Good morning … Bonds are aggressively UNCH and so I’ll lead with a look at 10s to consider (and note I may NOT have time this weekend for an update) …

10yy WEEKLY: I’m watching weekly close in / around 3.64% …

… momentum remains overBOUGHT and so, some time at a price incorporating various inputs (stimmy near and far, ‘flation, etc…) will determine the whatever next

… Good morning and especially from those in China …

Bloomberg: China’s Biggest Stock Buying Frenzy in Years Overwhelms Exchange

… Authers’ today nails it asking …

Bloomberg: Markets Suddenly Trust China Again, Up to a Point

The Politburo’s economic plans have a welcome impact for investors. The proof will be in what gets achieved with consumers.

… The CSI-300, an index of the biggest mainland A-shares traded in Shanghai and Shenzhen, has rallied by more than 10% this week, and it’s nearly back to its high for the year:

That rally extended Friday after the central bank confirmed it was cutting the reserves thatbanks must hold, with the CSI-300 gaining another 2.7% in the morning session. This must of course be put in the context of a biblically awful run for Chinese equities since a brief boomlet ended early in 2021. The index fell more than 50% after that — although it’s still noticeable that the CSI-300 is now further above its 200-day moving average than at any time since then, which does suggest a significant reversal:

It’s also had a real impact on equities beyond China’s borders, helping in particular to spur excitement outside of America. FTSE’s index of all world markets excluding the US has rallied within a whisker of its high from 2021:

Back to this side of the globe where the day yesterday ….

ZH: Initial Jobless Claims Drop Back Near Multi-Decade Lows ZH: Final Q2 GDP Beats Estimates On Inventory, Government Boosts; Second Half 2023 Revised Lower

