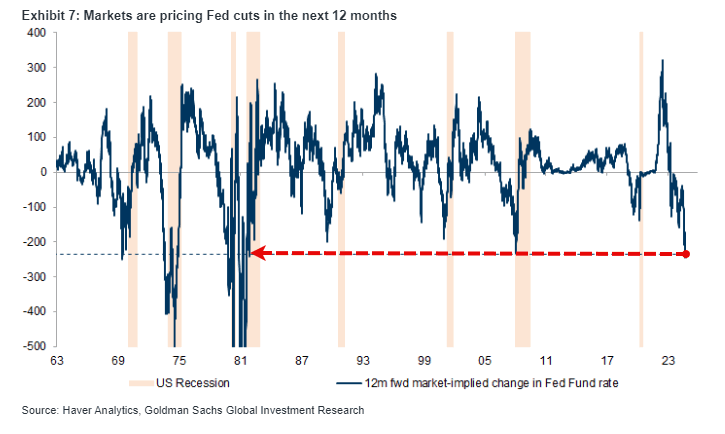

We revise our rate forecasts accordingly (Exhibit 7). Our new 2Y & 10Y: end ’24 = 3.1 & 3.5, end ’25 = 3.2 & 3.6. Our forecasts are below the forwards & below consensus near term. Our 2Y end ’25 forecast includes some expectation for future rate hikes given solid US economy & inflation re-acceleration risk. Our long end forecasts include gradual cheapening & higher rates to reflect tighter spreads & supply / demand issues. We also push out our QT stop from end ’24 to end Q1 ’25 (for detail see US front end).

Bottom line: Sept FOMC was dovish to us & implies lower FF. Lower FF = bullish bonds. We recommend M5-Z7 SOFR curve steepeners for cut front loading & solid economy. History also says Fed front loads. Forecast changes: rates slightly lower & below forwards; QT end timing is pushed out to end Q1 ’25.

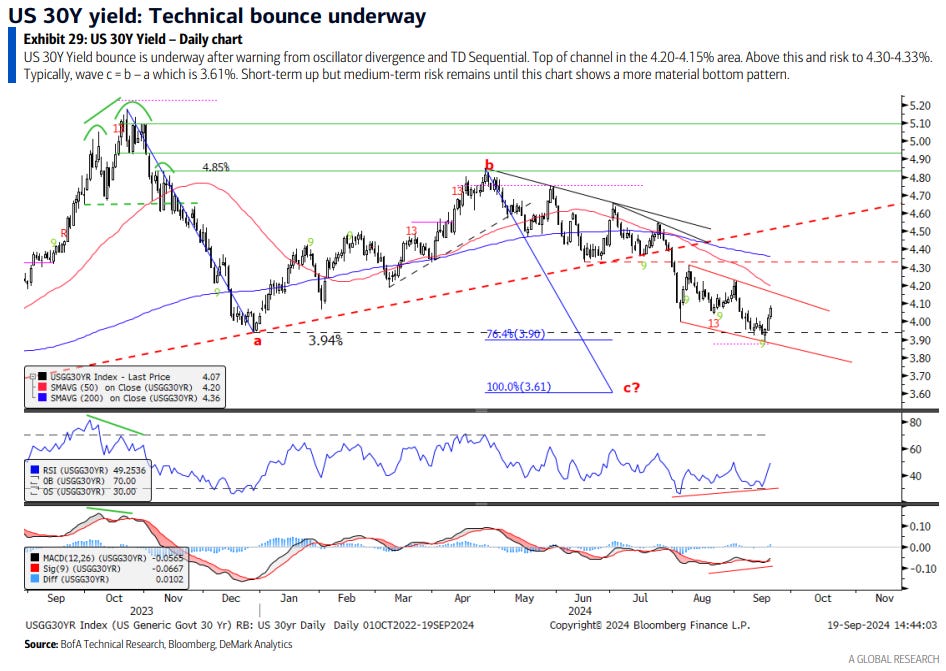

…Technicals: US yields bounce from key levels Oscillator divergences and TD Sequential warned a bounce in yields was a risk into the Fed. This is underway and for now is a bounce, unless bottom patterns form.