… these set the table for liquidity event …

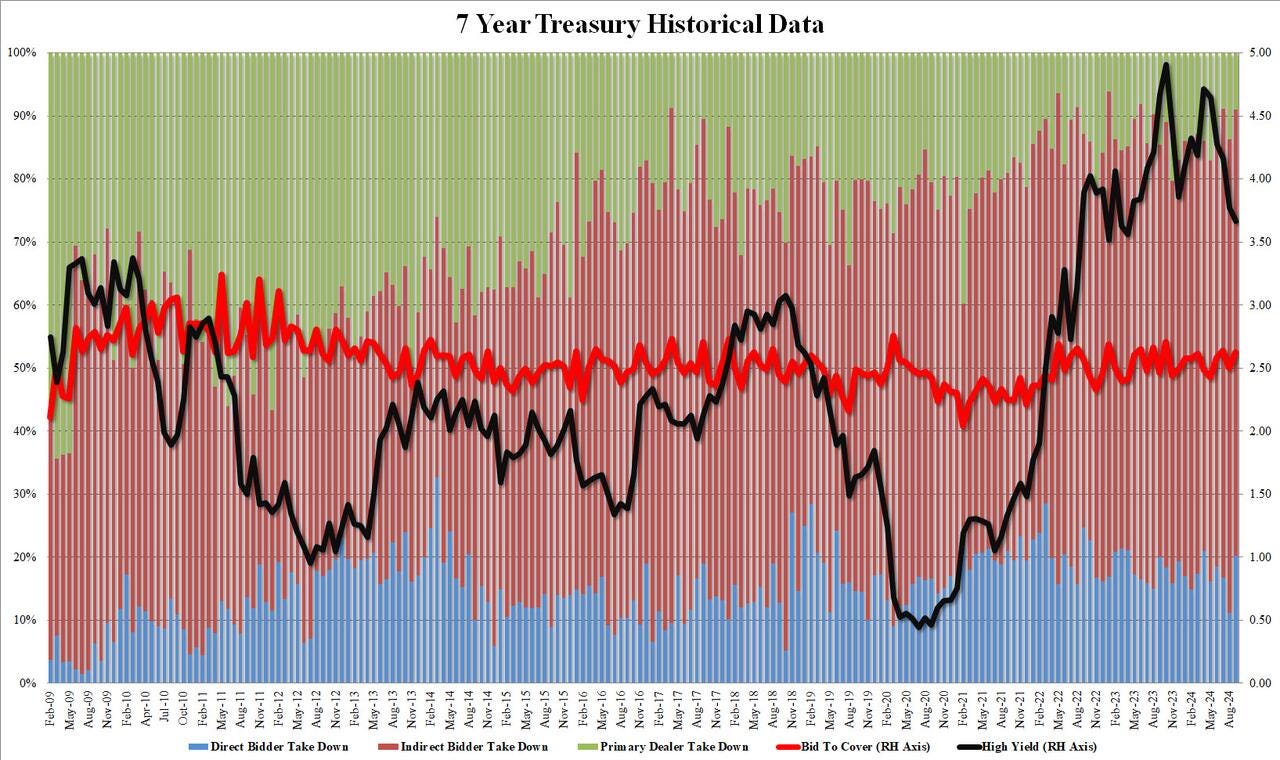

ZH: Solid 7Y Auction Stops Through Despite Drop In Foreign Buyers

The internals were average, with Indirects taking down 70.8%, the lowest since June if just above the six-auction average of 70.1%. And with the Directs take downjumping to 20.3%, from 11.2%, Dealers were left holding just 8.9%, a drop from 13.7% last month, and one of the lowest on record.

Overall, this was a solid, if not stellar, 7Y auction and one which clearly took advantage of the concession in today's modest selloff which pushed yields near session highs ahead of the auction deadline.

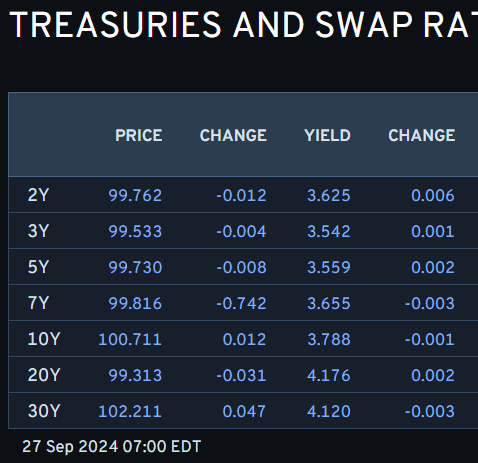

… which then brings us to the here and now and SO, here is a snapshot OF USTs as of 700a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Japan elects hawkish candidate, ECB rate cut bets rise, PCE due … USTs are firmer but to a lesser extent than peers given that price action on the other side of the Atlantic is more a by-product of EZ-specific events. From a US perspective, attention will be on the August PCE data. The 10yr yield is currently tucked within yesterday's 3.754-3.821% range.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Starting with a question …

ABNAmro: US - Fed cuts by 50 bps, recession imminent?

The Fed decided on a 50 bps cut to initiate its easing cycle. Outsized rate cuts are usually reserved for cycles where recessions have started or are imminent. There are pockets of weakness in growth and the labor market, but risks of a recession remain contained.

A couple things on CHINA (and perhaps impact on US…)

September's Politburo meeting reinforced expectations that China is likely to pull the fiscal trigger soon. We discuss what we see as an effective policy package to reverse deflationary expectations and the downward economic trend, and explore two scenarios to assess the economic implications of a bigger fiscal stimulus.

BARCAP U.S. Equity Strategy: Food for Thought: A Boost From Beijing

Chinese regulators surprised the markets with a package of policy easing actions. Both Chinese equities and US stocks with exposure to China had strong positive reactions to the news, notably led by Discretionary exposure, despite our macro colleagues' belief that the boost to China's real economy is likely to be limited.