… The Biggest Picture: Wall St loves “panic cuts” when no panic (Chart 2); 50bps as Fed wants to slash real rates to prevent recessionary small biz sector cutting jobs (Chart 3); Wall St chase says Fed “ahead of curve” and 250bps cuts = 15-20% EPS growth in ‘25; best “soft landing” plays = international stocks & commodities; we use rip to buy dips in Bonds & Bullion to hedge recession & inflation “tails”.

… and there’s really no doubt about this next note / title as the Fed certainly did get off to a strong start … the bit about POSITIONS (which you know I firmly believe matters) caught my eyes …

In the US, we maintain our recommendation of paying 5y5y on a cross-market basis, as the Fed’s reaction function along with robust activity continue to argue for higher far forward rates. In Europe, we view the outlook for rates as asymmetrically bullish. In Japan, a Takaichi-led LDP could dampen BoJ rate hike expectations.

… Third, macro HF/CTA positioning is quite long duration, the catalyst for a large rally is fading and we could see unwinding of these positions. Figure 16 shows that our empirical proxy for positioning is quite long (roughly the same as it was coming into the year). Figure 17 shows that data surprises are turning around and could potentially turn positive given FCI has been easing for some time.

The Fed initiated its easing cycle with a 50bp cut, signalling its focus on achieving a soft landing. The BoE and BoJ stood pat, as expected. Next week, US PCE, European PMIs and Japan's election are key as markets assess the Fed's next steps, chances for an October ECB cut, and the future of BoJ policy normalisation.

…US Outlook Recalibration... at a cost The FOMC delivered a 50bp "recalibration" to the policy rate, while leaning against hopes for an expeditious descent to long-run neutral. This "hawkish 50" likely came with the cost of heightened sensitivity to financial press noise during future blackouts. With easier financial conditions ratified, we upgrade our outlook.

Best in the strategy biz doesn’t need much of a reason for you to pause and click through BUT for those wanting to hear in his own words, well … scroll all way to bottom for the weekly pod. For now, though …

… This week's economic data calendar doesn't hold any particularly consequential information as it relates to near-term monetary policy expectations which will leave the market primarily focused on the implications of supply and the return of Fed-speak in earnest. The cluster of talking Feds will help shed some light on the FOMC's decision to lower rates by 50 bp and signal another 50 bp of cuts by year-end. Broadly speaking, we anticipate that policymakers will frame the Fed's outsized cut as a risk-management decision that was aimed at preserving the health of the labor market and a healthy pace of growth.

In other words, we suspect the Fed-speak will frame the 50 bp cut as a proactive move that will transition into a more measured pace of 25 bp moves as the data warrants further action. Powell made it clear the pace of rate cuts moving forward will depend on the way the economy evolves – so even if the Fed-speakers don't offer any explicit guidance on the rate cut outlook, their views on the current and future balance of risks will be relevant to policy expectations over the coming months and quarters…

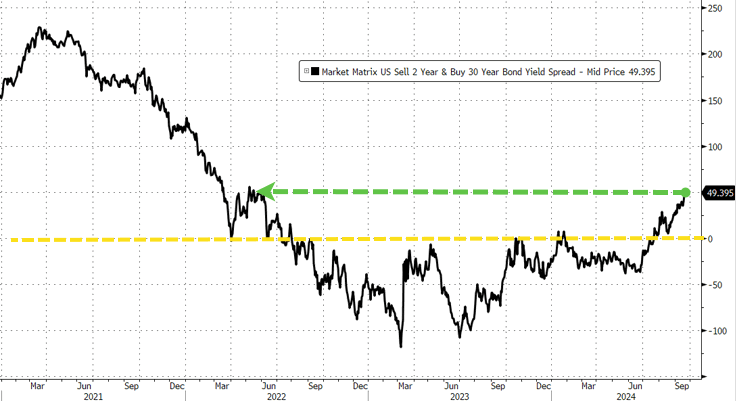

Large French Open sponsoring bank has a great chart and some context on money mkt mutual fund flows and the yield curve and so, as it is finally the year of the curve steepener (it is, right?) …