BNP: China equities: Bolder stimulus expectations, adopting bull case scenario

Chinese equities surged on Thursday with an elevated turnover following the strong pro-growth tone in the September Politburo meeting. Given the stronger policy support, we adopt our previous bull case scenario (65) as our new end-2024 target on MSCI China.

The sustainability of the rally still depends on the coordination of the fiscal policy stimulus and monetary easing execution that may bring improved corporate earnings. Further, there’s a risk of profit-taking as we approach the US election (tail risk of large tariff)…

China has delivered a potential policy game changer, with stronger-than-expected stimulus ranging from monetary to property and capital market measures followed by a surprise September Politburo meeting that directly pledged to stabilize the property market.

We recommend investors add quality internet and consumer stocks to the growth side of a balanced barbell approach, given that more broad-market upside is likely.

Within China credit, we like high-beta SOEs and central SOE perpetual bonds for yield pickup, and select Macau gaming bonds for decent carry.

We revise our USDCNY target to 7.2 (from 7.3) for December 2024, and 7.0 (from 7.2) for March, June, and September 2025. The US election remains a key risk for the CNY over the next six weeks.

On that GDP revision …

BARCAP: GDP Annual revision: Game and set to the soft landing camp

The BEA's latest annual revision portrays an economy that has been expanding even faster in recent years than previously thought, and generating substantially more income to support household spending. Stronger income fundamentals boost our conviction that a soft landing is on track.

‘Bout NEXT weeks NFP report…a couple notes as they are starting to drip in …

BARCAP: September employment preview: The calm before the strike effects

We expect a 150k increase in nonfarm payroll employment in September, slightly faster than August's 142k gain, with average hourly earnings rising 0.3% m/m (3.8% y/y). On the household side, we look for the unemployment rate to remain at 4.2%.

We estimate payrolls will expand by 150k in September as the unemployment rate remains unchanged at 4.2%.

We expect the US labor market will allow the Fed to continue its cutting cycle at a measured 25bp pace, after last week’s initial 50bp adjustment.

The bar remains low for a more aggressive move, so we outline some labor market thresholds that we expect would trigger another outsized cut.

I despise over promising and under delivering and it feels like thats where we are, economically speaking …

ING: Rates Spark: Markets are positioned for disappointment

Data still determines direction. But markets seem positioned for disappointments that, on balance, are not there yet. With next week's payrolls data looming large, we don't expect larger moves just yet. Today's key data is the core PCE deflator, which should confirm that inflation is no longer standing in the way of Fed cuts

US Treasury curve dives into cuts and risks being caught by upside surprises While markets are prepared for more US data disappointments, the durable goods orders and jobless claims both performed better than consensus. The outperformance wasn’t much, but nevertheless moved the 2Y UST yield higher by some 5bp and shaved off 4bp of cuts for 2024. Such a reaction really underlines the pessimistic positioning of markets and the expectation of an economy grinding to a halt.

In a broader sense, recent economic surprises have improved recently, yet the front end of the US Treasury curve continues to dive deeper into cuts. Of course, positive economic surprises are also more likely when consensus turns more pessimistic, but even then the latest data points are far from recessionary territory. A slowdown is still our baseline, but the sentiment in rates markets may see some recovery if the data doesn’t deteriorate as promptly as feared, potentially helping the back end of the curve retrace higher…

US economic surprises making a recovery

On TIPPING us to ‘flation oblivion and on name calling…

Yesterday’s US GDP revisions offered several lessons to investors. The tendency for many countries to revise economic activity frequently, significantly, and positively is a reminder that real-time data lacks precision and data dependency is not a proper policy framework. Someone should attempt to explain that to Federal Reserve Chair Powell. The 2022 “technical recession” (a media term, not an economist’s term) was predictably revised out of existence.