…Curve steepening has been a better real-time indicator of MMF outflows, relative to rate cuts. We find that a steeper 3m10Y UST curve tends to be associated with outflows from Money Market Funds. As an approximate guide, we find that historically MMF AUM growth has inflected negative when the 3m10Y steepens to at least 100bp or more. Putting this threshold into context, the current 3m10Ys is -123bp. Looking ahead, BNPP’s Markets360 Rates forecast into year-end 2025 implies 3m10Y at +20-40bp. In the past, the 20-40bp 3m10Y level has been associated with limited outflows from Money Market Funds.

I don’t pass these notes / thoughts along all the time but I do ALWAYS read through weekly from DB and this week they’ve had quite a few things which caught my eyes. IF you have access, might be worth a point / click … here’s couple thinks I’m re/reading (and clearly the updated f’cast ALWAYS a reason to pause …)

…US rates forecast update Following this week’s Fed meeting, we update our UST rates forecast to reflect a more rapid cutting cycle. In line with the US Economics team’s revised fed funds rate path, our baseline forecast assumes a string of 25bp cuts through March followed by quarterly cuts that bring the fed funds rate to its longer-run level of 3.25- 3.5% next September. Our assumptions on term premia are not materially changed.

The updated forecast puts 2y and 10y UST yields in the middle of next year at 3.50% and 4.05%, respectively. Yields across the curve are projected to be 30-50bp above forwards in the middle of next year, driven by a higher expected fed funds rate path and term premia compared to market pricing. Viewed through the lens of this updated projection and the alternative low-rate scenario in our previous forecast, the market is currently pricing around a 60% probability of a soft-landing.

Risks to this baseline (modal) forecast are skewed to the downside, given the significant possibility that continued labor market cooling could precipitate additional 50bp Fed rate cuts and a reduction in the fed funds rate through neutral. Upside risks stem from easy financial conditions and the possibility that inflation settles at an uncomfortably high level for the Fed, as well as prospects that the upcoming US election produces bigger budget deficits and more inflationary trade, immigration, or regulatory policies.

… Extreme CTA positioning adds bearish technical pressure for US rates

CTA funds are very long US rates

DB Investor Positioning and Flows - Inflows Surge, Positioning Edges Higher

While I cannot wait to see this next groups equity writer and his weekly warm up reflexing TO 50bps CUT, a couple other divisions have some insights …

MS: Ground Control to Major Dove | Global Macro Strategist

Take your rate cuts and put your helmet on. Ground control to Major Dove. Commencing countdown, easing on. Ground control and Major Dove want a soft landing. More dovishness could come from weaker inflation, a weaker labor market, or both. That skew of risks keeps us in UST yield curve steepeners.

Interest Rate Strategy United States We suggest investors remain in UST 2s20s yield curve steepeners – a position that an expansion of front-end negative risk premiums should benefit. In addition, we suggest investors maintain an outright received fixed position in the November FOMC OIS rate.

We think investors will be sensitive to any additional downside volatility in employment data, given Chair Powell's comments in the press conference. In addition, we think investors will be sensitive to any downside volatility in inflation data, given Governor Waller's comments on Friday.

A government shutdown beginning after September 30 is not our base case, but the risk would become bigger if Congress does not pass its annual funding bills as we approach the end of the month. Background reporting indicates that the House of Representatives plans to move ahead with a clean three-month stopgap funding bill that will keep current levels constant until mid-December.

In the event of a shutdown, our economists see a 0.05ppt drag to GDP per week that the shutdown endures. We also note there are some critical indirect impacts of shutdowns that can delay routine government operations (in particular data releases that markets pay close attention to, as we note here.