Positive revisions to the strength of the consumer and evidence of a large savings stockpile than previously estimated suggest today’s consumer spending data should continue to be healthy. Data revisions also suggested that profit-led inflation peaked in the second quarter (retailers’ profits as a share of their economic activity basically plateaued). The data yesterday and today are likely to scream “soft economic landing”…

Visitors to the United States are immediately confronted with an aggressive tipping culture. When paying for most personal services—e.g., taxis, restaurant meals, etc.—a tip is expected and often prompted. The rise of digital payment platforms is giving greater control over tips to the seller.

Paying digitally, customers are often nudged to tip with three “suggested” tip amounts. This triggers two behavioural economic responses. There is herd mentality, whereby people think, “If everyone else is tipping, I should too.” More people tip when paying digitally. There is also a middle option bias, where if presented with choices, consumers will tend to avoid extremes and choose the middle option.

So if the suggested tips are 10%, 15%, and 20%, customers will more likely tip 15%. But if the suggestions switch to 15%, 20%, and 25%, customers are then more likely to tip 20%, which is effectively a 5% cost increase. Critically, there has not been a 5% price increase, and voluntary gratuities are not included in inflation.

There is evidence that suggested tip ranges may indeed have risen, creating a hidden inflation. However, companies that try paying their staff a fair wage by raising prices and banning tips find that customers are unhappy. People simply prefer the deception of a lower price and a rising gratuity.

Adorable … goods …

Wells Fargo: Durable Goods: When Doing Nothing is Really Something

Summary Despite an upwardly revised surge in July durable goods orders, the payback decline that had been feared did not materialize in August with durable goods orders technically positive, but essentially flat. Excluding transport categories, durables orders had their best month of the year.