Recalibrations The 50bp rate cut showed that the Fed is ready to react to weaker data. Softness in the labor market is impossible to ignore, but strong consumer spending still paints the picture of a solid economy. We expect a string of 25bp cuts through the June FOMC unless employment weakens substantially…

…The dot plot and the dissent collectively indicate that a 50bp cut was far from unanimous. The dots imply that 9 of the FOMC participants did not want to cut 50bp this year, and only one dot implied two 50bp cuts this year. This meeting was not the tipping point for an accelerated cutting cycle. The revisions to the economic variables were similarly muted. Effectively, the forecast for unemployment was revised up two-tenths across the forecast, notwithstanding this year’s mark-to-market four-tenths revision. Similarly, inflation forecasts were revised down, but neither change indicated a fundamental rethink. Chair Powell used the word “recalibration” more than once, and while we think that term is apt, it may even overstate the change…

…So, our baseline view is that the 50bp cut this week will prove to be a one-off event, and subsequent cuts will be 25bp. Chair Powell said at the press conference that no one should infer that 50bp is the expected pace of cuts, but of course, when the Fed was hiking and increased rates by 75bp, he similarly said that no one should expect that increment to be the new baseline. When the facts change, so will actions. We think there is clearly scope for more 50bp cuts. Though the threshold is a bit murky, conditions are weakening in the labor market. Our baseline payrolls forecast has a bit of an uptick from the last reading, hence we look for 25bps. The strike at Boeing (30k) and the threatened port strike (45k) could slow payrolls. But if we get a number closer to 100k excluding strike effects, then Powell’s determination not to fall behind the curve will be brought to the fore.

Even those up NORTH the border are mildly revising outlook …

… We have modestly revised our rate forecasts following the larger 50bp rate cut at the start of the cycle, but continue to expect lower rates and a steeper curve as the year proceeds.

AND those with the covered wagons out with an updated f’cast so as NOT to be left out of the conversation …

United States: Recalibrating the Monetary Policy Stance The commencement of monetary policy easing comes at a time when overall economic growth remains solid, supported by stronger-than-expected retail sales, industrial production and residential construction in August. Yet, signs of labor market weakness have posed meaningful threats to the sustainability of growth, which underpinned the FOMC's decision to start the easing cycle with a 50 bps cut, rather than a conventional 25 bps move

…Interest Rate Watch: An Update to Our Fed Funds Forecast The Federal Open Market Committee (FOMC) opted to reduce the target range for the federal funds rate by 50 bps at its meeting this week. Based on what we know now, we believe the FOMC probably leans toward downshifting to a 25 bps pace going forward. Accordingly, we look for the FOMC to cut the federal funds rate by 25 bps at each of its two remaining meetings of the year…

…Looking ahead to 2025, we expect the string of 25 bps rate cuts to continue. We project five 25 bps cuts from the start of the year through the summer, such that in one year's time the target range for the federal funds rate will have returned to 3.00%-3.25%, our current estimate of the neutral rate. Gradually removing policy restrictiveness should help keep inflation in check, while transitioning back to a more neutral policy setting will help keep this economic expansion going…

… AND more. MUCH, much more…

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AND a quick weekly read-through from the good Dr Torsten Slok, formerly of DB and now with PE shop …

… With financial conditions easing further because of the 50bps Fed cut and still strong tailwinds to economic growth from the CHIPS Act, the IRA, the Infrastructure Act, strong AI spending, and strong defense spending, the bottom line is that there are no signs of the economy entering a recession. And because of these tailwinds, there are no reasons to expect a recession. On the contrary, the incoming data seen in our chart book (available here), in particular jobless claims and the Atlanta Fed GDP Now, are pointing to a reacceleration in employment growth over the coming months…

… he reports, WE decides …

POSITIONS matter and while NOT ALL positions are created equally (some, for what its worth, had record LEVERAGED bets on 50 … ) and so … another expression of a record speculative position … this time further OUT the curve …

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

… think ‘bout these positions as they peacefully coexist (perhaps funding one another and morphing themselves into … bullish STEEPENER?)??