… ‘bout that there GDP report from the good Dr Bond Vigilante …

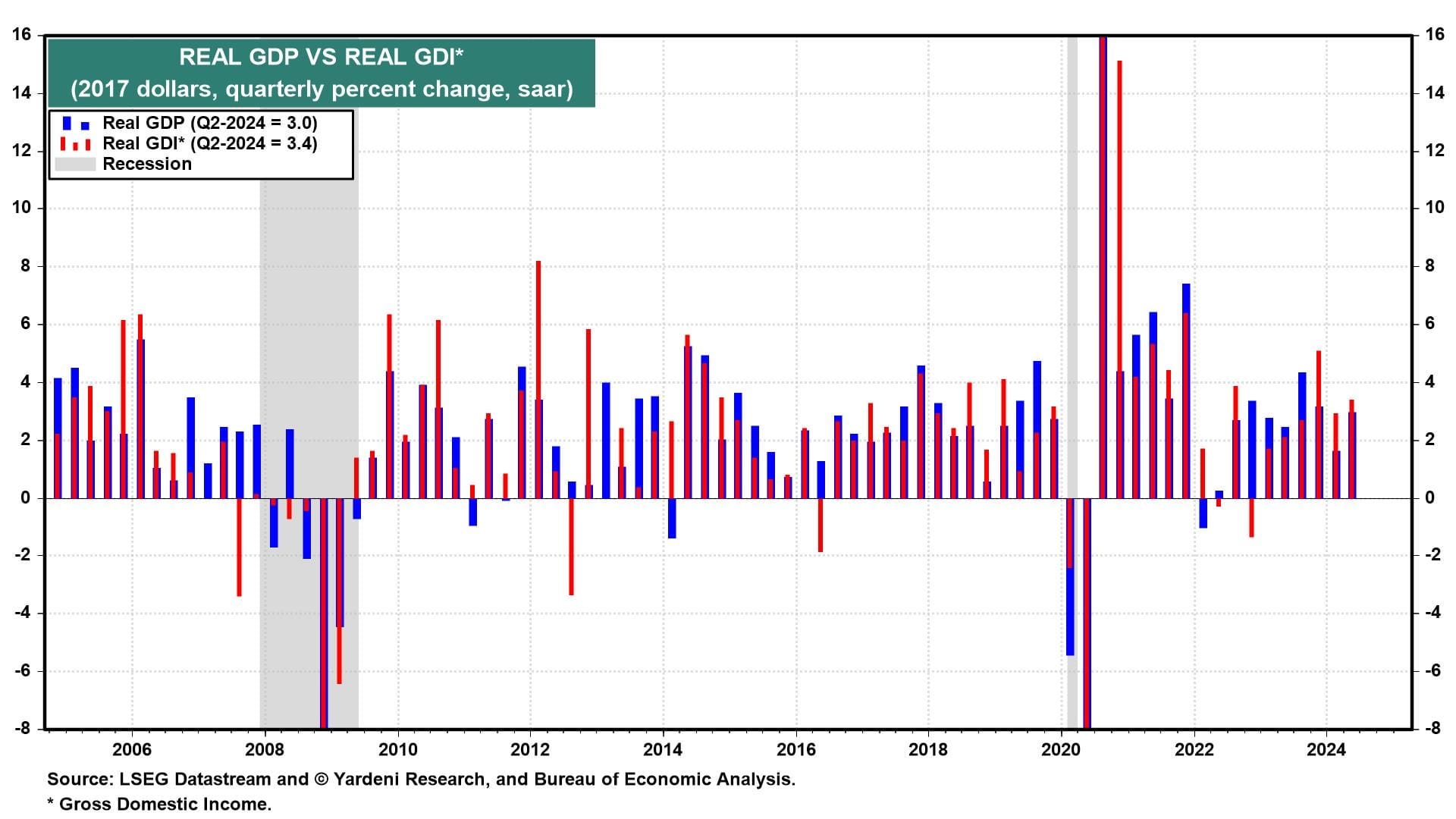

Yardeni: Revisions Show US Economy Is Still Flying High

…The previous estimate of Q2 real GDP showed it rose 3.0% (saar), while real GDI increased by 1.3%. That created the largest gap between the two since 1993. The BEA's final estimate of Q2 real GDI raised it to 3.4%. GDI was also revised higher in Q1, from 1.3% to 3.0% (chart). Real GDP growth remained at 3.0% during Q2 and was revised up slightly to 1.6% in Q1.

Furthermore, the technical recession from two-straight quarters of negative real GDP growth in H1-2022 was revised away as well.