Macrobond puts out some decent work and all the cool kids use the software and I’ll admit … i was never and am still NOT very cool. Never used it always ALWAYS said if I was paying for Terminal license the princely sum, it best be able to do everything AND make coffee in the morning … that said, a weekly blog / chart for your review…

By Simon White, Macro Strategist, Bloomberg The market is now considering a recession as its base case. Secured Overnight Financing Rate (SOFR) options, which assume a hard landing to be likely and a Federal Funds Rate of 3% or below by next June, now see a downturn as having a 50% probability. However, that's too pessimistic a view based on the data, which show a low chance of recession over the next three to four months.

…Loosening financial conditions may delay rate cuts

By Diana Mousina, Deputy Chief Economist, AMP The Goldman Sachs Financial conditions index is a measure of overall financial conditions using market-based indicators, with different weights across countries depending on the structure of their economies.

An index above 100 indicates that financial conditions are tighter than long-term “normal” for that country, while an index below 100 indicates conditions are looser than “normal.” In the current environment, despite significant tightening in monetary policy across major economies such as the US and Australia, financial conditions have not tightened considerably relative to historical levels. And more recently, conditions have loosened again, driven by lower market volatility, rate cuts priced in by financial markets, and better equity performance.

This recent loosening in financial conditions could argue against significant interest rate cuts from central banks in the near term. But bear in mind that while financial conditions indicators are a good gauge of market conditions, they are less of a guide to actual economic conditions.

Here’s very comprehensive run through of the week just past and of the rate CUT, bringing forward couple visuals I thought worthwhile (I hope you’ll forgive me here as I am straying a bit off the RATES CENTRIC reservation)…

… The Federal Reserve has historically cut rates as economic growth declines and unemployment increases. (Note: It appears that aggressive Fed rate-cutting cycles coincided with recessions; however, there is about a 9-month lag between the initial rate cuts and recession recognition.)

With this understanding, analysis of the historical relationship between rate cuts and market returns is worthwhile…

… The crucial point is not whether the Federal Reserve cuts rates further but economic growth and its impact on earnings. As shown, there is a high correlation between the annual rate of change in the S&P 500 versus the annual growth in earnings.

The onset of a recession, or even a more aggressive economic slowdown, becomes the most significant risk. Given that earnings are derived from economic activity, any slowdown in consumer demand results in lower earnings. This is because …

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Finally, from BMO, a few AUDIO words in effort to bring their research (above) to life. Listen, subscribe, etc … you’ll thank me for it and be far better off …

Powell's half-point cut has left us humming the tune to the late-60s classic “First Cut is the Deepest” – written by Cat Stevens... who knew? It was originally released by P.P. Arnold and also became a hit single by Keith Hampshire, Rod Stewart, Papa Dee, and Sheryl Crow. Truly, this leaves only one lingering question - when will the former Fed Vice Chair release his version of the classic? We suppose it is prudent to see the size of November's cut before embracing the lyrics.

Episode 292: "The Journey to Neutral" is now available. This week, the team discusses the 50 bp rate cut and the implications for the forward path of policy rates. We also contemplate the debate surrounding the reflationary risks associated with the process of normalization with a backdrop of a still-resilient labor market and solid consumption.

If you haven't listened or subscribed yet, please do so at the links below or search for "Macro Horizons" on your favorite podcast app.

… and as we reflect on the recent price action … it strikes us that policy rates are down, Treasury yields are UP, and stocks are at record highs, leaving only one real question … What could possibly go wrong from here?

… Best in biz basically sayin’ …

… tell you what I’m not worried but then, how’s about P Diddy … think HE be worried yet ??

THAT is all for now. Enjoy whatever is left of YOUR weekend …

what…me worry? | technolandy: site of Ian Landy")

Mad Magazine and Alfred E Neuman, I remember those days, fondly...

Spy vs Spy....

Great Satire.....

https://schwab.com/learn/story/what-fed-rate-cut-means-with-claudia-sahm