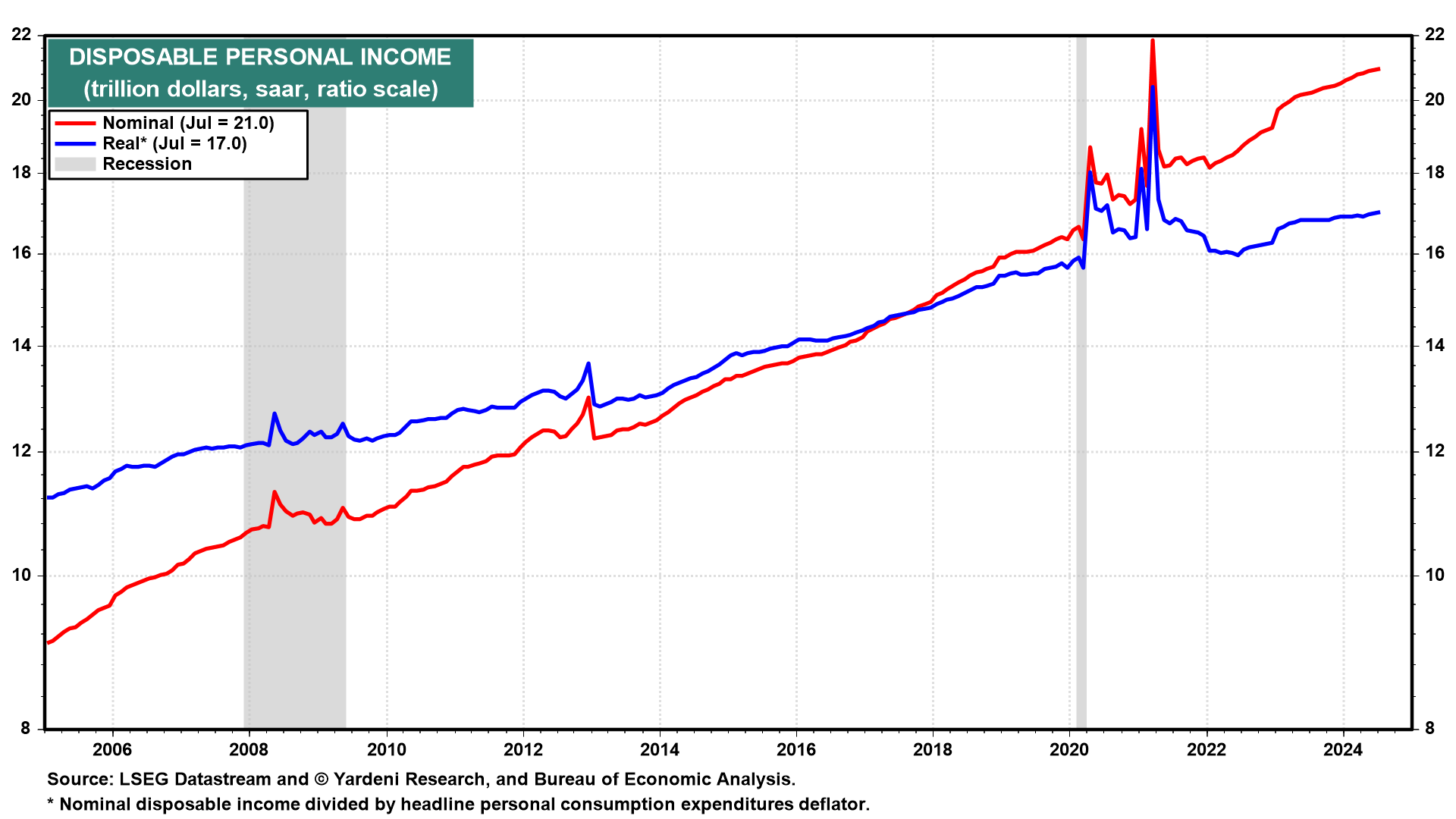

(2) Wages & salaries. Much of the increase in GDI was due to increased worker compensation. Real disposable personal income growth was raised from 1.0% to 2.4% (chart).

… these NOT the same revisions showing jobs were actually NOT created? askin’ for a friend…

… And from Global Wall Street inbox TO the WWW,

STOCKS and earnings …

Investing.com: S&P 500: Dip-Buying Remains the Go-To Strategy If Next Resistance Proves Stubborn

The S&P 500 and Nasdaq are set for potential breakouts amid strong gains.

Key levels suggest pullbacks may provide re-entry points.

Traders should watch for opportunities as indexes near resistance.

… Importantly, recent economic data shows no signs of a looming recession, suggesting these rate cuts aren’t a rescue attempt but rather a calculated move to stimulate growth.

The People's Bank of China also contributed to the positive sentiment by cutting interest rates, unlocking over $140 billion in lending capacity to help achieve its 5% growth target for the year.

…S&P 500: Pullback in the Offing?

The S&P 500 has been a beacon of strength, recently pushing past its previous all-time highs.

This breakout signals robust market demand, driven largely by expectations of further rate cuts and favorable economic conditions.

From a technical perspective, this move has firmly established 5,720 points as a critical support level.

If the current pullback extends, this zone may act as the first line of defense for the bulls, offering an opportunity for traders to re-enter the market.

Beyond 5,720 points, a deeper correction could target the 5,660 level, where the upward trendline intersects…

… finally, while everything is bigger in Texas, last night here at the Meadowlands, a summary of dem Boys vs Giants:

Why is it that real time data, such as Voting Results, or Econ Data, with all our current high tech gadgetry, ain't what it once was I wonders....